DHAHRAN — The United States has struck Kharg Island twice in thirty-six days. Both times it left the oil terminals standing. The question facing Saudi Arabia is what happens when it doesn’t — and whether Aramco can fill the resulting vacuum without turning its own export infrastructure into the next target on the IRGC’s counter-strike list.

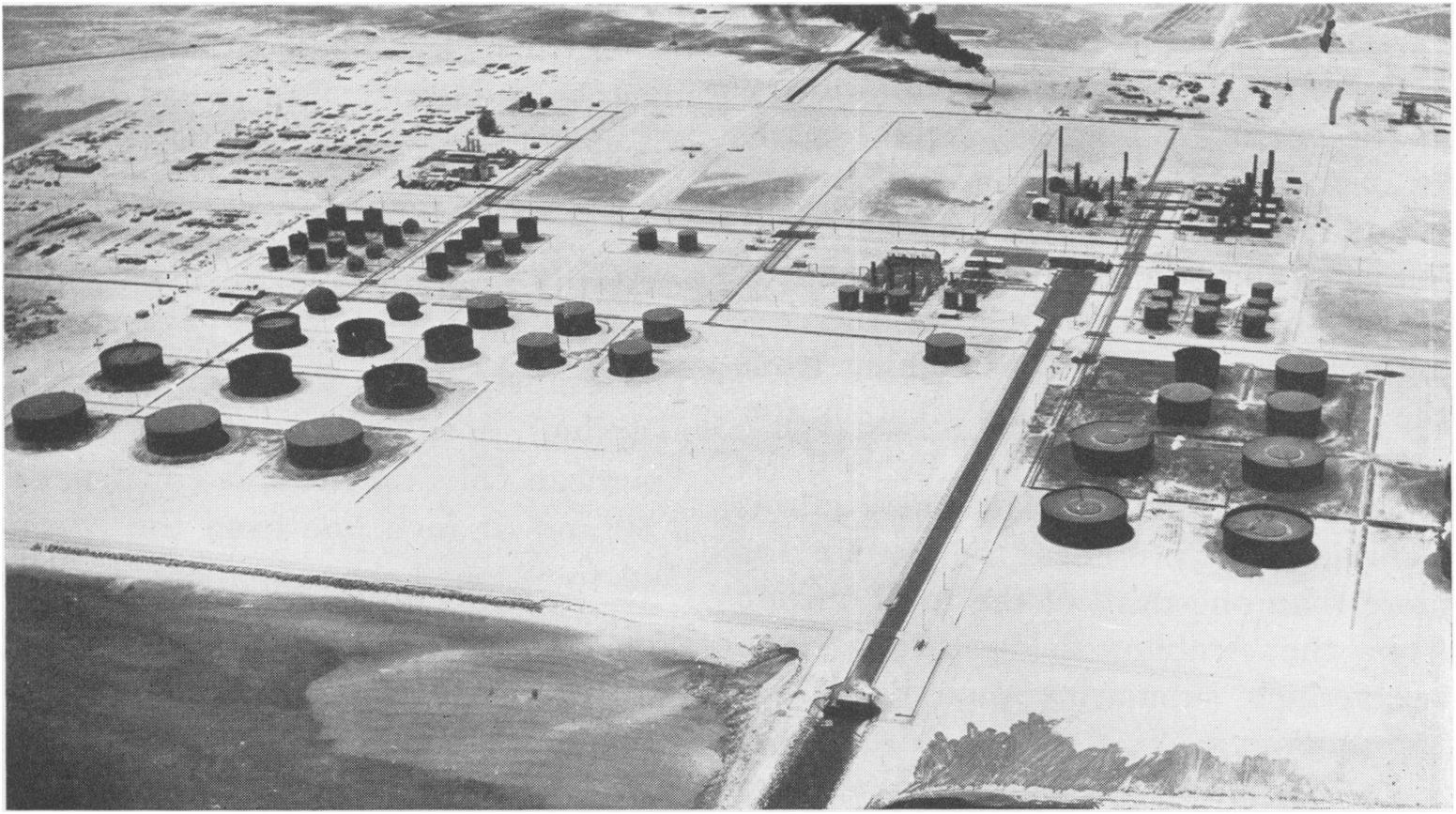

Kharg Island processes roughly 90 percent of Iran’s crude oil exports, loading approximately 1.52 million barrels per day across three terminal systems on a coral island twenty miles off the Iranian coast (Kpler, March 2026). Iran earned $139 million per day from oil exports in March — up $24 million per day from February — while the rest of the Gulf’s producers watched their own tankers sit idle or reroute at enormous cost (Bloomberg). If Kharg goes dark, roughly 1.6 million barrels per day disappear from global supply. Saudi Arabia has the spare capacity to replace most of it. The problem is that doing so transforms Aramco’s terminals from bystander infrastructure into active instruments of Iran’s economic destruction — precisely the justification the IRGC needs for the strike it has already threatened.

Table of Contents

- Kharg Is Still Standing — and Still Paying for the War

- What Happens to Saudi Spare Capacity If Kharg Goes Offline?

- The Co-Belligerence Trap

- Can Saudi Arabia Fill the Gap Without Becoming the Target?

- The Yanbu Bottleneck

- What Does the Tanker War Teach About Kharg’s Resilience?

- Iran’s Bypass Is a Fiction at Current Capacity

- Pezeshkian’s Three-to-Four-Week Clock

- Does Saudi Arabia Need the Barrels or the Price?

- Frequently Asked Questions

Kharg Is Still Standing — and Still Paying for the War

On March 13, the United States Air Force destroyed more than ninety military targets on Kharg Island — naval mine storage facilities, missile storage bunkers, air defenses — in what CENTCOM called a “large-scale precision strike.” The oil infrastructure, spread across the Kharg Terminal’s east-coast T-shaped jetty, the Sea Island Terminal off the west coast, and the Darius Terminal in the south, was left intact. President Trump said he had chosen “for reasons of decency” not to destroy it. Satellite imagery taken days later showed three tankers still moored at the terminal (Al Jazeera; Wikipedia/2026 Kharg Island raid).

On April 7, the U.S. struck again. Mehr News Agency reported multiple explosions across the island. NBC News confirmed the strikes targeted “dozens of military targets” — not oil infrastructure. The terminals kept loading. A full operational account of the second Kharg strike is in US Strikes 50 Military Targets on Kharg Island, Spares Oil Terminal Again.

Moussa Ahmadi, head of Iran’s parliamentary energy commission, stated on April 4 that “in recent days not only have oil exports not decreased, but they have increased” (Al Arabiya). Iran’s oil revenue in March surged to approximately $139 million per day, up from $115 million per day in February (Bloomberg, March 26, 2026). The country that is supposedly being economically strangled by the most intensive bombing campaign in the Gulf since 1991 actually improved its cash flow by 21 percent in four weeks.

This revenue has direct military consequences. Iran’s 2025 budget allocated $12.4 billion in oil revenue directly to the armed forces. The IRGC alone received over 311 trillion tomans — roughly $6 billion — nearly twice the regular army’s allocation (Iran Open Data). Approximately 47 percent of Iran’s $23.1 billion military budget is funded through special crude oil quotas rather than cash transfers. Every tanker that loads at Kharg’s jetties finances a share of the missile inventory aimed at Ras Tanura, Abqaiq, and the East-West Pipeline.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

What Happens to Saudi Spare Capacity If Kharg Goes Offline?

Saudi Arabia’s maximum sustainable crude production capacity is approximately 12.2 million barrels per day (S&P Global). Current production runs at roughly 10.1 to 10.2 million bpd, leaving an estimated 1.4 to 2 million bpd of spare capacity — enough, in theory, to absorb most of Kharg’s 1.52 million bpd throughput.

The OPEC+ April 5 meeting produced a symbolic output increase of 206,000 bpd. At $110 Brent, every OPEC+ member is financially rewarded to produce more. The output increase functions as political signal management, not genuine supply strategy — given that infrastructure damage and Hormuz restrictions limit real-world deliverability for most producers (Reuters/gCaptain). Saudi Arabia is the only major Gulf producer with both a functioning Hormuz bypass and meaningful spare capacity.

The arithmetic is simple. If Kharg goes offline and Saudi Arabia fills the gap, Aramco captures not just additional volume but pricing power over every Asian refiner currently dependent on Iranian crude — at prices Goldman Sachs has warned could exceed the 2008 record of $147 per barrel if Strait disruptions worsen (Bloomberg/FX Leaders). Saudi Arabia’s fiscal breakeven is approximately $80-85 per barrel (Middle East Insider). At $110 Brent, the kingdom generates an estimated $900 million per day in oil revenues. At $147, it would be closer to $1.2 billion.

| Metric | Iran (Kharg) | Saudi Arabia |

|---|---|---|

| Primary export volume | ~1.52M bpd (90% of exports) | ~7M bpd via Yanbu bypass |

| Export revenue (March 2026) | $139M/day | ~$900M/day |

| Bypass terminal capacity | Jask: ~0.3M bpd effective | Yanbu: 7M bpd (at max) |

| Spare production capacity | Minimal | 1.4–2M bpd |

| Fiscal breakeven | ~$144/bbl (IMF est.) | ~$80-85/bbl |

| Gulf terminal exposure | Kharg (struck twice) | Ras Tanura (struck March 2) |

| Military budget from oil | 47% ($10.9B via crude quotas) | ~$75B total defense (broader base) |

The Co-Belligerence Trap

Iran’s threat architecture is explicit. The IRGC warned via state media on April 7 that all oil and gas infrastructure in the region where the U.S. and its allies hold interests would be “set on fire and destroyed” if Iranian oil infrastructure is hit (NBC News). Foreign Minister Abbas Araghchi, through Tasnim News Agency, specified the targeting logic: “If Iranian facilities are targeted our forces will target facilities of American companies in the region or companies in which the United States has shares.” That formulation covers Aramco. It covers every refinery, processing plant, and terminal in which American institutional capital holds a position.

The IRGC’s escalation doctrine, as analyzed by Mona Yacoubian of CSIS, rejects calibrated responses in favor of what she calls “unbridled escalation” — horizontal expansion across nations and vertical escalation from military to civilian to energy infrastructure to data centers. Iran does not distinguish between a military combatant and an economic one. If Saudi Arabia fills the barrel gap left by Kharg’s destruction, the IRGC’s doctrinal framework treats that as economic warfare requiring kinetic response.

This is not theoretical. Ras Tanura — Saudi Arabia’s largest refinery complex, handling approximately 3.4 million bpd — was struck by Iranian drones on March 2, 2026. Two drones were intercepted; shrapnel caused a minor fire; the facility reopened after roughly a week (Euronews/Wikipedia). The IRGC demonstrated willingness to hit Aramco infrastructure when it perceived military justification. Saudi Arabia has intercepted 894 Iranian drones and missiles since March 3 — but its PAC-3 MSE stockpile is estimated at roughly 400 rounds, down from approximately 2,800, with Camden Arsenal producing only 620 per year.

Seth G. Jones, Harold Brown Chair at CSIS, identified three Saudi installations as Iran’s most likely escalation targets: Abqaiq — the world’s largest oil processing facility at 7-plus million bpd capacity — Ras Tanura at 3.4 million bpd, and Yanbu at 1.3 million bpd. His assessment places Iran’s escalation threshold at “actions that threaten the regime’s survival.” Losing $139 million per day in oil revenue meets that standard.

JPMorgan analysts separately identified Ras Tanura and Abqaiq as “potentially vulnerable targets” following any Kharg infrastructure strike (Euronews). Roukaya Ibrahim of BCA Research put it directly: “Not only would an attack on Kharg Island’s oil infrastructure damage Iran’s export capacity, it would also increase the risk of wider attacks on regional energy infrastructure.”

Can Saudi Arabia Fill the Gap Without Becoming the Target?

The operational question is whether Saudi Arabia can increase production to capture Kharg’s lost volume without crossing the line — in Iranian doctrinal terms — from non-belligerent to co-belligerent. The answer is almost certainly no, because the IRGC’s targeting logic does not require Saudi Arabia to declare itself a party to the conflict. It requires only that Saudi actions “threaten the regime’s survival.”

An additional 1.4 to 2 million bpd of Saudi production replacing Iranian barrels would accomplish precisely that. Iran’s annual oil revenue was approximately $53 billion in 2025, representing roughly 11 percent of GDP (CFR/IEA). The FDD estimates roughly half of Iran’s total government revenue comes from oil and gas. Replacing those barrels with Saudi crude does not just take market share. It collapses the revenue stream that funds the IRGC, the regular army, and the ballistic missile program — roughly $10.9 billion annually allocated through direct crude quotas.

The IRGC has already stated, via PressTV and GlobalSecurity on April 5: “The Strait of Hormuz will never return to its previous status, especially for the US and Israel.” Iran is not blockading Hormuz entirely — it is franchising it, granting selective exemptions to Chinese and Iraqi tankers while choking competitors. A Saudi production surge to replace Iranian barrels would end whatever ambiguity remains about Riyadh’s role. The IRGC’s counter-target list already includes King Fahd Causeway, Ras Tanura, and — per CSIS — Abqaiq.

The Yanbu Bottleneck

Saudi Arabia’s strategic advantage in this conflict is the East-West Pipeline to Yanbu, which allows crude to bypass the Strait of Hormuz entirely by routing it 1,200 kilometers across the Arabian Peninsula to Red Sea terminals. Aramco CEO Amin Nasser confirmed in March 2026 that the pipeline has reached its maximum operating capacity of 7 million bpd (S&P Global).

That confirmation contains the constraint. The pipeline is full. Any additional Saudi production above the current Yanbu throughput must flow through Gulf-facing terminals — Ras Tanura, Ju’aymah, and the offshore platforms that sit within range of every Iranian ballistic missile, cruise missile, and drone in the IRGC’s inventory. CSIS’s assessment confirms that all major Saudi Gulf facilities fall within 2,000-kilometer range of Iranian launch sites.

The arithmetic is unforgiving. If Saudi Arabia raises production by 1.5 million bpd to fill the Kharg gap, those barrels cannot go through Yanbu. They go through the same Gulf terminals that the IRGC has already struck once and threatened to destroy. Each additional barrel routed through the Gulf is a barrel that increases Saudi exposure without additional defensive coverage. The PAC-3 stockpile is not expanding — Camden Arsenal’s production of 620 rounds per year cannot replenish the estimated 2,400 already expended. Poland refused a Patriot transfer on March 31. The $16.5 billion in emergency arms sales went to the UAE, Kuwait, and Jordan — not Saudi Arabia.

What Does the Tanker War Teach About Kharg’s Resilience?

Iraq bombed Kharg Island repeatedly beginning in 1984, using French-supplied Super Etendard fighters armed with Exocet missiles. The objective was identical to Washington’s current pressure point: choke off Iranian oil revenue to force a settlement. The result was four more years of war.

Iran responded with infrastructure repair, route diversification to Sirri and Larak Islands further south, a twenty-tanker shuttle service escorted by Iranian fighter jets, and aggressive price discounting to offset higher shipping insurance premiums. Lloyd’s of London recorded 546 commercial vessels damaged and 430 civilian sailors killed before it ended (Britannica). Iran’s oil exports continued throughout, though at reduced volume and lower prices.

The 2026 baseline is substantially weaker than the 1984 baseline. Iran entered this war with 40-plus percent of the population below the absolute poverty line, the rial at 1,430,000 to the dollar, and inflation on basic goods running at 105 to 115 percent by February 2026 (The Defense News). The economic cushion that allowed Iran to absorb four years of Kharg strikes in the 1980s does not exist today. But the institutional instinct — repair, reroute, discount, endure — remains embedded in the IRGC’s operational culture. A CIA assessment declassified in 1984 described Kharg as “the most vital” facility in Iran’s oil system. Forty-two years later, with Kharg processing approximately 90 percent of Iran’s crude exports, the assessment is structurally identical (CFR).

Iran’s Bypass Is a Fiction at Current Capacity

Iran’s Jask terminal on the Gulf of Oman — connected to southern oil fields via the Goreh-Jask pipeline — was designed to provide exactly the kind of Hormuz bypass that the East-West Pipeline provides Saudi Arabia. Its design capacity is 1 million bpd. Its effective throughput as of March 2026 is approximately 0.3 million bpd (Kpler). The first crude loading since September 2024 occurred on March 7, when a single tanker, the Dore, loaded 2 million barrels.

Jask cannot absorb Kharg’s volume. At 0.3 million bpd effective capacity, it covers roughly 20 percent of Kharg’s 1.52 million bpd throughput. If Kharg’s oil infrastructure is destroyed, Iran loses access to approximately 1.2 million bpd of export capacity with no near-term replacement. The Tanker War-era workaround — shuttling crude to Larak and Sirri — required years to develop and operated at dramatically reduced volumes. Iran does not have years. President Pezeshkian said as much.

Pezeshkian’s Three-to-Four-Week Clock

President Masoud Pezeshkian warned the IRGC in March that Iran’s economy could face “total collapse within three to four weeks” without a ceasefire (The Defense News). The indicators supporting that assessment: oil revenue’s share of the national budget had fallen from 32 percent to approximately 5 percent; government employees had gone unpaid for up to three months; ATMs had run out of cash in multiple cities; inflation on basic goods was running at 105 to 115 percent.

The IRGC has not responded to Pezeshkian’s warning with concessions. Mojtaba Khamenei — now acting as supreme leader after his father’s prolonged absence — vowed to keep blocking the Strait of Hormuz and to continue attacking Gulf states (NBC News). Pezeshkian himself posted on April 7: “Ready to give my life for Iran” — accompanied by claims of 14 million volunteers willing to defend infrastructure (Jerusalem Post/Military.com).

If Kharg’s oil terminals are destroyed, Pezeshkian’s three-to-four-week timeline compresses. The $139 million per day in oil revenue does not decline gradually. It collapses to whatever Jask can push through at 0.3 million bpd — roughly $28 million per day at current prices, assuming the crude reaches a buyer. The fiscal gap is approximately $111 million per day, or $3.3 billion per month. That is the difference between a war economy functioning under extreme strain and one that cannot pay its soldiers.

Saudi Arabia’s interest in this arithmetic is obvious. A faster Iranian economic collapse increases pressure for a ceasefire. But it also increases the probability of an IRGC escalation — the kind Yacoubian describes as “unbridled” — before the collapse is complete. The IRGC’s counter-strike doctrine exists precisely for this scenario: the moment Iran’s economic lifeline is severed, the IRGC’s institutional incentive shifts from attrition to destruction. If Iran’s revenue disappears, the cost of hitting Abqaiq drops to zero — there is nothing left to protect.

Does Saudi Arabia Need the Barrels or the Price?

Saudi Arabia projects a $44 billion budget deficit in 2026, driven by Vision 2030 spending growth (Middle East Insider). At $110 Brent, the kingdom is already generating revenues well above its $80-85 fiscal breakeven. The war has been, in crude financial terms, a windfall. Aramco’s May Official Selling Price for Arab Light to Asia reached a record $19.50 per barrel premium — and still left an estimated $20.50 on the table relative to Bloomberg’s projection.

The pricing restraint was deliberate. Aramco maintained term-contract discipline even as spot prices for Dubai benchmark crude approached $170 per barrel (Platts). The restraint preserves long-term buyer relationships — Asian refiners who accept OSP pricing in April remain contractually locked in for months. If Iranian supply disappears, those buyers have nowhere else to go. Saudi Arabia captures volume, pricing power, and contractual lock-in simultaneously, without needing to announce a production increase.

But there is a second-order consideration that complicates the windfall logic. If Saudi Arabia visibly fills the gap left by Kharg’s destruction — ramping production and redirecting cargoes to Asian refiners who were buying Iranian crude — the ceasefire incentive structure collapses. The 45-day ceasefire framework currently under negotiation, thin as it is, depends in part on the promise that oil market normalization follows a deal. If Saudi Arabia has already normalized the market by replacing Iranian barrels, Iran’s ceasefire incentive evaporates. Why negotiate the reopening of Kharg if the buyers have already moved to Aramco?

Bilal Y. Saab, associate fellow at Chatham House’s MENA Program, argued that occupation of Kharg could “remove an economic lifeline for the regime — and perhaps lower its chances of survival — and stabilize global energy markets” (CFR). The stabilization and the regime collapse are not sequential. They are competing. If Saudi Arabia stabilizes markets by replacing Iranian crude, it accelerates the regime’s fiscal crisis. If the regime collapses before a ceasefire is reached, the IRGC’s “unbridled escalation” doctrine activates with nothing left to lose.

MBS privately urged Trump to pursue regime change, according to the New York Times, citing people briefed by U.S. officials. Bernard Haykel of Princeton characterized the resulting Trump-MBS dynamic as “constrained not detonated” (Bloomberg). The constraint is economic as much as military. Saudi Arabia benefits from Iran’s weakened state. It does not benefit from the IRGC deciding, in its final days of fiscal solvency, to fire everything it has at Abqaiq.

Goldman Sachs warned that Brent could exceed $147 per barrel if Strait disruptions worsen — but also projected that WTI could fall to the mid-$80s if a ceasefire is announced (Bloomberg/FX Leaders). The spread between those scenarios is roughly $60 per barrel. For Saudi Arabia, producing 10.2 million bpd, that spread represents approximately $612 million per day in revenue variance. The kingdom’s production decision is not just about filling a supply gap. It is a $612 million daily bet on whether the war continues or ends.

The Washington licenses Iranian crude paradox compounds the dilemma. The U.S. General License U allows Indian refiners to import Iranian crude — the first shipments since May 2019 — even as American bombs land on the island from which those cargoes load. Saudi Arabia has watched its share of the Indian market fall from 16 percent to 11 percent as Iranian crude, at a $6-8 premium above Brent, flows to IOC, BPCL, and Nayara Energy. If Kharg is destroyed, that Indian market share reverts to Aramco — but only if Aramco has the volumes to deliver through terminals that are not under Iranian fire.

The strategic position is a closed loop. Saudi Arabia can hold production and wait for the ceasefire, preserving the incentive structure but forfeiting the market share and revenue. Or it can pump, capture the windfall, and accept that every additional barrel flowing through Ras Tanura and Ju’aymah registers in IRGC targeting cells as evidence that the kingdom has chosen a side. The pipeline to Yanbu is full. The Gulf terminals are exposed. The PAC-3 stockpile is depleting. And the IRGC has already demonstrated — at Ras Tanura on March 2 — that it does not wait for formal declarations before it strikes.

Frequently Asked Questions

How long would it take to repair Kharg Island’s oil infrastructure if it were destroyed?

During the Tanker War (1984-1988), Iraq’s sustained bombing campaign rendered Kharg’s facilities “all but destroyed,” according to the U.S. Naval History and Heritage Command. Post-war reconstruction took approximately three to four years before the terminal returned to pre-war throughput of roughly 1.5 million bpd. Modern precision-guided munitions would likely cause more targeted but structurally severe damage to specific terminal systems — the subsea loading arms and pipeline connections are more difficult to repair than storage tanks. Iran’s current economic condition, with government employees unpaid for three months and ATMs running dry, would severely constrain its ability to finance reconstruction at the scale required.

Could China broker continued Iranian oil exports if Kharg is destroyed?

China has already established itself as the de facto operating system for Hormuz transit — brokering the Al Daayen LNG tanker passage on April 6 and maintaining an estimated 8 MTPA in contracted LNG offtake from Qatar’s North Field East, where CNPC and Sinopec hold 5 percent equity. Beijing’s Kunlun Bank processes Iranian oil payments in yuan outside the SWIFT system. However, China’s brokerage capacity is limited to transit facilitation, not physical infrastructure. If Kharg’s loading terminals are destroyed, there is no Chinese mechanism to move crude that cannot reach a functioning jetty. The Jask bypass at 0.3 million bpd is an Iranian infrastructure constraint, not a diplomatic one.

What is the 2019 Abqaiq precedent and why does it matter now?

On September 14, 2019, a coordinated drone and cruise missile attack — attributed to Iran but claimed by Yemen’s Houthis — struck Saudi Aramco’s Abqaiq processing facility and the Khurais oil field, temporarily halving Saudi production capacity and removing approximately 5.7 million bpd from global supply. The attack demonstrated that Abqaiq’s physical vulnerability is not hypothetical: eighteen drones and seven cruise missiles penetrated Saudi air defenses and struck with precision sufficient to damage specific processing trains. The 2026 context is worse. Iran is now launching attacks under its own flag rather than through proxies, the IRGC has explicitly named Gulf oil infrastructure as retaliatory targets, and Saudi Arabia’s PAC-3 interceptor stockpile is estimated at roughly 400 rounds — compared to the several thousand available in 2019.

Would a Saudi production increase violate OPEC+ agreements?

The April 5, 2026, OPEC+ agreement established a collective increase of 206,000 bpd — Saudi Arabia’s share of which is modest. However, OPEC+ agreements have historically included force majeure provisions that allow members to increase production when supply disruptions threaten market stability. The destruction of Kharg Island would constitute the largest single supply disruption since the 2019 Abqaiq attack and would likely trigger emergency consultations. The more relevant constraint is not OPEC+ compliance but the physical bottleneck: Saudi spare capacity must flow through Gulf terminals that the East-West Pipeline to Yanbu cannot accommodate, and those terminals are within IRGC missile range.

Has Saudi Arabia ever publicly addressed the co-belligerence risk?

Riyadh has maintained a formal posture of non-belligerence throughout the conflict, hosting U.S. forces at Prince Sultan Air Base and other facilities while declining to participate in offensive operations against Iran. Saudi Arabia’s Ambassador to the United States, Princess Reema bint Bandar, has described the kingdom’s role as “defensive” — a characterization that becomes more difficult to sustain if Aramco actively replaces Iranian crude in Asian markets during active hostilities. The kingdom’s April 7 closure of the King Fahd Causeway after Iranian ballistic missiles struck the Eastern Province illustrates the tension: Saudi Arabia is absorbing Iranian strikes on its territory while maintaining that it is not a party to the war. Filling the Kharg supply gap would add an economic dimension to a military exposure the kingdom already struggles to define.

The same dynamic played out simultaneously at Jubail Industrial City, where debris from intercepted missiles ignited a fire at SABIC’s petrochemical complex — the same proof-of-concept that the Eastern Province cannot be defended by interception alone. The Jubail fire and its implications for Saudi industrial exposure are detailed here.

The same pattern of striking oil infrastructure through ceasefire windows continued when the Lavan Island refinery attack on April 8 hit Iran’s central Gulf export terminal hours after the halt nominally took effect.