Table of Contents

WASHINGTON — President Donald Trump told the Financial Times on March 29 that his “preference would be to take the oil in Iran,” explicitly raising the prospect of a US military seizure of Kharg Island, the offshore terminal that handles 90 percent of Iran’s crude exports. The remarks, published as Day 30 of the US-led war against Iran drew to a close, sent Brent crude futures up 3.2 percent to $116.12 per barrel on March 30 and injected a new uncertainty into global oil markets already reeling from what the International Energy Agency has called the “biggest oil shock in history.”

For Saudi Arabia, the statement created a paradox with no comfortable resolution. The Kingdom is banking record wartime oil revenues — but a US-controlled Iranian oil spigot, even a theoretical one, threatens the foundations of Saudi pricing power and market share that Riyadh has spent decades building.

What Trump Told the Financial Times

Trump’s remarks in the Financial Times interview were unscripted and expansive. “To be honest with you, my favorite thing is to take the oil in Iran but some stupid people back in the US say: ‘Why are you doing that?’ But they’re stupid people,” the president said, according to NBC News and Bloomberg, which independently confirmed the quotes.

“Maybe we take Kharg Island, maybe we don’t. We have a lot of options,” Trump continued. He acknowledged that a seizure would require an extended American military presence: “It would also mean we had to be there for a while.”

Trump drew a parallel to US ambitions regarding Venezuela’s oil after the capture of Nicolás Maduro, signaling that resource extraction remains a central pillar of his foreign policy calculus. The remarks arrived as thousands of additional US troops massed in the Persian Gulf region, including an amphibious assault team that arrived over the weekend, according to CNN.

The Pentagon has already prepared plans to deploy 10,000 more troops to the Gulf theater, and US forces bombed Kharg Island once before during this conflict, on March 13.

Brent Surges Past $116 on Seizure Fears

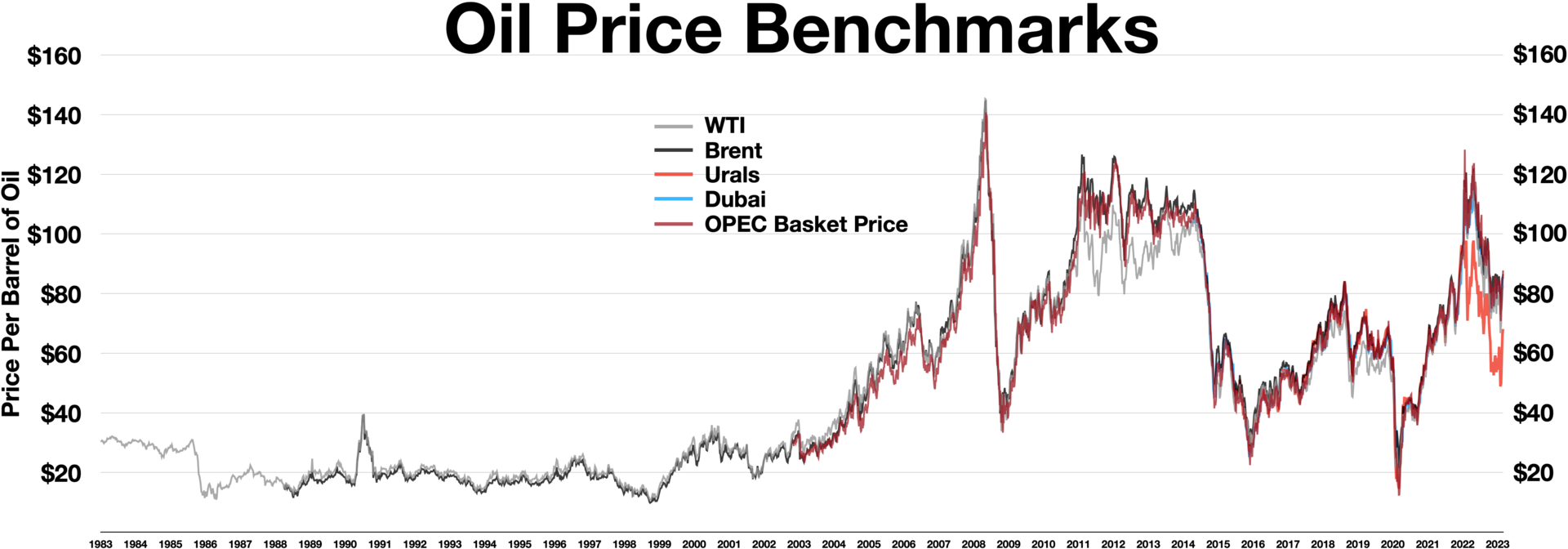

Oil markets responded immediately. Brent May futures rose more than $4 to hit a session high of $116.71 per barrel before settling at $116.12, according to MarketScreener data. WTI crude climbed 3.4 percent to $102.96. The surge marked Brent’s highest point since March 19, when the benchmark briefly touched $119.

The numbers tell a story of sustained disruption. Brent has risen more than 50 percent since the war began on February 28, when the benchmark sat near $72 per barrel. The average OPEC reference basket price for March reached $115.88, compared to $67.90 in February — a 71 percent month-on-month increase that has no precedent in the post-2008 era.

| Benchmark | Pre-War (Feb 27) | March Peak | March 30 | Change Since War Began |

|---|---|---|---|---|

| Brent Crude | ~$72/bbl | $126/bbl | $116.12/bbl | +61% |

| WTI Crude | ~$67/bbl | ~$118/bbl | $102.96/bbl | +54% |

| OPEC Basket (March avg) | $67.90 (Feb avg) | — | $115.88 (March avg) | +71% |

Goldman Sachs has forecast Brent averaging $115 per barrel in April before retreating to $80 by year-end, a projection that assumes roughly six weeks of Strait of Hormuz supply disruptions. The bank warned that a US seizure of Kharg could push Brent past $150 within days, according to Goldman Sachs research published in mid-March.

JP Morgan issued a separate warning that Iran’s oil production could be “slashed in half” and exports could “virtually stall” if US forces seize the island, compounding an oil shock that has already seen maritime traffic through the Strait of Hormuz fall by 90 percent.

Why Is the Saudi Windfall Also a Threat?

The arithmetic of Saudi Arabia’s wartime revenues is staggering. At roughly 9 million barrels per day of production and Brent above $100, the Kingdom is generating approximately $900 million per day in oil revenue. Saudi Arabia’s fiscal breakeven price is approximately $81 per barrel. The surplus — annualized at $49 billion to $72 billion — dwarfs the fiscal gaps that forced Riyadh to scale back Vision 2030 megaprojects over the past two years.

Saudi Finance Minister Mohammed Al-Jadaan, speaking at the Future Investment Initiative conference in Miami, declared that the “Saudi economy is resilient and able to manage crises.” GDP growth for 2026 is forecast at 4.6 percent, with the non-oil economy expanding at 4.9 percent.

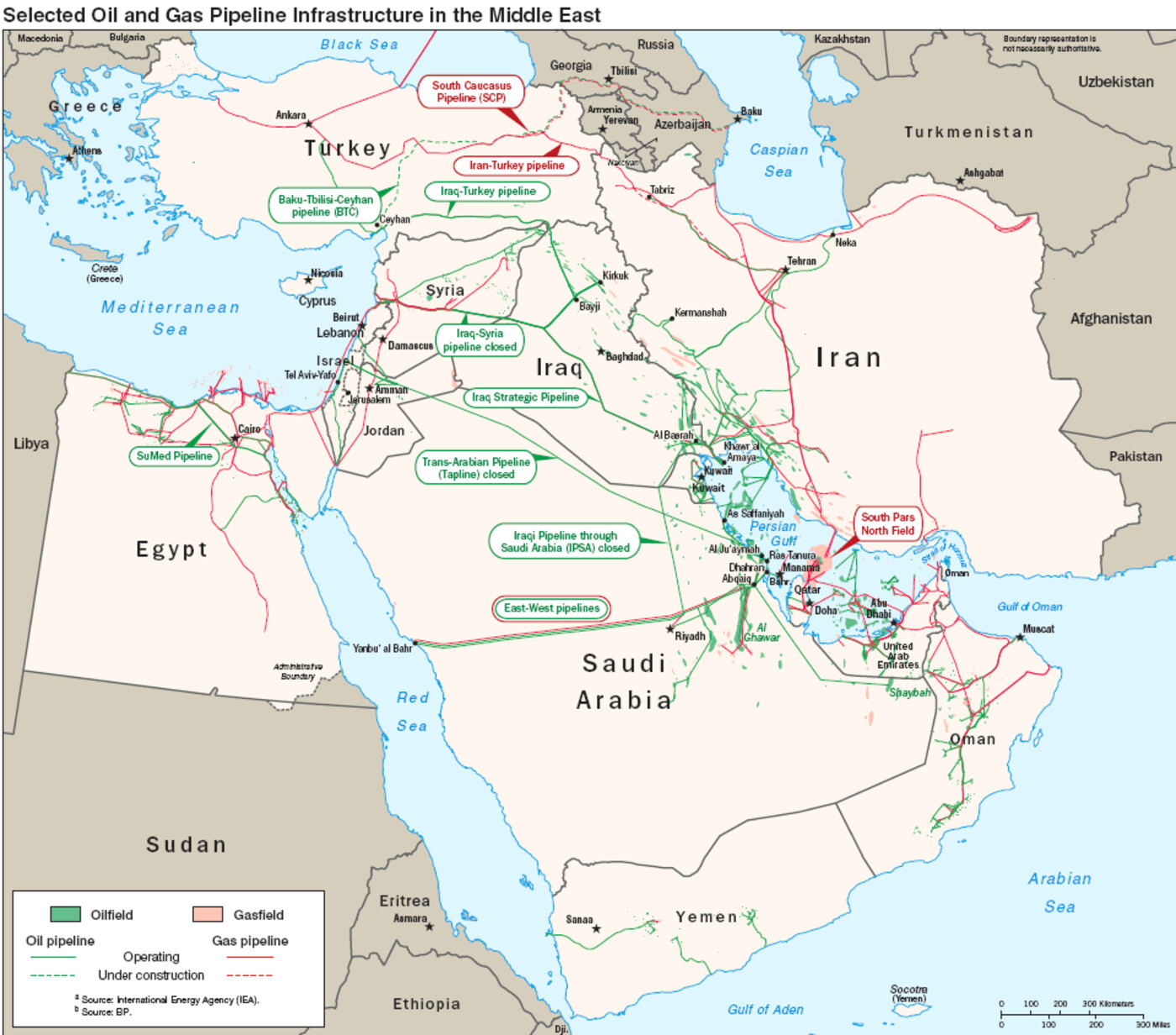

But the windfall conceals a structural vulnerability. If the United States seizes and holds Kharg Island, Washington would control a terminal with a design capacity of 7 million barrels per day — though actual pre-war Iranian exports ran between 1.5 and 2 million barrels daily, according to Argus Media. In the weeks immediately before the war, Iran accelerated shipments to between 3 and 4 million barrels per day.

An American-controlled Kharg could, over time, restore some or all of that Iranian output under US direction — flooding a market that Saudi Arabia has spent years carefully managing through OPEC+ production cuts. The Kingdom currently bears approximately 45 percent of total OPEC+ voluntary cuts and holds the world’s largest spare capacity at 3 to 3.5 million barrels per day. That spare capacity is the source of Saudi pricing power. A rival spigot under American control would erode it.

Can the US Actually Hold Kharg Island?

Kharg is a small coral island roughly 25 kilometers off Iran’s southern coast in the northern Persian Gulf. It hosts storage capacity of 32 to 34 million barrels of crude oil plus 5 to 7 million barrels of oil products, along with a petrochemical plant, according to Columbia University’s Center on Global Energy Policy.

Mark Cancian, a senior adviser at the Center for Strategic and International Studies, told media that “the US forces currently deployed in the Middle East are sufficient for punitive airstrikes, but somewhat inadequate for conducting a large-scale ground war.” A seizure and sustained occupation of Kharg would require substantially more forces than are currently in theater.

The Pentagon’s ground war planning has already drawn Saudi Arabia deeper into the conflict. US forces operate from King Fahd Air Base in Saudi Arabia, and the Saudi Ministry of Defense has intercepted 35 drone attacks overnight in the Eastern Region alone. A US amphibious operation launched from Saudi-hosted bases would, by implication, make the Kingdom a direct co-belligerent in any ground campaign.

Robin Mills, a non-resident fellow at Columbia University’s Center on Global Energy Policy, cautioned that a Kharg takeover may not achieve its stated objective. “That seems to me to be more threatening than having their oil cut off, and yet they keep going,” Mills said of Iran’s willingness to absorb strikes.

Trump’s own acknowledgment — “we had to be there for a while” — signals a long-term occupation rather than a raid, raising comparisons to Iraq’s oil infrastructure challenges that persisted for years after the 2003 invasion.

The Market Share Nightmare for Riyadh

Saudi Arabia’s post-war oil market position depends on a specific sequence: Iran’s oil infrastructure remains degraded, global demand stays elevated, and the Kingdom controls the marginal barrel. Trump’s Kharg remarks threaten all three assumptions simultaneously.

If Washington seizes Kharg and restores Iranian exports under American supervision, it would create a competing source of heavy-sour crude that directly overlaps with Saudi Arabia’s primary export grades. China, Iran’s largest pre-war customer, would face a choice between sanctioned Iranian barrels and American-supervised ones — and Beijing has historically prioritized price over politics.

The scale of the threat is measurable. Iran’s pre-war capacity stood at 3.2 million barrels per day, with potential capacity reaching 4 to 5 million barrels per day under sustained investment. Even restoring half of that under US control would equal Saudi Arabia’s entire spare capacity buffer.

| Metric | Saudi Arabia | Iran (Pre-War) | Iran (Potential Under US Control) |

|---|---|---|---|

| Production Capacity | ~12.5M bpd | ~3.2M bpd | 4–5M bpd |

| Spare Capacity | 3–3.5M bpd | Minimal | N/A |

| Hormuz Bypass | East-West Pipeline (7M bpd design) | None | Kharg is in the Gulf, not Hormuz-dependent |

| Primary Customers | China, India, Japan, S. Korea | China (dominant) | Global market access |

The one-month balance sheet of the war shows Saudi Arabia profiting enormously from the conflict’s immediate effects. But the Kingdom’s strategists recognize that wartime windfalls are temporary while market structure shifts are permanent. The Public Investment Fund has already cut construction contracts from $71 billion to $30 billion — a 60 percent reduction — and PIF governor Yasir Al Rumayyan is finalizing a revised 2026-2030 strategy that includes a further 15 percent capital spending reduction, according to PIF’s revised five-year strategy announced at FII Miami.

That fiscal caution suggests Riyadh is not treating the current revenue surge as permanent — and Trump’s Kharg remarks explain why.

Tehran’s Counter-Demands and the Hormuz Card

Iran’s response to escalating US threats has been to raise its own price for peace. Tehran’s five counter-demands, as articulated through diplomatic channels, include a halt to all aggression, mechanisms to prevent resumption of hostilities, war reparations, an end to attacks on Hezbollah and Iraqi militias, and “international recognition and guarantees” for Iran’s authority over the Strait of Hormuz.

The final demand is the most consequential for oil markets. Iran is effectively asking for permanent veto power over the world’s most critical energy chokepoint — a concession that no Gulf state, and certainly not Saudi Arabia, could accept. The Kingdom activated its East-West Pipeline at 7 million barrels per day design capacity to bypass Hormuz, though actual throughput has been constrained by port capacity at Yanbu on the Red Sea.

The IRGC has demonstrated its willingness to target Gulf economic infrastructure beyond oil. Retaliatory strikes hit aluminium plants at Emirates Global Aluminium in the UAE and Aluminium Bahrain, exposing the Gulf’s industrial vulnerability to Iranian economic warfare. Iran’s parliament speaker accused the United States of planning a ground invasion, a claim that Trump’s Financial Times interview did little to dispel.

For Saudi Arabia, Iran’s Hormuz demand and Trump’s Kharg ambitions represent two sides of the same threat: external actors claiming control over the physical infrastructure that determines who sells oil, at what price, and to whom. Both threats trace back to the structural failure of the 1945 oil-for-security bargain that was supposed to prevent exactly this scenario.

Background

The US-led war against Iran began on February 28, 2026. Over 30 days, the conflict has produced 3,461 Iranian deaths including 1,551 civilians according to the Human Rights Activists News Agency, while Iran’s government acknowledges 3,117 deaths. Thirteen US service members have been killed and more than 300 wounded.

Saudi Arabia has absorbed over 600 strikes without directly entering the war as a combatant, though it expelled the Iranian military attaché and four embassy staff on March 21 and had its foreign minister state that the Kingdom “reserves the right to take military action against Iran.”

The Strait of Hormuz closure, which began on March 4, sent Brent crude to a peak of $126 per barrel on March 8 before Saudi pipeline capacity partially compensated for the lost maritime route. Formula One cancelled the Saudi Arabian and Bahrain Grand Prix events due to the war.

OPEC+ has maintained existing production cuts with gradual output increases planned for Q2 2026, though the war has rendered those plans largely academic as physical disruptions override quota management.

Frequently Asked Questions

How much oil does Kharg Island actually handle?

Kharg Island’s loading infrastructure can accommodate 10 supertankers simultaneously and has a design capacity of approximately 7 million barrels per day, according to Argus Media. In practice, pre-war exports from Kharg ranged between 1.5 and 2 million barrels per day under normal conditions. In the two weeks before the war began, Iran surged shipments to between 3 and 4 million barrels daily. The island also holds 32 to 34 million barrels of crude storage capacity and 5 to 7 million barrels of product storage, per Columbia University’s Center on Global Energy Policy.

Has the US ever seized a foreign country’s oil infrastructure before?

The closest historical parallel is the US occupation of Iraq’s oil fields after the 2003 invasion. US forces secured the Rumaila oil field and other southern Iraqi infrastructure within days of crossing the border, but restoring full production took years. Pre-invasion Iraqi output of approximately 2.5 million barrels per day did not recover to that level until 2008. The Iraq precedent suggests that seizing Kharg is militarily feasible but that restoring and maintaining production under occupation conditions is far more difficult than Trump’s remarks imply.

What would a Kharg seizure mean for OPEC+ quotas?

Iran’s production has been effectively exempt from OPEC+ quota discipline since US sanctions decimated its output after 2018. If the United States seized Kharg and restored Iranian exports outside OPEC+ coordination, it would create a non-quota supply source of potentially 2 to 4 million barrels per day. That volume, unregulated by the cartel, would undermine OPEC+’s ability to manage prices through coordinated cuts — a mechanism that Saudi Arabia has used since 2016 to support prices above its fiscal breakeven point. Goldman Sachs estimated that unconstrained Iranian barrels could push long-term Brent equilibrium down by $10 to $15 per barrel.

How are Asian buyers reacting to the Kharg threat?

China imported approximately 1.5 million barrels per day of Iranian crude before the war, making it Iran’s dominant customer. According to Kpler data, Chinese refiners have already begun redirecting purchases toward Saudi, UAE, and West African crudes as Iranian supplies dried up during the conflict. A US-controlled Kharg would force Beijing to negotiate with Washington for access to Iranian barrels — a geopolitical concession that Chinese state refiners would resist. India and South Korea, also significant Iranian customers, have diversified toward Saudi and Iraqi supply lines during the war.

What is Saudi Arabia’s East-West Pipeline and can it fully bypass Hormuz?

The East-West Pipeline, also known as the Petroline, connects Saudi Arabia’s Eastern Province oil fields to the Red Sea port of Yanbu. Built during the 1980s Iran-Iraq “Tanker War” as a Hormuz contingency, it has a design capacity of 7 million barrels per day. Saudi Arabia activated the pipeline at full capacity after Hormuz closed on March 4, but port infrastructure at Yanbu has created a bottleneck, capping actual throughput below the pipeline’s nameplate capacity. By late March, Saudi pipeline flows averaged 2.9 million barrels per day, up from 770,000 barrels per day in January and February, according to Al Jazeera.