DHAHRAN — Hours after Iran’s Supreme National Security Council announced it would honor a ceasefire, an IRGC drone struck a pumping station on Saudi Arabia’s East-West Pipeline — the 1,200-kilometer bypass corridor that had become the kingdom’s sole credible alternative to the Strait of Hormuz, and that had reached its full 7 million barrel-per-day capacity for the first time in history barely eleven days earlier. The strike did not merely damage infrastructure; it collapsed the financial and strategic logic on which Mohammed bin Salman’s entire wartime export strategy, his May pricing, and his post-war fiscal architecture all simultaneously depended.

Brent crude had already cratered from $109.27 to $91.70 on ceasefire hopes — the steepest single-session decline since the 1991 Gulf War — erasing the price assumption embedded in Aramco’s record May Official Selling Price of +$19.50 per barrel above the Oman/Dubai average. The East-West Pipeline was supposed to be the instrument that converted ceasefire into export recovery, the mechanism through which Saudi Arabia would pump its way out of a war that had already stripped 39% of its export volumes before April 8. Instead, the IRGC turned ceasefire day into an export-compression event: the pipeline compromised, Hormuz still throttled to 15-20 ships per day versus a pre-war 138, and the price at which MBS had locked Asian buyers into May contracts now sitting $17 above the benchmark those buyers would actually face.

Table of Contents

- The Strike That Followed the Ceasefire

- What Did the Pipeline Strike Mean for Saudi Export Capacity?

- The IRGC’s Two-Front Corridor Denial

- Why Does the Brent Crash Destroy Aramco’s May Pricing?

- The PIF’s Broken Assumptions

- A Ceasefire the IRGC May Not Have Intended to Honor

- Can Saudi Arabia Replace Hormuz Without the Pipeline?

- The Asian Buyer Trap

- From Pipeline to Balance Sheet: The Fiscal Cascade

- FAQ

The Strike That Followed the Ceasefire

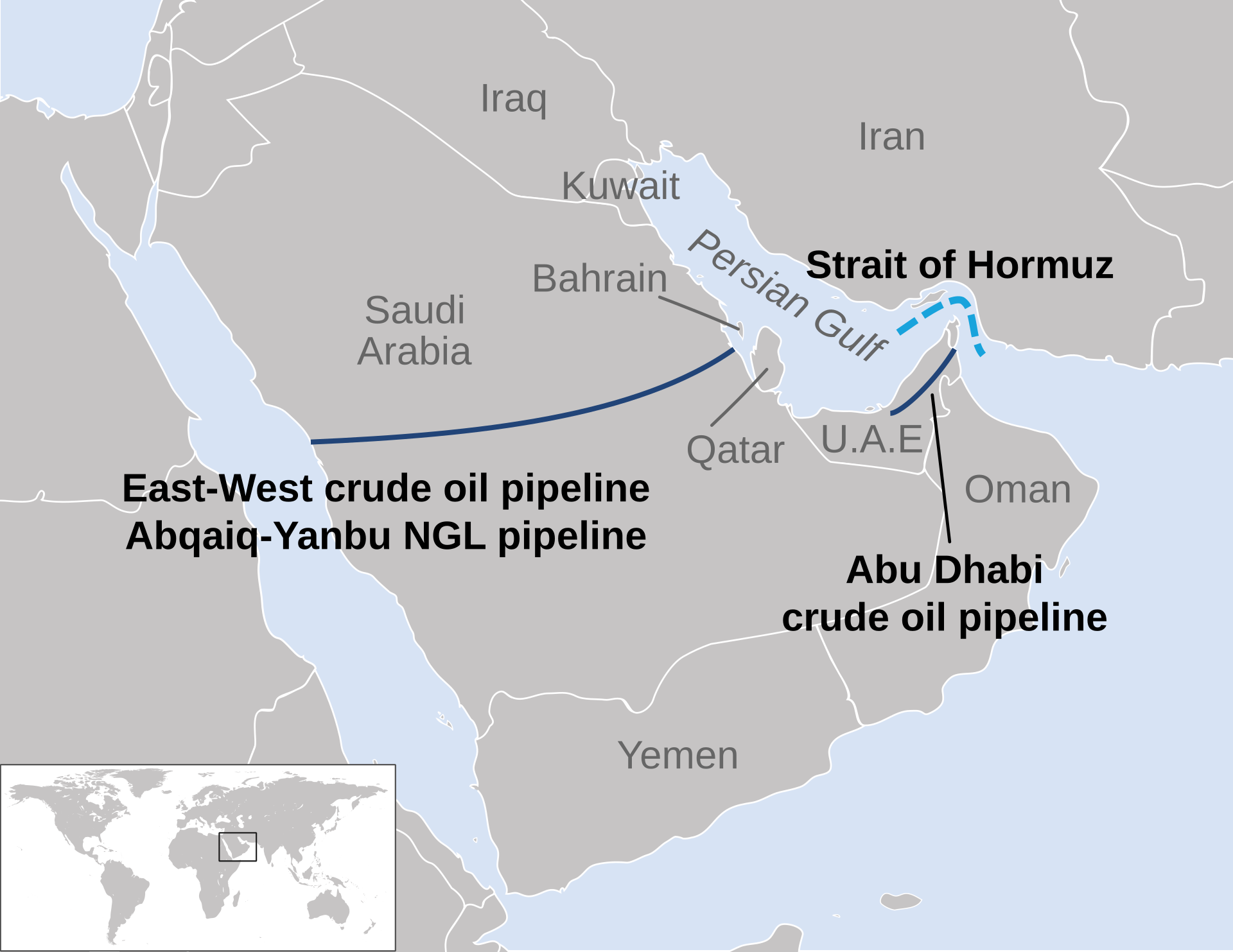

At approximately 1:00 p.m. local time on April 8, 2026, a drone struck a pumping station along Saudi Arabia’s East-West Pipeline — the Petroline system running from Abqaiq in the Eastern Province to Yanbu on the Red Sea coast. Bloomberg, citing Financial Times sources, reported the hit within hours. Aramco declined to comment, stating only that a damage assessment was underway. The pipeline has 13 pumping stations spread across the desert corridor, and the loss of output from even a single station can reduce throughput substantially, because each station maintains the pressure gradient that moves crude across the full 1,200-kilometer route.

The timing is the fact that matters most. Iran’s SNSC had formally accepted a ceasefire framework earlier that same day, and the White House had acknowledged that halt orders would “take time to reach lower ranks” of the IRGC’s decentralized command structure. But the pipeline strike landed not in a grey zone of ambiguous timing — it landed in broad daylight, hours after Tehran’s announcement, against a target that Iran’s own Fars News agency had pre-designated as a conditional response to American strikes on Iranian power plants and bridges. The IRGC’s Brigadier General Ebrahim Zolfaqari had declared the day before, on April 7, that “all considerations” of restraint toward regional American partners had been “removed” — a statement made before any ceasefire was announced, and one that no subsequent SNSC communique explicitly countermanded.

This was not the first time the East-West Pipeline served as an IRGC targeting template. In May 2019, IRGC-directed drones launched from Iraq struck the same pipeline system — an attack the Washington Institute later identified as a rehearsal for the far more devastating Abqaiq strike four months later. The 2019 hit was a proof of concept; the April 8, 2026 strike was its operational maturation, delivered with the additional flourish of landing on a ceasefire day that was supposed to mark the beginning of Saudi Arabia’s export recovery.

What Did the Pipeline Strike Mean for Saudi Export Capacity?

The strike degraded Saudi Arabia’s only high-capacity Hormuz bypass at the moment the kingdom needed it most. The pipeline had reached a record 7 million bpd just eleven days earlier, but Yanbu’s wartime loading capacity was capped at 3-4 million bpd (Vortexa), and the pumping station hit adds an upstream constraint to a system already bottlenecked at the terminus.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

That record was built on a wartime improvisation. The pipeline reached full 7 million bpd capacity around March 28, 2026, for the first time in its operational history — a feat accomplished by converting natural gas liquid pipelines to crude service beginning March 11, a conversion that Aramco engineered in under three weeks (Fortune, S&P Global). Of that 7 million bpd, approximately 2 million bpd was diverted to western Saudi refineries, leaving roughly 5 million bpd theoretically available for export through Yanbu. That theoretical number, however, already exceeded Yanbu’s actual wartime loading capacity, which Vortexa estimated at approximately 3 million bpd and market sources placed at a more generous 4 million bpd.

Even before the April 8 strike, Yanbu’s export performance was deteriorating. LSEG and Kpler data, reported through Baird Maritime, showed Yanbu exports dropping 15% week-on-week to 3.9 million bpd in the week of March 30, down from 4.6 million bpd the prior week. Saudi crude exports overall averaged just 4.355 million bpd in March 2026 (Kpler), compared to 7.1 million bpd in February 2026 — a 39% decline that predated the pipeline strike and reflected the combined effect of Hormuz closure, repeated strikes on Eastern Province infrastructure, and the SAMREF refinery hit at Yanbu around April 3 that had already compromised the Red Sea terminus before the pumping station was targeted.

| Metric | Pre-War (Feb 2026) | March 2026 Average | Post-Strike Estimate |

|---|---|---|---|

| Saudi crude exports (bpd) | 7.1M | 4.355M | Under assessment |

| East-West Pipeline throughput (bpd) | ~5M (partial) | 7M (full capacity March 28) | Degraded — extent unknown |

| Yanbu export loading (bpd) | ~2.5M | 3.9M (w/o March 30) | Constrained by pipeline + SAMREF |

| Hormuz daily transits | 138 ships/day | Effectively closed | 15-20 ships/day |

| Brent crude ($/bbl) | ~$82 | ~$109 | $91.70 (session low April 8) |

The pipeline strike does not need to have destroyed the pumping station outright to impose severe consequences. A single station offline forces the remaining twelve to compensate, reducing overall throughput capacity and increasing the mechanical stress on equipment already running at unprecedented utilization rates. Aramco’s silence — the company declined to comment entirely — suggests the damage assessment is either incomplete or unfavorable, because the standard corporate response to a contained incident is rapid reassurance, and no reassurance came.

The IRGC’s Two-Front Corridor Denial

The IRGC’s operational logic on April 8 was a simultaneous denial of both export corridors available to Saudi Arabia. Hormuz remained functionally throttled: despite the ceasefire announcement, only 15-20 ships transited the strait in the first 24 hours, compared to the pre-war baseline of 138 per day (Windward). Iran’s Foreign Minister Araghchi stated that Hormuz operations would require “coordination with Iranian armed forces,” and the SNSC’s own ceasefire text declared that negotiations constitute “a continuation of the battlefield.” Over 800 vessels remained trapped in or around the strait. The pipeline strike, landing on the same day, meant that neither corridor — the one Iran formally controlled through naval positioning nor the one Saudi Arabia had built specifically to avoid Iranian interdiction — was operating at anything close to capacity.

Fars News had laid the groundwork weeks earlier, explicitly naming the East-West Pipeline as a conditional target should the United States strike Iranian power plants or bridges — a condition that had been met when B-1 strikes hit the Karaj bridge on April 2 and multiple rounds of strikes destroyed over 140 installations across two Kharg Island campaigns. The IRGC was, in effect, executing a pre-announced strike against a pre-announced target, and doing so on the day that was supposed to mark the transition from war to negotiation. Whether the drone was launched before or after the halt order reached its operators is a question that matters legally but not strategically: the decentralized command structure of the IRGC, operating under Zolfaqari’s blanket authorization to remove “all restraint,” made the strike functionally inevitable regardless of what the SNSC announced from Tehran.

Why Does the Brent Crash Destroy Aramco’s May Pricing?

Aramco’s record May OSP of +$19.50/bbl above Oman/Dubai was calibrated at approximately $109 Brent, but the ceasefire crashed Brent to $91.70 — a 16% decline, the largest single session since 1991 (CNBC, Reuters). The premium is locked and non-renegotiable. Asian term buyers will pay wartime prices into a post-ceasefire market where the Brent benchmark has fallen roughly $17 from the level at which the OSP was set.

The May OSP represented a $17 jump from April and a record (Bloomberg). That premium was calibrated when Brent was trading around $109, reflecting war-driven scarcity that had compressed global supply by an estimated 6 million bpd (Kpler) and driven Asian buyers into a scramble for every available cargo. The editorial logic of the OSP at the time of its setting was that Aramco was actually leaving money on the table — Bloomberg’s implied equilibrium suggested a premium closer to $40 per barrel, meaning the $19.50 figure represented strategic restraint designed to preserve long-term buyer relationships.

The ceasefire collapsed that logic overnight. The May OSP, locked in and non-renegotiable for the month, now sits at a premium calibrated for a market that no longer exists. WTI’s parallel crash — from $112.95 to $95.85 — confirmed the scale of the price signal. Asian buyers who signed term contracts at +$19.50 above Oman/Dubai will pay that premium against a benchmark that has fallen roughly $17 from the assumption embedded in the pricing, creating an effective overpayment that makes Saudi crude less competitive than spot alternatives for the entire month of May.

This is not merely a pricing embarrassment — it is a volume risk. Asian buyers with contractual flexibility will defer or reduce liftings, opting for cheaper spot cargoes from producers who were not pricing for war. Buyers without flexibility will absorb the cost but register the lesson: Saudi term pricing, in a war environment, carries asymmetric downside that spot markets do not. Aramco’s market-share defense strategy, which had been the institutional logic behind the relatively modest December 2024 OSP cut, is now being undermined by a pricing decision made under conditions that evaporated within days of its announcement.

Regional American partners should know that, until now we have exercised significant restraint for the sake of good neighborliness and have taken precautions in selecting retaliatory targets, but from now on, all such considerations have been removed.

Brigadier General Ebrahim Zolfaqari, IRGC, April 7, 2026 — one day before the pipeline strike

The PIF’s Broken Assumptions

The Public Investment Fund’s 2026-2030 strategy document, published in early April, was already a document of managed retreat: The Line formally suspended at 2.4 kilometers of its planned 170, construction commitments slashed from $71 billion to $30 billion, Aramco’s dividend cut by roughly one-third, and the fund’s 2024 return effectively zero. The strategy rested on two compensating pillars — the East-West Pipeline delivering 7 million bpd to Yanbu as the Hormuz bypass, and Brent remaining above the $108-111 per barrel fiscal break-even that Bloomberg Economics calculated as the PIF-inclusive threshold for Saudi budgetary solvency.

Both pillars broke on April 8. The pipeline strike degraded the bypass corridor’s throughput at a moment when Yanbu exports were already declining, and the Brent crash dropped the kingdom below its PIF-inclusive fiscal break-even by at least $15 per barrel. Even if Brent stabilizes closer to $93 — the closing price after the initial panic subsided — Saudi Arabia faces a structural deficit that Goldman Sachs had already estimated at $80-90 billion for 2026 (6-6.6% of GDP, CNBC), nearly double the official projection of $44 billion. The PIF’s pivot to artificial intelligence — Humain, with $23 billion in partnerships across NVIDIA, AMD, AWS, Qualcomm, and Cisco — requires sustained capital deployment at a time when the fund’s primary revenue source (Aramco dividends) has been cut and the price of its primary commodity has fallen below the level needed to fund both government operations and the transformation program simultaneously.

The non-oil PMI reading of 48.8 — contraction territory — confirms that the war’s damage extends beyond the hydrocarbon sector. The PIF’s eight planned IPOs, designed as capital recycling mechanisms, will now price into a market where Saudi Arabia’s wartime economic resilience narrative has been punctured by simultaneous infrastructure compromise and price collapse. Gulf producers collectively have lost at least $15.1 billion in revenue since the war began, according to Kpler’s calculation of $1.2 billion per day in stranded Hormuz supply (OilPrice.com), and that figure does not account for the additional revenue compression from price declines that accelerated on April 8.

A Ceasefire the IRGC May Not Have Intended to Honor

The pipeline strike illuminates a problem that has defined this conflict since its earliest days: the gap between what Iran’s civilian government announces and what the IRGC’s operational commanders execute. The SNSC’s ceasefire acceptance and the drone strike on the East-West Pipeline pumping station occurred on the same day, issued from the same state apparatus that the SNSC’s own communique described as engaged in “negotiations” that constitute “a continuation of the battlefield.” The halt order’s reversibility architecture — Khamenei’s attributed statement that “this is not the end of the war, but all units must ceasefire” — was designed to preserve operational flexibility, and the pipeline strike demonstrated that flexibility in action within hours of its issuance.

Zolfaqari’s April 7 declaration that “all restraint” had been removed was not retracted, amended, or contradicted by the SNSC’s ceasefire text. Khamenei himself had been absent from public view for 39 days at the time of the ceasefire announcement, with the Times of London reporting a memo suggesting he was “unconscious in Qom.” The IRGC’s decentralized mosaic structure — 31 corps operating with substantial operational autonomy since a September 2008 reorganization — means that a halt order from the SNSC does not automatically translate into a stand-down at the tactical level, particularly for operations already in the launch sequence. The White House’s own acknowledgment that orders would “take time to reach lower ranks” effectively conceded this structural reality, though it did so in language that preserved diplomatic ambiguity about whether the strike represented defiance or delay.

For Saudi Arabia, the distinction is irrelevant. Whether the IRGC struck the pipeline because it chose to ignore the ceasefire or because the ceasefire order had not yet propagated through a command structure designed for autonomous action, the result is identical: the bypass corridor is compromised, the ceasefire’s economic dividend is nullified, and the kingdom’s ability to convert a diplomatic pause into an export recovery has been materially degraded on the first day of that pause.

Can Saudi Arabia Replace Hormuz Without the Pipeline?

No. All three bypass pipelines — Saudi East-West (7M bpd, now degraded), UAE ADCOP (1.5M bpd), and Iraq-Turkey (0.2M bpd) — sum to roughly 8.7 million bpd against the strait’s pre-war throughput of 20 million bpd (EIA). That gap exceeds 11 million bpd and cannot be closed by overland infrastructure alone.

Saudi Arabia’s pre-war share of Hormuz throughput alone was approximately 5.5 million bpd, or 38% of the strait’s total (EIA), and redirecting that volume through the East-West Pipeline to Yanbu was the kingdom’s entire wartime strategy. The missing 11-plus million bpd represents crude from Kuwait, Iraq’s southern fields, Qatar, and the UAE’s offshore production — output that has no overland route to market and depends entirely on maritime access through a strait where the IRGC still permits only 15-20 transits per day, a fraction that keeps global supply compressed even after ceasefire.

Even at full pre-strike throughput, Yanbu’s loading infrastructure could handle only 3-4 million bpd of actual exports (Vortexa and market sources) — a bottleneck that capped the pipeline’s practical value well below its 7 million bpd capacity. The April 8 strike adds a second constraint upstream of that bottleneck, compressing throughput before crude even reaches the Red Sea coast, and the SAMREF refinery strike around April 3 had already demonstrated that the Red Sea terminus itself was vulnerable to IRGC reach through what were likely Houthi-aligned assets in Yemen.

OPEC+ approved a modest +206,000 bpd output increase for May on April 5 (Middle East Insider), a decision that assumed the production would find a route to market. With the pipeline degraded and Hormuz at less than 15% of its pre-war transit rate, additional production authorizations become theoretical — barrels that are permitted but cannot physically reach buyers. The ceasefire, rather than unlocking export recovery, has produced a situation where production capacity, pipeline throughput, port loading, and maritime transit are all simultaneously constrained, each by a different mechanism and none by the same solution.

The Asian Buyer Trap

Asian refiners — particularly in China, India, South Korea, and Japan — now face an unprecedented pricing dislocation. They are contractually committed to May liftings at Aramco’s +$19.50 OSP premium, a price set when Brent sat near $109 and the war risk premium reflected genuine scarcity. That premium cannot be retroactively adjusted. These buyers will pay wartime prices for what they expect to be peacetime barrels — except the pipeline strike means the barrels themselves may not arrive on schedule, compounding a pricing penalty with a delivery risk that the contract terms were never designed to accommodate.

The trap is structural, not incidental. Aramco’s term contracts with Asian national oil companies represent the backbone of Saudi Arabia’s market-share strategy, and those contracts depend on a reliability premium — the implicit guarantee that Saudi crude will arrive predictably at a price that, while sometimes above spot, compensates through supply security. The April 8 convergence of inflated pricing and compromised delivery infrastructure inverts that value proposition entirely: buyers are paying a premium for security that the IRGC has just demonstrated it can revoke with a single drone. The Indian market, where Saudi Arabia’s share had already declined from 16% to 11% amid competition and the reintroduction of Iranian crude under OFAC General License U, is particularly exposed. Indian refiners with spot flexibility — IOC, BPCL — will redirect purchases to cheaper alternatives, while captive term buyers absorb the loss and recalibrate their long-term Saudi exposure downward.

Negotiations are a continuation of the battlefield.

Iran Supreme National Security Council ceasefire communique, April 7-8, 2026

From Pipeline to Balance Sheet: The Fiscal Cascade

The pipeline strike’s financial consequences extend well beyond oil export revenue, cascading through an industrial and fiscal architecture that was already under severe stress. Sadara Chemical Company’s $3.7 billion debt, whose grace period expires on June 15, 2026, depends on feedstock flows from the Eastern Province petrochemical corridor — the same corridor that the East-West Pipeline serves and that has been under sustained IRGC attack since late March. SABIC’s force majeure declaration of March 26-27, the Jubail debris fire of April 7, and now the pipeline pumping station strike of April 8 represent an escalating pattern of industrial degradation that makes Sadara’s June debt service increasingly uncertain.

Saudi Arabia’s fiscal break-even, on the IMF’s central government measure, sits at $86.60 per barrel — a threshold that Brent still exceeds at $93. But the IMF measure excludes PIF capital expenditure, sovereign wealth fund deployment, and the off-balance-sheet commitments embedded in Vision 2030’s surviving projects (Expo 2030, FIFA 2034, the Humain AI platform). Bloomberg Economics’ PIF-inclusive break-even of $108-111 per barrel is the relevant number for understanding whether the kingdom can simultaneously service its transformation ambitions and its wartime expenditures, and at $93 Brent, it cannot. Goldman Sachs’ fiscal deficit estimate of $80-90 billion for 2026 — nearly double the official $44 billion projection — was calculated before the pipeline strike added a new variable to the export volume equation, and before the Brent crash reduced per-barrel revenue by approximately $17 from the level assumed in Aramco’s May pricing.

The revenue arithmetic is punishing at every level. Saudi Arabia’s March exports of 4.355 million bpd at approximately $109 per barrel generated roughly $475 million per day; the same volume at $93 Brent would yield $405 million — a $70 million daily reduction from price alone, before accounting for the volume compression the pipeline strike will impose. Over a month, the price decline alone represents approximately $2.1 billion in lost revenue against March benchmarks, and the volume decline — if the pipeline operates at even 80% of its pre-strike capacity — could add another $1-2 billion in foregone exports. Gulf producers collectively have lost at least $15.1 billion since the war began, measured in stranded Hormuz supply at $1.2 billion per day (Kpler/OilPrice.com); that figure does not yet incorporate the April 8 price collapse.

Saudi Arabia’s exclusion from the Islamabad bilateral negotiations, where Iran is negotiating the terms of Hormuz reopening without Saudi participation, means the kingdom cannot even influence the timeline on which its primary export corridor might return to full function. The ceasefire, far from providing fiscal relief, has created a worst-of-both-worlds scenario: the price declined as if peace had arrived, but the infrastructure damage continued as if war had not paused.

FAQ

How long could the East-West Pipeline pumping station take to repair?

Historical precedent from the May 2019 IRGC drone attack on the same pipeline system suggests repair timelines of days to weeks for a single pumping station, depending on whether the strike damaged the pumps, the control systems, or the pipeline casing itself. Aramco demonstrated rapid repair capability after the 2019 Abqaiq attack, restoring 5.7 million bpd of processing within approximately 10 days, but that repair was conducted in peacetime conditions without ongoing threat of follow-on strikes — a condition that does not apply in April 2026, when the IRGC has explicitly stated that “all restraint” has been removed and the pipeline’s 12 remaining stations present a target-rich environment for sustained interdiction.

Could Aramco adjust the May OSP retroactively for Asian buyers?

Aramco has never retroactively reduced a published OSP in the modern pricing era. The company could offer ad hoc discounts, cargo deferrals, or volume flexibility to preserve relationships with key buyers (particularly Chinese state refiners and Indian national oil companies), but any such accommodation would be bilateral and confidential rather than a formal OSP revision. The June OSP, expected in early May, will be the market’s first signal of whether Aramco is willing to absorb the pricing dislocation or will attempt to maintain elevated premiums despite the changed fundamentals — and that decision will reveal whether Riyadh prioritizes revenue maximization or market-share preservation in the post-ceasefire environment.

What does the pipeline strike mean for Phase 2 ceasefire negotiations?

Iran’s Phase 2 agenda — Hormuz governance and HEU caps — was already the harder negotiation. The pipeline strike on Phase 1’s first day demonstrates to every party at the table that the IRGC can compress Saudi export capacity independently of whatever diplomatic framework Tehran endorses. That reshapes Saudi Arabia’s Phase 2 bargaining position: Riyadh now negotiates not just for Hormuz reopening but for enforceable guarantees over a 1,200-kilometer overland corridor that Iran has proven it can reach. The 45-day Phase 1 window is also the window in which PAC-3 stockpiles — estimated at roughly 400 rounds remaining after intercepting 894 aerial threats since March 3 — may fall below minimum credible defense thresholds.

Is the Yanbu corridor still viable as a long-term Hormuz bypass?

The corridor remains physically intact — one pumping station strike does not sever a 1,200-kilometer pipeline with 13 stations — but the April 8 attack, combined with the SAMREF refinery strike around April 3, has demonstrated that the entire Yanbu route, from Eastern Province intake to Red Sea loading, falls within IRGC operational range. The Houthi-aligned threat from Yemen places the Yanbu terminus under a separate and independent interdiction envelope, meaning the pipeline must survive threats from both the Persian Gulf and the Red Sea simultaneously. Long-term viability depends less on repair timelines than on whether Saudi air defenses can sustain the coverage density required to protect 13 dispersed pumping stations across open desert while simultaneously defending Ras Tanura, Jubail, and Prince Sultan Air Base.

How exposed are China and India as term buyers?

China’s state refiners — Sinopec and PetroChina — hold the largest Saudi term volumes and have the least contractual flexibility to redirect purchases mid-month. India’s exposure is more differentiated: IOC and BPCL retain some spot-market flexibility and will face pressure from domestic pricing constraints to minimize overpayment, while Nayara Energy (Rosneft-affiliated) has been rerouting to Russian and Iranian alternatives. The May OSP dislocation arrives at the same moment that OFAC General License U has re-enabled Indian access to Iranian crude at a premium above Brent — creating a direct competitive wedge in the market Saudi Arabia most needs to hold.

The East-West Pipeline pumping station will be repaired — Aramco’s engineering capability is not in question, and a single station among thirteen can be restored. What cannot be restored is the assumption that the bypass corridor existed outside the war. MBS built his wartime export strategy, his May pricing, and his PIF restructuring on the premise that crude pumped west to Yanbu was crude that had escaped the conflict, crude that flowed through Saudi sovereign territory beyond Iranian reach, crude whose price could be set at wartime premiums because its delivery was guaranteed by geography rather than by the same military deterrence that had already failed to protect Ras Tanura, Jubail, and Prince Sultan Air Base. On April 8, a single drone — almost certainly costing less than the $3.9 million per PAC-3 interceptor that Saudi Arabia has been expending at the rate of hundreds per week — erased that premise, and with it the difference between a ceasefire that ends a war and a ceasefire that merely rearranges where the war’s costs accumulate.