DHAHRAN — Brent crude surged 4.22 percent on Friday to settle at $112.57 per barrel, its highest close since July 2022, while West Texas Intermediate briefly touched $100.04 intraday, as Israel’s strikes on two Iranian nuclear facilities, a Houthi threat to close the Bab al-Mandeb strait, and the deployment of 82nd Airborne elements to the Gulf combined to price nine more days of uncertainty into every barrel leaving the ground.

For Saudi Arabia, the number contains a paradox that no treasury spreadsheet can resolve. At current prices the Kingdom is earning roughly $119 million per day above its pre-war revenue baseline, according to calculations based on Aramco’s disclosed production and the differential between today’s Brent price and the $76–$77 range that prevailed in late February. Yet the infrastructure that produces and ships that oil is degrading by the week: Ras Tanura, the world’s largest crude-export terminal, has been offline since an Iranian drone strike on March 2; four supergiant offshore fields have been shuttered on safety grounds; and the Strait of Hormuz, through which roughly 20 percent of global oil once flowed, is operating at less than 10 percent of pre-conflict capacity, according to the International Energy Agency.

Table of Contents

- Anatomy of the $112 Barrel

- The Revenue Paradox: Richer on Paper, Poorer in Capacity

- Can Saudi Oil Escape Two Chokepoints at Once?

- Iran’s Yuan Toll Booth and the Two-Tier Market

- What Happens When Trump’s April 6 Deadline Arrives?

- The Reconstruction Bill Nobody Is Discussing

- Background: From $77 to $112 in 28 Days

- Frequently Asked Questions

Anatomy of the $112 Barrel

Friday’s close did not arrive in a vacuum. Three separate escalatory events converged within a 36-hour window to push crude past the $110 threshold that traders had treated as a psychological ceiling since the war began on February 28.

First, Israel struck two Iranian nuclear sites on Thursday — the Khondab Heavy Water Complex and a yellowcake production plant in Yazd province — prompting Tehran to vow that retaliation “will no longer be an eye for an eye,” according to Al Jazeera. Second, the Pentagon confirmed elements of the 82nd Airborne Division, including the division headquarters and the 1st Brigade Combat Team, were deploying to the Gulf after an Iranian missile and drone attack on Prince Sultan Air Base wounded 10 American troops and damaged multiple aircraft, according to Military Times. Third, a senior Houthi military spokesman declared that “our fingers are on the trigger for direct military intervention” and that closing the Bab al-Mandeb strait remained a “primary option,” according to The National.

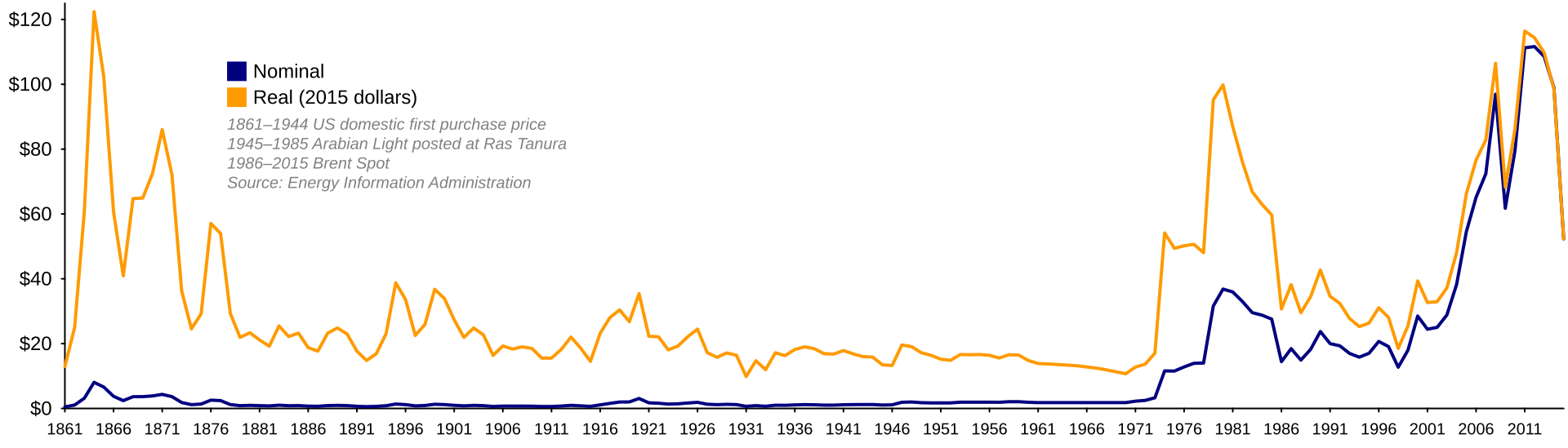

Goldman Sachs estimates that $14 to $18 of the current Brent price constitutes a geopolitical “war risk premium” — money that traders are paying not for oil in a tanker but for the probability that the next tanker may never arrive. In a March 22 note, the bank warned that “Brent is likely to exceed its 2008 all-time high if depressed flows keep the market focused on the risk of lengthier disruptions.” That all-time high was $147.50.

The broader numbers tell a blunt story. Brent has risen 36 percent from February 27 through March 27, according to CNBC. The Dubai benchmark, which tracks physical delivery from Middle Eastern sellers and therefore captures the real cost of getting crude out of the Gulf, has risen 76 percent to $126 per barrel, according to Kpler.

| Benchmark | Pre-War (Feb. 27) | March 28 Close | Change |

|---|---|---|---|

| Brent Crude | $76.80 | $112.57 | +46.6% |

| WTI | $71.65 | $99.64 | +39.1% |

| Dubai (Physical) | ~$71.60 | $126.00 | +76.0% |

| Goldman Sachs Risk Premium | — | $14–$18/bbl | — |

The gap between Brent and the Dubai physical benchmark is itself a signal. It means that actually procuring a barrel of Gulf-origin crude — arranging the tanker, securing insurance, navigating the Hormuz corridor or rerouting around the Cape of Good Hope — costs substantially more than the futures contract implies. That gap is where Saudi Arabia’s paradox lives.

The Revenue Paradox: Richer on Paper, Poorer in Capacity

Saudi Arabia entered the war producing approximately 10.1 million barrels per day, according to OPEC+ data from February 2026. At pre-war Brent prices of roughly $77 per barrel, that translated to approximately $778 million in daily gross revenue. At $112.57, the same volume would yield $1.137 billion per day — a windfall of $359 million.

But Saudi Arabia is not producing the same volume. Aramco has shut four supergiant offshore oil fields in the Persian Gulf on safety grounds after repeated Iranian missile and drone strikes on Gulf infrastructure. Ras Tanura, which processes 550,000 barrels per day and serves as the Kingdom’s primary eastern export terminal, has been offline since the March 2 drone strike that forced an emergency shutdown, according to Bloomberg.

Aramco has rerouted significant crude volumes westward through the 1,200-kilometre East-West Pipeline to the Red Sea port of Yanbu. But Yanbu lacks the loading capacity of Ras Tanura, and the pipeline itself has finite throughput. The Middle East Insider reported in March that even with the reroute, Saudi Arabia’s realized export volumes have fallen substantially from pre-war levels.

The $119 million daily windfall figure cited by analysts accounts for this reduced volume: it compares what Saudi Arabia is actually earning on the barrels it can ship at $112 versus what it would have earned on the same reduced volume at pre-war prices. The number is real, but it obscures the counterfactual — what the Kingdom would be earning if it could produce and ship at full capacity in a $112 market.

“The price of oil depends on regional security, and you are the main source of insecurity in the region. Expect oil at $200 per barrel.”

— Islamic Revolutionary Guard Corps spokesperson, March 11, as quoted by Al Jazeera

The Saudi Central Bank (SAMA) reported foreign reserve assets of SR 1.78 trillion ($475 billion) in January 2026, a six-year high, with net foreign assets rising 10 percent year-on-year through February, according to Arab News. The treasury is flush. But the assets that fill it are burning.

Can Saudi Oil Escape Two Chokepoints at Once?

The arithmetic of Saudi oil exports now depends on geography in a way it has not since the Tanker War of the 1980s. Two of the world’s most critical maritime chokepoints are simultaneously under threat.

The Strait of Hormuz, through which roughly 17.8 million barrels per day transited before the war, is operating at a fraction of normal capacity. The IEA’s March Oil Market Report stated that export volumes of crude and refined products through the strait are “currently at less than 10 percent of pre-conflict levels.” Iran’s IRGC has declared that “not a litre of oil” will pass through for vessels linked to the United States, Israel, or their allies, according to Al Jazeera.

The alternative route — shipping crude from Yanbu through the Red Sea and the Bab al-Mandeb strait — is now under a second threat. The Houthis have threatened to close the Bab al-Mandeb, and daily transits through the narrow waterway between Yemen and Djibouti have halved from roughly 60 to 28, according to Lloyd’s List data. A full closure would create what the Sunday Guardian called a “double chokepoint” scenario, potentially disrupting 30 percent of the world’s seaborne oil.

Al Jazeera reported on March 27 that Saudi Arabia, the UAE, and Iraq are exploring whether three existing pipelines could help oil bypass Hormuz entirely. The options include the Saudi East-West Pipeline to Yanbu, the UAE’s Habshan-Fujairah pipeline to the Gulf of Oman, and Iraq’s Basra-Ceyhan pipeline through Turkey. Combined, these pipelines have a theoretical capacity of approximately 8 million barrels per day — less than half of what Hormuz carried before the war.

Iran’s Yuan Toll Booth and the Two-Tier Market

Iran’s Hormuz strategy has produced a market distortion with no modern precedent. The IRGC has established what traders now call the “Tehran toll booth” — a single designated corridor near Larak Island through which vetted vessels can transit under Iranian naval escort, according to earlier reporting.

Between March 13 and March 25, a total of 26 vetted vessels were tracked on this escorted route using Automatic Identification System data, according to Lloyd’s. At least two of those vessels paid transit fees in yuan, China’s currency, and the Financial Times reported that Iran’s parliament is seeking to formalize a toll-collection law for the waterway.

The result is a two-tier oil market. Chinese-flagged vessels transit with relative ease; others pay $2 million or more per transit or reroute around the Cape of Good Hope, adding roughly two weeks and millions of dollars in fuel and insurance costs to every voyage. An Iranian lawmaker confirmed the $2 million fee to state media, as reported by NBC News.

This arrangement benefits Beijing, which secures discounted Gulf crude while competitors pay a war premium. It benefits Tehran, which collects hard-currency revenue in a sanctions environment. And it punishes Saudi Arabia, whose oil reaches non-Chinese buyers at an inflated cost that compresses the Kingdom’s competitive advantage against rival suppliers in the Atlantic Basin.

What Happens When Trump’s April 6 Deadline Arrives?

Markets are now pricing in a specific date: April 6, 2026, at 8:00 p.m. Eastern Time. That is the deadline President Trump set on March 26 for Iran to reopen the Strait of Hormuz, threatening to destroy Iran’s energy infrastructure “starting with the biggest one first” if Tehran fails to comply, according to NPR.

The deadline has already been extended twice. Trump initially gave Iran 48 hours on March 21, then pushed the deadline back by 10 days, writing on Truth Social that the extension came “as per Iranian Government request,” according to Euronews. Iran has publicly denied making any such request and denied that it is in direct talks with Washington.

Secretary of State Marco Rubio told G7 foreign ministers in France on March 27 that the war would continue for “two to four more weeks,” according to Axios, citing three sources with direct knowledge of the meeting. In a subsequent press gaggle, Rubio said the U.S. expects the conflict to end within “weeks and not months.”

For oil markets, Rubio’s timeline creates a specific pricing problem. If traders take the two-to-four-week estimate at face value, they must price in sustained conflict through mid-to-late April. If the April 6 deadline passes without resolution — or triggers further escalation — the Goldman Sachs warning about Brent exceeding its 2008 all-time high of $147.50 becomes a plausible near-term scenario rather than a tail risk.

The 400-million-barrel strategic petroleum reserve release coordinated by the IEA on March 11, the largest in the agency’s history, has done little to arrest the price climb. CNBC reported on March 14 that crude surged 17 percent in the three days after the release announcement, and the U.S. contribution of 172 million barrels — releasing roughly 1.4 million barrels per day over 120 days — covers only 15 percent of the supply lost due to the Hormuz closure.

The Reconstruction Bill Nobody Is Discussing

Every day that Ras Tanura remains offline is a day that its processing capacity sits idle, its desalination plants corrode in the Gulf humidity, and its loading berths — designed to handle Very Large Crude Carriers — degrade from disuse. Satellite imagery published by India TV News in early March showed fire damage to the facility’s tank farm and crude distillation units.

Aramco has not disclosed a reconstruction timeline. The 2019 Abqaiq-Khurais attack, which temporarily knocked out 5.7 million barrels per day of Saudi production, took weeks to repair even with comparatively limited damage. The current conflict has struck a broader array of facilities, and unlike 2019, the threat environment remains active.

The one-month balance sheet for Saudi Arabia published by this site estimated that infrastructure damage across the Eastern Province alone could run into the tens of billions of dollars. That figure does not account for the opportunity cost of lost production during reconstruction or the capital expenditure required to harden facilities against future strikes.

This creates the core tension in Riyadh’s war calculus. As earlier analysis noted, Saudi Arabia’s post-war competitive position depends on how much capacity survives the conflict.

A quick war preserves infrastructure but deflates the price premium. A long war maximizes per-barrel revenue but destroys the physical capacity to capitalize on post-war demand. The $119 million daily windfall is real, but it accrues on a shrinking asset base.

“Iran war threatens catastrophic consequences for the oil market.”

— Amin Nasser, Saudi Aramco CEO, March 10, as quoted by CNBC

Aramco CEO Amin Nasser made this warning during the company’s 2025 earnings call, where the company reported full-year net income of $104.7 billion. The stock has rallied on the price surge, but the physical assets underpinning that valuation are under sustained attack.

Background: From $77 to $112 in 28 Days

Brent crude was trading at approximately $76.80 per barrel on February 27, 2026, the day before the U.S. and Israel launched strikes against Iran. Within the first week, prices surged past $85 as Ras Tanura went offline and Iran began restricting Hormuz traffic. By March 8, Brent breached $100 for the first time in nearly four years, according to CNBC.

Prices briefly touched $120 in early March before Trump floated the idea of taking over the Strait of Hormuz, causing a temporary pullback. On March 23, Brent crashed 13 percent in a single session after Trump announced a pause in military operations, the largest single-day drop since the war began. That pause proved short-lived; within 48 hours Israel resumed strikes and Iran retaliated against Prince Sultan Air Base.

The price has since recovered and surpassed pre-crash highs. The trajectory — shock, partial recovery, policy-driven crash, rapid rebound to new highs — mirrors the pattern seen in the early months of Russia’s invasion of Ukraine in 2022, when Brent last traded at these levels. The difference is that the Hormuz disruption affects a substantially larger volume of global supply than the Russian sanctions did.

The IEA’s March Oil Market Report described the current disruption as “the largest in the history of the global oil market,” noting that the oil shortfall of roughly 10 million barrels per day is comparable in scale to the demand destruction during the worst of the COVID-19 pandemic — except this time it is supply, not demand, that has collapsed.

Frequently Asked Questions

How does the current oil price compare to the 2022 Ukraine-driven spike?

Brent crude peaked at $139.13 per barrel in March 2022 following Russia’s invasion of Ukraine, according to EIA data. The current price of $112.57 is below that peak but has risen faster — 36 percent in 28 days versus 40 percent over roughly six weeks in early 2022. The key difference is structural: the Ukraine crisis primarily disrupted Russian exports through sanctions, while the Hormuz closure physically blocks a corridor that carried 17.8 million barrels per day.

What happens to U.S. gasoline prices if Brent stays above $110?

The EIA’s Short-Term Energy Outlook projects that sustained Brent prices above $110 would push the U.S. national average for regular gasoline above $4.50 per gallon by mid-April, up from $3.89 in early March. The political consequences are significant: Trump has repeatedly linked his energy policy to lowering consumer prices, and sustained $4-plus gasoline heading into the midterm campaign season creates domestic pressure to resolve the conflict.

Could OPEC+ increase production to offset the Hormuz losses?

OPEC+ agreed to increase output by 206,000 barrels per day beginning in April, bringing Saudi Arabia’s target to 10.2 million barrels per day, according to the group’s most recent communique. But this is marginal. The Hormuz closure has removed roughly 10 million barrels per day from accessible supply, according to the IEA.

Non-Gulf OPEC+ members — primarily those in West Africa and Latin America — lack the spare capacity to replace Gulf production. The Dallas Federal Reserve noted in a March 20 analysis that “no combination of strategic releases, OPEC+ adjustments, or pipeline reroutes can fully compensate for a sustained Hormuz closure.”

Is China benefiting from Iran’s Hormuz toll system?

Chinese-flagged tankers have been among the primary beneficiaries of the IRGC’s selective transit system. Lloyd’s data shows that a substantial share of vessels cleared for escorted Hormuz transit in mid-March were Chinese-linked. China’s alternate payment system, CIPS, has seen record-high transaction volumes in March, consistent with reports of yuan-denominated toll payments, as reported by Fortune. Beijing is effectively securing Gulf crude at a discount while competitors pay higher freight, insurance, and rerouting costs.

When could Ras Tanura resume operations?

Industry analysts cited by Bloomberg estimate that full restoration could take 12 to 18 months after hostilities cease, at a cost of several billion dollars. For comparison, the 2019 Abqaiq-Khurais attack saw partial production restored within two weeks, but full restoration took months — and that damage was more concentrated. The critical variable now is that Ras Tanura sits within range of ongoing Iranian strikes, meaning repair crews cannot work safely until a ceasefire holds.