DHAHRAN — When Iranian drones struck Saudi Aramco’s Ras Tanura refinery complex on the morning of March 2, 2026, they did more than set fire to one of the Middle East’s most critical pieces of oil infrastructure. They triggered the activation of an emergency rerouting plan that had been designed four decades ago for precisely this scenario — and exposed the fragility of a global energy system that still depends on a 34-kilometre-wide chokepoint for one-fifth of its daily oil supply. The shutdown of Ras Tanura, which processes 550,000 barrels per day and serves as one of Saudi Arabia’s primary crude export terminals, has forced Aramco into an unprecedented logistical pivot: redirecting millions of barrels of crude oil westward across 1,200 kilometres of desert pipeline to the Red Sea port of Yanbu, even as the Strait of Hormuz remains effectively closed for the sixth consecutive day.

The consequences are radiating outward at remarkable speed. Brent crude has surged past $85 a barrel, up roughly 20% in a single week. Aramco has hiked prices for Asian buyers by $2.50 per barrel — more than three times the expected increase. VLCC supertanker rates have shattered all-time records. And hundreds of ships sit stranded on both sides of the Hormuz chokepoint, their insurers having pulled war-risk coverage, their owners unwilling to run a gauntlet of Iranian threats, GPS jamming, and intermittent missile fire. The price surge has created a remarkable paradox for the Kingdom: even with Ras Tanura offline, the wartime revenue windfall from elevated oil prices far exceeds the cost of infrastructure damage.

Table of Contents

- What Happened at Ras Tanura on March 2?

- Why Ras Tanura Matters to Global Energy Markets

- How Severe Is the Damage to Aramco’s Largest Refinery?

- The Petroline Lifeline — Aramco’s East-West Pipeline

- Yanbu and the Red Sea Pivot

- The Hormuz Bottleneck — Six Days of Closure

- What Does the Tanker Crisis Look Like in Numbers?

- The Price Shock — From $70 to $85 and Counting

- The Ticking Clock on Gulf Oil Storage

- The Saudi Paradox — Profiting from a War on Its Doorstep

- Who Bears the Brunt? Asian Buyers and the Supply Scramble

- What Does Ras Tanura Reveal About Saudi Air Defense?

- The Ripple Effect — From Dhahran to Des Moines

- Risk Assessment — Four Scenarios for Aramco’s Export Capacity

- Can Aramco Keep the Oil Flowing?

- Frequently Asked Questions

What Happened at Ras Tanura on March 2?

At approximately 7:04 a.m. local time on Monday, March 2, 2026, two Iranian-launched drones approached the Ras Tanura refinery complex on Saudi Arabia’s Persian Gulf coast. The Saudi air defense network intercepted both drones in the vicinity of the facility, but falling debris from the interceptions struck processing infrastructure within the refinery perimeter, igniting a fire that emergency response teams subsequently contained.

The Saudi Ministry of Energy, in a statement carried by the state-backed Saudi Press Agency, described the fire as “limited” and confirmed it was “immediately contained by emergency response teams” with no casualties reported. The ministry added that “some operational units at the refinery were shut down as a precautionary measure, without any impact on the supply of petroleum products to local markets.”

That cautious official language, however, belied the severity of the disruption. Within hours, Aramco confirmed that the entire Ras Tanura complex would remain shut down for an extended period while damage assessments continued and exports were rerouted to alternative facilities. High-resolution satellite imagery obtained by commercial providers on March 3 revealed visible structural damage at the site, including burn scars, impact zones, and damaged sections of refining infrastructure that suggest the “precautionary” shutdown was anything but routine.

The attack came as part of a wider Iranian retaliatory campaign following Operation Epic Fury — the coordinated U.S.-Israeli strikes on Iranian military and nuclear facilities that began on February 28, 2026. Iran’s response targeted oil and gas infrastructure across the entire Gulf region, with strikes or attempted strikes on facilities in Abu Dhabi, Dubai, Doha, Manama, and Oman’s Duqm port, alongside the effective closure of the Strait of Hormuz by the Islamic Revolutionary Guard Corps Navy.

Why Ras Tanura Matters to Global Energy Markets

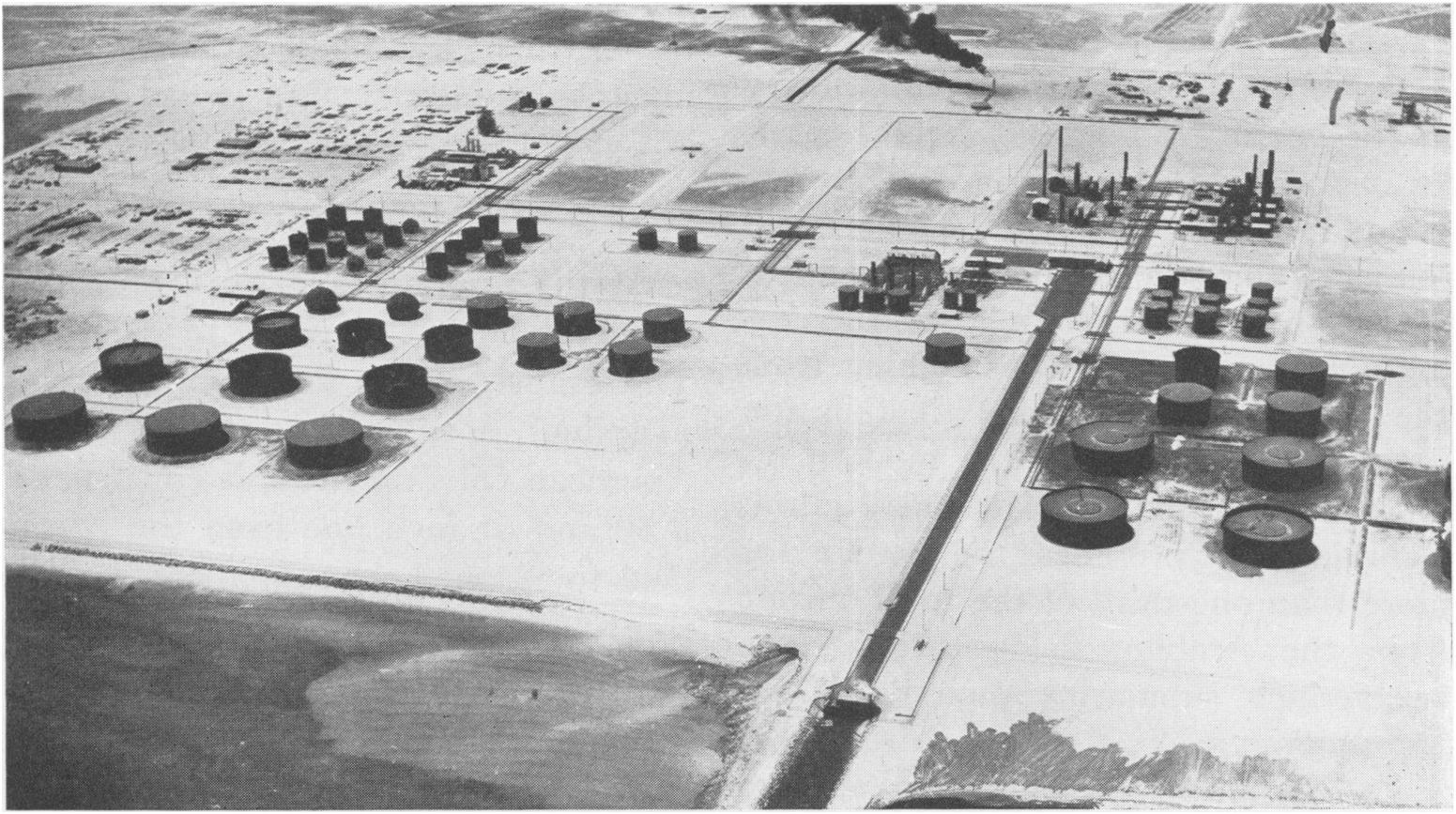

Ras Tanura is not merely large. It occupies a position in the global energy architecture that makes its shutdown a first-order geopolitical event. The complex, situated on a peninsula jutting into the Persian Gulf roughly 50 kilometres north of Dammam in Saudi Arabia’s Eastern Province, has been at the heart of the kingdom’s oil industry since Aramco built its first 3,000-barrel-per-day refining unit there in 1940.

The refinery today processes 550,000 barrels per day of crude oil and gas condensates, making it the largest single refining facility in the Middle East. But Ras Tanura’s significance extends far beyond refining. The complex also houses a natural gas liquids processing facility, a crude oil stabilization plant, and one of the kingdom’s most important maritime export terminals. An estimated 31% of Saudi domestic demand for refined petroleum products and NGL flows through Ras Tanura.

| Metric | Detail |

|---|---|

| Refining capacity | 550,000 bpd |

| Year commissioned (current capacity) | 1986 (expanded 2007-2012) |

| Share of Saudi domestic fuel supply | ~31% |

| Owner/Operator | Saudi Aramco |

| Location | Eastern Province, Persian Gulf coast |

| Expansion investment (2007-2012) | $8 billion |

| Products | Gasoline, diesel, jet fuel, NGL, naphtha |

| Export terminal capacity | Multiple single-point moorings for VLCCs |

The facility underwent a major $8 billion expansion between 2007 and 2012 that added a new crude distillation unit and upgraded its clean fuels production capacity. It is Aramco’s most complex refinery, processing both crude oil and gas condensates across an integrated facility that feeds both the domestic market and the export terminal. Gasoil futures spiked immediately on news of the shutdown, reflecting Ras Tanura’s role as a key regional supplier of diesel fuel — the lifeblood of industrial economies across Asia.

How Severe Is the Damage to Aramco’s Largest Refinery?

Aramco has not provided a detailed public assessment of the structural damage at Ras Tanura, and no official restart timeline has been communicated to the market. This silence is itself significant. After the September 2019 drone and cruise missile attack on Aramco’s Abqaiq and Khurais facilities — which temporarily knocked out 5.7 million barrels per day of processing capacity — the company restored operations within approximately two weeks and was notably transparent about the recovery timeline. The current reticence suggests either greater uncertainty about the repair schedule or a deliberate decision not to signal vulnerability during an active conflict.

Satellite imagery from March 3 tells a partial story. Analysts at commercial imagery firms identified burn scars in at least two distinct areas within the refinery perimeter, along with what appear to be impact zones near processing units. The damage pattern is consistent with debris scatter from drone interceptions at relatively low altitude — fragments of airframe, warhead material, and interceptor remnants raining down across a wide area rather than concentrated at a single strike point.

Beyond the structural damage, the fires and debris scatter have added to a growing ecological damage to Gulf waters that is compounding with each strike on coastal oil infrastructure. Hydrocarbons from breached pipelines and burning refinery units drain into the shallow Persian Gulf, whose enclosed waters have almost no capacity to disperse or dilute what enters them.

This distinction matters for the restart timeline. A direct hit from a heavy warhead on a crude distillation column or catalytic cracking unit could take months to repair. Scattered debris damage to auxiliary systems, piping, and control infrastructure is typically repairable in weeks — but only if replacement components are available and the security environment permits sustained repair operations. With the broader conflict still intensifying, neither condition is guaranteed.

Torbjorn Soltvedt, principal Middle East analyst at risk intelligence company Verisk Maplecroft, noted that Iran’s targeting of Ras Tanura was strategic rather than purely military. The goal, Soltvedt assessed, was to raise the economic costs of the conflict for Gulf states, forcing Saudi Arabia and the UAE to calculate whether the price of continued association with the U.S.-led campaign against Iran was worth the risk to their hydrocarbon infrastructure.

The Petroline Lifeline — Aramco’s East-West Pipeline

Buried beneath 1,200 kilometres of Saudi desert, running from the Abqaiq oil processing facility in the Eastern Province to the Red Sea port of Yanbu on the kingdom’s western coast, lies the infrastructure that may determine whether this crisis becomes a manageable disruption or a catastrophic one. The East-West Pipeline — officially known as the Petroline — was built in 1981 for precisely the scenario now unfolding.

The pipeline’s origin story is instructive. In the early 1980s, the Iran-Iraq War was raging, and planners in Riyadh feared that the Strait of Hormuz could be closed or mined, severing Saudi Arabia’s primary export route. The General Petroleum and Mineral Organization (Petromin) commissioned a twin-pipeline system capable of moving crude oil across the full width of the Arabian Peninsula, bypassing the Gulf entirely. Aramco simultaneously built a parallel pipeline for natural gas liquids. The strategic logic was clear: if Hormuz closed, Saudi oil could still reach world markets via the Red Sea and the Suez Canal.

For more than four decades, the Petroline operated well below its design capacity, serving primarily as supplementary export infrastructure and a hedge against disruption. Its capacity was expanded to 5 million barrels per day in 1992. During the 2019 Abqaiq-Khurais attacks, Aramco temporarily converted NGL pipelines to carry crude, pushing throughput to approximately 7 million bpd for a brief period. That demonstrated the system’s theoretical maximum — and its limitations.

As of March 2026, the East-West Pipeline has become the critical lifeline for Saudi oil exports. Aramco confirmed on March 5 that it was actively redirecting export volumes from its main producing regions in the east via the Petroline to Yanbu, and has informed some buyers of its Arab Light crude that they must now load cargoes at Yanbu rather than at Gulf terminals.

| Parameter | Detail |

|---|---|

| Length | 1,200 km (746 miles) |

| Diameter | 48 inches (120 cm), twin-pipe |

| Normal capacity | 5 million bpd |

| Surge capacity (with NGL conversion) | ~7 million bpd |

| Origin | Abqaiq processing facility, Eastern Province |

| Terminus | Yanbu, Red Sea coast |

| Year built | 1981 |

| Capacity expanded | 1992 |

| Operator | Saudi Aramco |

Bob McNally, president of Rapidan Energy Group, has warned that even more concerning than the closure of the strait itself would be if Saudi Arabia’s oil production facilities were knocked offline for an extended period. The Petroline addresses the export bottleneck, but it cannot solve for production disruptions. If further Iranian strikes target the Abqaiq processing facility — the entry point for the East-West Pipeline and the single most critical node in Saudi Arabia’s entire oil infrastructure — the pipeline becomes irrelevant regardless of its capacity.

Yanbu and the Red Sea Pivot

Five very large crude carriers departed the port of Yanbu in the first four days of March 2026, collectively loading approximately 10 million barrels of crude oil. Average shipments from Yanbu so far this month total about 2.5 million barrels per day — a threefold increase from February’s average of 786,000 barrels per day, according to Bloomberg tanker-tracking data.

The ramp-up at Yanbu represents the largest and fastest reorientation of Saudi export flows in the kingdom’s history. Even during the 2019 attacks, Gulf-side terminals were only temporarily disrupted; the system never required a wholesale shift to Red Sea loading. What is happening now is qualitatively different — an open-ended diversion of the majority of Saudi crude exports through a single western port, under wartime conditions, with no clear timeline for the resumption of normal Gulf-side operations.

Yanbu’s port infrastructure, while substantial, was not designed to handle the full volume of Saudi exports. The facility has multiple deep-water berths capable of accommodating VLCCs, and the adjacent King Fahd Industrial Port provides additional loading capacity. But moving 5 to 7 million barrels per day through a single port complex — even with the pipeline feeding it at full capacity — introduces bottleneck risks at the terminal itself. Berth availability, tug capacity, pilotage scheduling, and the sheer number of tankers that need to cycle through the loading bays all become potential constraints.

There is also a secondary vulnerability. Vessels sailing to and from Yanbu must transit the Bab el-Mandeb Strait at the southern end of the Red Sea. For the past two years, Iran-backed Houthi militants in Yemen conducted a sustained campaign of missile, drone, and small-arms attacks against commercial shipping transiting the Red Sea. While the Houthis suspended those attacks following the October 2025 Israel-Hamas ceasefire and a subsequent U.S.-brokered understanding, the group threatened on February 28 to resume operations in response to the U.S.-Israeli strikes on Iran. As of March 5, Houthi attacks have not resumed — internal debate within the group reportedly continues — but the threat alone adds a risk premium to any vessel loading at Yanbu.

Egypt has entered the picture as well. Cairo has reportedly offered capacity on the Sumed (Suez-Mediterranean) Pipeline, which connects the Red Sea to the Mediterranean, as an additional bypass option for Saudi crude that needs to reach European markets without transiting the Suez Canal. The 320-kilometre pipeline has a capacity of approximately 2.5 million barrels per day and could theoretically absorb a portion of diverted Saudi flows, though negotiations on terms and logistics remain ongoing.

The Hormuz Bottleneck — Six Days of Closure

The Strait of Hormuz has been effectively closed since March 1, 2026. On that day, following the launch of Operation Epic Fury, Iran’s Islamic Revolutionary Guard Corps Navy began threatening vessels attempting to transit the waterway. On March 2, a senior IRGC official publicly confirmed the closure and warned that any ship attempting to pass would be attacked — a declaration subsequently disputed by the U.S. military’s Central Command, though the practical effect was identical regardless of its legal status.

The numbers tell the story of collapse. On a normal day, approximately 100 vessels transit the Strait of Hormuz, carrying roughly 19.8 million barrels of crude oil — about 20% of global daily supply. On March 1, only 18 ships made the crossing, many at night with their Automatic Identification System transponders switched off. By March 4, the number had fallen to just five crossings for the entire day. On March 5, only three tankers carrying a combined 2.8 million barrels made it through — an 86% decline from normal daily volumes.

The key question for the global economy is obvious: Will the Strait of Hormuz be effectively closed for oil and gas exports for more than a few weeks? If so, it would hurt global growth and raise global inflation noticeably.

Holger Schmieding, Chief Economist, Berenberg Bank

The closure has not been achieved solely through kinetic means. Widespread GPS and AIS jamming — affecting more than 1,100 ships in the past 24 hours alone, according to Windward maritime analytics — has made navigation in the strait and surrounding waters actively dangerous. Vessels have been falsely positioned at airports, a nuclear power plant, and on Iranian land, creating what Dryad Global described as “heightened risk” from electronic warfare activity. At least 21 AIS jamming clusters have been identified across UAE, Qatari, Omani, and Iranian waters. In congested waterways where precise navigation is essential for collision avoidance and traffic separation compliance, the inability to trust GPS data is functionally equivalent to closing the strait even without a single shot being fired.

| Date | Vessel Crossings | Est. Oil Volume (million bbl) | Notable Events |

|---|---|---|---|

| Feb 28 (normal) | ~100 | ~19.8 | Operation Epic Fury begins |

| Mar 1 | ~18 | ~3.5 | IRGC threats begin; Maersk suspends transits |

| Mar 2 | ~10 | ~2.0 | IRGC declares strait closed; Ras Tanura hit |

| Mar 3 | ~8 | ~1.5 | Insurance carriers pull war-risk cover |

| Mar 4 | 5 | ~1.0 | GPS jamming hits 1,100+ ships |

| Mar 5 | 3 | ~2.8 | VLCC rates hit all-time record |

What Does the Tanker Crisis Look Like in Numbers?

Approximately 200 internationally trading, non-sanctioned tankers are now stranded in the Persian Gulf, according to Lloyd’s List. These are compliant vessels — not the shadow fleet that carries sanctioned crude — either anchored at terminals, berthed at loading facilities, or slow-steaming in circles as their operators wait for clarity on security conditions.

The congestion is most acute among very large crude carriers. According to Kpler data, 60 VLCCs are trapped inside the Gulf, representing nearly 8% of the global compliant VLCC fleet. Of those, 13 are alongside loading terminals (loaded but unable to depart), 33 are at anchor, and 14 are slow-steaming. Each VLCC can carry approximately 2 million barrels. The crude sitting in stranded tankers alone represents more than 120 million barrels of oil that cannot reach consumers.

The financial consequences for shipowners are paradoxical. VLCC spot earnings have shattered all previous records, reaching $423,000 to $445,000 per day for Middle East Gulf-to-Far East routes — an increase of more than 94% from February 28 levels. But these rates are theoretical for trapped vessels. Ships that can operate outside the Gulf — loading at Yanbu or West African and U.S. Gulf ports — are commanding historic premiums. Ships inside the Gulf are earning nothing, burning fuel at anchor, and watching their insurance evaporate.

That insurance collapse is perhaps the most consequential element of the shipping crisis. Since the conflict began, leading maritime Protection and Indemnity clubs — including Norway’s Gard and Skuld, Britain’s NorthStandard, and the London P&I Club — have canceled war-risk coverage for vessels operating in the Gulf. War-risk premiums for ships that can still obtain coverage have surged from 0.125% to between 0.2% and 0.4% of the insured hull value per transit. For a VLCC valued at $120 million, that translates to an additional cost of $240,000 to $480,000 per crossing — a quarter of a million dollars in insurance alone before the ship has burned a single barrel of bunker fuel.

Maersk, MSC, Hapag-Lloyd, and CMA CGM — the four largest container shipping companies — have all suspended Hormuz transits and are rerouting vessels around the Cape of Good Hope, adding approximately 3,500 nautical miles and 10 to 14 days to voyages between Asia and Europe. Maersk has gone further, temporarily suspending cargo booking acceptance for all Gulf ports except Salalah in Oman, with exceptions limited to critical foodstuffs, medicine, and essential goods. The container shipping disruption compounds the crude oil crisis, threatening supply chains for manufactured goods, electronics, and food imports across the Gulf states.

| Metric | Before Crisis (Feb 28) | Current (Mar 5) | Change |

|---|---|---|---|

| VLCC spot rate (ME Gulf to China) | $218,000/day | $423,000-$445,000/day | +94% |

| War-risk insurance premium | 0.125% hull value | 0.2%-0.4% hull value | +60% to +220% |

| VLCCs stranded in Gulf | 0 | 60 | 8% of global fleet |

| Total tankers stranded | 0 | ~200 | — |

| Ships with GPS jamming | 0 | 1,100+ | — |

| Major insurers offering cover | All major P&I clubs | Most terminated | — |

The Price Shock — From $70 to $85 and Counting

Brent crude closed at $85.41 per barrel on March 5, 2026, its highest level since the summer of 2024 and representing a roughly 20% increase from the pre-crisis level of approximately $71 per barrel on February 27. WTI crude, the U.S. benchmark, topped $80 per barrel. The price surge reflects not merely the loss of Ras Tanura’s 550,000 bpd of refining capacity but the far larger disruption to the 19.8 million barrels per day that normally transit the Strait of Hormuz.

The immediate market impact was captured in Aramco’s pricing decision for April deliveries to Asian buyers. The company raised the official selling price of its flagship Arab Light crude by $2.50 per barrel above the regional benchmark — the largest increase since August 2022. A pre-conflict survey of traders and refiners had forecast an increase of approximately $0.80 per barrel. The gap between expectation and reality — more than three times the consensus forecast — reflects the severity of the supply disruption and Aramco’s assessment of its own pricing power in a market suddenly short of available barrels.

Tom Kloza, a veteran oil analyst and adviser to Gulf Oil, warned that wholesale gasoline futures prices could rise by 25 cents immediately because of the war, translating to retail increases of 5 to 10 cents per day at the pump for a sustained period. That assessment is already proving conservative. U.S. retail gasoline prices jumped 27 cents in a single week to $3.25 per gallon, according to AAA — a 9% weekly surge that has prompted immediate comparisons to the 1973 oil embargo and the 1979 Iranian Revolution, the two previous instances when Gulf conflict produced sustained price shocks in Western consumer markets.

The question on every trading floor is whether $85 represents the ceiling or merely a waypoint. If the Hormuz closure persists beyond two to three weeks — the threshold at which Gulf storage begins to overflow and production must be physically curtailed — analysts at JPMorgan, Goldman Sachs, and Rapidan Energy have all indicated that $100 per barrel becomes likely. A sustained closure of one month or longer could push prices toward $120 to $150, driven not by speculation but by the physical reality of 20 million missing barrels per day.

Central banks are watching with alarm. The price shock arrives at a moment when the U.S. Federal Reserve, the European Central Bank, and the Bank of England had all been signaling the potential for further interest rate cuts in 2026. An oil-driven inflation surge could freeze or reverse those plans, tightening monetary conditions at the worst possible moment for an already fragile global economy. The CNBC assessment that the Middle East conflict poses “a fresh test for central banks” understates the severity. If oil reaches triple digits and stays there, the policy framework that has governed the post-pandemic recovery effectively collapses. Europe faces the sharpest energy crisis since 2022, with gas prices doubling and storage at decade lows.

The Ticking Clock on Gulf Oil Storage

The most underappreciated dimension of the crisis is not what is happening at sea but what is happening on land. With the Strait of Hormuz closed and Gulf-side exports reduced to a trickle, crude oil that would normally be loaded onto tankers is instead flowing into onshore storage tanks across Saudi Arabia, Kuwait, the UAE, Iraq, and Qatar. Those tanks have finite capacity. When they fill, production must be physically shut in — wells capped, processing plants idled, entire fields taken offline.

Natasha Kaneva, head of commodity markets strategy at JPMorgan, has warned that some Persian Gulf producers may exhaust their crude storage in just over three weeks. Kuwait, with limited storage relative to its production, could face a reckoning in less than two weeks. Iraq, which has the least storage capacity among major Gulf producers, has already been compelled to begin production cuts.

Saudi Arabia is in a stronger position than its neighbours. The kingdom’s storage infrastructure is among the most extensive in the world, and the East-West Pipeline’s ability to divert up to 5 million barrels per day to Yanbu relieves pressure on Gulf-side tanks. But even Saudi capacity has limits. Aramco produced approximately 9 million barrels per day in February; if even half of that volume cannot be exported through the Gulf, the surplus accumulates at roughly 4.5 million barrels per day. At that rate, even substantial storage reserves would fill within weeks.

The storage crunch introduces a vicious feedback loop. Production curtailments reduce supply, which pushes prices higher, which in turn generates political pressure to resolve the conflict or find alternative export routes. But production curtailments also threaten the physical integrity of oil fields — shutting in wells can cause reservoir damage that takes months to reverse, and restarting complex production systems is neither instant nor risk-free. The 2019 Abqaiq-Khurais attacks demonstrated that Aramco can recover from infrastructure damage; a prolonged production shutdown from full storage tanks would present a qualitatively different challenge.

The Saudi Paradox — Profiting from a War on Its Doorstep

There is a deeply uncomfortable dynamic at the centre of this crisis that few commentators have addressed directly. Saudi Arabia is simultaneously suffering from the conflict — its largest refinery shut down, its Gulf export terminals paralysed, its infrastructure under direct military threat — and benefiting from it. Every dollar per barrel that Brent crude rises adds approximately $3 billion in annual revenue to the kingdom’s oil income. The move from $71 to $85 represents roughly $42 billion in annualised additional revenue if sustained — a windfall that would substantially ease the fiscal pressures that have constrained Crown Prince Mohammed bin Salman’s ambitious Vision 2030 spending programme.

The $2.50 per barrel price hike for Asian buyers underscores the point. Aramco does not set its official selling prices as an act of generosity. The increase reflects a calculated assessment that demand for Saudi crude is sufficiently inelastic — Asian refiners have few alternatives when Iranian, Iraqi, and Kuwaiti barrels are stranded behind a closed strait — to support aggressive pricing even while Aramco’s own infrastructure is damaged. The kingdom is selling less oil, but at substantially higher prices, and the net revenue effect may well be positive.

This paradox creates a complex incentive structure for Riyadh. Saudi Arabia has publicly positioned itself as a victim of Iranian aggression, and the Ras Tanura attack provides genuine grounds for that claim. But the kingdom’s calculated response — hiking prices, redirecting exports, maintaining production — suggests a strategic actor making rational decisions under pressure rather than a passive victim being overwhelmed by events. The speed with which Aramco activated the Petroline system and began loading tankers at Yanbu indicates that contingency planning for precisely this scenario was well advanced, possibly for years.

OPEC+ dynamics add another layer. The cartel had paused a series of planned production increases through the first quarter of 2026, with key members led by Saudi Arabia and Russia agreeing to add 206,000 barrels per day in April — a decision whose strategic calculus reveals a multi-layered gambit involving Washington, Moscow, and the oil futures market. The conflict has rendered that planned increase almost irrelevant — additional supply cannot reach the market if the Strait of Hormuz is closed — but it gives Saudi Arabia diplomatic cover to maintain its production capacity while prices surge. The International Energy Agency estimates OPEC’s total spare capacity at 5.3 million barrels per day, of which 3.1 million is held by Saudi Arabia. That spare capacity is the kingdom’s ultimate strategic asset, but as one unnamed analyst told Bloomberg, “Everything that you bring on now leaves less in reserve.” The war simultaneously makes the spare capacity more valuable and more difficult to deploy.

Who Bears the Brunt? Asian Buyers and the Supply Scramble

The geography of global oil trade means the Hormuz crisis inflicts its heaviest costs on Asian economies. Japan, South Korea, India, and China collectively import approximately 15 million barrels per day from Persian Gulf producers, with the vast majority transiting the Strait of Hormuz. For Japan and South Korea, Gulf crude represents more than 80% of total oil imports. For India, the figure is approximately 60%. These nations have limited strategic petroleum reserves relative to their consumption — Japan holds approximately 130 days of imports, South Korea approximately 90 days, and India roughly 65 days — and each day of Hormuz closure drains those buffers.

The immediate scramble for alternative supply has intensified competition for non-Gulf barrels. West African crude — from Nigeria, Angola, and Equatorial Guinea — has seen premiums spike as Asian refiners bid aggressively for cargoes that do not require Hormuz transit. U.S. Gulf Coast crude exports, which have grown substantially since the shale revolution, are commanding historic premiums for delivery to Asian ports. Brazilian pre-salt crude, which has quietly become one of the world’s most important swing supplies, is being redirected to Asian buyers willing to pay spot premiums well above contract prices.

China’s position is particularly complex. As the world’s largest crude oil importer at approximately 11 million barrels per day, China has the most to lose from a sustained Hormuz closure. But Beijing also maintains substantial strategic reserves — estimated at 500 to 600 million barrels in above-ground storage — and has quietly increased purchases of Iranian crude through the shadow fleet over the past several years, creating a diplomatic entanglement that complicates its response to the crisis. Chinese refiners are the most aggressive bidders for Yanbu-loaded Saudi crude, and Beijing has reportedly made diplomatic approaches to Riyadh seeking assurances of continued supply via the Red Sea route.

India faces a different set of pressures. Indian refiners had become increasingly reliant on discounted Russian crude since the Ukraine war, but Russian crude from the Pacific port of Kozmino is not a substitute for the middle-weight sour crudes that Gulf producers supply and that Indian refineries are configured to process. The configuration mismatch means India cannot simply swap Russian barrels for Saudi ones without incurring refinery efficiency losses and product quality compromises. Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum have all reportedly activated emergency procurement protocols, sourcing spot cargoes from West Africa and the Americas at prices that will ultimately be passed through to Indian consumers.

| Country | Total Oil Imports (million bpd) | Gulf Share (%) | Strategic Reserve (days of imports) | Primary Vulnerability |

|---|---|---|---|---|

| China | ~11.0 | ~45% | ~50-55 | Volume — largest importer globally |

| India | ~5.0 | ~60% | ~65 | Refinery configuration for sour crude |

| Japan | ~2.5 | ~85% | ~130 | Almost total Gulf dependence |

| South Korea | ~2.8 | ~80% | ~90 | Limited domestic production |

| Taiwan | ~0.9 | ~70% | ~90 | Island supply chain fragility |

The LNG dimension adds another pressure layer. Qatar, the world’s largest LNG exporter, ships virtually all of its gas through the Strait of Hormuz. South Korea and Japan are the two largest LNG importers globally, and both rely heavily on Qatari supply. A prolonged Hormuz closure does not merely threaten their oil supply — it threatens their electricity generation, industrial gas supply, and heating fuel for hundreds of millions of people. The interconnection between the oil crisis and the gas crisis multiplies the economic damage far beyond what crude oil prices alone suggest.

What Does Ras Tanura Reveal About Saudi Air Defense?

Saudi Arabia operates one of the most expensive and technologically sophisticated air defense networks in the Middle East, anchored by the Patriot PAC-3 missile system, the Terminal High Altitude Area Defense (THAAD) system, and a growing inventory of domestically produced short-range interceptors. The Kingdom has spent an estimated $65 billion on defense and security in 2025 alone, ranking among the top five military spenders globally. Yet the Ras Tanura attack — like the 2019 Abqaiq-Khurais strikes before it — has raised searching questions about the effectiveness of these systems against low-flying drone threats.

The Saudi Ministry of Energy stated that both drones were “intercepted” in the vicinity of Ras Tanura, and technically, the claim may be accurate — the drones did not reach their intended impact points intact. But interception debris raining down onto a refinery complex and starting a fire that forced a complete operational shutdown is not the kind of success that any air defense commander would celebrate. The fundamental challenge is one of physics and economics: a Shahed-136 one-way attack drone costs Iran approximately $20,000 to $50,000 to produce, while a Patriot PAC-3 interceptor missile costs approximately $4 million. The exchange ratio is roughly 80 to 200 in Iran’s favour.

This cost asymmetry — which defense analysts have termed the “drone dilemma” — means that Iran can launch dozens or hundreds of cheap drones against Saudi infrastructure, forcing the Kingdom to expend interceptors that cost orders of magnitude more. Even when interceptions succeed, as they apparently did at Ras Tanura, the probability of some debris causing damage to a target-rich industrial environment remains significant. A refinery is not a hardened military bunker; its processing units, piping, control systems, and storage tanks present thousands of square metres of vulnerable surface area.

The timing of the attack also suggests intelligence-driven targeting. Ras Tanura was struck at a moment when global attention was focused on the Strait of Hormuz, and when the psychological impact of shutting down one of the world’s most recognized oil facilities would be maximized. Iranian planners appear to have calculated that even a partially successful attack — intercepted drones, limited fire, precautionary shutdown — would achieve strategic objectives by demonstrating that Saudi oil infrastructure remains vulnerable regardless of the Kingdom’s defensive investments.

For the Saudi royal family, the defense implications extend beyond this single attack. If Iran can reach Ras Tanura, it can reach Abqaiq, Dhahran, Jubail, and the storage facilities that line the Eastern Province coast. The entire Saudi oil infrastructure complex sits within drone range of Iranian launch sites, and the volume of threats that Iran can generate vastly exceeds the interceptor inventory that Saudi Arabia maintains. Crown Prince Mohammed bin Salman’s multi-billion dollar defense modernization programme was designed in part to address this vulnerability, but the Ras Tanura attack suggests that the gap between threat and capability remains wider than Riyadh would prefer to acknowledge.

The Ripple Effect — From Dhahran to Des Moines

The Ras Tanura shutdown and Hormuz closure are not merely energy events. They are transmitting economic shocks through every sector of the global economy, from agriculture to aviation, from manufacturing to consumer confidence. Understanding the full scope of the ripple effect requires following the oil price signal through the chain of industries and consumers that ultimately absorb it.

Transportation costs are the most immediate transmission mechanism. Diesel fuel powers the trucks, trains, and container ships that move goods through global supply chains. The 20% surge in crude prices translates directly into higher freight costs, which are passed through to the price of every physical product that moves by road, rail, or sea. The American Trucking Associations has estimated that a sustained $15 per barrel increase in crude oil prices adds approximately 5 to 8 cents per mile to trucking costs — a margin that the industry’s razor-thin profit margins cannot absorb.

Agriculture is especially exposed. Modern farming depends on diesel for tractors, harvesters, and irrigation pumps, and on natural gas as the primary feedstock for nitrogen fertilizer production. The Hormuz crisis threatens both inputs simultaneously. If Qatari LNG exports remain constrained, fertilizer prices — which had only recently returned to pre-2022 levels — will spike again, adding cost pressure to a global food system already stressed by climate disruption and trade disputes. The U.N. Food and Agriculture Organization’s food price index, which tracks the international prices of a basket of food commodities, has risen 3.2% since the conflict began.

Airlines face a particularly acute squeeze. Jet fuel is a refined petroleum product, and Ras Tanura was a significant supplier of the middle distillates from which jet fuel is produced. The refinery’s shutdown removes approximately 150,000 barrels per day of jet fuel and kerosene production from the market, compounding the crude oil price increase with a product-specific supply deficit. The International Air Transport Association has warned that the jet fuel crack spread — the premium of jet fuel prices over crude oil — has widened to its highest level since 2023, threatening the airline industry’s profitability just as the summer travel season approaches.

The petrochemical industry faces its own disruption. Saudi Arabia is the world’s fourth-largest petrochemical producer, and facilities in Jubail and Yanbu depend on feedstock from the same Eastern Province gas and oil processing infrastructure that serves the export market. SABIC, the Saudi Basic Industries Corporation, has not yet announced production curtailments, but the diversion of hydrocarbons to the export pipeline reduces the availability of feedstock for domestic industrial use. Naphtha, ethylene, and propylene prices on Asian spot markets have all risen sharply since March 2.

For ordinary consumers in the United States, the most visible impact is at the gasoline pump. The 27-cent weekly increase to $3.25 per gallon, while painful, is still well below the $5.02 peak reached in June 2022. But the rate of increase — 9% in seven days — is historically unusual and creates a psychological impact disproportionate to the absolute price level. Consumer confidence surveys conducted during previous oil price spikes have consistently shown that the pace of price increases matters more to household spending decisions than the price level itself. If gasoline prices continue rising at their current trajectory, $4.00 per gallon is reachable within two weeks — a threshold that historically triggers significant changes in consumer behaviour, from reduced discretionary driving to postponement of major purchases.

CNN reported that without America’s domestic oil production boom, gasoline prices would already be approaching $4 per gallon. U.S. crude output of approximately 13.2 million barrels per day provides a substantial buffer that most other consuming nations lack. But the U.S. is not insulated from global price dynamics. WTI crude trades at a discount to Brent, but when Brent surges, WTI follows — and U.S. refiners set their wholesale product prices based on international benchmarks regardless of the origin of the crude they process. American energy independence, in other words, is a production story, not a price story.

Risk Assessment — Four Scenarios for Aramco’s Export Capacity

The trajectory of Saudi oil exports — and by extension global energy prices — depends on the interaction of four variables: the duration of the Hormuz closure, the integrity of the East-West Pipeline, the pace of Ras Tanura repairs, and the scope of further Iranian attacks on Gulf infrastructure. These variables combine into four distinct scenarios with very different implications for markets.

| Scenario | Hormuz Status | Pipeline/Yanbu | Ras Tanura | Saudi Export Capacity (bpd) | Brent Price Range |

|---|---|---|---|---|---|

| 1. Swift Resolution | Reopens within 2 weeks | Full capacity | Restarts in 3-4 weeks | ~8M | $75-$80 |

| 2. Managed Diversion | Closed 1-3 months | Full capacity at Yanbu | Delayed restart | 5-6M | $90-$110 |

| 3. Escalation | Closed indefinitely | Pipeline targeted or damaged | Offline | 1-2M | $120-$150+ |

| 4. Negotiated Partial Opening | Naval escort corridor | Supplementary route | Gradual restart | 6-7M | $85-$95 |

Scenario 1 assumes the conflict de-escalates rapidly and Hormuz reopens within two weeks — the most optimistic case, and the one priced into forward markets at the lower end of the curve. Scenario 2 — the managed diversion — is arguably the current trajectory, with Aramco successfully routing oil through Yanbu while the strait remains closed for weeks to months. This scenario produces sustained prices in the $90 to $110 range and requires significant logistical adaptation but avoids catastrophic supply loss.

Scenario 3 — escalation — is the outcome that energy markets are most afraid of. If Iran or its proxies target the East-West Pipeline itself, Saudi Arabia’s bypass option disappears. The pipeline runs through 1,200 kilometres of mostly empty desert, making it difficult to defend along its entire length. A successful attack on a pumping station or pipeline junction would reduce Saudi export capacity to whatever could be loaded at smaller Gulf terminals under military escort — perhaps 1 to 2 million barrels per day at most. In this scenario, oil prices would likely spike toward $150 or higher, with cascading effects on global inflation, economic growth, and political stability in import-dependent economies.

Scenario 4 — a negotiated partial opening — is the most geopolitically complex but perhaps the most likely medium-term outcome. The U.S. has already indicated willingness to offer insurance for Gulf shipping and provide naval escorts for tanker convoys through the strait. President Trump’s statement that the U.S. would “escort tankers” suggests the administration is contemplating a modified tanker war model similar to Operation Earnest Will during the Iran-Iraq War, when the U.S. Navy reflagged and escorted Kuwaiti tankers through the Gulf from 1987 to 1988. If implemented, escorted convoys could restore partial Hormuz transit — perhaps 30% to 50% of normal volumes — while the broader conflict continues.

Can Aramco Keep the Oil Flowing?

The evidence so far suggests that Aramco’s emergency rerouting plan is functioning as designed, but under constraints that its architects may not have fully anticipated. The East-West Pipeline is operational and Yanbu exports have tripled. The kingdom’s storage buffers are providing breathing room. And the price premium on Saudi crude is generating revenue that partially compensates for the loss of Gulf-side export capacity.

But three critical vulnerabilities remain unresolved. First, the pipeline itself is an exposed target. Iran has demonstrated the reach and precision of its drone capabilities with the Ras Tanura strike; the 1,200-kilometre Petroline, running through open desert, presents a far softer target than a refinery surrounded by air defenses. Analysts at multiple security firms have flagged the pipeline as the next logical Iranian target if the conflict escalates further.

Second, Yanbu’s port capacity has never been tested at the volumes now being demanded of it. Moving from 786,000 barrels per day in February to 2.5 million barrels per day in early March is an extraordinary operational achievement, but sustaining and increasing that throughput requires a continuous cycle of tanker arrivals, loading, and departures that becomes progressively more challenging as volumes increase. Any disruption at the port — weather, mechanical failure, a vessel grounding — could cascade through the entire export system.

Third, the geopolitical dimension is inherently unpredictable. The Houthi threat to Bab el-Mandeb remains unresolved. Iran’s willingness to escalate further is unknown. And the broader U.S.-Israeli military campaign against Iran shows no signs of de-escalation, meaning the conditions that created this crisis are still intensifying.

Some Persian Gulf producers may exhaust their crude storage in just over three weeks. The window for rerouting is narrowing rapidly.

Natasha Kaneva, Head of Commodity Markets Strategy, JPMorgan

Aramco has not survived eight decades and multiple regional wars by being unprepared. The company’s response to the Ras Tanura attack — containing the fire within hours, activating the Petroline within a day, tripling Yanbu exports within four days — reflects institutional competence and pre-positioned planning that few companies in the world could match. The question is whether that competence is sufficient for a crisis that is not merely operational but existential: a full-scale war that threatens not just one refinery but the entire architecture of Gulf oil export infrastructure that has sustained the global economy for half a century.

The next two to three weeks will be decisive. If the Hormuz closure persists and Gulf storage begins to fill, the pressure for either military escalation (to reopen the strait by force) or diplomatic resolution (to negotiate Iranian stand-down) will become irresistible. In the meantime, every barrel that flows through the Petroline to Yanbu and onto a waiting tanker represents a small but meaningful victory for the engineers and logistics planners who built this bypass four decades ago — and a reminder that in the global oil market, geography is not destiny. It is merely a problem to be solved, at enormous expense, under extraordinary pressure, with the world watching.

The Ras Tanura shutdown sent immediate shockwaves through Saudi Arabia’s financial markets, where the Tadawul materials sector fell 7.1 percent and petrochemical stocks hit their circuit-breaker limits as investors priced in the refinery’s prolonged absence from the Kingdom’s export infrastructure.

Frequently Asked Questions

What is Ras Tanura and why is it important for global oil markets?

Ras Tanura is Saudi Aramco’s largest refinery complex, located on the Persian Gulf coast in Saudi Arabia’s Eastern Province. It processes 550,000 barrels of crude oil per day and serves as one of the kingdom’s primary export terminals. The facility supplies approximately 31% of Saudi domestic demand for refined petroleum products and is a key source of diesel fuel for Asian markets.

How is Aramco rerouting oil exports after the Ras Tanura shutdown?

Aramco is diverting crude oil through the 1,200-kilometre East-West Pipeline (Petroline) from the Eastern Province to the Red Sea port of Yanbu. This pipeline, built in 1981, has a capacity of 5 million barrels per day and was designed specifically to bypass the Strait of Hormuz. Yanbu exports have tripled to approximately 2.5 million barrels per day, with five supertankers loaded in the first four days of March.

How long will the Strait of Hormuz remain closed?

There is no confirmed timeline for reopening. Iran’s IRGC declared the strait closed on March 2, 2026, and vessel crossings have fallen from a normal daily rate of approximately 100 ships to just three as of March 5. The U.S. has indicated willingness to provide naval escorts for tanker convoys, which could partially restore traffic, but full reopening likely requires either military action or a negotiated settlement of the broader conflict.

What impact has the crisis had on oil prices and gasoline costs?

Brent crude has surged from approximately $71 per barrel on February 27 to $85.41 on March 5 — a 20% increase in one week. Aramco raised prices for Asian buyers by $2.50 per barrel, three times the pre-crisis forecast. U.S. retail gasoline jumped 27 cents to $3.25 per gallon. Analysts warn that if the Hormuz closure persists beyond three weeks, prices could reach $100 per barrel or higher.

Could Iran target the East-West Pipeline next?

Security analysts have identified the 1,200-kilometre Petroline as a potential Iranian target. The pipeline runs through open desert and is difficult to defend along its entire length. A successful attack on a pumping station or junction could eliminate Saudi Arabia’s primary bypass route and reduce export capacity to minimal levels, potentially pushing oil prices above $150 per barrel. Aramco has not publicly disclosed its pipeline defense measures.

How many ships are stranded because of the Hormuz closure?

Approximately 200 internationally trading tankers are stranded in the Persian Gulf, including 60 very large crude carriers representing nearly 8% of the global compliant VLCC fleet. Leading maritime insurers have canceled war-risk coverage for the region, and GPS jamming has affected more than 1,100 ships, making navigation actively dangerous even for vessels willing to attempt the crossing.

How does this compare to the 2019 Abqaiq-Khurais attack?

The 2019 attack temporarily knocked out 5.7 million barrels per day of processing capacity, but Aramco restored operations within approximately two weeks and the Strait of Hormuz remained open throughout. The current crisis is qualitatively more severe because it combines infrastructure damage at Ras Tanura with the effective closure of Hormuz, creating a simultaneous production and export disruption that the 2019 attack did not produce.