DHAHRAN — Iran’s Parliament Speaker Mohammad Bagher Ghalibaf posted a question to X on April 4 that was not a question. “What share of global oil, LNG, wheat, rice, and fertilizer shipments transits the Bab-el-Mandeb Strait?” he wrote. “Which countries and companies account for the highest transit volumes through the strait?” The man asking already knows the answer. Ghalibaf commanded the IRGC Air Force from 1997 to 2000 — the years Iran’s ballistic missile architecture was being assembled — and holds a doctorate in political geography. He is a brigadier general who became a politician, not the reverse.

His post arrived less than 24 hours after an Iranian Shahed-type drone struck the SAMREF refinery at Yanbu, Saudi Aramco’s Red Sea export hub. The timing frames a specific threat: Saudi Arabia spent four decades and billions of dollars building the East-West Pipeline to survive a Hormuz closure, and in March 2026, Yanbu loaded a record 3.23 million barrels per day — crude that overwhelmingly exits the Red Sea through the same Bab el-Mandeb strait Ghalibaf was publicly cataloguing.

Table of Contents

- The Man Behind the Post

- Why Does the East-West Pipeline Feed Directly Into Bab el-Mandeb?

- The April 3–4 Sequence

- Yanbu at the Ceiling

- What Happens if Both Hormuz and Bab el-Mandeb Close?

- Can the Houthis Actually Close Bab el-Mandeb?

- The Insurance Market Will Decide Before the Navy Does

- Saudi Arabia’s Western Flank

- How Did Saudi Arabia Trade One Chokepoint for Another?

- Frequently Asked Questions

The Man Behind the Post

Western media identified Ghalibaf as “Iran’s Parliament Speaker” in their coverage of the April 4 post. The label is accurate and incomplete. Mohammad Bagher Ghalibaf joined the Islamic Revolutionary Guard Corps in 1980 at age eighteen, during the first months of the Iran-Iraq War. By 1997, he had risen to command the IRGC Air Force — the institutional ancestor of what is now the IRGC Aerospace Force, the branch responsible for Iran’s entire ballistic and cruise missile inventory.

His three-year tenure at the IRGC Air Force, from 1997 to 2000, coincided with the period when Iran was converting its scattered missile experiments into an organized production capability. The Shahab-3 medium-range ballistic missile — the backbone of Iran’s deterrent architecture for a generation — entered testing in 1998 and initial operational service in 2003. Ghalibaf was not merely adjacent to this work. He ran the organization doing it.

After the military career came Tehran’s mayoralty, two presidential campaigns, and in 2024, the speakership of the Majlis. But his doctorate in political geography from Tarbiat Modares University is the detail that explains the April 4 post’s phrasing. The post did not threaten. It enumerated: oil, LNG, wheat, rice, fertilizer. It asked which countries and companies have the highest exposure. That is the language of targeting — identifying what passes through a kill zone, and who bears the cost when passage stops.

No competing outlet covering the post identified Ghalibaf’s IRGC Air Force command during the missile program’s formative years. NBC News and the United Against Nuclear Iran database document the biography. The connection between his formative career in IRGC missile development and the April 4 post’s precise, commodity-by-commodity enumeration is one that his résumé, read in full, makes clear.

Why Does the East-West Pipeline Feed Directly Into Bab el-Mandeb?

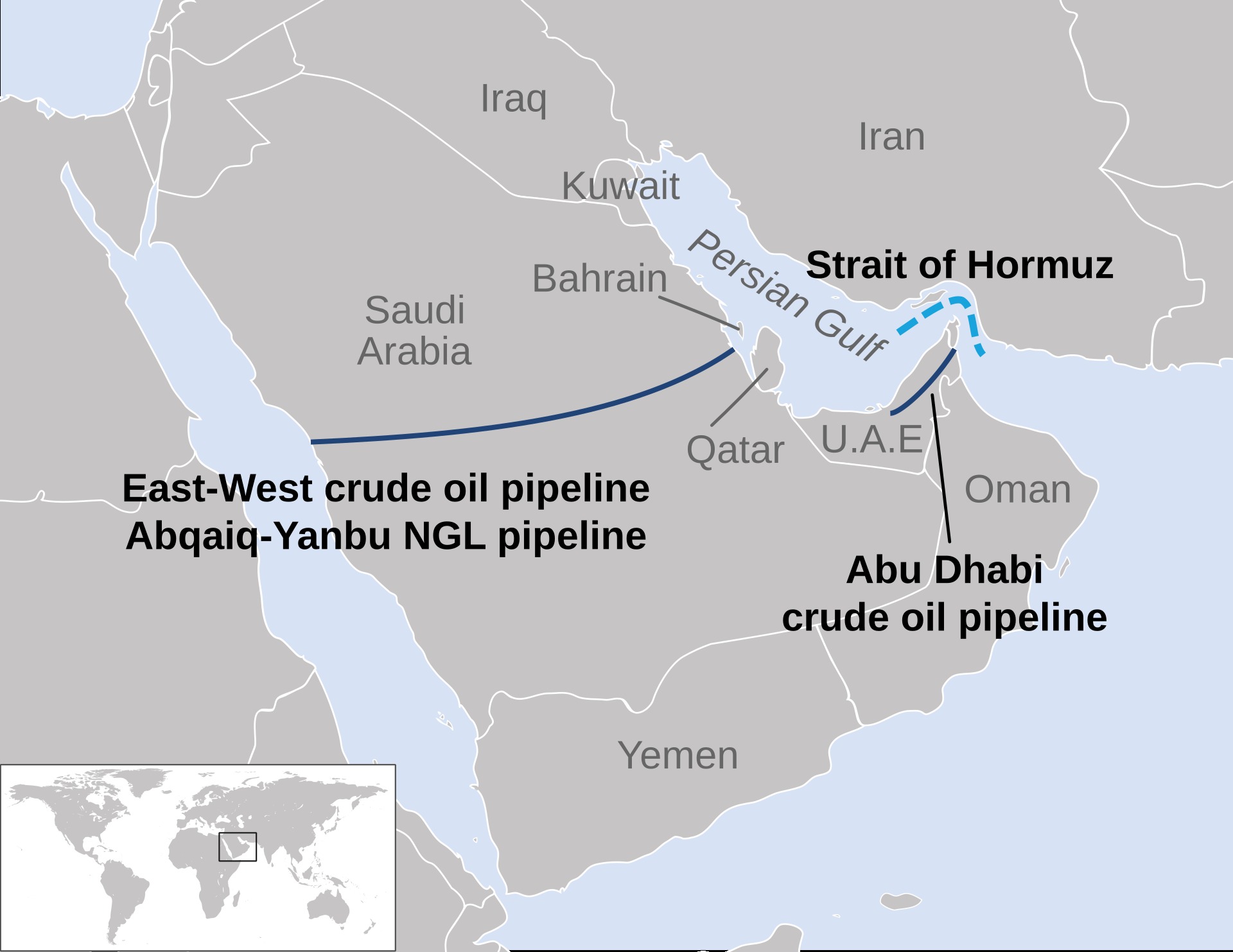

Because the pipeline was designed to avoid Hormuz — not the entire threat environment. Built after the 1979 Iranian Revolution to carry Saudi crude from the Eastern Province to the Red Sea, it deposits oil at Yanbu, where tankers must then transit the Bab el-Mandeb strait to reach Europe and Asia. One chokepoint was replaced with another.

The answer is forty-five years old. In 1979, the Iranian Revolution installed a government in Tehran that immediately became hostile to Saudi oil shipments through the Strait of Hormuz. In 1981, Riyadh began construction of a 1,200-kilometer pipeline from Abqaiq — the processing hub in the Eastern Province — across the Arabian Peninsula to the Red Sea port of Yanbu. The pipeline was built to do one thing: move Saudi crude to market without passing through waters that Iran could close.

The original line carried 5 million barrels per day. After the September 2019 Houthi drone and cruise missile strikes on Abqaiq — an attack that temporarily knocked out half of Saudi production — Aramco expanded the system. A converted 48-inch NGL line was added to the network, pushing combined emergency capacity to 7 million barrels per day. Saudi Aramco’s CEO confirmed in March 2026 that the pipeline has reached that ceiling.

The pipeline works. In March 2026, Yanbu loaded 3.23 million barrels per day, according to Kpler tanker-tracking data — a fourfold increase over the pre-war typical volume of 750,000 to 850,000 barrels per day. The Hormuz-to-Yanbu reroute has been the single most consequential piece of energy infrastructure in the current war.

But nearly 90% of crude loaded at Yanbu goes onto Very Large Crude Carriers that cannot transit the Suez Canal fully laden. Those VLCCs head south, through the Red Sea, and out through the Bab el-Mandeb strait — the 30-kilometer-wide passage between Yemen and Djibouti. Ghalibaf’s question about “what transits Bab el-Mandeb” was a question about where Saudi oil goes after the pipeline ends.

The April 3–4 Sequence

On April 3, Day 34 of the Iran-Saudi war, an Iranian Shahed-type drone struck the SAMREF refinery at Yanbu. SAMREF is a joint venture between Saudi Aramco and ExxonMobil with a processing capacity of 400,000 barrels per day. A Greek-operated PAC-3 Patriot battery — part of the bilateral air defense arrangement between Athens and Riyadh — intercepted two ballistic missiles launched in coordination with the drone. The Patriot is optimized for high-altitude ballistic threats. The low-altitude, low-radar-cross-section Shahed got through.

The strike demonstrated something specific: Yanbu’s air defenses have a gap at the bottom of the threat envelope. Then, less than 24 hours later, Ghalibaf published his Bab el-Mandeb post. The sequencing — a physical test of Yanbu’s defenses on Day 34, followed by a public cataloguing of what flows through the Red Sea chokepoint on Day 35 — is either coordination or a coincidence that every outlet covering the story has treated as a coincidence.

Iranian state media suggests coordination. PressTV, on March 30, had already published an article framing “Bab el-Mandeb joining Hormuz as pillars of global economic power.” On April 3 — the same day as the SAMREF strike — PressTV ran a second piece detailing Ansarullah’s formal position that Bab el-Mandeb closure was among its primary steps “in support of Iran.” Ghalibaf’s April 4 post then provided the public-facing signal from Tehran’s civilian leadership. The chronology reads like a three-beat messaging operation: frame, demonstrate, signal.

Yanbu at the Ceiling

The March 2026 loading data from Kpler tells a story that the pipeline’s supporters would prefer to keep quiet. Yanbu loaded 3.23 million barrels per day — a record. But the terminal’s nominal loading ceiling is approximately 4 to 4.5 million barrels per day, and Vortexa, the commodity analytics firm, has estimated the wartime operationally tested throughput at approximately 3 million barrels per day. At 3.23 million, Yanbu is already operating above what analysts considered its practical limit.

The gap between Yanbu’s output and what was lost at Hormuz remains enormous. Matt Smith, Kpler’s lead oil analyst, told ABC News that the world is “short of about 13 million barrels of oil per day that once came through the Strait of Hormuz.” The pipeline, at its absolute ceiling of 7 million barrels per day of throughput, cannot make up the difference — and even that throughput number is the pipeline’s capacity, not the terminal’s. The terminal is the bottleneck.

| Metric | Figure | Source |

|---|---|---|

| East-West Pipeline maximum capacity | 7 million bpd | Saudi Aramco CEO confirmation |

| Yanbu nominal loading ceiling | 4–4.5 million bpd | Argus Media |

| Yanbu wartime operational ceiling (tested) | ~3 million bpd | Vortexa |

| Yanbu actual loading, March 2026 | 3.23 million bpd | Kpler |

| Yanbu typical pre-war loading | 750,000–850,000 bpd | S&P Global |

| Total oil transiting Bab el-Mandeb, March 2026 | 3.97 million bpd | Kpler |

| Total oil transiting Bab el-Mandeb, February 2026 | 2.95 million bpd | Kpler |

The February-to-March jump — from 2.95 million to 3.97 million barrels per day transiting Bab el-Mandeb — is almost entirely Saudi rerouted crude. Rico Luman, a transport economist at ING Bank, described the tanker traffic increase as “three to four tankers more per day, which is still a notable difference.” The difference is that those three to four additional tankers per day carry the portion of Saudi Arabia’s export revenue that is keeping the kingdom’s wartime budget solvent.

The East-West Pipeline was designed for a crisis measured in weeks, not a war approaching its second month.

What Happens if Both Hormuz and Bab el-Mandeb Close?

The Center for Strategic and International Studies has modeled the scenario. A combined Hormuz-plus-Bab el-Mandeb closure would block approximately 30% of global container shipping from its normal routing and threaten roughly 22% of global oil supply. The estimated daily trade at risk is $10 billion.

David Butter, an associate fellow at Chatham House, told CSIS that alternative routes can only cover about one-quarter of the oil that normally goes through Hormuz, “and these are vulnerable to attack by Iran and by Yemen’s Houthis.” The “these” in his statement is the Red Sea route — the same route that Ghalibaf’s April 4 post was probing.

“Moving oil out of the Arabian Peninsula would become virtually impossible” if both Yanbu and Fujairah were compromised.

Matt Smith, Lead Oil Analyst, Kpler — ABC News

The arithmetic is not complicated. Saudi Arabia’s Eastern Province exports through Hormuz are already closed. The kingdom’s oil weapon — its ability to flood or restrict markets — depends entirely on moving crude to buyers. If Yanbu is constrained by air defense gaps, and the Bab el-Mandeb is constrained by Houthi anti-ship missiles, the kingdom’s revenue falls to whatever volume it can load at Yanbu and safely escort through 100 kilometers of strait.

JP Morgan analysts estimated, against a pre-war Brent baseline of approximately $80, that disruption to Bab el-Mandeb oil passage could add $20 per barrel to oil prices. Brent crude was trading between $105 and $115 per barrel in early April 2026. The $20 increment is a directional signal, not a linear model — applied to the current range, it puts crude at $125 to $135, territory last seen in 2022 after Russia’s invasion of Ukraine, but with roughly twice the supply disruption.

There is no land bypass for Bab el-Mandeb. The East-West Pipeline exists because someone in Riyadh in 1981 asked “what if Hormuz closes?” and built 1,200 kilometers of steel across the desert. No one built the equivalent from Yanbu south. The pipeline’s Red Sea exit was assumed to be the safe end.

Can the Houthis Actually Close Bab el-Mandeb?

The 2023–2025 campaign provides the empirical answer: yes, without a formal blockade. Houthi attacks halved Suez Canal transits from 26,000 ships per year to 12,700 and diverted approximately 90% of container shipping around the Cape of Good Hope. Physical closure was never required — only premiums high enough that underwriters refused to cover the route.

The arsenal has grown since then. The Houthis now operate the Asef anti-ship ballistic missile, which carries a 500-kilogram warhead and has a range of 400 kilometers, according to Washington Institute for Near East Policy analysis. The Al-Mandeb 2 anti-ship cruise missile has a 120-kilometer range. A MARAD Advisory issued in 2026 estimated that approximately 30 tankers waiting offshore Yanbu are currently within the Asef’s strike envelope.

Nabeel Khoury, former US Deputy Chief of Mission in Yemen, described the threshold to Al Jazeera with precision: the Houthis could halt shipping by “fire at a couple of ships coming through, and that would lead to the arrest of all commercial shipping.” The word “arrest” is doing specific work in that sentence. Commercial shipping does not require a blockade to stop. It requires a credible threat that underwriters refuse to price.

On March 14, 2026, senior Houthi officials formally declared military alignment with Iran — what they called “Hour Zero.” Houthi Deputy Information Minister Mohammed Mansour stated plainly that “closing the Bab al-Mandeb strait is among our options.” Ahmed Nagi, Yemen Senior Analyst at the International Crisis Group, observed that in the 72 hours before April 4, the Houthis had deliberately not resumed Gulf shipping attacks. The restraint, Nagi assessed, was calculated alignment with Tehran’s negotiating strategy — the threat held in reserve is more powerful than the threat executed.

| System | Type | Range | Warhead | Threat Profile |

|---|---|---|---|---|

| Asef | Anti-ship ballistic missile (ASBM) | 400 km | 500 kg | Reaches tankers offshore Yanbu |

| Al-Mandeb 2 | Anti-ship cruise missile | 120 km | — | Covers full width of Bab el-Mandeb |

| Shahed-type drones | One-way attack UAV | 1,500+ km | ~40 kg | Demonstrated at SAMREF, April 3 |

The Insurance Market Will Decide Before the Navy Does

During the 2023–2024 Red Sea crisis, war risk insurance premiums surged from 0.6% of cargo value to as high as 2%, according to Flavio Macau, Associate Dean at Edith Cowan University. A VLCC carrying two million barrels of crude at $110 per barrel represents approximately $220 million in cargo value. At 2% war risk premium, that is $4.4 million in additional insurance cost per voyage — on top of the standard hull and machinery coverage.

The current situation is worse than 2023–2024 in every measurable dimension. The Houthis have formally declared alignment with Iran. An actual refinery strike has been demonstrated at Yanbu. And the Bab el-Mandeb strait, at 30 kilometers wide, is physically narrower than the approaches the Houthis were attacking during the prior campaign.

Ship-owner risk committees, not admirals, will make the operative decision. If underwriters at Lloyd’s or the Norwegian War Risk Insurance Association raise Bab el-Mandeb premiums to levels that make the Red Sea route commercially unviable, tanker operators will divert around the Cape of Good Hope regardless of what any navy promises about escort capability. The Saudi Arabia-to-Netherlands route via Red Sea covers 12,000 kilometers and takes 19 days. The Cape route covers 20,000-plus kilometers and takes 34 days, adding approximately $1 million in fuel costs per round trip per tanker.

The numbers compound at Yanbu’s current throughput. At 3.23 million barrels per day, the terminal is loading roughly 1.5 to 2 VLCCs per day. If insurance-driven diversions reduce that to one per day — or if tanker operators simply refuse the route — Saudi export volumes drop by hundreds of thousands of barrels per day before a single Houthi missile is fired. Yanbu has essentially no surge buffer. The terminal is already past Vortexa’s operational ceiling estimate of 3 million barrels per day.

Saudi Arabia’s Western Flank

The Royal Saudi Naval Force’s Western Fleet, based at King Faisal Naval Base in Jeddah, is the kingdom’s primary surface asset in the Red Sea. The fleet operates four Al Madinah-class guided missile frigates — built in France and commissioned between 1985 and 1986, making them forty years old — and three newer Al Jubail-class corvettes based on the Spanish Avante 2200 design.

Seven surface combatants, four of them aging, cannot provide continuous escort coverage for the volume of tanker traffic Yanbu is generating. Convoy escort requires at least one warship per convoy, and convoys must be assembled and held — introducing delays that further reduce the terminal’s effective throughput. The US Fifth Fleet, headquartered in Bahrain, has periodically surged assets into the southern Red Sea, but the primary American naval presence is in the Gulf of Aden and the Arabian Sea, not in the Bab el-Mandeb transit zone itself.

The Greek-operated Patriot battery at Yanbu is an air defense asset, not a maritime one. It protects the refinery. It does not protect the tankers anchored offshore, and it cannot engage the low-altitude cruise missiles that constitute the primary anti-shipping threat in the strait. The Day 35 war update documented the defense gap the SAMREF strike exposed — a gap that extends over the water.

How Did Saudi Arabia Trade One Chokepoint for Another?

The East-West Pipeline solved the Hormuz problem by routing crude to Yanbu on the Red Sea — then assumed that exit was permanently safe. The Houthis’ post-2023 capacity to threaten Bab el-Mandeb, combined with Iran’s zero self-harm exposure at that strait, turned the 40-year-old bypass into a second chokepoint with worse asymmetries.

The East-West Pipeline was an engineering triumph and a strategic assumption. The assumption was that the Red Sea end of the pipeline was safe — that the threat to Saudi oil exports was concentrated at Hormuz, and that moving crude 1,200 kilometers west eliminated the vulnerability. For forty years, the assumption held. The pipeline was expanded twice — once in 1992, again after the 2019 Abqaiq strikes — always in service of the same logic: more capacity through the safe corridor.

What the pipeline actually did was transfer Saudi Arabia’s chokepoint exposure from Hormuz to Bab el-Mandeb. The transfer carried a hidden asymmetry. At Hormuz, Iran faces self-harm: Iranian crude exports from Kharg Island transit the same strait. A Hormuz closure costs Iran its own revenue. At Bab el-Mandeb, the self-harm calculus disappears. Iran’s crude does not route through the Red Sea. The Houthis, operating as Tehran’s proxy force in Yemen, can threaten or close the strait without costing Iran a single barrel of export revenue.

The unnamed Iranian military official quoted by Tasnim News Agency in late March stated that Iran could open a new front at Bab el-Mandeb “if attacks are carried out on Iranian territory or its islands.” The conditional phrasing — “if” — is the threat being held in reserve, consistent with the pattern Ahmed Nagi identified. The Houthis are holding the trigger. Tehran is pointing at it.

PressTV’s March 30 framing — “Bab el-Mandeb joins Hormuz as pillars of global economic power” — was not analysis. It was a public statement of doctrine. Two chokepoints, one controlled directly by Iran and one controlled by Iran’s most capable proxy force, presented as a unified deterrence architecture. Ghalibaf’s April 4 post was the civilian-political articulation of the same doctrine, delivered by a man whose professional formation was in the IRGC’s missile program.

The pipeline that was supposed to make Saudi Arabia resilient against Iran at Hormuz now delivers Saudi crude into a Red Sea corridor where Iran can operate through the Houthis at lower cost and lower risk than it ever could at Hormuz itself. The 40-year investment did not eliminate the chokepoint. It relocated it to a geography where the adversary’s position is stronger.

| Factor | Strait of Hormuz | Bab el-Mandeb |

|---|---|---|

| Width | ~54 km (navigable channel ~3 km) | ~30 km |

| Iran self-harm from closure | High — Kharg Island exports transit Hormuz | None — Iran’s crude does not route through Red Sea |

| Controlling actor | Iran (direct) | Houthis (Iranian proxy) |

| Land bypass infrastructure | East-West Pipeline (7 million bpd ceiling) | None |

| Saudi oil volume at risk (March 2026) | Closed — traffic rerouted | 3.97 million bpd transiting |

| Demonstrated disruption capability | 1980s Tanker War, 2019 attacks | 2023–2025 Houthi campaign halved Suez transits |

Frequently Asked Questions

What is the Bab el-Mandeb strait and why does it matter for oil prices?

Bab el-Mandeb is the roughly 100-kilometer-long, 30-kilometer-wide strait connecting the Red Sea to the Gulf of Aden at the southern tip of the Arabian Peninsula. It carries approximately 12% of global trade by value and, as of March 2026, 3.97 million barrels per day of oil — mostly Saudi crude rerouted from the Persian Gulf via the East-West Pipeline. The strait has Houthi-controlled western Yemen on its northern shore and Djibouti — home to Chinese, American, and French military bases — on its southern shore. Chinese naval presence at Djibouti adds a complication absent from most Western analyses: Beijing has its own interests in keeping the strait open for Belt and Road shipping, creating a three-way deterrence dynamic distinct from the bilateral Iran-Saudi contest at Hormuz.

Could Saudi Arabia reroute oil exports if Bab el-Mandeb were closed?

Unlike the Hormuz closure — where the East-West Pipeline provided the Red Sea alternative — there is no land-based bypass for Bab el-Mandeb. The only maritime alternative is routing tankers north through the Suez Canal, but VLCCs carrying Saudi crude cannot transit Suez fully laden and would require lightering operations at Ain Sukhna or Sidi Kerir — a process that adds 7 to 10 days and requires port infrastructure Egypt has not scaled for wartime throughput. The SUMED pipeline from the Red Sea to the Mediterranean has a capacity of approximately 2.5 million barrels per day, but it was operating near capacity before the war began with non-Saudi flows and would require diplomatic agreements with Cairo that do not currently exist at the volumes needed.

How does Ghalibaf’s background differ from typical Iranian politicians?

Ghalibaf is one of the few senior Iranian political figures whose career began in operational military command during the formative period of Iran’s missile program. Most Majlis speakers have been clerics or civilian technocrats. Ghalibaf’s path — IRGC enlistment at 18, divisional command in the Iran-Iraq War, IRGC Air Force command during the Shahab-3 development era, then Tehran mayor and parliamentarian — gives him technical fluency in targeting, range envelopes, and force projection that his April 4 post’s precise commodity-by-commodity enumeration reflects. His 2013 and 2017 presidential campaigns both centered on economic management, not security — a deliberate rebranding that has led most Western media to categorize him as a technocratic conservative rather than as a military officer.

What happened to Suez Canal traffic during the 2023–2025 Houthi campaign?

Annual Suez Canal ship transits fell from approximately 26,000 in 2023 to 12,700 by 2025 — a decline of more than 50% — driven entirely by commercial shipping decisions, not a physical blockade. Egypt’s Suez Canal Authority revenue dropped correspondingly, from $9.4 billion in fiscal year 2022–2023 to an estimated $5.1 billion by 2025, creating a fiscal crisis in Cairo that complicated US diplomatic efforts to secure Egyptian cooperation on Red Sea escort operations. The revenue loss exceeded Egypt’s annual IMF disbursement tranche, a comparison that received almost no coverage in energy-focused outlets but shaped Cairo’s willingness to permit military operations from Egyptian territory.

What would a $20-per-barrel oil price increase mean for global economies?

JP Morgan’s pre-war estimate of a $20-per-barrel increase from Bab el-Mandeb disruption was modeled against a Brent baseline of approximately $80. Applied to the current baseline of $105–115, the increase would push crude to $125–135 per barrel — a range that, according to the International Energy Agency’s demand-destruction models, historically triggers measurable GDP contraction in oil-importing economies within two quarters. India, which imports approximately 85% of its crude and sources a growing share from Saudi Red Sea loadings, would face a current-account impact estimated by the Reserve Bank of India at 0.4% of GDP per $10 increase in Brent. Japan and South Korea, which also receive Yanbu-loaded cargoes via Bab el-Mandeb, would face similar exposure amplified by yen and won weakness against the dollar.