DHAHRAN — Saudi Arabia has built an informal rationing system for crude oil exports to Asia, allocating barrels bilaterally to allied governments while maintaining its headline May OSP at a record +$19.50/bbl premium that no buyer in the commercial queue can economically justify. South Korea’s confirmation on April 12 that it has secured 80% of its May crude needs — through direct government-to-government commitments from seven GCC states — is the first publicly documented case of the architecture in operation.

The system is not a discount. It is a wartime volume allocation mechanism operating beneath a uniform posted price, and it inverts the logic of the last comparable precedent: the 1973 Arab oil embargo, which used selective supply to punish adversaries. The 2026 version rewards allies. It holds together only as long as Asian buyers accept Saudi terms rather than calculating that Iran’s $2M-per-VLCC Hormuz toll offers cheaper access to alternative crude.

Table of Contents

- The Three-Tier Allocation System

- What Did South Korea Actually Secure?

- Japan’s Pre-Positioned Legal Claim

- Why Can’t Saudi Arabia Simply Export More?

- The OSP Trap: $19.50 Above a Market That No Longer Exists

- China’s Structural Arbitrage

- The Benchmark Revolt

- Is Iran’s $2M Hormuz Toll Cheaper Than Saudi Allocation?

- The June OSP Decision and the Fracture Point

- Frequently Asked Questions

The Three-Tier Allocation System

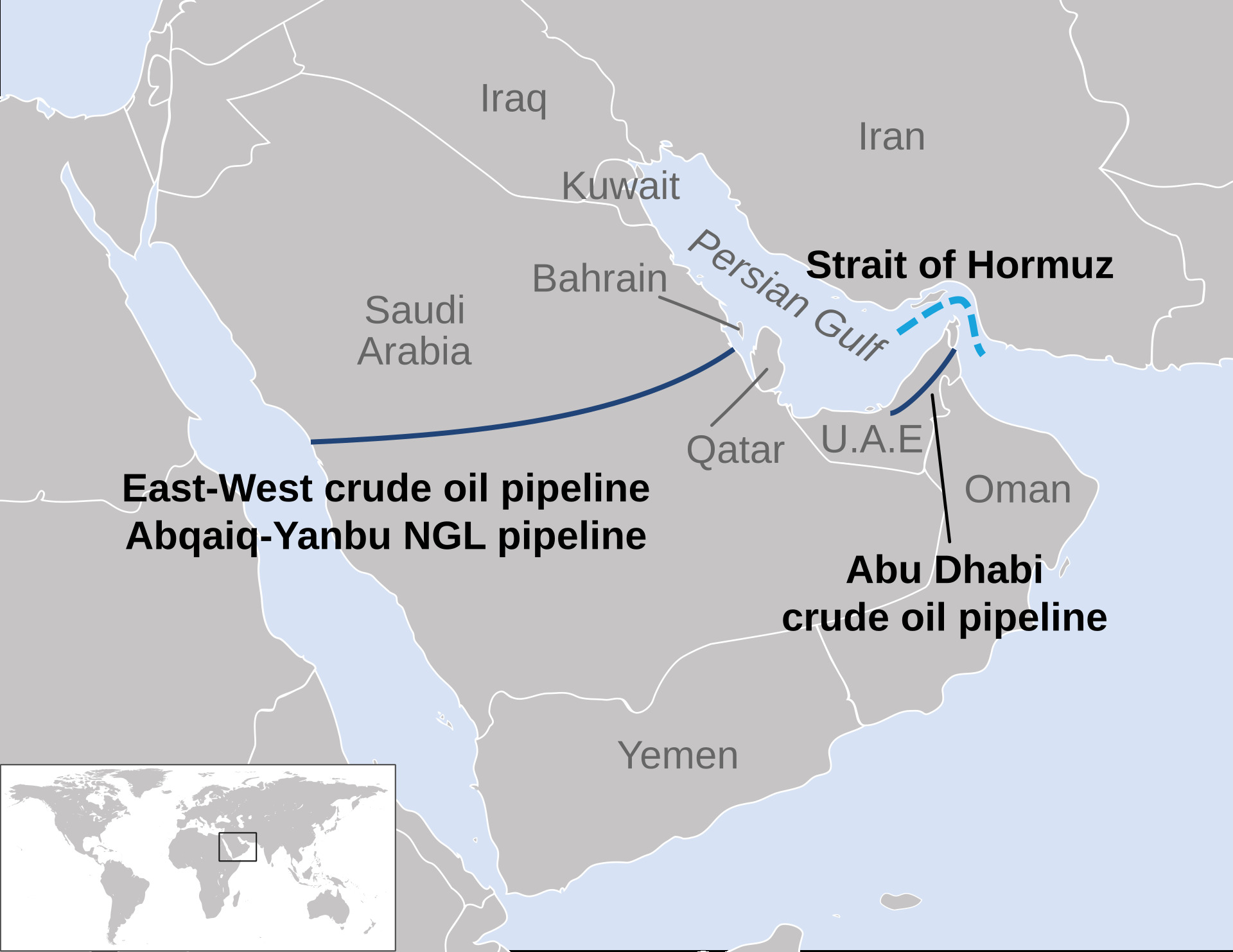

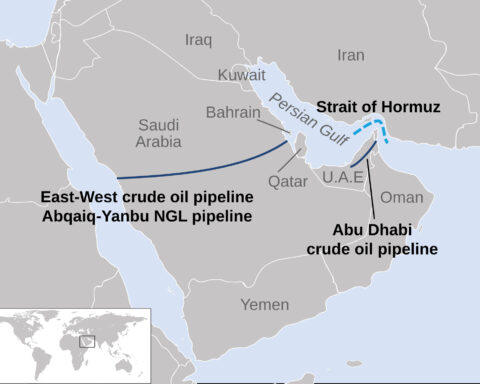

Saudi crude exports to Asia fell 38.6% in a single month — from 7.108 million bpd in February 2026 to 4.355 million bpd in March, according to Bloomberg tracking data. The collapse is structural, not cyclical. With the Strait of Hormuz under IRGC operational control and Yanbu as Saudi Arabia’s only functioning deepwater export terminal, every barrel loaded is a barrel denied to someone else.

What has emerged in the six weeks since Aramco restricted April liftings to Arab Light grade via Yanbu is a three-tier allocation hierarchy that operates entirely beneath the uniform OSP price sheet.

Tier 1 is contractual. Japan holds a pre-positioned legal claim on 8.2 million barrels of Aramco crude stored in Okinawa, secured through a 2010 storage-for-priority agreement that converts Tokyo’s access from diplomatic goodwill to enforceable obligation. Tier 2 is diplomatic. South Korea, and to a lesser extent India, have secured verbal government-to-government commitments for priority volumes — commitments that required a 869.1 billion won supplementary budget from Seoul and direct ambassadorial pledges from seven GCC states. Tier 3 is the commercial queue: everyone else, paying record VLCC charter premiums, accepting whatever volumes remain, absorbing an OSP-above-spot inversion with no bilateral relief.

The distinction between tiers is not price. All three pay the same +$19.50/bbl May OSP differential. The distinction is access — whether a buyer receives barrels at all, and how many.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

What Did South Korea Actually Secure?

Trade Minister Kim Jung-kwan disclosed on April 12 that South Korea had “received commitments to prioritize allocations to Korea” for May crude needs, securing approximately 80% of requirements without triggering a strategic petroleum reserve drawdown. “If our ships can operate with assured safety, we will be able to secure the volumes,” Kim told Seoul Economic Daily.

The 80% figure sits within a broader bilateral architecture. Between April and May, South Korea secured commitments for 110 million barrels from 17 countries — 50 million for April, 60 million for May. The GCC diplomatic infrastructure behind those numbers was formalized on April 7, when ambassadors from Saudi Arabia, the UAE, Kuwait, Qatar, Oman, Bahrain, and Jordan met South Korean National Assembly legislators and “reaffirmed the commitment of their governments to prioritize the supply of crude oil from the Middle East to Korea.”

Rep. Kim Seok-ki of the National Assembly Foreign Affairs Committee framed the arrangement plainly: “The situation in the Middle East is directly related to Korea’s economy, supply chains and energy security.”

The UAE component is separately documented. Abu Dhabi pledged 24 million barrels designated as “number one priority,” including 18 million barrels for urgent import. Two supertankers of Murban crude arrived March 29 and April 1.

None of this involved a price concession. South Korea pays the same OSP differential as every other term contract buyer. What Seoul purchased — with $640 million in supplementary budget, direct ministerial engagement, and a seven-nation ambassadorial pledge — was priority in the loading queue at Yanbu.

Japan’s Pre-Positioned Legal Claim

Japan’s position is structurally different from South Korea’s, and the difference illuminates the allocation hierarchy. Since 2010, ENEOS and Cosmo Oil have leased 13 storage tanks to Aramco in Okinawa, fee-free. In exchange, Aramco commits to supply Japan with priority access in an emergency. The stored volume — 8.2 million barrels — functions as a contractual entitlement rather than a diplomatic favor.

Aramco accounts for approximately 40% of Japan’s total crude imports. The Okinawa arrangement, renewed most recently in 2025, means Japan’s claim on Saudi barrels is not subject to the same diplomatic friction that South Korea navigated through seven-nation ambassadorial meetings and a supplementary budget. Tokyo’s access is pre-positioned in legal documentation.

But Japan is also hedging. Japanese refiners purchased at least 13 million barrels of US WTI and Mars crude for April delivery — potentially a record monthly level. The WTI Midland CFR Asia premium over second-month Dubai tells the story of escalating desperation across the market: $6.2/bbl in January, $7.2/bbl in February, $16.7/bbl in March. A 2.7-fold surge in eight weeks.

The US crude is not replacing Saudi barrels. It is supplementing them — filling the gap between contractual entitlement and actual refinery demand. Even Tier 1 access does not make a refiner whole.

Why Can’t Saudi Arabia Simply Export More?

The answer is physical infrastructure. The East-West Pipeline connecting Eastern Province fields to Yanbu has a nameplate capacity of 7 million bpd, but approximately 2 million bpd is consumed domestically by Red Sea coast refineries and petrochemical plants. That leaves roughly 5 million bpd of export headroom. Actual loadings in late March averaged 4.4 million bpd over a five-day window, according to Bloomberg tracking.

Before the war, Saudi Arabia shipped approximately 6 million bpd through Hormuz alone. The Yanbu ceiling of 4.0–4.5 million bpd means Aramco is distributing 56–63% of pre-war Asian export volumes. Every allocation decision is zero-sum.

On April 12, Reuters and Bloomberg reported the East-West Pipeline restored to full 7 million bpd capacity following the IRGC pumping station strike on April 8 — a strike that came hours after the ceasefire was nominally in effect. The restoration loosens the constraint marginally, but the domestic consumption draw and Yanbu port throughput limits remain binding. Prof. Majid al-Moneef, chairman of the Saudi Association for Energy Economics and a former Saudi OPEC Governor, described Aramco’s pipeline rerouting as the Kingdom’s role as “safety valve” of global markets — a valve now under structural strain.

Aramco’s restriction of April liftings to Arab Light grade compounded the problem. Bloomberg reported on March 26 that Saudi Arabia was “giving long-term oil customers the option of receiving their allocations for April via the Red Sea port of Yanbu,” with the option applying “mainly to Arab Light crude” and not replacing full volumes. Arab Medium, Arab Heavy, and Extra Light grades — the workhorses of Asian refinery slates — were unavailable. Customers received a binary choice: accept reduced Arab Light volumes ex-Yanbu, or receive nothing.

The OSP Trap: $19.50 Above a Market That No Longer Exists

The May OSP differential of +$19.50/bbl was set when Brent traded at approximately $109. By April 8, Brent had fallen $17–20 to the $91–95 range, placing the effective OSP $11–15 above spot. The previous record differential was +$9.80 in August 2022. Bloomberg’s pre-announcement survey had expected differentials as high as +$40/bbl; Aramco left $20.50/bbl on the table.

That restraint — analyzed in detail when the May OSP was announced — was not charity. It was the price ceiling above which Aramco’s own term contract buyers would have refused to lift. The +$19.50 already represents a $17/bbl single-month increase from April’s +$2.50.

Saudi Arabia’s fiscal break-even sits at $108–111/bbl, according to Bloomberg calculations that include PIF commitments. Aramco’s dividend was already cut to approximately $85 billion in 2025, down from $124 billion in 2024.

Cutting the OSP would acknowledge that the pricing benchmark — Oman/Dubai — has become untethered from the physical market it is meant to represent. It would also reduce per-barrel revenue at the precise moment when volume is already constrained to 56–63% of pre-war levels. With Goldman Sachs projecting a war-adjusted deficit of $80–90 billion — against an official projection of $44 billion — the arithmetic runs in one direction only.

| Buyer | Tier | Mechanism | Volume Secured (May) | Pre-War Baseline |

|---|---|---|---|---|

| Japan | 1 — Contractual | Okinawa storage-for-priority (2010) | 8.2M bbl entitlement + US supplement | ~40% of imports from Aramco |

| South Korea | 2 — Diplomatic | 7-nation GCC ambassadorial pledge | 80% of needs (~60M bbl April+May) | ~1.0M bpd total crude imports |

| India | 2 — Diplomatic | Bilateral surge (Feb hit 6-year high) | ~1.0–1.1M bpd (Feb rate) | 0.7–0.8M bpd from Saudi |

| China | 2–3 — Mixed | Largest Aramco customer; reduced allocation | ~40M bbl (April) vs 48M bbl (Feb) | ~1.7M bpd from Saudi |

| Commercial queue | 3 — Spot | Record VLCC premiums, reduced volumes | Residual after Tiers 1–2 | Variable |

China’s Structural Arbitrage

China is the buyer that breaks the tier system’s internal logic. Beijing absorbed 1.6 million bpd of Iranian crude in March 2026, the highest volume since November 2025 and approximately 16% of China’s 10 million bpd total seaborne imports, according to Kpler tracking data. Simultaneously, China received 40 million barrels from Saudi Arabia in April — reduced from 48 million in February, a 16.7% cut, but still the single largest country allocation from Aramco.

China is playing both sides because it can. CNPC and Sinopec hold 8 million tonnes per annum of contracted offtake from Qatar’s North Field East plus 5% equity — meaning Beijing’s LNG and crude access routes run through both the Saudi bilateral system and the Iranian-controlled Hormuz corridor simultaneously. China’s 1.2 billion barrels of onshore crude inventory, roughly five months of Middle East import needs, insulates it from pressure by either supplier.

The Al Daayen LNG transit in early April demonstrated the mechanism. A Qatari LNG carrier transited Hormuz toward China at 8.8 knots after Beijing — not Doha — brokered the passage with Iranian intermediaries. Payment was in yuan via Kunlun Bank, outside SWIFT. Al Jazeera framed the arrangement as China and Iran “taking aim at US dollar hegemony.” From Riyadh’s perspective, the framing is less interesting than the fact: China can access Gulf crude through Iran’s toll system while simultaneously receiving Saudi bilateral allocations, extracting advantage from both without committing to either.

The Benchmark Revolt

The allocation crisis has exposed a deeper structural problem in Gulf crude pricing. Asian refiners have formally requested that Saudi Arabia switch the OSP benchmark from Oman/Dubai to ICE Brent. The reason, per Bloomberg reporting on March 19, is that Oman and Dubai benchmarks “have skyrocketed since the start of the war, outpacing gains in global benchmarks.”

The distortion is severe enough that S&P Global Platts excluded Gulf-loading grades from its Market on Close assessment platform — the daily price-discovery process that underpins physical crude trading across Asia. When the benchmark administrator excludes the grades the benchmark is meant to price, the pricing architecture has functionally collapsed.

Aramco’s refusal to switch benchmarks is not stubbornness. Oman/Dubai pricing preserves Saudi nominal pricing authority because the benchmark reflects the scarcity premium that Hormuz closure has created. Switching to ICE Brent would lock in a lower absolute delivered cost for Asian buyers — effectively conceding that Saudi crude should be priced against Atlantic Basin alternatives rather than against the Gulf market Saudi Arabia dominates.

The +$19.50 differential was itself the concession. By holding the differential well below Bloomberg’s expected +$40, Aramco acknowledged the benchmark distortion without formally abandoning the benchmark. The restraint on the differential magnitude was the substitute for the benchmark switch that buyers demanded and Riyadh refused.

Is Iran’s $2M Hormuz Toll Cheaper Than Saudi Allocation?

The bilateral allocation system holds together only as long as the cost of accepting Saudi terms remains lower than the cost of defecting to alternatives. The most dangerous alternative, from Riyadh’s perspective, is Iran’s restricted-passage corridor through Hormuz.

Iran’s toll — $2 million per VLCC, payable in Chinese yuan via Kunlun Bank — grants access to a 5-nautical-mile channel between Qeshm and Larak islands, inside Iranian territorial waters. Ships must provide detailed crew and cargo manifests to IRGC intermediaries. At least two vessels have paid and transited, per Bloomberg reporting.

The arithmetic for a Tier 3 buyer deciding whether to accept Saudi allocation or pay the Iranian toll involves three variables: the delivered cost of Saudi Arab Light at the May OSP (+$19.50 above Oman/Dubai), the delivered cost of alternative crude (Russian Urals, US WTI, West African grades) accessed via the toll corridor, and the VLCC charter premium for Yanbu loading versus Hormuz transit.

VLCC charter rates from Yanbu to East Asia peaked at $450,000/day in early March before settling to approximately $200,000/day. Yanbu spot rates hit $127/tonne on March 12, a 140% increase from March 1. A VLCC loading at Yanbu was $12 million more expensive than a comparable loading from the US Gulf and $17 million more expensive than West Africa, according to Breakwave Advisors.

A Tier 3 buyer loading a 2-million-barrel VLCC at Yanbu pays the OSP premium (approximately $39 million at +$19.50/bbl), the VLCC charter premium (approximately $12 million above US Gulf equivalent), and receives a reduced volume allocation. The same buyer accessing crude through the Iranian toll corridor pays $2 million for transit access and then purchases non-Saudi crude — Russian Urals at a $15–20/bbl discount to Brent, or Iranian crude under OFAC General License U — at a delivered cost potentially $20–30/bbl below the effective Saudi price.

Jim Krane, energy fellow at the Rice University Baker Institute, described the post-war Hormuz arrangement as “an Iranian-controlled fee-for-use waterway” replacing what had been an international transit passage under UNCLOS. The toll removes approximately 20 million bpd from free global circulation; only 3.5–5.5 million bpd is replaceable through bypass pipelines.

For now, the compliance risk of transiting under Iranian terms — sanctions exposure, insurance voidance, flag-state liability — keeps most OECD-allied refiners inside the Saudi allocation system. That compliance shield weakens if the war extends beyond the ceasefire period ending April 22, or if OFAC expands General License U to cover broader Iranian crude purchases.

The June OSP Decision and the Fracture Point

Aramco will announce June OSP differentials around May 5. The decision arrives into a market where Brent has settled $17–20 below the price at which the May OSP was calibrated, where Hormuz throughput remains at 15–20 ships per day versus a pre-war 138, and where the ceasefire expires April 22 with no extension mechanism identified by the Soufan Center or any other monitoring body.

Aramco can hold the differential near +$19.50, preserving fiscal revenue per barrel but accelerating defection by Tier 2 and Tier 3 buyers toward spot alternatives, Russian crude, or Iranian toll access. The OFAC General License U, which authorized Indian crude imports from Iran for the first time since May 2019, already demonstrated the defection path. India’s Saudi imports hit a six-year high in February at 1.0–1.1 million bpd — but that surge coincided with Nayara Energy’s maintenance shutdown removing Russian crude from the Indian market. When Nayara restarts, India’s Saudi purchases will fall unless Aramco offers volume priority that competes with the GL U pricing advantage.

Aramco can cut the differential substantially — back toward the +$2.50 that prevailed in April — acknowledging the benchmark distortion and attempting to hold market share by making the headline price competitive. But a cut from +$19.50 to even +$10 — a reduction of $9.50 per barrel — would cost approximately $1.1–1.3 billion in monthly revenue against the current Yanbu export volume of 4.0–4.5 million bpd. With the Goldman Sachs deficit estimate already at $80–90 billion, the fiscal space for price concessions is effectively zero.

Or Aramco can deepen the bilateral allocation system — offering Tier 2 buyers explicit volume guarantees at the current OSP, extending the South Korea model to India, Taiwan, and Thailand, and accepting that the posted price becomes a political instrument maintained for fiscal accounting purposes while actual market clearing happens through government-to-government volume deals.

| Scenario | Differential | Monthly Revenue Impact vs. May | Buyer Defection Risk |

|---|---|---|---|

| Hold near +$19.50 | +$18–20 | Neutral | High — Tier 3 defects to Iranian toll or Russian crude |

| Moderate cut | +$8–12 | −$0.9–1.6B/month | Medium — holds Tier 2, loses fiscal margin |

| Deep cut to pre-war levels | +$2–4 | −$1.9–2.4B/month | Low — but validates benchmark distortion permanently |

The IEA’s release of 400 million barrels from strategic reserves on March 11 — described as “unprecedented” — provided a temporary cushion. But strategic reserves are a finite buffer, not a structural solution. They buy time for the allocation system; they do not fix the pricing architecture beneath it.

The 1973 Architecture, Inverted

The closest historical parallel is the 1973 Arab oil embargo, and the structural similarities are more precise than the analogy might suggest. During the 1973 crisis, European states reached individual bilateral deals with Saudi Arabia, Iraq, and Iran — each securing volume allocations at the official posted price while the Netherlands, targeted by the embargo, was excluded. The mechanism was identical: sellers maintained a uniform headline price while differentiating physical access by political relationship.

The 2026 system inverts the political logic. In 1973, selective allocation punished adversaries — the Netherlands, the United States, Portugal. In 2026, it rewards allies — Japan, South Korea, India, and selectively the UAE’s downstream partners. The architecture is the same; the directional flow of political favor is reversed.

The inversion has a structural consequence that the 1973 precedent did not. In 1973, excluded buyers had no alternative supplier willing to break the embargo at a competitive price. In 2026, excluded buyers — or buyers insufficiently prioritized in the allocation queue — have Iran’s toll corridor, Russian Urals at a $15–20/bbl discount, and a growing fleet of dark-fleet tankers willing to load sanctioned crude outside established insurance frameworks. The Saudi allocation system faces competitive pressure from below that OPEC’s 1973 cartel never confronted.

We have received commitments to prioritize allocations to Korea. If our ships can operate with assured safety, we will be able to secure the volumes.

Kim Jung-kwan, South Korea Trade Minister, April 12, 2026

Frequently Asked Questions

Why doesn’t Saudi Arabia simply lower the OSP to retain Asian buyers?

Lowering the OSP differential from +$19.50 would reduce per-barrel revenue when export volumes are already constrained to 56–63% of pre-war levels by the Yanbu port ceiling. Saudi fiscal break-even requires $108–111/bbl. At current Brent prices of $91–95, each dollar of OSP reduction costs approximately $130–150 million per month against 4.0–4.5 million bpd of Yanbu throughput. A cut to pre-war levels (+$2–4) would widen the Goldman Sachs-estimated $80–90 billion deficit by an additional $70–90 billion annualized — an amount that exceeds PIF’s liquid reserves drawdown capacity without triggering credit rating action.

How does the bilateral allocation system differ from normal Aramco term contracts?

Standard Aramco term contracts specify annual volume commitments at the monthly OSP differential, with Aramco retaining the right to adjust nominated volumes by ±10% at its discretion. The wartime bilateral system layers government-to-government diplomatic commitments on top of the commercial contract framework. South Korea’s 80% May allocation was secured not through Aramco’s commercial department but through ambassadorial pledges from seven sovereign governments — a mechanism with no precedent in Aramco’s post-1988 pricing history. The distinction matters because diplomatic volume commitments are not enforceable through commercial arbitration, creating a two-track system where legal contracts (Japan’s Okinawa arrangement) and political promises (South Korea’s GCC pledges) coexist without a unified enforcement framework.

Can China be excluded from the allocation system for buying Iranian crude?

Saudi Arabia reduced China’s April allocation by 16.7% — from 48 million barrels in February to 40 million — but a full cutoff is structurally impossible. China remains Aramco’s single largest customer globally. More fundamentally, China’s 1.2 billion barrels of onshore crude inventory provides approximately five months of insulation from supply pressure, meaning a Saudi cutoff would hurt Aramco’s revenue before it constrained Chinese refiners. Beijing’s simultaneous access to Iranian crude (1.6 million bpd in March via the toll corridor) and Saudi bilateral allocations gives it a hedged position that no other buyer replicates.

What happens to the allocation system if the ceasefire collapses after April 22?

A ceasefire collapse would likely trigger renewed IRGC strikes on Saudi energy infrastructure — the April 8 East-West Pipeline pumping station attack occurred hours after the ceasefire nominally took effect. If the pipeline is degraded below its restored 7 million bpd capacity, the Yanbu export ceiling falls further, tightening the allocation pool and forcing Aramco to choose between maintaining Tier 2 diplomatic commitments or preserving commercial volumes for Tier 3 buyers who generate higher per-barrel margin through spot-market premiums. The IEA’s 400-million-barrel strategic reserve release on March 11 provides roughly 60–90 days of cushion at current draw rates.

Will OPEC+ intervene to coordinate allocation across member states?

OPEC+ paused output adjustments at its April 5 meeting, deferring to bilateral market dynamics. The UAE’s separate 24-million-barrel pledge to South Korea — explicitly designated as “number one priority” — demonstrates that allocation decisions are being made at the sovereign-bilateral level, not through the OPEC+ coordination framework. Kuwait and Qatar made similar pledges through the seven-nation ambassadorial commitment on April 7. Each member state is building its own hierarchy of preferred buyers, creating overlapping and potentially conflicting bilateral networks that no OPEC+ ministerial meeting has attempted to rationalize.