JEDDAH — Saudi Arabia imports more than 80 percent of its food, and the single most important chokepoint for those supplies — the Strait of Hormuz — is now effectively closed. The Iran war that began on 28 February 2026 has not only sent oil prices surging past $80 a barrel, forced Aramco to reroute crude exports, and drained the missile interceptor stockpiles that protect the Kingdom; it has triggered something far more immediately dangerous for 36 million Saudi residents: the prospect that supermarket shelves could begin to empty within weeks rather than months.

The Kingdom maintains strategic wheat reserves covering roughly four months of consumption, and the Public Investment Fund’s overseas farmland portfolio spans six continents. Yet neither stockpiles nor foreign acreage can fully offset the logistical reality that more than 70 percent of all GCC food imports transit the Strait of Hormuz — the same 33-kilometre-wide passage that Iran’s Islamic Revolutionary Guard Corps has declared a no-go zone for commercial shipping since 1 March. For a nation that abandoned domestic wheat production barely a decade ago in order to conserve groundwater, the timing is brutally inconvenient. This is the story of Saudi Arabia’s most dangerous vulnerability, the multi-billion-dollar strategy designed to mitigate it, and the uncomfortable question of whether any of it is enough.

Table of Contents

- How Dependent Is Saudi Arabia on Food Imports?

- What Happens When the Strait of Hormuz Closes?

- Saudi Arabia’s Four-Month Countdown — Strategic Reserves Under Pressure

- The SALIC Gambit — Can Overseas Farmland Feed a Nation at War?

- Why Did Saudi Arabia Abandon Domestic Wheat Production?

- The Desert Farm Paradox — Center-Pivot Irrigation and the Water Trade-Off

- How Is Vision 2030 Addressing Food Security?

- The Gulf Food Resilience Matrix — Ranking GCC Vulnerability

- Will Saudi Arabia’s Food Prices Spiral Out of Control?

- The Contrarian Case — Saudi Arabia Is Better Prepared Than Anyone Thinks

- The Red Sea Lifeline — Why Jeddah May Matter More Than Dammam

- What Happens Next — Three Scenarios for Saudi Food Security

- Frequently Asked Questions

How Dependent Is Saudi Arabia on Food Imports?

Saudi Arabia imports between 80 and 85 percent of its total food requirements, according to data from the UN Food and Agriculture Organization and the Saudi General Food Security Authority (GFSA). The Kingdom has virtually no commercial rice production, zero tropical fruit cultivation, and limited vegetable farming concentrated in a handful of regions. For a population of 36 million — including approximately 13.4 million expatriate workers — the arithmetic of food dependency is stark.

USDA Foreign Agricultural Service data for the 2025/26 marketing year forecasts Saudi wheat imports at 3.1 million metric tons, barley imports at 4 million metric tons, rice imports at 1.5 million metric tons, and corn imports at approximately 4.5 million metric tons. Local wheat production covers roughly 1.1 million metric tons, meeting less than a quarter of domestic demand. The rest arrives on ships.

| Commodity | Domestic Production (MMT) | Imports (MMT) | Import Dependency (%) | Primary Sources |

|---|---|---|---|---|

| Wheat | 1.1 | 3.1 | 74% | Canada, EU, Australia, Black Sea |

| Barley | 0.0 | 4.0 | 100% | EU, Black Sea, Australia |

| Rice | 0.0 | 1.5 | 100% | India, Pakistan, Thailand |

| Corn | 0.0 | 4.5 | 100% | Argentina, Brazil, US |

| Poultry | 0.7 | 0.5 | 42% | Brazil, US, France |

| Red Meat | 0.1 | 0.3 | 75% | India, Brazil, Australia |

| Fresh Fruit | 0.4 | 1.8 | 82% | Egypt, South Africa, India |

The aggregate picture is one of a wealthy nation that chose, deliberately and rationally, to buy its food on global markets rather than drain its aquifers growing grain in the desert. That strategy made perfect sense when shipping lanes were open, global trade was functioning, and the Strait of Hormuz was a geographic feature rather than a military front line. As of March 2026, none of those conditions hold.

What makes Saudi Arabia’s position different from other import-dependent nations — Japan imports 60 percent of its calories, South Korea roughly 70 percent — is the concentration of supply routes. The majority of Saudi food imports arrive through just two corridors: the Strait of Hormuz via eastern ports (Dammam, Jubail) and the Red Sea via Jeddah Islamic Port. The first corridor is now closed. The second is carrying the entire burden.

What Happens When the Strait of Hormuz Closes?

The Strait of Hormuz handles approximately 21 percent of global petroleum trade and, less often discussed, roughly 70 percent of all food imports destined for GCC states. When Iran’s Islamic Revolutionary Guard Corps issued its prohibition on commercial shipping through the strait on 1 March 2026 — backed by anti-ship missile batteries on the Iranian coastline and a demonstrated willingness to fire on vessels — the immediate impact fell on energy markets. Brent crude surged 10 to 13 percent within 48 hours, reaching $80 to $82 per barrel, according to Bloomberg data. The food supply implications, however, are potentially more severe.

Approximately 33 percent of the world’s fertilizer supply transits the Strait of Hormuz, according to analysis by Janes Defence Intelligence. QatarEnergy’s Ras Laffan complex — the world’s largest LNG liquefaction and industrial facility — halted urea, ammonia, methanol, and related chemical production following Iranian drone strikes on the site. These chemicals are feedstocks for fertilizer production across Asia and Africa. The cascade effect means that even nations thousands of kilometres from the Gulf will feel the food security impact within months as fertilizer shortages drive up crop production costs globally.

For Saudi Arabia specifically, the Hormuz closure means that food shipments that would normally dock at the Kingdom’s eastern ports — King Abdulaziz Port in Dammam and Jubail Commercial Port — must now be rerouted around the Arabian Peninsula to Jeddah Islamic Port on the Red Sea coast. This adds approximately 10 to 14 days of transit time for ships originating from South and Southeast Asia, and significantly longer for vessels from Australia or the Black Sea region.

The rerouting creates a bottleneck. Jeddah Islamic Port, while the largest port in Saudi Arabia, was not designed to handle the full volume of the Kingdom’s eastern seaboard imports simultaneously. Port congestion, container dwell times, and cold-chain disruptions for perishable goods are all increasing. Goods that spoil quickly — bananas, fresh dairy, leafy vegetables — are particularly vulnerable. Residents in the Eastern Province have already reported grocery costs tripling for certain fresh produce items, according to Reuters.

The financial costs of rerouting are also significant. Maritime insurance premiums for Gulf-bound vessels have risen to their highest levels since the Iran-Iraq Tanker War of the 1980s. Lloyd’s of London war risk insurance for ships entering the Persian Gulf exceeded 2 percent of hull value in the first week of March — a tenfold increase from February. These costs are passed directly to importers and, ultimately, to consumers. A metric ton of wheat that cost $280 to deliver to Dammam in January now costs an estimated $340 to $360 when rerouted through Jeddah and trucked overland — a 20 to 30 percent logistics premium before any commodity price increase is factored in.

The closure also affects overland supply routes. Roughly 15 percent of Saudi food imports arrive via road through Jordan, Bahrain, and the UAE. The Bahrain causeway and UAE border crossings remain operational, but the broader regional disruption — closed airspace, diverted shipping, and the general fog of war — has slowed truck traffic and complicated customs processing. Turkey, which has become an increasingly important food trade partner for the Gulf states through its southeastern border crossings, has seen overland exports to Saudi Arabia slow by an estimated 25 percent due to security checks and route disruptions in Iraq and Jordan, according to the Turkish Exporters Assembly.

The cold chain — the refrigerated supply infrastructure that keeps perishable food safe from farm to supermarket — is under particular strain. Saudi Arabia’s cold storage capacity is concentrated at its ports and in major distribution centres. When imports shift from Dammam to Jeddah, the cold chain must stretch an additional 1,200 kilometres overland across desert terrain where summer temperatures exceed 50 degrees Celsius. Refrigerated trucking capacity is finite. The Saudi Food and Drug Authority has intensified inspections of perishable imports arriving via the rerouted supply chain, recognising that compromised cold chains create food safety risks on top of food supply risks.

Saudi Arabia’s Four-Month Countdown — Strategic Reserves Under Pressure

The General Food Security Authority maintains strategic wheat reserves equivalent to four months of national consumption, stored across a network of 14 silo branches operated by the National Grain Supply Company (SABIL). These facilities, located in major population centres and at key ports, hold a combined storage capacity of 3.5 million tons — a figure that increased 40 percent from 2.5 million tons in 2016 following a deliberate expansion programme.

Four months of wheat reserves sounds reassuring. It is not. The four-month figure covers only wheat — the Kingdom’s primary staple. Strategic reserves for rice, corn, barley, cooking oil, sugar, and dairy are significantly smaller, with some commodities carrying reserves of as little as six to eight weeks. The GFSA does not publicly disclose the precise reserve levels for non-wheat commodities, citing national security, but industry sources familiar with the authority’s operations told Bloomberg in early 2025 that overall food reserves across all categories average between two and three months.

There is also the consumption spike to account for. Wartime conditions change eating patterns. Panic buying — already visible in Riyadh, Dammam, and Jeddah supermarkets in the first week of March — accelerates the depletion of reserves. During the 2020 COVID-19 pandemic, Saudi Arabia experienced a 30 percent surge in grocery purchases within the first two weeks of lockdown, according to the Saudi Retailers Committee. A military conflict with missiles hitting Saudi cities is a far more intense trigger for hoarding behaviour.

| Commodity | Estimated Reserve (months) | Storage Network | Primary Risk Factor |

|---|---|---|---|

| Wheat/Flour | 4.0 | SABIL 14-branch silo network | Panic buying depletion |

| Rice | 2.5 | Port warehouses, private sector | 100% imported, long transit reroute |

| Barley (animal feed) | 2.0 | Regional warehouses | Livestock sector collapse risk |

| Cooking Oil | 2.0 | Refinery storage, private sector | Palm oil supply chain disruption |

| Sugar | 3.0 | Refinery storage | Brazil/India supply route changes |

| Dairy | 1.5 | Cold chain, domestic production | Imported feed dependency |

| Fresh Produce | 0.5 | Minimal — perishable | Immediate supply chain failure |

The mathematics of reserve depletion are unforgiving. If the Hormuz closure persists beyond six weeks — a scenario that market analysts at Goldman Sachs consider likely based on the current trajectory of the conflict, according to a Fortune report — Saudi Arabia will begin to face genuine shortages in non-wheat commodities. Fresh produce shortages are already materialising. Rice and cooking oil would follow. Only the wheat reserves provide a genuine multi-month buffer, and even those assume no acceleration in consumption.

The Saudi government has not publicly discussed rationing. But the GFSA activated its emergency food security protocol in the first 48 hours of the conflict, according to an Arab News report, and has been in daily coordination with the Kingdom’s largest food retailers — Tamimi Markets, Panda (owned by Savola Group), Carrefour Saudi Arabia, and Danube — to monitor stock levels and prevent hoarding.

The SALIC Gambit — Can Overseas Farmland Feed a Nation at War?

The Saudi Agricultural and Livestock Investment Company (SALIC), wholly owned by the Public Investment Fund, was created in 2009 with a singular mandate: ensure the Kingdom’s food supply by investing in agricultural assets abroad. Fifteen years and billions of dollars later, SALIC’s portfolio spans ten companies across seven countries, and the question of whether this sprawling empire can actually deliver food to Saudi Arabia when the shipping lanes are disrupted has never been more urgent.

SALIC’s international holdings include Continental Farms in Ukraine (100 percent owned), Meridian Agriculture in Australia (100 percent owned), a 75 percent stake in G3 Canada — one of North America’s largest grain handling companies — a 9.2 percent stake in India’s LT Foods (a major basmati rice producer), a 35 percent stake in Minerva Foods Australia, and significant positions in Saudi domestic food companies including Almarai (16.32 percent), Nadec (20 percent), and the National Aquaculture Group (42.4 percent).

On paper, this is an impressive portfolio. In practice, owning farmland in Ukraine, Australia, and Canada does not automatically mean grain arrives in Saudi ports when the Strait of Hormuz is closed. The grain still needs to be harvested, transported to an export terminal, loaded onto a ship, and sailed to a Saudi port — a process that takes weeks under normal conditions and significantly longer during a conflict that has disrupted global shipping routes, closed airspace across the Middle East, and sent maritime insurance premiums for Gulf-bound vessels to their highest levels since the Tanker War of the 1980s.

SALIC’s Ukrainian operations present the most immediate challenge. Continental Farms, which operates large-scale grain cultivation in Ukraine, has been functioning under wartime conditions since Russia’s 2022 invasion, but Black Sea export routes remain complicated. Canadian operations through G3 are more reliable — Canadian grain ships to the Gulf via the Atlantic, through the Suez Canal, and into the Red Sea, bypassing the Hormuz bottleneck entirely. This route remains functional, though transit times from Canada’s Pacific coast via the Panama Canal have increased due to congestion.

The critical limitation of SALIC’s model is that ownership of foreign farmland is not the same as ownership of a dedicated supply chain. SALIC’s investments give it priority access to commodities, but the logistics of moving those commodities to Saudi Arabia still depend on the same global shipping infrastructure that serves everyone else. When that infrastructure is disrupted, SALIC’s farms in Australia are no more useful than any other Australian farm — the bottleneck is not production but transportation.

Why Did Saudi Arabia Abandon Domestic Wheat Production?

Between the 1970s and the early 2000s, Saudi Arabia pursued one of the most ambitious agricultural self-sufficiency programmes in history. The Kingdom became the world’s sixth-largest wheat exporter by the 1990s, growing millions of tons of grain in the desert using centre-pivot irrigation fed by non-renewable fossil aquifers. The achievement was genuine — and ecologically catastrophic.

Saudi Arabia was draining the Saq and Wajid aquifer systems at rates that exceeded natural recharge by a factor of more than ten, according to hydrogeological assessments conducted by the Saudi Geological Survey and later cited by the World Bank. These aquifers — formed over tens of thousands of years — were being emptied in decades. Water tables in the Wadi As-Sirhan basin, once the breadbasket of Saudi agriculture, dropped by more than 200 metres in some locations between 1980 and 2005.

In 2008, the Saudi government made the strategically rational decision to phase out domestic wheat production over eight years, completing the transition by 2016. The Grain Silos and Flour Mills Organisation (now SABIL) stopped purchasing domestically grown wheat, and farmers were incentivised to shift to less water-intensive crops or exit agriculture entirely. Domestic wheat production fell from a peak of over 4 million tons annually in the early 1990s to approximately 1.1 million tons by 2025 — a figure sustained only by smaller operations and limited government contracts.

The decision to abandon wheat self-sufficiency was endorsed by virtually every credible water policy expert who examined the data. Saudi Arabia chose food imports over aquifer depletion — a trade-off between short-term vulnerability and long-term survival. The Crown Prince Mohammed bin Salman’s Vision 2030 economic programme explicitly prioritised water conservation, and the agricultural phase-down was presented as a cornerstone of sustainable development.

Nobody anticipated, or at least nobody planned for, a scenario in which the primary import route would be closed by a military conflict. The 2008 decision assumed a functioning global trade system. In March 2026, that assumption has failed.

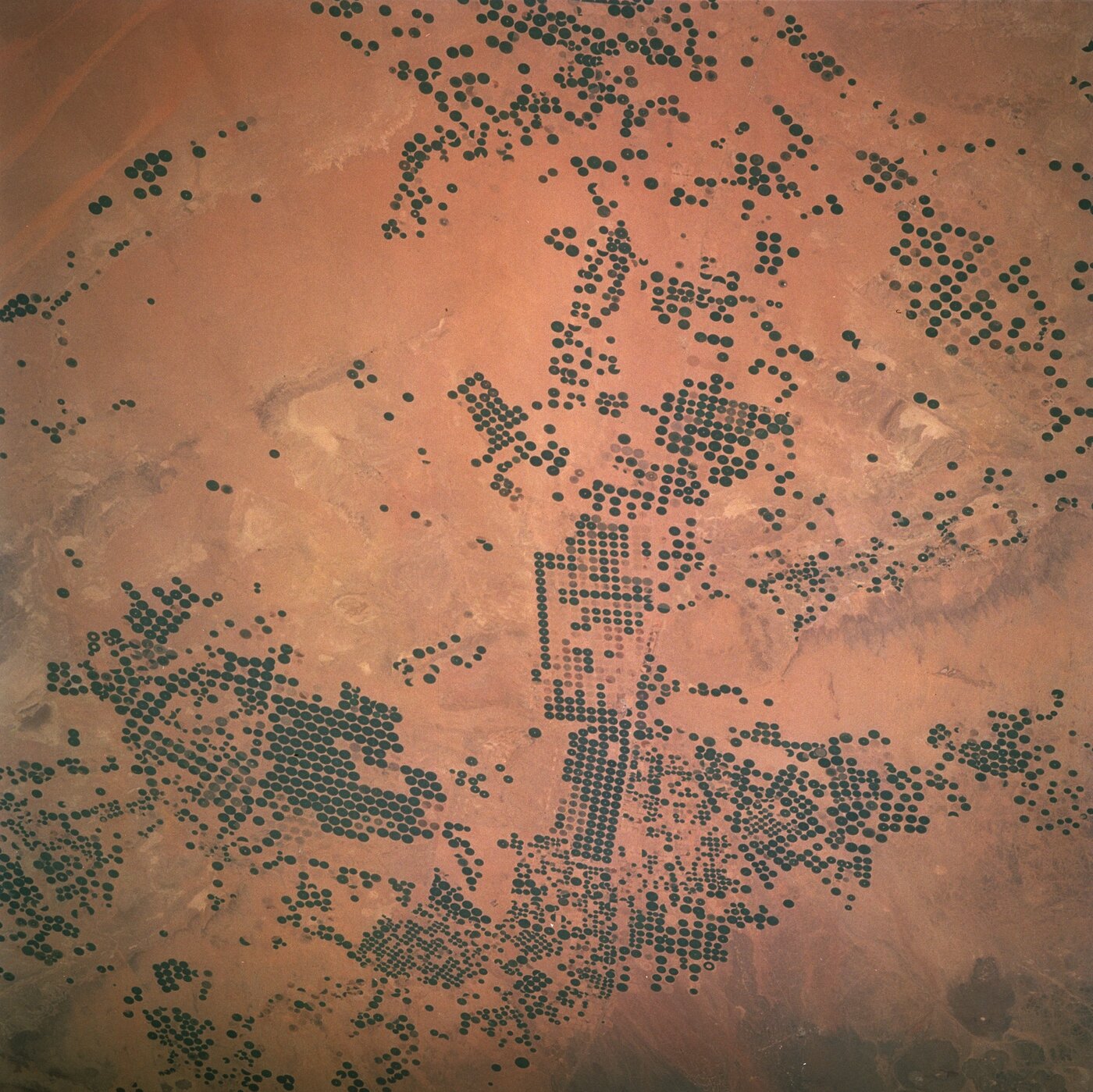

The Desert Farm Paradox — Center-Pivot Irrigation and the Water Trade-Off

Satellite imagery of Saudi Arabia reveals a striking pattern: thousands of green circles dotting the otherwise rust-coloured desert, each one a centre-pivot irrigation farm drawing water from deep underground. These circular farms, visible from space, represent both Saudi Arabia’s agricultural ingenuity and its fundamental resource constraint. Growing food in one of the most arid environments on Earth requires prodigious quantities of water — water that Saudi Arabia does not have in renewable supply.

Saudi Arabia’s annual renewable freshwater resources total approximately 2.4 billion cubic metres, according to the FAO’s AQUASTAT database — among the lowest per capita water availability figures on the planet. The Kingdom’s total water consumption exceeds 24 billion cubic metres annually, with agriculture historically consuming 80 to 85 percent of that total. The gap is filled by desalination (which produces roughly 7.5 million cubic metres per day, making Saudi Arabia the world’s largest desalination producer) and by drawing down fossil groundwater that will not be replenished within any meaningful human timeframe.

This is the desert farm paradox: Saudi Arabia could, in theory, restart large-scale wheat production and reduce its food import dependency. The infrastructure — the wells, the pivots, the centre-point systems — still exists in many locations. Some could be reactivated within months. But doing so would resume the depletion of aquifers that are already severely stressed, effectively trading a short-term food security problem for a long-term water security catastrophe.

The NEOM megaproject in the northwest, despite its current restructuring and construction suspension, included plans for advanced agricultural technology — vertical farms, AI-optimised greenhouses, and desalination-fed hydroponic systems. These technologies could eventually reduce water consumption per unit of food production by 90 percent or more. But “eventually” is not a timeline that addresses a food security crisis unfolding in real time.

A more immediate option is the expansion of greenhouse and protected agriculture in regions with relatively better water access — the Tabuk region in the northwest, Al-Jouf in the north, and parts of the Asir highlands in the southwest. These areas already produce significant quantities of tomatoes, cucumbers, peppers, and leafy greens under controlled conditions. The Saudi Ministry of Environment, Water and Agriculture reported that protected agriculture area exceeded 40,000 hectares by 2024, a significant increase from 12,000 hectares a decade earlier. But these operations produce fresh vegetables, not staple grains — the gap they fill is narrow.

How Is Vision 2030 Addressing Food Security?

Vision 2030’s National Industrial Development and Logistics Program (NIDLP) includes specific food security targets that were ambitious before the Iran war and now appear prescient. The programme aims to localise 85 percent of food processing in eleven domestic industrial clusters by 2030 — shifting from importing finished food products to importing raw commodities and processing them domestically. This does not reduce import dependency in tonnage terms, but it does reduce vulnerability to supply chain disruptions by ensuring that processing capacity, packaging, and distribution infrastructure remain within Saudi borders.

The Public Investment Fund has committed substantial capital to food and agriculture ventures. PIF’s food and agriculture portfolio includes SALIC (overseas farming), the National Grain Company (50 percent owned, managing domestic grain logistics), Almarai (one of the world’s largest vertically integrated dairy companies), and a joint venture with the American company AeroFarms to build indoor vertical farms across the Middle East and North Africa.

Green Dunes, a vertical farming venture supported by PIF through the food retailer Tamimi Markets, uses 95 percent less water than conventional agriculture and can produce leafy greens, herbs, and berries year-round without soil or sunlight. The Saudi government’s target for vertical farming production has not been publicly quantified, but industry analysts at the World Economic Forum estimated in February 2025 that Gulf states collectively plan to invest $2 billion in controlled environment agriculture by 2030.

Aquaculture is another pillar. Saudi Arabia’s fisheries and aquaculture production increased 55.56 percent in 2023, surpassing 140,000 tonnes, according to the Ministry of Environment, Water and Agriculture. SALIC’s 42.4 percent acquisition of the National Aquaculture Group in 2023 signalled the Kingdom’s intention to scale marine protein production dramatically. The NIDLP target of 600,000 tonnes of aquaculture production by 2030 would, if achieved, make Saudi Arabia a significant player in farmed seafood — reducing red meat import dependency.

The livestock sector represents both a strength and a vulnerability within the Vision 2030 food framework. Saudi Arabia’s poultry industry — concentrated around major producers like Al-Watania and Fakieh — produces approximately 700,000 tonnes of chicken meat annually, meeting roughly 58 percent of domestic demand. This is one of the highest food self-sufficiency rates in the Saudi economy. But poultry production depends entirely on imported corn and soybean meal for feed. If the Hormuz closure disrupts feed grain imports for more than two months, domestic poultry production could fall by 30 to 40 percent — turning a relative strength into an acute shortage.

Dairy tells a similar story. Almarai, one of the world’s largest integrated dairy companies and a PIF portfolio company, operates massive dairy farms in Saudi Arabia with herds exceeding 190,000 cattle. The milk is produced domestically, but the cows eat imported alfalfa and compound feed. Saudi Arabia abandoned domestic alfalfa production in 2019 as part of the same water conservation strategy that ended wheat farming. Almarai sources alfalfa from the United States, Argentina, and East Africa — supply chains that now face the same Hormuz disruption as grain imports.

The problem with all of these initiatives is timescale. Vertical farms, aquaculture expansions, and food processing clusters are multi-year infrastructure projects. They will improve Saudi food resilience by 2030 or 2032. They do nothing for the crisis unfolding in March 2026. The war has arrived before the strategy matured — a timing gap that no amount of PIF capital can close retroactively.

The wealthy Gulf states are facing their biggest food security challenge since the 2008 global food crisis, as the Iran conflict threatens ports and disrupts shipping through the Strait of Hormuz.

Reuters, March 2026

The Gulf Food Resilience Matrix — Ranking GCC Vulnerability

Not all Gulf states face the same level of food supply risk from the Hormuz closure. Five factors determine a nation’s resilience: import dependency ratio, strategic reserve depth, availability of alternative supply routes, domestic production capacity, and financial buffer to absorb price surges. Scoring each GCC state across these dimensions reveals a hierarchy of vulnerability that defies simple assumptions.

| Country | Import Dependency | Reserve Depth (months) | Alt. Supply Routes | Domestic Production | Financial Buffer | Overall Score (/50) | Vulnerability |

|---|---|---|---|---|---|---|---|

| Saudi Arabia | 7/10 | 7/10 | 8/10 | 4/10 | 9/10 | 35 | Moderate |

| UAE | 8/10 | 7/10 | 5/10 | 3/10 | 9/10 | 32 | Moderate-High |

| Qatar | 9/10 | 5/10 | 3/10 | 2/10 | 10/10 | 29 | High |

| Kuwait | 9/10 | 4/10 | 4/10 | 2/10 | 8/10 | 27 | High |

| Bahrain | 9/10 | 3/10 | 3/10 | 1/10 | 5/10 | 21 | Very High |

| Oman | 7/10 | 4/10 | 6/10 | 5/10 | 5/10 | 27 | High |

The scoring reveals several counterintuitive findings. Saudi Arabia, despite importing over 80 percent of its food, scores the highest resilience among GCC states — driven primarily by two factors. First, the Kingdom possesses the deepest strategic reserves in the Gulf, with four months of wheat and two to three months of other staples. Second, and more importantly, Saudi Arabia has a functioning Red Sea coastline with major port infrastructure at Jeddah and Yanbu that entirely bypasses the Strait of Hormuz. No other Gulf state has a comparable alternative maritime route.

Qatar emerges as the most paradoxically vulnerable. Despite possessing the highest GDP per capita in the world and effectively unlimited financial resources, Qatar is a small peninsula connected to Saudi Arabia by a single land border and surrounded by waters that are now a conflict zone. Its food imports arrive almost exclusively through Hormuz. The 2017 blockade by Saudi Arabia, the UAE, and Bahrain demonstrated Qatar’s logistical vulnerability; the 2026 Hormuz closure is an order of magnitude more severe.

The UAE’s score reflects a tension between Dubai’s role as a global logistics hub — with extensive air freight capacity and Jebel Ali, the largest port in the Middle East — and the reality that much of its food import infrastructure faces the Persian Gulf and the now-closed Hormuz strait. The UAE has stated that its strategic reserves cover four to six months, according to government announcements reported by Gulf News. If accurate, this is the strongest reserve position in the GCC.

Bahrain’s position is the most precarious. The island nation has negligible domestic production, minimal reserves, limited port capacity, and depends heavily on the King Fahd Causeway to Saudi Arabia for overland food supplies. If Saudi Arabia itself faces supply constraints, Bahrain’s lifeline narrows further.

The financial buffer dimension is critical because price surges can be absorbed by wealthy governments through subsidies, market interventions, and direct distribution. Saudi Arabia and Qatar, with sovereign wealth funds exceeding $900 billion and $500 billion respectively, can afford to buy food at any price. Poorer nations in the region — Jordan, Egypt, Yemen — face a far grimmer calculation. The Iran war’s food security impact will fall hardest on those who can least afford it.

Will Saudi Arabia’s Food Prices Spiral Out of Control?

Retail food prices in Saudi Arabia rose an estimated 8 to 12 percent in the first week following the Hormuz closure, according to anecdotal reports from retailers and early data compiled by the Saudi Retailers Committee. The increase is not uniform: staple commodities with deep reserves (bread, flour, pasta) have seen modest increases of 3 to 5 percent, while fresh produce and imported dairy products have spiked 15 to 30 percent. Bananas, which Saudi Arabia imports almost entirely from the Philippines and Latin America via sea routes, are among the first casualties — prices in some Riyadh supermarkets tripled within days.

The Saudi government maintains a system of price controls and subsidies on essential commodities, administered through the Ministry of Commerce and the GFSA. Bread prices are effectively fixed. Rice, sugar, and cooking oil are subject to soft price ceilings that the Ministry enforces through supplier agreements and the implicit threat of regulatory action. These mechanisms can contain price increases for weeks or months, but they cannot override the underlying supply-demand reality indefinitely.

Global commodity markets are amplifying the domestic pressure. Wheat futures on the Chicago Board of Trade rose 14 percent in the first week of March. Rice prices, already elevated due to India’s export restrictions in 2023 and 2024, surged a further 9 percent. Cooking oil — palm oil from Malaysia and Indonesia, sunflower oil from the Black Sea region — saw double-digit price increases as traders priced in extended Hormuz disruption.

The fertilizer dimension adds a delayed-action price shock. With 33 percent of global fertilizer supply transiting the Hormuz strait and Qatar’s urea production halted, the world faces a fertilizer shortage that will not manifest in food prices for three to six months — when the next crop cycle depends on inputs that are no longer flowing. This means that even if the Hormuz closure ends tomorrow, food prices globally will remain elevated through late 2026 as reduced fertilizer availability constrains harvests in Asia, Africa, and Latin America.

For Saudi Arabia’s 13.4 million expatriate workers — many of whom earn wages that leave minimal margin for food price increases — the crisis is acute. The Saudi royal family is aware that food price inflation is historically one of the most potent triggers of social unrest across the Middle East. The Arab Spring of 2011 was ignited in part by bread prices. Crown Prince Mohammed bin Salman’s government has every incentive to prevent a repeat — and the financial resources to do so, at least for several months.

The Contrarian Case — Saudi Arabia Is Better Prepared Than Anyone Thinks

The prevailing narrative — that Saudi Arabia is dangerously vulnerable to food supply disruption — contains a significant analytical blind spot. It treats the Kingdom’s 80-percent import dependency figure as evidence of fragility, when the more relevant metric is the Kingdom’s ability to manage that dependency through crisis.

Several factors suggest that Saudi Arabia’s food security position, while under genuine stress, is substantially more resilient than the headline import figure implies.

The Red Sea advantage is the single most important variable that most analyses underweight. Jeddah Islamic Port is the largest port in Saudi Arabia and the fourth-largest in the Middle East. It handles approximately 6.5 million twenty-foot equivalent units (TEUs) annually and has direct maritime connections to Egypt, East Africa, India’s western coast, and the Mediterranean via the Suez Canal. None of these routes transit the Strait of Hormuz. For commodities sourced from Europe, Africa, and the Americas — which collectively supply a significant share of Saudi wheat, corn, and sugar imports — the Hormuz closure is logistically irrelevant. The ships never go through Hormuz in the first place.

Saudi Arabia’s land borders also provide alternative supply corridories that are often overlooked. The Kingdom shares a border with Jordan, which serves as a transit corridor for Turkish and European goods. The King Fahd Causeway connects to Bahrain, and road links through the UAE and Oman provide additional overland options — though these are themselves affected by the broader regional disruption. Nevertheless, the Saudi Transport General Authority reported that approximately 15 percent of food imports arrive by road under normal conditions, and this percentage is likely to increase as the Hormuz closure redirects supply flows.

The financial dimension is decisive. Saudi Arabia’s foreign exchange reserves exceeded $450 billion in early 2026, according to Saudi Arabian Monetary Authority data. The Kingdom can afford to pay premium prices for food, charter dedicated shipping, and if necessary, airlift critical commodities. During the early weeks of the conflict, Saudia Cargo — the freight division of the national airline — has reportedly begun transporting high-value perishable foods by air from India and East Africa, a prohibitively expensive option that only a wealthy state can sustain.

Finally, Saudi Arabia’s domestic food production, while modest as a share of total consumption, is not negligible. Almarai — one of the world’s largest dairy companies, partly owned by PIF — produces approximately 3.5 billion litres of dairy products annually from domestic herds. NADEC produces dairy, juice, and agricultural products. The National Aquaculture Group farms shrimp and fish domestically. Saudi Fisheries operates along the Red Sea and Gulf coasts. These companies provide a floor of domestic protein and dairy production that would continue even if all imports ceased — not enough to feed the nation, but enough to prevent the most extreme crisis scenarios.

There is also a geopolitical advantage that is rarely discussed in food security analyses. Saudi Arabia maintains strong bilateral relationships with many of the world’s largest food-exporting nations — Brazil, India, Australia, Argentina, and Canada — and these relationships are backed by significant Saudi investment in those countries’ agricultural sectors. When supply is constrained, relationships and investment ties translate into preferential access. SALIC’s 75 percent ownership of G3 Canada means that Saudi Arabia effectively controls one of North America’s largest grain export channels. In a competition for scarce shipping capacity, that kind of structural advantage matters far more than spot market purchasing power alone.

The Kingdom’s experience during the COVID-19 pandemic also provides a template. In March and April 2020, Saudi Arabia successfully managed a 30 percent surge in food demand without significant shortages, deploying a combination of strategic reserve drawdowns, emergency procurement, and retailer coordination that kept supermarket shelves stocked while many other nations struggled. The institutional capacity built during that crisis — the GFSA’s monitoring systems, the retailer coordination protocols, the logistics flexibility — is being reactivated for the Hormuz crisis. The 2020 playbook is not a perfect fit for 2026, but the muscle memory exists.

Saudi Arabia chose food imports over aquifer depletion — a trade-off between short-term vulnerability and long-term survival. The 2008 decision assumed a functioning global trade system. In March 2026, that assumption has failed.

Editorial analysis

The Red Sea Lifeline — Why Jeddah May Matter More Than Dammam

The Hormuz crisis has fundamentally reordered Saudi Arabia’s port hierarchy. Under normal conditions, King Abdulaziz Port in Dammam handles the majority of containerised imports for the Eastern Province and central regions, while Jeddah Islamic Port serves the western coast and Hajj-related logistics. The Hormuz closure has made Jeddah the Kingdom’s primary lifeline — a role for which it was not fully optimised but is proving capable of filling.

Jeddah Islamic Port’s strategic advantage is geographic: it sits on the Red Sea, connected to global shipping lanes via the Suez Canal to the north and the Bab el-Mandeb strait to the south. Neither passage is affected by the Iran-US conflict. The port handled over 5.7 million TEUs in 2024 and has undergone significant expansion under Vision 2030’s National Transport and Logistics Strategy, including the development of a new fourth terminal by DP World and the expansion of cold-chain storage facilities.

The Saudi government has activated emergency port protocols that prioritise food and medical supply vessels at Jeddah, according to industry sources cited by Baird Maritime. Container ships carrying non-essential cargo — consumer electronics, automobiles, construction materials — are being held in anchorage while food-laden vessels receive priority berthing. This triage system, while disruptive to the broader economy, ensures that the food supply chain receives maximum port capacity.

Yanbu Commercial Port, Saudi Arabia’s second Red Sea port located approximately 300 kilometres north of Jeddah, is also absorbing diverted cargo. Yanbu handled 590,000 TEUs in 2024 and has bulk commodity facilities suited to grain and agricultural imports. The Saudi Ports Authority has reportedly increased staffing and extended operating hours at both Jeddah and Yanbu to manage the surge in diverted traffic.

An overland bridge is also emerging. Container and bulk cargo arriving at Jeddah is being trucked across the Kingdom to eastern cities — Riyadh, Dammam, and the industrial cities of the Eastern Province — via the Kingdom’s well-maintained highway network. The roughly 1,200-kilometre Jeddah-to-Dammam corridor is one of Saudi Arabia’s most heavily trafficked freight routes, and the Royal Commission for Riyadh City has expedited permits for additional trucking capacity.

The same East-West pipeline infrastructure that Crown Prince Mohammed bin Salman is using to reroute oil exports has a food supply parallel: the Kingdom’s internal logistics network, built over decades to connect its dispersed population centres, is proving adaptable to the wartime redirection of supply flows. The pipeline carries oil west; the highways carry food east. Both are lifelines.

What Happens Next — Three Scenarios for Saudi Food Security

The trajectory of Saudi Arabia’s food security crisis depends almost entirely on one variable: how long the Strait of Hormuz remains closed to commercial shipping. Three scenarios frame the range of outcomes.

Scenario One — Hormuz Reopens Within Four Weeks (Probability: 25-30%)

If a ceasefire or de-escalation allows commercial shipping to resume through the strait within approximately 30 days, Saudi Arabia’s food supply system will experience disruption but not crisis. Strategic reserves remain adequate. Price increases of 10 to 20 percent across most food categories would gradually reverse. The Red Sea rerouting adds costs but does not break the supply chain. Fresh produce shortages ease as shipping normalises. This is the scenario Goldman Sachs analysts have characterised as the market’s base case for a short war, though intelligence assessments from the US and UK suggest longer timelines are more probable.

Scenario Two — Hormuz Closed for Two to Four Months (Probability: 40-45%)

An extended closure of two to four months — aligning with the conflict timeline that Pentagon planners have discussed, according to multiple media reports — would exhaust non-wheat strategic reserves and force Saudi Arabia to rely heavily on Red Sea imports, overland routes, and emergency air freight. Food prices would rise 25 to 40 percent across the board, with fresh produce and dairy seeing the largest increases. The Saudi government would likely implement informal rationing through purchase limits at major supermarket chains, as several Gulf states did during COVID-19. The livestock sector, dependent on imported barley and corn for animal feed, would face the most severe stress — potentially leading to herd culling and long-term reduction in domestic dairy and meat capacity. PIF’s financial reserves would absorb the cost, but the economic impact on lower-income expatriate households would be severe.

Scenario Three — Prolonged Closure Beyond Four Months (Probability: 20-25%)

A Hormuz closure lasting beyond four months — possible if the conflict escalates further or if Iran’s mining and missile capabilities prevent safe transit even after hostilities decrease — would constitute the most serious food security challenge in Saudi Arabia’s modern history. Wheat reserves would begin to deplete. The Kingdom would need to consider emergency measures including large-scale government food distribution, mandatory rationing, and potentially the reactivation of dormant agricultural infrastructure despite the water cost. International humanitarian supply chains — the kind more typically associated with conflict zones in Africa or the Middle East — might need to be activated. This scenario is unlikely but not impossible, and the GFSA’s emergency planning includes provisions for it.

| Scenario | Hormuz Closure Duration | Price Impact | Reserve Status | Government Response Required | Probability |

|---|---|---|---|---|---|

| Short Disruption | 0-4 weeks | 10-20% | Adequate across all commodities | Price monitoring, retailer coordination | 25-30% |

| Extended Closure | 2-4 months | 25-40% | Non-wheat reserves depleted | Purchase limits, emergency imports, subsidies | 40-45% |

| Prolonged Crisis | 4+ months | 50-80% | All reserves under pressure | Rationing, agricultural reactivation, humanitarian aid | 20-25% |

Across all three scenarios, one conclusion remains constant: Saudi Arabia’s decision to build strategic reserves, invest in overseas farmland, develop Red Sea port infrastructure, and maintain a highway network connecting its population centres has provided meaningful — if imperfect — resilience. The Kingdom is not facing famine. It is facing a logistics crisis that its considerable financial resources and institutional infrastructure can manage, provided the disruption does not exceed the outer bounds of current planning assumptions.

The deeper lesson is systemic. Saudi Arabia made a rational decision in 2008 to prioritise water conservation over food self-sufficiency. That decision was correct on its own terms. But it was made in a world where the Strait of Hormuz was a trade route, not a battlefield. The Iran war has exposed the hidden cost of that trade-off — and no nation that imports 80 percent of its food through a single chokepoint can consider itself fully secure, regardless of how many overseas farms it owns or how many silos it builds.

For the Kingdom’s leadership and for Crown Prince Mohammed bin Salman personally, the food security crisis adds yet another dimension to a war that was supposed to neutralise Iran’s nuclear ambitions but has instead unleashed cascading risks across every sector of Saudi national life — from the Crown Prince’s legacy to the empty shelves in a Dammam supermarket where a Filipino construction worker is trying to buy rice.

Frequently Asked Questions

How much food does Saudi Arabia import?

Saudi Arabia imports between 80 and 85 percent of its total food requirements, including 100 percent of its rice, barley, and corn, approximately 74 percent of its wheat, and more than 75 percent of its red meat. The Kingdom’s total food import bill exceeded $25 billion annually before the 2026 conflict.

How long can Saudi Arabia’s food reserves last?

Saudi Arabia’s strategic wheat reserves cover approximately four months of national consumption, stored across 14 silo branches with a combined capacity of 3.5 million tons. Non-wheat commodity reserves — rice, cooking oil, sugar — average two to three months. Fresh produce has virtually no strategic reserve due to its perishable nature.

Does the Strait of Hormuz closure affect all Saudi food imports?

The Hormuz closure directly affects imports arriving at Saudi Arabia’s eastern ports of Dammam and Jubail, which handle a significant share of containerised food imports. However, Jeddah Islamic Port on the Red Sea operates independently of the Hormuz strait, and a substantial volume of imports from Europe, Africa, and the Americas routes through Jeddah via the Suez Canal, bypassing the conflict zone entirely.

What is SALIC and how does it protect Saudi food security?

The Saudi Agricultural and Livestock Investment Company (SALIC) is a PIF-owned entity that invests in overseas agricultural assets to secure food supply chains for the Kingdom. SALIC owns farmland in Ukraine, Australia, and Canada, holds a 75 percent stake in Canadian grain handler G3, and has investments in companies across seven countries. While it provides priority commodity access, its effectiveness depends on functioning global shipping infrastructure.

Could Saudi Arabia restart domestic wheat production?

Saudi Arabia could reactivate some dormant centre-pivot irrigation infrastructure to increase domestic wheat output, but this would resume the depletion of non-renewable fossil aquifers — the same environmental crisis that prompted the Kingdom to phase out domestic production between 2008 and 2016. Restarting large-scale desert agriculture would provide short-term food security at the cost of long-term water security.

How do Saudi food prices compare to pre-war levels?

Retail food prices in Saudi Arabia rose an estimated 8 to 12 percent in the first week following the Hormuz closure, with fresh produce and imported dairy seeing increases of 15 to 30 percent. Banana prices tripled in some locations. Staple commodities with deep reserves, such as bread and flour, have seen more modest increases of 3 to 5 percent, helped by government price controls and subsidies.

Which GCC country is most vulnerable to food supply disruption?

Bahrain is the most vulnerable GCC state, with near-total food import dependency, minimal strategic reserves, no alternative maritime route bypassing the Hormuz strait, and limited financial buffers compared to wealthier neighbours. Qatar, despite its immense wealth, also faces high vulnerability due to its geographic position and near-total reliance on Hormuz-transiting shipping for food imports.