WASHINGTON — Three weeks into the deadliest maritime crisis since the Second World War, the Trump administration’s signature policy response to the Strait of Hormuz shutdown — a $20 billion government-backed reinsurance program run through the US Development Finance Corporation and led by global insurer Chubb — has failed to restart commercial tanker traffic through the waterway. Not a single major oil tanker has transited the strait under the program since Chubb was announced as lead underwriter on March 11, according to shipping industry data and insurance market sources, leaving approximately 1,000 vessels and 20,000 seafarers stranded across the Persian Gulf.

The program, which President Donald Trump ordered the DFC to create “at a very reasonable price” to restore energy flows, covers hull and machinery damage and cargo losses but excludes the liability insurance that shipowners say they need most — protection against the catastrophic pollution and third-party damage claims that would follow if an Iranian missile or drone struck a fully loaded crude carrier. Without that coverage, maritime industry executives say, no responsible shipowner will order a Very Large Crude Carrier through waters where at least 20 vessels have been attacked since March 1.

Table of Contents

- What Is the DFC Reinsurance Program and How Does It Work?

- Why Is the $20 Billion Plan Failing to Restart Tanker Traffic?

- The Insurance Crisis in Numbers

- The Liability Gap That Sinks the Entire Plan

- What the Insurance Failure Means for Saudi Oil Exports

- One Thousand Ships and Twenty Thousand Sailors

- From Earnest Will to Earnest Won’t

- What Comes Next for Gulf Shipping Insurance?

- Frequently Asked Questions

What Is the DFC Reinsurance Program and How Does It Work?

The US International Development Finance Corporation announced on March 6 that it would deploy maritime reinsurance — including war risk coverage — across the Persian Gulf region to stabilize commercial shipping. The agency committed to covering losses “up to approximately $20 billion on a rolling basis,” with each vessel transit treated as a separate project rather than an aggregated portfolio.

On March 11, the DFC named Chubb, the world’s largest publicly traded property and casualty insurer, as lead underwriter for the program. Chubb CEO Evan Greenberg called the strait “vital to the global economy” and confirmed his firm would write reinsurance policies for vessels transiting the waterway under US military escort. The program coordinates directly with US Central Command, which has pledged Navy escorts for tankers by the end of March.

The structure works as follows: private insurers write primary policies for vessel owners, and the DFC provides reinsurance — effectively a government backstop — that absorbs losses if claims exceed the primary insurer’s capacity. No single entity can represent more than 5 percent of the DFC’s total exposure, capping individual coverage at roughly $10.25 billion per project.

The DFC, established in 2019 to replace the Overseas Private Investment Corporation, typically finances infrastructure, energy, and technology projects in developing nations. Clemence Landers of the Center for Global Development described the maritime insurance deployment as “a profound departure” from the agency’s core mission, calling it “the public sector subsidizing potentially a massive payout to private investors.”

Why Is the $20 Billion Plan Failing to Restart Tanker Traffic?

The program has failed because it addresses only one component of the maritime insurance chain while leaving the most expensive risk uncovered. Benjamin Serra, Senior Vice President at Moody’s Ratings, told InsuranceJournal on March 16 that the plan is “useful, but it’s probably not enough currently to solve the situation.” Serra warned that shipowners remain unwilling to assume the risk level present in the strait “at least today, as long as the situation is not safe.”

The core problem is structural. Maritime insurance operates across four interlocking categories: hull and machinery (covering physical damage to the vessel), cargo (covering the goods on board), war risk (covering losses from hostile acts), and Protection and Indemnity, known as P&I (covering third-party liability, pollution, and crew injury). The DFC program covers the first three categories through its reinsurance facility. It does not cover P&I.

For a loaded VLCC carrying two million barrels of crude oil through waters where Iranian anti-ship missiles, drones, and sea mines are actively deployed, the P&I exposure dwarfs every other risk combined. An oil spill from a struck tanker in the shallow, enclosed Persian Gulf could generate pollution cleanup costs, environmental damage claims, and third-party lawsuits running into the tens of billions of dollars. No shipowner will accept that exposure without coverage, regardless of what the DFC offers on the hull side.

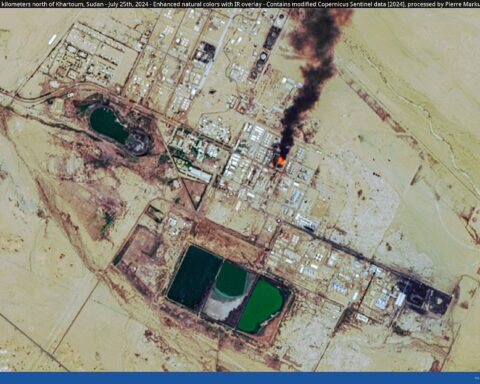

The five major P&I clubs that cancelled war risk coverage on March 5 — Gard, Skuld, NorthStandard, the London P&I Club, and the American Club — have not reinstated their policies. Without P&I coverage, a vessel is effectively uninsurable for commercial operations, and Saudi Aramco’s operational crisis deepens with each day the strait remains commercially dead.

The Insurance Crisis in Numbers

The scale of the maritime insurance collapse in the Persian Gulf is without modern precedent. War risk premiums have surged from roughly 0.2 percent of vessel value before the conflict to approximately 5 percent — a twenty-five-fold increase in three weeks, according to S&P Global Market Intelligence.

| Metric | Pre-War (Feb 2026) | Current (March 22) | Change |

|---|---|---|---|

| War risk premium (% of hull value) | 0.2% | 5.0% | +2,400% |

| Cost to insure $100M tanker (war risk) | $200,000 | $5,000,000 | +$4.8M |

| Cost to insure $200M LNG carrier | $625,000 | $7,500,000 | +$6.9M |

| P&I clubs offering Gulf war coverage | 13 | 0 | All cancelled |

| Vessels attacked since March 1 | 0 | 20+ | — |

| Vessels stranded in Gulf | ~50 | ~1,000 | +1,900% |

| Seafarers stranded | ~1,500 | ~20,000 | +1,233% |

JPMorgan has estimated that the total maritime insurance exposure in the Gulf — covering all vessels, cargoes, and liabilities — could reach $352 billion. The DFC’s $20 billion program covers less than 6 percent of that figure. Lloyd’s Market Association has estimated the value of trapped vessels alone at $25 billion, while some insurers have placed worst-case loss exposure at $40 billion or higher, according to Moody’s Ratings.

The DFC’s own balance sheet raises questions about the program’s credibility. The agency’s statutory risk exposure stood at $205 billion as of December 2025. A $20 billion maritime reinsurance commitment in an active war zone could consume a significant portion of that capacity, potentially crowding out the development finance projects the agency was created to support.

The Liability Gap That Sinks the Entire Plan

Serra at Moody’s identified the specific scenario that keeps tanker operators anchored: an Iranian missile striking a loaded crude carrier near the UAE coastline. “An oil tanker strike could cause massive pollution to Dubai’s beaches, creating enormous industry costs,” he said. The resulting claims — from coastal states, tourism operators, fisheries, desalination plant operators, and environmental agencies — would run into the billions before legal fees.

Under normal conditions, P&I clubs pool these risks across thousands of member vessels worldwide, spreading the liability so thin that individual shipowners face manageable premiums. The Iran war has shattered that model. With Iranian drones and missiles striking commercial vessels on a near-daily basis, and with the IRGC having explicitly declared Gulf shipping a legitimate target, the actuarial foundation for P&I coverage in the region has collapsed.

The liability gap extends beyond pollution. Standard P&I policies cover crew injury and death, wreck removal, cargo damage to third parties, and fines from port states. A vessel entering the Persian Gulf without P&I coverage exposes its owner to unlimited personal liability for all of these risks. No corporate board, no shipping company’s legal counsel, and no flag state registry will authorize that exposure.

London market insurers have confirmed to InsuranceJournal that coverage technically remains available — but at costs that make commercial voyages economically irrational. Insuring a vessel valued at $200 to $300 million could cost approximately 3 percent of hull value, or about $7.5 million, for war risk alone. Add cargo insurance, P&I surcharges (where available), and the cost of private or military escort arrangements, and a single voyage through Hormuz can cost a shipowner $15 to $20 million in insurance and security premiums before fuel and crew costs.

What the Insurance Failure Means for Saudi Oil Exports

Saudi Arabia has diverted the bulk of its crude exports to the Red Sea port of Yanbu, using the East-West Pipeline system that can carry up to 7 million barrels per day — roughly 5 million of which are available for export. Loadings at Yanbu averaged 2.2 million barrels per day in the first nine days of March, up from 1.1 million in February, with shipping data pointing to a potential record month of 37 to 40 tanker loadings.

The insurance crisis affects even the Yanbu bypass. Tankers loading at Yanbu must transit the Red Sea and pass through the Bab el-Mandeb strait, where Houthi forces — Iran’s Yemeni allies — have the capability to strike commercial shipping. While the Houthis have not launched attacks on Red Sea vessels since the Iran war began, their declared readiness to enter the conflict on Tehran’s behalf has pushed war risk premiums for Red Sea voyages above pre-war levels. Approximately 30 tankers near Yanbu currently sit within Houthi strike range, according to maritime tracking data.

The insurance failure has compounded Aramco’s operational crisis. Saudi Arabia cut production by as much as 2.5 million barrels per day after reaching storage capacity, joining the UAE, Iraq, and Kuwait in forced output reductions. The kingdom’s daily oil revenue, which at $100 Brent and 9 million barrels per day generated approximately $900 million, has fallen sharply as both production and export volumes decline.

The International Energy Agency confirmed that the Hormuz disruption represents the largest supply shock in the history of the global oil market, exceeding the 1973 Arab oil embargo and the Iranian Revolution. Approximately 20 percent of global oil supplies — some 16 to 20 million barrels per day that normally transit the strait — have been disrupted.

One Thousand Ships and Twenty Thousand Sailors

Beyond the insurance arithmetic, the DFC program’s failure has created a humanitarian crisis at sea. An estimated 20,000 seafarers remain stranded on approximately 1,000 vessels in the Persian Gulf, according to the International Transport Workers’ Federation. These crews — predominantly from the Philippines, India, Bangladesh, and Myanmar — are trapped on ships that cannot move because their insurance has been cancelled, their charterers have suspended operations, and the waterway they need to exit is mined, patrolled by Iranian fast attack boats, and targeted by coastal anti-ship missiles.

The trapped fleet includes crude oil tankers, LNG carriers, container ships, dry bulk carriers, and chemical tankers spread across anchorages from Kuwait’s Mina al-Ahmadi to the UAE’s Fujairah. Several vessels have been at anchor since the first week of March, their crews cycling through dwindling provisions while watching Iranian drones pass overhead en route to Gulf state targets. Port state authorities in Kuwait, Bahrain, and the UAE have provided emergency food and water deliveries to anchored vessels, but long-term crew welfare remains precarious.

The UK Maritime Trade Operations Center has confirmed at least 20 security incidents involving commercial vessels since March 1, including a container ship struck on March 12 that caught fire. The threat level across the Gulf, Strait of Hormuz, and Gulf of Oman remains classified as “critical” — the highest designation.

Standard marine insurance policies include a “total loss” clause triggered when a vessel is trapped for 12 months — potentially generating billions in payouts to shipowners even if their vessels are never physically damaged. Moody’s has warned that marine insurers could face aggregate losses of $40 billion or more if the disruption intensifies, a figure that would strain the global reinsurance market and push premium rates higher worldwide.

The stranded seafarer crisis has drawn criticism from the International Maritime Organization, maritime unions, and flag state registries. Several nations — including the Philippines, India, and Bangladesh — have demanded that shipowners either evacuate their crews or provide combat zone hazard pay. Neither option is straightforward when the vessels themselves cannot move and air evacuations face the same airspace restrictions that have disrupted civilian flights across the region.

From Earnest Will to Earnest Won’t

The DFC program inevitably draws comparison to Operation Earnest Will, the 1987-1988 US Navy convoy escort operation that protected reflagged Kuwaiti tankers during the Iran-Iraq War. That operation succeeded in keeping oil flowing through Hormuz despite Iranian mine-laying and fast boat attacks — but it operated under fundamentally different insurance conditions.

During the Tanker War of the 1980s, P&I clubs maintained coverage for Gulf voyages, albeit at elevated premiums. Lloyd’s of London continued to write war risk policies. The US government provided both military escorts and a legal framework that limited shipowner liability for vessels operating under naval protection. The insurance chain remained intact, even if it was expensive.

In 2026, the insurance chain has broken entirely. The scale of Iranian attacks — hundreds of drones and missiles fired at Gulf states and commercial vessels over three weeks — exceeds anything the maritime insurance industry has confronted. The Tanker War of the 1980s involved sporadic attacks on individual vessels. The current conflict involves systematic, daily bombardment of entire coastlines, ports, and shipping lanes using precision-guided weapons that did not exist in the 1980s.

The DFC program attempts to fill part of the gap but leaves the largest piece missing. Military escorts without insurance do not restart shipping. Insurance without military escorts does not restart shipping. Both without P&I coverage still do not restart shipping. The equation requires all three components, and the Trump administration has so far delivered only two — escorts that are still being organized and partial insurance that covers the wrong risks.

What Comes Next for Gulf Shipping Insurance?

Maritime industry executives and insurance analysts have identified three scenarios for breaking the insurance deadlock. The first involves the DFC expanding its program to include P&I reinsurance — a step that would require either congressional authorization or a creative interpretation of the agency’s existing mandate. The DFC has not indicated any plans to extend coverage.

The second scenario involves the creation of a sovereign-backed insurance pool by Gulf states themselves. Saudi Arabia, the UAE, Kuwait, and Qatar collectively manage sovereign wealth exceeding $3 trillion. A Gulf-backed war risk pool could theoretically provide the comprehensive coverage — hull, cargo, and liability — that the private market will not. This approach would keep shipping costs within the region’s control but would expose Gulf sovereign funds to potentially enormous claims.

The third and most likely scenario, according to Moody’s, is that commercial shipping through Hormuz remains frozen until the military situation changes. “It’s probably not a great incentive to try to cross the strait, at least today, as long as the situation is not safe,” Serra said. No amount of insurance, at any price, will persuade shipowners to send vessels into a waterway where Iranian anti-ship missiles have already struck multiple targets — and where the military conflict shows no signs of ending.

For Saudi Arabia, the insurance failure accelerates a strategic shift already underway. The kingdom’s pivot to Red Sea export capacity through Yanbu — once considered a backup route — is becoming the primary artery for Saudi oil. If the Iran war persists for weeks or months beyond its current trajectory, that shift may become permanent, redrawing the energy map of the Middle East around a chokepoint that is 2,400 kilometers from Tehran’s missiles but within range of Yemen’s.

The insurance failure also raises a broader question about the limits of American economic statecraft during a shooting war. Washington can deploy carrier strike groups, drop 5,000-pound bunker-buster bombs on Iranian coastal facilities, and announce billion-dollar reinsurance programs from the White House podium. What it cannot do is force a private insurance company in London, Oslo, or Bermuda to write a policy covering a $300 million LNG carrier sailing through an active minefield. The market has spoken, and the market says the Strait of Hormuz is closed for business — regardless of what the DFC’s press releases claim.

Frequently Asked Questions

What is the DFC’s $20 billion Gulf shipping reinsurance program?

The US International Development Finance Corporation announced a $20 billion maritime reinsurance facility on March 6, 2026, with Chubb as lead underwriter. The program provides government-backed reinsurance for hull and machinery damage and cargo losses on vessels transiting the Strait of Hormuz. It coordinates with US Central Command and aims to restore commercial oil and gas shipping through the waterway, which Iran has effectively closed since early March.

Why has the program failed to restart tanker traffic?

The program excludes Protection and Indemnity insurance, which covers third-party liability, pollution cleanup, crew injury, and wreck removal. Without P&I coverage, shipowners face unlimited personal liability if a vessel is struck while carrying crude oil through the Gulf. All five major P&I clubs cancelled Gulf war coverage on March 5, and none have reinstated policies. No responsible shipowner will transit Hormuz without comprehensive insurance covering all risk categories.

How much does it cost to insure a tanker through the Strait of Hormuz?

War risk premiums have surged to approximately 5 percent of hull value — roughly twenty-five times pre-war levels. Insuring a $100 million oil tanker costs about $5 million for war risk alone. A $200 to $300 million LNG carrier faces premiums of approximately $7.5 million. Adding cargo insurance, P&I surcharges, and escort costs pushes the total insurance burden for a single Hormuz transit to $15 to $20 million.

How many ships are stranded in the Persian Gulf?

Approximately 1,000 vessels carrying an estimated 20,000 seafarers are stranded in the Persian Gulf, according to the International Transport Workers’ Federation and Lloyd’s Market Association data. The Lloyd’s Market Association estimates the trapped fleet is worth roughly $25 billion. At least 20 vessels have experienced security incidents since March 1, including missile strikes, drone hits, and mine damage.

What does the insurance failure mean for global oil prices?

The insurance collapse has contributed to the largest oil supply disruption in recorded history, with approximately 16 to 20 million barrels per day of Hormuz transit volume disrupted. Oil prices have risen approximately 45 percent since the war began, with Brent crude trading above $110 per barrel. The IEA has released a record 400 million barrels from strategic reserves but has warned that stockpile drawdowns cannot sustain current consumption levels for more than 60 to 90 days without resumed Gulf exports.