DHAHRAN — Brent crude closed March 30 at $115.35 per barrel, capping the largest monthly price surge in the benchmark’s four-decade history at approximately 60 percent. Saudi Arabia, the world’s largest oil exporter with more than 9 million barrels per day of pre-war capacity, should be collecting record revenue. Instead, with the Strait of Hormuz shut since early March and Houthi forces now threatening to close Bab al-Mandeb, the kingdom is leaving an estimated $500 million to $600 million per day on the table.

The gap between what Saudi Arabia could earn and what it can actually ship defines the central paradox of this war’s oil shock. At $115 per barrel, full-capacity exports would generate roughly $1 billion per day. Actual exports through the Yanbu bottleneck on the Red Sea yield $400 million to $500 million per day, according to tanker-tracking data compiled by Vortexa and Kpler.

Table of Contents

- The Record: 60 Percent in 31 Days

- Why Can’t Saudi Arabia Cash the Check?

- The Double Chokepoint: Hormuz and Bab al-Mandeb

- How Does March 2026 Compare to Past Oil Shocks?

- Quantifying the Daily Revenue Gap

- What Does the Price Spike Mean for the Global Economy?

- Background: 31 Days From $72 to $115

- Frequently Asked Questions

The Record: 60 Percent in 31 Days

Brent crude opened March at approximately $72 per barrel, according to ICE Futures data. It closed March 30 at $115.35, a gain of roughly 60 percent in a single calendar month. That surpasses the previous record of 46 percent set in September 1990, when Iraq’s invasion of Kuwait sent prices from $23.73 to $34.64 per barrel, according to EIA historical price data.

The speed of the March 2026 move reflects something qualitatively different from past supply shocks. In 1990, the disruption removed roughly 4.3 million barrels per day from global supply. The Hormuz closure has removed approximately 17.8 million barrels per day of crude and condensate flow, according to the International Energy Agency’s March 2026 Oil Market Report. That represents nearly 20 percent of global daily supply passing through a single waterway that Iran’s Islamic Revolutionary Guard Corps sealed in the first week of the war.

WTI crude traded at $101 to $103 per barrel on March 30, while the OPEC Reference Basket averaged $115.88 per barrel, according to OPEC’s daily basket price. The WTI-Brent spread has widened to roughly $13, reflecting the fact that American producers face less direct supply disruption than waterborne crude markets.

Why Can’t Saudi Arabia Cash the Check?

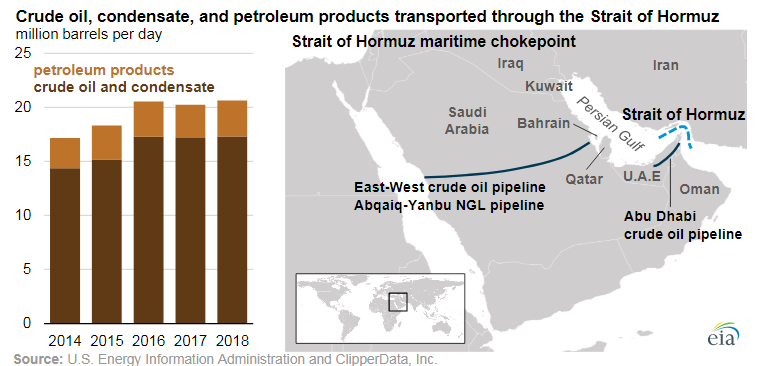

Saudi Arabia’s pre-war export capacity exceeded 9 million barrels per day, with roughly 6 to 7 million barrels per day flowing through eastern terminals at Ras Tanura and Ju’aymah into the Persian Gulf and out through the Strait of Hormuz. When the IRGC closed Hormuz in early March, Aramco activated its primary contingency: the East-West Pipeline, a 1,200-kilometer artery connecting the Eastern Province oil fields to the Red Sea port of Yanbu.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The pipeline hit its maximum throughput of 7 million barrels per day by March 28, according to Aramco. That was a technical achievement. The problem lies at the other end.

Yanbu’s port infrastructure, designed to handle roughly 1 to 1.5 million barrels per day under normal operations, was pushed to a peak of 5.9 million barrels on March 9, according to IEA data. But sustained loading rates have settled closer to 4 to 5 million barrels per day, with approximately 40 tankers queuing offshore at any given time, according to Maritime Executive reporting.

Of the 7 million barrels per day flowing through the pipeline, approximately 2 million barrels per day are consumed domestically by refineries in Riyadh, Yanbu, and Jazan, as well as power plants and desalination facilities, according to Asharq Al-Awsat. That leaves roughly 5 million barrels per day available for export, but port loading constraints mean actual sustained export volumes hover between 3.5 and 5 million barrels per day.

Aramco CEO Amin Nasser, who cancelled his CERAWeek appearance in Houston, described the blockade as “by far the biggest crisis the region’s oil and gas industry has faced” in an emergency briefing on March 10, according to Semafor. He warned of “catastrophic consequences” for the global economy if the disruption continued, and revealed that Aramco was drawing on storage facilities around the world to meet customer commitments.

The Double Chokepoint: Hormuz and Bab al-Mandeb

No oil exporter in recorded history has faced the simultaneous closure or threat of closure of both its primary and secondary export chokepoints. The Strait of Hormuz, shut since approximately March 2 to 4, handles 17.8 million barrels per day of crude flows under normal conditions, according to the IEA. Saudi Arabia’s fallback was the Red Sea route through Yanbu, which requires tankers to transit Bab al-Mandeb to reach European and Asian markets via the Suez Canal.

On March 29, Mohammed Mansour, the Houthis’ deputy information minister, told local media that the group is “conducting this battle in stages, and closing the Bab al-Mandeb strait is among our options,” according to Al Jazeera and Middle East Monitor. Mansour stated the Houthis are coordinating with Iran, Lebanon, and Iraq, having joined the conflict “to provide support to our brothers in Iran.”

Houthi military spokesperson Brigadier-General Yahya Saree announced missile strikes targeting Israel on March 28, with a second operation claimed on March 29, according to CNBC. Red Sea shipping traffic was already “sharply reduced” before any formal blockade, according to Kpler maritime tracking data.

The strategic arithmetic is straightforward. If Bab al-Mandeb closes, tankers loading at Yanbu face a choice: turn south around the Cape of Good Hope, adding 10 to 14 days and tens of millions of dollars in freight costs, or not sail at all. Either option compresses the volume of Saudi crude reaching global markets further. The IRGC’s formalized yuan-denominated toll system at Hormuz already selectively permits some vessels from China, India, and allied nations to pass, but Saudi-flagged or Saudi-bound tankers remain blocked.

How Does March 2026 Compare to Past Oil Shocks?

March 2026 is the most severe single-month price event in the history of internationally traded crude oil. The comparison table below places it alongside every major oil shock since the OPEC era began.

| Event | Year | Monthly Peak Gain | Supply Disrupted (bpd) | Duration of Price Spike |

|---|---|---|---|---|

| Iran War / Hormuz Closure | 2026 | ~60% | ~17.8 million | Ongoing (31 days) |

| Gulf War / Kuwait Invasion | 1990 | 46% | ~4.3 million | ~7 months |

| Russia-Ukraine War | 2022 | ~20-25% | ~1-2 million (sanctions lag) | ~4 months |

| Iranian Revolution | 1979 | ~15-20% | ~3.5 million | ~12 months |

| Arab Oil Embargo | 1973-74 | ~30% (cumulative) | ~4.4 million (embargo) | ~6 months |

The 1973 Arab oil embargo quadrupled prices but did so over several months. The 1979 Iranian Revolution doubled them over a longer period still. The 1990 Gulf War spike, until now the single-month record, involved a disruption one-quarter the size of the current Hormuz closure. The 2022 Russia-Ukraine spike peaked at roughly 20 to 25 percent monthly gains before sanctions regimes and supply rerouting stabilized markets, according to EIA data.

What distinguishes 2026 is the combination of scale and chokepoint concentration. In 1990, oil could still flow through Hormuz because Iraq and Kuwait were the disrupted producers, not the transit corridor. In 2026, the corridor itself is closed. Aramco has imposed a $40 per barrel premium over benchmark prices for Asian customers, reflecting scarcity that transcends the price itself.

Quantifying the Daily Revenue Gap

The mathematics of Saudi Arabia’s revenue paradox are stark. At pre-war export capacity of approximately 9.5 million barrels per day and today’s price of $115.35 per barrel, theoretical daily revenue would reach $1.096 billion. At actual export volumes of 3.5 to 5 million barrels per day through Yanbu, daily revenue falls to $404 million to $577 million.

| Scenario | Export Volume (bpd) | Price ($/barrel) | Daily Revenue |

|---|---|---|---|

| Pre-war full capacity | ~9.5 million | $115.35 | ~$1.096 billion |

| Yanbu peak loading | ~5 million | $115.35 | ~$577 million |

| Yanbu sustained average | ~4 million | $115.35 | ~$461 million |

| Yanbu conservative estimate | ~3.5 million | $115.35 | ~$404 million |

| Pre-war normal (Feb 2026) | ~7.5 million | $72 | ~$540 million |

The paradox sharpens when comparing current revenue to pre-war levels. At February prices of roughly $72 per barrel and normal export volumes of approximately 7.5 million barrels per day, Saudi Arabia was earning about $540 million per day. At the Yanbu sustained average of 4 million barrels per day and $115.35, the kingdom earns approximately $461 million per day. The price has risen 60 percent, yet daily revenue may have fallen by roughly $80 million from pre-war levels.

Over 31 days of conflict, the gap between theoretical full-capacity exports and actual Yanbu-constrained volumes means Saudi Arabia has left an estimated $15 billion to $21 billion on the table, according to calculations based on Vortexa tanker-tracking data and ICE Futures pricing.

The kingdom’s fiscal position, however, remains stable. Saudi Central Bank (SAMA) data published in March showed foreign reserve assets at a six-year high of SAR 1.78 trillion (approximately $475 billion), up 10 percent year-on-year, according to Arab News. The reserves provide a substantial buffer, though they were accumulated at pre-war production levels that may not return quickly. The subsequent April tariff shock has since transformed that buffer calculus: with Brent collapsing to $65 while the Yanbu ceiling held, the projected 2026 deficit has widened to roughly $110 billion — forcing a reserve drawdown that the March picture did not anticipate.

What Does the Price Spike Mean for the Global Economy?

The OECD’s Interim Economic Outlook, published March 26, revised global inflation projections upward by 1.2 percentage points for 2026 to 4 percent across the G20, according to the OECD’s March 2026 report. The United States faces a projected inflation rate of 4.2 percent, up sharply from the prior forecast of 2.8 percent, according to CNBC. Global GDP growth was revised to 2.9 percent, with the OECD noting that early-year indicators had pointed to a 0.3 percentage point upgrade before the Middle East conflict “entirely erased that boost.”

The OECD warned that a prolonged disruption could reduce global GDP by an additional 0.5 percent in the second year, while consumer prices would rise by 0.7 percentage points in year one and 0.9 percentage points in year two. The report’s simulations assumed oil and gas prices rising “well above baseline projections by around a quarter in the first year” and remaining elevated thereafter.

For Saudi Arabia specifically, the budget implications are mixed. The 2026 budget was prepared on an assumed oil price of approximately $78 to $85 per barrel, according to the Ministry of Finance’s Budget Statement. Prices are now 35 to 48 percent above that assumption. The Public Investment Fund has already cut spending by 15 percent, according to Financial Times reporting, a measure taken before the war began as part of broader fiscal consolidation.

Aramco’s 2025 net income of $93.4 billion, down 12 percent year-on-year according to the company’s annual results, was achieved at lower prices and full production. The 2026 earnings trajectory depends entirely on how quickly export volumes recover. Record prices at half-capacity production could produce roughly flat or even lower annual revenue compared to 2025 full-capacity output at moderate prices.

“We are no longer talking about a mere price spike. We are witnessing a systemic failure of the global energy architecture.”

Amin Nasser, CEO of Saudi Aramco, emergency briefing, March 10, 2026

From Tehran, the IRGC offered a different reading. Ebrahim Zolfaqari, a spokesperson for the IRGC’s Khatam al-Anbiya Central Headquarters, warned in mid-March: “Get ready for oil to be $200 a barrel, because the oil price depends on regional security, which you have destabilized,” according to Al Jazeera. The IRGC stated that “not a litre of oil” would pass through Hormuz, and that any vessel linked to the United States, Israel, or their allies would be considered “a legitimate target.”

The war’s long-term energy transition implications may ultimately matter more than the immediate price spike. European and Asian governments that spent the first week of March scrambling for emergency oil supplies are now accelerating renewable energy investment timelines and strategic petroleum reserve policies that will permanently reduce crude demand.

Background: 31 Days From $72 to $115

The conflict began on February 28 when the United States and Israel launched joint military strikes against Iran. The IRGC responded by closing the Strait of Hormuz within days. By March 8, Brent crude had crossed $100 per barrel for the first time in four years, according to CNN.

Saudi Arabia moved quickly to activate the East-West Pipeline. Yanbu exports surged from 760,000 barrels per day in February to 2.47 million barrels per day in the first week of March, more than tripling, according to Kpler data. By late March, loadings had reached 4 to 5 million barrels per day.

Prince Faisal bin Farhan, the Saudi foreign minister, reserved the kingdom’s “right to take military action” on March 19. Saudi Arabia expelled the Iranian military attache on March 21.

The Houthi entry into the conflict on March 28 opened a second front that directly threatens the Yanbu workaround. Bab al-Mandeb carries approximately 8.2 million barrels per day of crude and petroleum products under normal conditions, according to the EIA. Even before the Houthis’ formal threat, shipping insurance premiums for Red Sea transits had risen sharply, and some tanker operators were already diverting south around the Cape of Good Hope.

The broader strategic bargain between Washington and Riyadh is also under strain. The United States, itself now facing 4.2 percent projected inflation partly driven by energy costs, has limited tools to restore Saudi export capacity short of reopening Hormuz through military action. President Trump has threatened to seize Iranian oil assets, according to reporting on his Kharg Island statements, but that would add supply only if the seized infrastructure remained operational.

For now, the largest monthly oil price surge ever recorded is producing a result that no market model anticipated: the biggest exporter on the planet is watching the windfall it cannot collect. The damage extends beyond crude oil: Sadara Chemical has shut down all 26 plants at its $20 billion Jubail petrochemical complex, stripping millions of tonnes of annual capacity from global markets while its debt clock ticks toward a June 15 deadline.

Frequently Asked Questions

Could Saudi Arabia build additional port infrastructure at Yanbu to increase loading capacity?

Major port expansion at Yanbu would require construction of new berths, storage tanks, and single-point mooring systems, a process that typically takes 18 to 36 months under peacetime conditions, according to port engineering assessments by the International Association of Ports and Harbors. Aramco has explored emergency measures including floating storage and offshore loading platforms, but these provide marginal capacity gains of roughly 500,000 to 800,000 barrels per day, not the 3 to 4 million barrels per day needed to replace Hormuz-routed exports.

What happens to Saudi oil revenue if both Hormuz and Bab al-Mandeb close simultaneously?

If Bab al-Mandeb were formally blockaded, Saudi tankers could still reach Asian markets by sailing south from Yanbu around the Cape of Good Hope, adding approximately 10 to 14 days to the voyage. Freight costs would rise by an estimated $3 million to $5 million per VLCC voyage, according to Clarksons Research, effectively reducing Aramco’s net revenue per barrel by $2 to $4. More critically, the extended voyage time would reduce the effective fleet capacity available for Saudi crude, potentially cutting realized exports to 2 to 3 million barrels per day.

Has Saudi Arabia ever faced a complete export blockade before?

Saudi Arabia participated in the 1973 Arab oil embargo, but that was a voluntary production cut, not a physical blockade. During the 1984 to 1988 Tanker War between Iran and Iraq, Saudi vessels were attacked in the Persian Gulf, but Hormuz remained open under international naval escort. The closest historical parallel is Iraq’s 1990 invasion of Kuwait, which shut Iraqi and Kuwaiti exports but left Saudi terminals operational. March 2026 is the first time Saudi Arabia has lost access to its primary eastern export terminals due to hostile action.

Why hasn’t the IEA strategic petroleum reserve release stabilized prices?

The IEA coordinated an emergency release from member nations’ strategic reserves in early March, but IEA member states collectively hold approximately 1.2 billion barrels of emergency stocks, according to the IEA’s March 2026 report. At a maximum drawdown rate of 4 to 5 million barrels per day, those reserves could sustain supplementary supply for 8 to 10 months. However, SPR releases address temporary shortfalls, not structural chokepoint closures. Markets have priced in the reality that reserves are a stopgap, not a solution, until Hormuz reopens.

How does the Aramco $40 premium affect Asian refiners?

Aramco’s $40 per barrel premium over benchmark pricing means Asian refiners that typically purchase Arab Light at a $1 to $3 premium to the Dubai/Oman average are now paying roughly $155 per barrel for delivered crude, according to Platts assessments. Several Chinese and Indian refiners have turned to Russian Urals crude and Iranian oil transiting through the IRGC’s Hormuz toll system as cheaper alternatives, accelerating a market fragmentation that may outlast the conflict itself.