DHAHRAN — Saudi Arabia can produce 12 million barrels of oil per day. It has the wells, the processing plants, and the workforce to sustain that output for at least a year without additional investment. Yet three weeks into the Iran war, roughly half the kingdom’s production sits stranded — pumped from the ground but unable to reach the tankers that would carry it to the refineries in Yokohama, Mumbai, and Rotterdam that are running dry. The world’s most celebrated energy insurance policy has been exposed as a promise that cannot be kept.

For fifty years, the concept of Saudi spare capacity has underpinned global energy security. When crises erupted — the Iraqi invasion of Kuwait, the Libyan civil war, the Russian invasion of Ukraine — markets calmed themselves with a single reassurance: Riyadh can always open the taps. That assumption was never wrong. It was simply never tested under conditions where the oil could be produced but not delivered. The 2026 Iran war has provided that test, and the result is a systemic failure of the energy security architecture that every major economy relies upon.

The numbers are stark. The Strait of Hormuz, through which 20 million barrels of oil transited daily before February 28, now carries less than 10 percent of that volume. Saudi Arabia’s East-West Pipeline — the Petroline, built in the 1980s for exactly this scenario — can move 7 million barrels per day to the Red Sea port of Yanbu. But Yanbu’s loading terminals can handle only 4.5 million barrels on a good day, and on March 22, Aramco suspended oil loading operations at Yanbu after Iranian missiles struck the nearby SAMREF refinery. The world’s backup plan has a backup plan, and that backup plan just failed.

Table of Contents

- What Is Saudi Arabia’s Spare Oil Production Capacity?

- Why Can’t Saudi Arabia Export the Oil It Produces?

- The Petroline Bottleneck — 7 Million Barrels and a Port That Cannot Keep Up

- How Much Oil Has the World Lost Since Hormuz Closed?

- Did the IEA Strategic Reserve Release Work?

- The Oil Delivery Vulnerability Matrix

- What Is the UAE Doing to Bypass Hormuz?

- The 1973 Myth — Why the Post-OPEC Energy Security Model Was Built on Sand

- Can Russia and Non-OPEC Producers Fill the Gap?

- What Comes After the Strait — The New Energy Geography

- How Is Saudi Arabia Adapting Its Oil Export Strategy?

- Frequently Asked Questions

What Is Saudi Arabia’s Spare Oil Production Capacity?

Saudi Arabia’s spare oil production capacity — the volume it can bring online within 90 days and sustain for at least a year — stands at approximately 2 to 3 million barrels per day. This figure represents the difference between Aramco’s maximum sustainable capacity of 12 million barrels per day, confirmed by CEO Amin Nasser in October 2025, and its current production rate of roughly 9 to 10 million barrels per day under OPEC+ quota agreements.

That spare capacity is the largest held by any single country in the world, and it is not close. The entire OPEC+ alliance collectively maintains approximately 3.5 million barrels per day of spare capacity, according to the International Energy Agency’s March 2026 Oil Market Report. Saudi Arabia accounts for roughly 70 percent of that buffer. The United Arab Emirates holds most of the remainder, with other OPEC members effectively producing at or near their maximum sustainable output.

The strategic significance of this capacity has been central to global energy markets for decades. When Iraq invaded Kuwait in 1990 and removed 5 million barrels per day from the market overnight, Saudi Arabia ramped production from 5.4 million to 8.5 million barrels per day within months. When Libyan output collapsed during the 2011 civil war, Saudi Arabia again stepped in. The pattern was consistent: crisis erupts, markets panic, Riyadh opens the taps, prices stabilise.

In January 2024, Saudi Arabia’s Energy Ministry instructed Aramco to abandon a planned expansion to 13 million barrels per day and revert to the longstanding 12 million barrel target. The decision was widely interpreted as fiscal prudence — why invest billions in capacity that might never be used? In hindsight, even 13 million barrels per day would not have solved the problem the kingdom now faces. The bottleneck is not underground. It is at the water’s edge.

Why Can’t Saudi Arabia Export the Oil It Produces?

Saudi Arabia cannot export much of the oil it produces because the infrastructure required to move crude from its eastern oil fields to open water was designed around a chokepoint that Iran now controls. Before February 28, approximately 7.5 million barrels per day of Saudi crude left the kingdom through terminals on the Persian Gulf coast — Ras Tanura, Ju’aymah, and Ras al-Khair — all of which require tankers to transit the Strait of Hormuz to reach international markets.

The Strait of Hormuz is 21 nautical miles wide at its narrowest point. Two shipping lanes, each two miles wide, separated by a two-mile buffer zone, accommodate roughly 70 to 80 tanker transits per day under normal conditions. Since Iran’s Islamic Revolutionary Guard Corps Navy imposed its selective blockade in the first week of March, transit volume has collapsed by more than 95 percent, according to tanker tracking data from Kpler. The few vessels that have passed through did so with Iranian approval under a new registration and vetting system that Tehran is developing on a case-by-case basis.

The only alternative route for Saudi crude is the East-West Pipeline — known as the Petroline — which runs 1,200 kilometres from the Abqaiq processing complex in the Eastern Province to the Red Sea port of Yanbu. Aramco activated this contingency within hours of the Hormuz closure, and by March 11, CEO Amin Nasser confirmed the pipeline was operating at full capacity of 7 million barrels per day after converting an accompanying natural gas liquids line to carry crude. In theory, this should have been enough. In practice, it was not.

The constraint is not the pipe. It is the port. Yanbu’s two export terminals — Yanbu North and Yanbu South — have a nominal combined loading capacity of approximately 4.5 million barrels per day, according to Argus Media. Market sources put the effective, operationally tested figure closer to 4 million barrels per day. Under wartime conditions, with tanker scheduling disruptions, insurance complications, and now the collapse of marine insurance coverage for Gulf loadings, the consultancy Vortexa estimated terminals could handle roughly 3 million barrels per day. In the first nine days of March, Yanbu averaged 2.2 million barrels per day — more than double its pre-war rate, but barely a quarter of Saudi Arabia’s total production capacity.

The Petroline Bottleneck — 7 Million Barrels and a Port That Cannot Keep Up

The East-West Crude Oil Pipeline was built during the Iran-Iraq War in the 1980s specifically to allow Saudi Arabian oil exports to bypass the tanker war raging in the Persian Gulf. It consists of two parallel lines: a 56-inch diameter main crude line and a 48-inch line originally designed for natural gas liquids. Together, when both carry crude, they can theoretically move 7 million barrels per day across the Arabian Peninsula.

This infrastructure was engineered for a scenario remarkably similar to the one Saudi Arabia now faces. King Fahd ordered the pipeline’s construction in 1981, at a time when Iranian attacks on Kuwaiti and Saudi-flagged tankers were disrupting Gulf oil exports. The pipeline was operational by 1987 and immediately redirected a significant portion of Saudi crude away from the Gulf coast. After the Iran-Iraq War ended, throughput gradually declined as Hormuz reopened. By the mid-2000s, the natural gas liquids line had been converted back to its original purpose, and the Petroline operated well below capacity.

The decision to maintain the pipeline rather than decommission it now appears prescient. The problem is that maintaining the pipeline is not the same as maintaining the export infrastructure at the other end. Yanbu was never designed to replace Ras Tanura and Ju’aymah, which together could handle over 10 million barrels per day of loadings. Yanbu was designed as a supplementary export point — an escape valve, not a main artery.

The Engineering News-Record published an analysis in March 2026 with a headline that captured the dilemma precisely: “Hormuz Bypass Infrastructure Was Sized for a Short Disruption. This Is Not That.” The article detailed how Yanbu’s storage capacity, berth availability, and tanker turnaround times all constrain throughput far below what the pipeline can deliver. On a busy day, a Very Large Crude Carrier takes 24 to 36 hours to load at Yanbu. The terminal can accommodate approximately 37 to 40 VLCCs per month — enough to export roughly 4 million barrels per day at maximum efficiency, but only if every berth is occupied, every tanker arrives on schedule, and no disruptions occur.

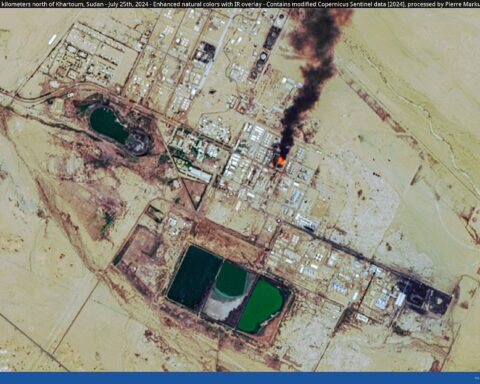

On March 22, that theoretical maximum became academic. Iranian ballistic missiles struck the SAMREF refinery adjacent to the Yanbu terminal, forcing Aramco to suspend oil loading operations. The Red Sea — Saudi Arabia’s last functioning export corridor — is no longer a safe harbour. The kingdom can produce the oil. It can push it through the pipeline. It simply has nowhere left to put it on a ship. The SAMREF strike coincided with the March 22 missile and drone barrage on Riyadh, in which Saudi air defences intercepted sixty drones and three ballistic missiles in a single day’s operations, confirming that Iran can now coordinate simultaneous attacks on the kingdom’s energy infrastructure and its capital.

How Much Oil Has the World Lost Since Hormuz Closed?

The scale of supply disruption caused by the Hormuz closure is without precedent in the modern oil market. According to the IEA’s March 2026 Oil Market Report, global oil supply fell by approximately 8 million barrels per day in March — a figure that subsequently rose to at least 10 million barrels per day by mid-month as Iraq declared force majeure on all foreign-operated oil fields and Kuwait shut in production after Iranian drone strikes damaged critical loading infrastructure.

To contextualise this loss: the 1973 Arab oil embargo removed approximately 4.4 million barrels per day from the market. The Iranian Revolution of 1979 disrupted roughly 5.6 million barrels per day. Iraq’s invasion of Kuwait in 1990 took out approximately 4.3 million barrels per day. The 2026 Hormuz crisis has eclipsed all of them. The Dallas Federal Reserve described it as “the largest disruption to energy supply in the history of the global oil market.”

The supply lost is not evenly distributed geographically. Eighty-four percent of crude oil and condensate transiting the Strait of Hormuz in 2024 was destined for Asian markets, according to the U.S. Energy Information Administration. Japan, South Korea, India, and China are the most exposed. Japan imports approximately 90 percent of its crude oil through the Strait. South Korea imports roughly 70 percent. India faces what economists describe as a dual physical and financial shock — more than half its LNG imports originate from the Gulf, and a significant portion of its crude contracts are Brent-indexed, meaning prices surge even for barrels that do not transit Hormuz.

| Crisis | Year | Supply Lost (M bpd) | Duration | Peak Oil Price | Recovery Mechanism |

|---|---|---|---|---|---|

| Arab Oil Embargo | 1973-74 | 4.4 | 6 months | $12 ($56 adj.) | Diplomacy, demand destruction |

| Iranian Revolution | 1978-79 | 5.6 | ~12 months | $40 ($148 adj.) | Saudi spare capacity ramp-up |

| Iraq-Kuwait War | 1990-91 | 4.3 | ~9 months | $46 | Saudi spare capacity + IEA release |

| Libya Civil War | 2011 | 1.5 | ~8 months | $127 | Saudi spare capacity + IEA release |

| Russia-Ukraine War | 2022 | ~1.0 | Ongoing | $128 | SPR release + rerouting |

| Iran War / Hormuz | 2026 | 8-10+ | Ongoing (23 days) | $126 | SPR release + Petroline (insufficient) |

The table reveals a pattern that energy security planners failed to anticipate. Every previous crisis was resolved through some combination of Saudi spare capacity deployment and coordinated strategic reserve releases. The 2026 crisis is the first in which spare capacity exists but cannot reach the market, and strategic reserves — while deployed at record scale — are being drawn down at a rate that renders them a stopgap measured in weeks rather than months.

Did the IEA Strategic Reserve Release Work?

On March 11, the 32-member International Energy Agency unanimously agreed to release 400 million barrels of oil from global strategic reserves — the largest coordinated release in the agency’s 50-year history. The United States committed 172 million barrels from the Strategic Petroleum Reserve, to be delivered over 120 days at a rate of approximately 1.4 million barrels per day. The release was more than double the 182 million barrels released across two tranches in 2022 during Russia’s invasion of Ukraine.

Oil prices initially fell on the announcement, dropping from $118 per barrel to $104 within two trading sessions. Within a week, Brent had climbed back above $110. As of late March, prices hover around $92 per barrel — lower than the $126 peak but still roughly 30 percent above pre-war levels. The release calmed markets psychologically but did not solve the fundamental supply deficit.

The arithmetic explains why. The Hormuz closure removed approximately 10 million barrels per day from the market. The IEA release adds 1.4 million barrels per day from the U.S. and perhaps another 1.5 million barrels per day from other member states. Combined, the strategic releases cover roughly 25 to 30 percent of the lost supply — enough to prevent a price spiral into the $150-plus territory that some analysts feared, but not nearly enough to restore market balance.

More critically, strategic reserves are finite. The U.S. Strategic Petroleum Reserve held approximately 390 million barrels before the latest drawdown — already significantly depleted from releases during the 2022 energy crisis. At the committed rate of 1.4 million barrels per day, the American reserve will be exhausted within nine months. Other IEA members face similar constraints. Japan’s strategic reserves can sustain approximately 150 days of net imports. Germany’s last roughly 90 days. The clock is ticking on every barrel in every salt cavern and steel tank across the industrial world.

The Al Jazeera analysis published on March 15 put it bluntly: “Strategic oil release may calm markets but cannot fix Hormuz disruption.” The reserves were designed to bridge short-term supply shocks — a hurricane shutting Gulf of Mexico production for two weeks, a pipeline rupture in Nigeria, a brief geopolitical flare-up. They were never designed to compensate for the sustained closure of a chokepoint through which one-fifth of the world’s seaborne oil moves. Using them for that purpose is like draining a bathtub to fill a swimming pool. The water runs out long before the pool is full.

The Oil Delivery Vulnerability Matrix

The crisis has exposed a gap in how the energy industry and governments assess supply security. Traditional metrics focus on production capacity, reserve-to-production ratios, and OPEC spare capacity. None adequately account for the ability to physically deliver oil from wellhead to consumer through functioning maritime and pipeline infrastructure. A more complete assessment requires a delivery vulnerability framework that evaluates five dimensions: production capacity, pipeline bypass options, port redundancy, maritime chokepoint exposure, and insurance availability.

| Exporter | Production (M bpd) | Bypass Capacity (M bpd) | Port Redundancy | Chokepoint Exposure | Insurance Available | Vulnerability Score |

|---|---|---|---|---|---|---|

| Saudi Arabia | 9.5 | 4.5 (Petroline) | Low (Yanbu only) | Critical (Hormuz) | Restricted | 8/10 (High) |

| UAE | 3.2 | 1.8 (ADCOP) | Low (Fujairah only) | Critical (Hormuz) | Restricted | 7/10 (High) |

| Iraq | 4.5 | 0.5 (Ceyhan pipeline) | Very Low | Critical (Hormuz + Basra) | Unavailable | 10/10 (Extreme) |

| Kuwait | 2.7 | 0 (no bypass) | None | Critical (Hormuz) | Unavailable | 10/10 (Extreme) |

| Russia | 10.5 | N/A (pipeline-linked) | High (multiple ports) | Low | Available | 2/10 (Low) |

| United States | 13.2 | N/A (domestic pipelines) | Very High | None | Full | 1/10 (Minimal) |

| Canada | 5.8 | N/A (pipeline to US) | High | None | Full | 1/10 (Minimal) |

| Norway | 1.9 | N/A (pipeline to Europe) | High | Very Low | Full | 1/10 (Minimal) |

| Brazil | 3.4 | N/A (Atlantic coast) | High | None | Full | 1/10 (Minimal) |

| Qatar | 1.8 (oil+condensate) | 0 (no bypass) | None | Critical (Hormuz) | Unavailable | 10/10 (Extreme) |

The matrix reveals a stark divide. Oil exporters whose production connects directly to open water via pipeline or coastal port — the United States, Canada, Norway, Brazil, Guyana — face minimal delivery vulnerability regardless of what happens in the Persian Gulf. Their oil reaches the market because it never passes through a chokepoint controlled by a hostile power. By contrast, every Gulf producer — regardless of how much oil sits beneath their sand — is hostage to a 21-mile-wide strait.

Saudi Arabia scores 8 out of 10 on the vulnerability scale rather than the maximum 10 because it possesses the Petroline bypass. That infrastructure, however, can deliver at most 4.5 million barrels per day to Yanbu — less than half the kingdom’s export requirements. Iraq and Kuwait, which lack any meaningful bypass, score at the maximum. Their oil is effectively stranded until Hormuz reopens.

The investment implications are immediate and lasting. Markets are already repricing Gulf crude at a discount not because of quality differentials but because of delivery risk. Brent crude surged past $119 before crashing as traders recalculated which barrels could actually reach refineries and which existed only on paper.

What Is the UAE Doing to Bypass Hormuz?

The United Arab Emirates operates the only other functioning Hormuz bypass in the Gulf: the Abu Dhabi Crude Oil Pipeline, known as ADCOP, which runs 500 kilometres from the Habshan gas field near Abu Dhabi to the port of Fujairah on the Gulf of Oman, outside the Strait. ADCOP has a nameplate capacity of 1.5 million barrels per day, with the ability to temporarily surge to 1.8 million barrels per day.

Before the war, ADCOP operated at approximately 71 percent utilisation, leaving around 440,000 barrels per day of spare pipeline capacity. ADNOC rapidly increased throughput in March, and the pipeline is now running near its maximum. A planned second pipeline from Jebel Dhanna to Fujairah, with an additional 1.5 million barrels per day of capacity, was scheduled to open in late 2026. The war has accelerated timelines, but the new line remains months away from commissioning.

Even with both Saudi and UAE bypass pipelines running at full capacity, the combined export volume through Yanbu and Fujairah reaches approximately 6 million barrels per day under optimistic assumptions. The Gulf was exporting roughly 18 to 20 million barrels per day through Hormuz before the war. The bypass gap — the volume that has no alternative route — stands at 12 to 14 million barrels per day. No amount of pipeline conversion or terminal expansion can close that gap while Hormuz remains effectively closed.

Fujairah itself has not escaped the war. Iranian drone strikes have targeted energy infrastructure across the Gulf, and the UAE’s decision to join the 22-nation coalition demanding Hormuz’s reopening has not gone unnoticed in Tehran. The port remains operational, but every day it functions as a high-value target represents a calculated bet that Iran will not escalate further against a nominal non-combatant.

The 1973 Myth — Why the Post-OPEC Energy Security Model Was Built on Sand

The conventional narrative of global energy security was written in the aftermath of the 1973 Arab oil embargo. That crisis demonstrated that oil supply could be weaponised, and the response — the creation of the International Energy Agency in 1974, the mandate for member states to hold 90 days of net import coverage in strategic reserves, and the informal understanding that Saudi Arabia would maintain swing capacity — became the pillars of the system that endured for half a century.

The model contained a fatal assumption. It presumed that the primary risk to oil supply was production disruption — wars, revolutions, sanctions that would physically prevent oil from being extracted. The 1973 embargo was a production cut. The 1979 Iranian Revolution halted Iranian production. The 1990 Kuwait invasion destroyed Kuwaiti production infrastructure. In every case, the solution was to produce more oil elsewhere and release strategic reserves. The system worked because the infrastructure to deliver replacement barrels — tankers, ports, shipping lanes — remained intact.

The 2026 Iran war has introduced a category of disruption for which the system was not designed: transit disruption at scale. Iran has not reduced its own production below pre-war levels. In a paradox noted by several analysts, Iran continues to sell oil through the very strait it has closed to others. Saudi Arabia, the UAE, Kuwait, Iraq, and Qatar all have the capacity to produce oil. What they cannot do is move it to the customers who need it.

The distinction matters enormously. Production disruptions can be offset by spare capacity elsewhere. Transit disruptions cannot, unless alternative transit routes exist with sufficient capacity. For fifty years, no one built enough alternative capacity because no one genuinely believed Hormuz would close. The pipeline bypasses that do exist — the Petroline and ADCOP — were sized for temporary disruptions lasting days or weeks. They were not sized for a sustained closure measured in months.

The Hormuz bypass infrastructure was sized for a short disruption. This is not that.

Engineering News-Record, March 2026

The contrarian reality is this: Saudi spare capacity — the world’s most famous energy insurance policy — was never insurance against the most probable catastrophic scenario. It insured against production loss. It did not insure against transit loss. And transit loss, through a narrow strait controlled by a regional power with the motivation and the means to close it, was always the more likely catastrophic event. The policy paid premiums for fifty years against a risk that was real but secondary, while leaving the primary risk entirely unhedged.

Can Russia and Non-OPEC Producers Fill the Gap?

The immediate beneficiary of the Hormuz closure is not a traditional ally of the Western energy order. Russia, producing approximately 10.5 million barrels per day and exporting through ports on the Baltic, Black Sea, and Pacific that face no chokepoint risk, has seen its oil become dramatically more valuable. On March 13, President Trump lifted Russian oil sanctions in an explicit acknowledgment that the world could not sustain the loss of both Gulf and Russian barrels simultaneously.

Russian crude — Urals blend — traded at a $30 discount to Brent before the war due to sanctions and logistical constraints. That discount has narrowed to less than $5. Russia is producing at near-maximum capacity, shipping every barrel it can to the same Asian refineries that previously relied on Gulf crude. The irony is caustic: a war launched in part by the United States has enriched Russia more than any OPEC production cut could have achieved.

Non-OPEC producers beyond Russia are also ramping output, but the volumes are modest relative to the scale of the disruption. U.S. shale producers can add approximately 500,000 to 800,000 barrels per day over six to nine months if prices remain above $80 per barrel. Brazil’s pre-salt fields are producing at 3.4 million barrels per day with limited room for rapid expansion. Guyana, the fastest-growing producer, adds roughly 100,000 barrels per day per quarter. Canada’s oil sands can expand modestly, but the Trans Mountain Pipeline expansion, which added 590,000 barrels per day of capacity to the Pacific Coast, is already running at capacity.

Combined, non-OPEC additions might reach 2 to 3 million barrels per day over the next six months — a meaningful contribution but far short of the 10 million barrels per day gap. The structural problem remains: the world’s largest concentration of spare capacity sits in countries whose export routes are blocked, and the countries with open export routes are already producing near their limits.

| Producer | Current Output (M bpd) | Ramp-Up Potential (M bpd) | Timeline | Constraints |

|---|---|---|---|---|

| United States (shale) | 13.2 | 0.5-0.8 | 6-9 months | Drilling rigs, labour, pipeline capacity |

| Russia | 10.5 | 0.2-0.3 | 3-6 months | Near maximum, aging fields |

| Brazil | 3.4 | 0.2-0.3 | 6-12 months | Pre-salt ramp timing, FPSOs |

| Canada | 5.8 | 0.1-0.2 | 6-12 months | Pipeline capacity, oil sands lead time |

| Guyana | 0.7 | 0.1 | Quarterly | FPSO phasing |

| Norway | 1.9 | 0.1 | 3-6 months | Mature fields, limited expansion |

What Comes After the Strait — The New Energy Geography

The 2026 Hormuz crisis is accelerating a restructuring of global energy trade that will outlast the war itself. The pre-war energy map was organised around three principles: Gulf production dominance, maritime chokepoint transit, and Asian consumption growth. All three remain true in the abstract. But the risk premium now attached to Hormuz-dependent oil is fundamentally reshaping investment, trade flows, and strategic planning.

Pipeline-connected oil has become a strategic asset of the first order. The war that MBS did not want is building infrastructure he had deprioritised. Saudi Arabia is already studying a second east-west pipeline that would double Yanbu throughput — a project that would cost an estimated $15 billion and take five to seven years to complete. The UAE’s second Fujairah pipeline is being fast-tracked. Iraq has revived discussions of a pipeline to Turkey’s Mediterranean coast at Ceyhan, which would bypass both Hormuz and Iran entirely.

For consuming nations, the crisis has triggered what the London School of Economics described as “a global inflation, shipping, and growth story.” European energy ministers held an emergency meeting as oil passed $106, announcing plans to accelerate renewable energy deployment and nuclear restarts. Japan and South Korea, the most Hormuz-dependent major economies, are reconsidering nuclear power phase-outs that now appear reckless. India is diversifying crude sources toward Russia, Brazil, and Africa at any price premium. The disruption has produced what analysts now call the world’s fourth great oil shock, with cascading effects on food prices, airline fares, and central bank policy worldwide.

The long-term implication is a de-Gulfification of energy trade for the most security-conscious consumers. Gulf oil will not disappear from the market — the reserves are too vast and the production cost too low. But the share of global oil trade that passes through Hormuz will decline structurally as pipelines, alternative routes, and non-Gulf sources absorb a larger share of demand. The premium that Gulf producers once commanded for reliability has inverted. Reliability now belongs to producers who can deliver without passing through a war zone.

How Is Saudi Arabia Adapting Its Oil Export Strategy?

Saudi Arabia’s response to the delivery crisis has been a mix of operational improvisation and strategic acceleration. In the immediate term, Aramco has focused on maximising Yanbu throughput. Tanker tracking data from Kpler showed 37 to 40 VLCCs expected to load at Yanbu in March, close to the terminal’s theoretical handling capacity of approximately 4.5 million barrels per day. Aramco has also opened Red Sea cargo corridors for non-oil commodities — petrochemicals, metals, and fertilisers — that previously transited Hormuz.

Prince Abdulaziz bin Salman, the energy minister, has coordinated closely with OPEC+ partners to manage the perception of supply adequacy even as physical barrels remain scarce. OPEC+ agreed at its March meeting to maintain the vast majority of production cuts with only minor adjustments, a decision that in any other context would have been criticised as restrictive but in the current crisis reflects the reality that production volumes are irrelevant if the oil cannot reach the market.

Strategically, Saudi Arabia is pursuing three parallel tracks. The first is diplomatic: working through the 22-nation coalition to pressure for Hormuz’s reopening, a process that remains uncertain given the escalation spiral between Trump’s ultimatum and Iran’s counter-threats. The second is military: Saudi air defenses are now engaged in the largest continuous air defense operation in the kingdom’s history, having abandoned any pretence of neutrality after three weeks of Iranian strikes. The third is infrastructural: accelerating the planning and pre-engineering for a second east-west pipeline, expanding Yanbu terminal capacity, and exploring an undersea pipeline to Egypt’s Red Sea coast that would provide a third export route entirely outside Saudi territory.

None of these solutions will resolve the immediate crisis. The diplomatic track depends on Iranian willingness to negotiate, which Tehran has explicitly rejected. The military track can defend existing infrastructure but cannot reopen Hormuz. The infrastructure track operates on a timeline of years, not weeks. For now, Saudi Arabia’s energy minister is managing a paradox that his predecessors never faced: the world’s swing producer, drowning in crude it cannot sell.

Frequently Asked Questions

How much oil can Saudi Arabia actually export right now?

Saudi Arabia can currently export approximately 2 to 4 million barrels per day through its Red Sea port of Yanbu, depending on terminal availability and security conditions. This represents roughly 25 to 40 percent of its total production capacity of 12 million barrels per day. The constraint is port loading capacity at Yanbu, not production or pipeline throughput. The Petroline can deliver 7 million barrels per day to Yanbu, but the port’s terminals can load only about 4.5 million barrels per day under optimal conditions.

Why was the East-West Pipeline not enough to replace Hormuz exports?

The East-West Pipeline was designed as a contingency bypass during the 1980s Iran-Iraq War, not as a full replacement for Gulf coast exports. Its 7 million barrels per day capacity exceeds the Yanbu port’s loading capacity of approximately 4.5 million barrels per day, creating a bottleneck at the terminal. Saudi Arabia was exporting roughly 7.5 million barrels per day through Persian Gulf terminals before the war, and Yanbu alone cannot absorb that volume — particularly under wartime conditions where Iranian strikes have intermittently shut down loading operations.

How long will global strategic petroleum reserves last at current draw rates?

At the committed release rate of approximately 3 million barrels per day from all IEA member states combined, total strategic reserves of roughly 1.2 billion barrels would be exhausted in approximately 12 to 14 months. However, individual country reserves vary significantly. The U.S. Strategic Petroleum Reserve, with approximately 390 million barrels before the March 2026 drawdown and a committed release of 1.4 million barrels per day, would be depleted in approximately nine months. Japan’s reserves cover roughly 150 days of net imports; Germany’s approximately 90 days.

Could a second east-west pipeline solve the problem?

A second east-west pipeline running from Saudi Arabia’s eastern oil fields to an expanded Red Sea terminal complex would approximately double Yanbu’s export capacity. However, such a project would require an estimated $15 billion in investment and five to seven years to design, construct, and commission. It would not address the current crisis but would significantly reduce Saudi Arabia’s vulnerability to future Hormuz disruptions. Aramco has reportedly begun preliminary engineering studies, suggesting the project has moved from theoretical discussion to active planning.

Which countries are most vulnerable to the Hormuz closure?

Japan, South Korea, and India face the greatest exposure. Japan imports approximately 90 percent of its crude oil through the Strait of Hormuz. South Korea imports roughly 70 percent. India faces a dual shock as both its crude oil and LNG imports are heavily Gulf-dependent. European nations are less directly exposed — most European crude comes from Norway, Russia, and West Africa — but face severe LNG supply disruption from the loss of Qatari gas exports through Hormuz, and are affected by the global oil price surge regardless of source.