DUBAI — Iran permitted between 15 and 20 vessels to transit the Strait of Hormuz in the first 24 hours after the ceasefire took effect on April 7, according to Fars News Agency and maritime analytics firm Windward — a figure that represents roughly 11 to 14 percent of the pre-war daily average of 138 transits. Oil markets responded as though the strait had fully reopened, with Brent crude falling approximately 15 percent to $92–95 per barrel and WTI dropping 16 percent to $94.47, the largest single-day decline since the 1991 Gulf War, according to Bloomberg commodity data. That partial reopening was upended within hours: explosions at Lavan Island and Sirri Island triggered a fresh Iranian retaliation wave, and the question of who struck the facilities now threatens to collapse the April 10 Islamabad framework before Phase 2 talks begin.

The gap between those two numbers — 15 ships moving through a waterway that carried 138 per day five weeks ago — is the gap between what was announced and what actually happened. Iranian Foreign Minister Abbas Araghchi described “safe passage through the Strait of Hormuz via coordination with Iran’s Armed Forces and with due consideration of technical limitations.” President Trump, on Truth Social, declared “COMPLETE, IMMEDIATE, and SAFE OPENING.” White House Press Secretary Karoline Leavitt framed it as a full reopening. These are not the same agreement, and the oil market priced in only one version of them.

Table of Contents

The 15-Ship Day

Windward, the maritime intelligence platform whose data has been cited by Bloomberg and CNBC throughout the conflict, recorded 20 transits on April 6–7 — 14 outbound and 6 inbound. That was, as Windward noted in data reported by Seatrade Maritime, “the highest number of transits since war started on 28 February but only a seventh of the historic average of 138 per day.” Fars News Agency, the semi-official Iranian wire service, separately reported 15 ships, framing the figure as evidence of Iran granting managed access rather than capitulating to American demands. Five days later, on April 12, the one vessel that continued through the strait as Islamabad talks collapsed — the Mombasa B VLCC — demonstrated how narrowly selective that access had become.

The pre-war baseline, depending on the source, was between 130 and 145 transits per day. Windward put it at 138. UNCTAD’s standing estimate is 145. Eurasia Group tracked 130 per day in February 2026, the final month before hostilities began. By any of those benchmarks, the ceasefire’s first day restored somewhere between a ninth and a seventh of normal traffic. Since March 1, according to Kpler, commodities carriers have made only 293 crossings total — a 94 percent decrease from peacetime levels.

The pattern of who was allowed through tracked a template established weeks earlier. Windward found that nearly all bulk carriers transiting during the war had previously called at Imam Khomeini port — permission was linked to prior commercial relationships with Iran. Iraqi vessels were explicitly exempted. French- and Japanese-owned ships received individual clearances. The ceasefire did not replace this selective system. It expanded its throughput from single digits to low double digits.

What Did Iran Actually Agree To?

The ceasefire text, as described by Araghchi in remarks carried by Al Jazeera on April 7, commits Iran to a two-week window: “For a period of two weeks, safe passage through the Strait of Hormuz will be possible via coordination with Iran’s Armed Forces and with due consideration of technical limitations.” Every clause in that sentence does work. “Coordination with Iran’s Armed Forces” means the IRGC Navy remains the gatekeeper. “Due consideration of technical limitations” provides an open-ended justification for restricting volume. “Two weeks” sets an expiration date — not a permanent reopening.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Trump’s version contained none of these qualifications. “COMPLETE, IMMEDIATE, and SAFE OPENING” implies unrestricted transit beginning at once. Leavitt’s briefing reinforced the framing of full restoration. Both statements were released within hours of each other, and the market — processing them in aggregate — treated the more optimistic reading as operative.

Iran’s Supreme National Security Council, in a separate statement carried by NBC News on April 7, declared that “nearly all war objectives” had been achieved. That victory framing, intended for a domestic audience, creates a political constraint: having told its public the war was won, Tehran now faces pressure not to appear to surrender control of Hormuz unconditionally. The SNSC language suggests Iran views the managed-access model — fees, coordination, military oversight — as the war’s primary institutional achievement, not a temporary measure to be dismantled in two weeks.

The SNSC statement carried a second register that the market did not price: Iran’s ceasefire halt order declared simultaneously that “this does not mean the end of the war” — a designed contradiction that preserves every precondition for resumption within the same document that orders the halt, making the two-week window a reversibility instrument rather than a peace agreement. The gap between Iran’s ceasefire framing and actual strait operations was made operational on April 9, when Iran turned back Cosco-linked tankers at Larak Island: Iran Blocked Chinese Tankers at Hormuz on April 9 — The Ceasefire and the Strait Are Two Separate Negotiations examines how Tehran has explicitly bifurcated the two tracks.

The Fee Protocol and Its Legal Problem

Iran’s Deputy Foreign Minister Kazem Gharibabadi confirmed on April 8 that Tehran is working with Oman to draft a protocol governing transit fees through Hormuz. The fees would vary by vessel type, cargo, and conditions, with Iran’s share directed to post-war reconstruction, according to reports in BusinessToday India and Al-Monitor. Gharibabadi framed the arrangement as “intended to facilitate passage rather than obstruct it.” The protocol had not been finalized as of April 8.

The legal foundation is contested. Iran’s Parliament passed a Hormuz transit fee bill on March 31 — a week before the ceasefire — institutionalizing the mechanism in domestic law, as reported by Seoul Economic Daily. But UNCLOS restricts coastal state charges on transit passages to service-based fees: piloting, tugging, navigational aid. A general toll on vessels exercising transit passage rights has no precedent in the post-1982 maritime legal order. Iran is not a party to UNCLOS, which complicates enforcement in both directions — Tehran is not bound by the convention’s restrictions, but neither can it invoke the convention’s protections.

The Oman channel is itself a development. Muscat’s role as co-drafter of the fee protocol gives the arrangement a veneer of multilateral legitimacy and provides a neutral administrative intermediary. For shipping companies, the practical question is whether paying the fee guarantees safe transit. For insurers, it is whether a paid transit constitutes an acknowledgment of Iranian sovereignty claims that could later be cited against flag-state interests. Neither question has been answered.

What the fee protocol does not resolve is the fundamental geography: both the inbound and outbound shipping lanes through Hormuz run through Omani territorial waters, giving Muscat a structural veto over any enforcement architecture Washington or Tehran designs without its consent.

Did the Market Overshoot?

The numbers suggest it did. Brent’s 13–15 percent single-day decline — from roughly $109 to $92–95 — was the steepest since January 17, 1991, when the coalition air campaign against Iraq began and markets concluded Saddam Hussein’s oil infrastructure would be neutralized within weeks. That analogy is instructive: in 1991, the market was pricing in the destruction of a threat. In April 2026, it priced in the voluntary removal of one. The collapse created an immediate pricing dislocation that has no modern precedent: Aramco’s May OSP, locked in at +$19.50 over Oman/Dubai, now sits roughly $15 above the spot market, leaving every Asian term buyer with a per-barrel incentive to lift minimum contractual volumes and fill the gap with cheaper spot cargoes. The same market assumption embedded in that price — that the blockade is temporary, enforceable, and will be lifted through diplomacy — is scrutinised in “Brent at $96 After a Declared Blockade Is the Price of Disbelief.”

Reid I’Anson, a Kpler analyst, estimated a net market deficit of 6 million barrels per day after accounting for rerouting and bypass capacity. Pre-war Hormuz flow was approximately 15 million barrels per day of crude alone, according to Kpler, and closer to 20 million barrels per day including refined products, per EIA data. Fifteen to twenty ships transiting in a day does not restore 15 million barrels per day. It does not restore 5 million.

Bloomberg columnist Javier Blas flagged the discrepancy directly, noting that “the full opening of the Strait of Hormuz depends on some technical limitations and military coordination” — language he identified as a pricing signal the market may have overshot. Polymarket, the prediction platform, placed the implied probability of normal traffic by May 31 at 64 percent — meaning 36 percent of money in the market was betting that restriction continues through at least seven more weeks.

Iraq’s export collapse illustrates the scale of what remains unreversed. Iraqi crude exports fell from 4 million barrels per day to roughly 900,000 barrels per day during the conflict, according to Kpler. Restoring those flows requires not just an open strait but functional port infrastructure, available tankers, and insurance coverage — none of which snap back in a single trading session. Aramco’s May OSP pricing, set before the ceasefire, already reflected a market paying record premiums for available barrels.

The Bypass Arithmetic

The war forced an accelerated reliance on overland bypass routes that were never designed for this volume or duration. Saudi Arabia’s East-West Pipeline pushed up to 7 million barrels per day through to Yanbu on the Red Sea, of which approximately 5 million barrels per day was export-ready crude. The UAE’s Fujairah pipeline, bypassing Hormuz to the Gulf of Oman, handled roughly 1.5 million barrels per day. Combined export-ready bypass capacity: approximately 6.5 million barrels per day.

Pre-war Hormuz carried 15 to 20 million barrels per day. The gap — 8.5 to 13.5 million barrels per day — cannot be filled by pipeline. ENR analysis described the bypass infrastructure as “sized for a short disruption,” not a multi-month conflict. Even if the ceasefire holds and transit volume scales up, the physical bottleneck is not the strait alone. It is the entire logistics chain between wellhead and destination refinery. On April 8, that calculus worsened further: the IRGC struck a pump station on the East-West Pipeline itself on ceasefire day, directly targeting the bypass corridor that had been carrying Saudi Arabia’s main export load. On April 11, CENTCOM attempted to address the Hormuz side of the equation directly, deploying two destroyers as part of the Hormuz mine-clearance campaign — a mission the IRGC simultaneously denied had occurred.

The Lebanon carve-out embedded in the ceasefire has since triggered a second Hormuz re-closure: within hours of IDF strikes on Lebanon on April 8, Iran halted the two tankers that had briefly transited, returning throughput to zero. The mechanism by which a Lebanese military operation becomes a Saudi revenue crisis — and why Riyadh has no channel to stop it — is examined in Lebanon Is Iran’s Kill Switch on Saudi Arabia’s Oil Recovery. Goldman Sachs cut its Q2 Brent forecast to $90 on April 8 on the assumption of mid-April LNG normalisation through Hormuz — an assumption Day 2 data invalidated within hours.

| Metric | Pre-War (Feb 2026) | During War (March) | Ceasefire Day 1 (April 7) |

|---|---|---|---|

| Daily Hormuz transits | 130–145 (Windward/UNCTAD) | ~6/day (Windward) | 15–20 (Fars/Windward) |

| Crude flow through Hormuz | ~15M bpd (Kpler) | ~1M bpd (est.) | Not yet measurable |

| Brent crude | ~$73/bbl | $109+/bbl | $92–95/bbl |

| Iraqi exports | 4M bpd | ~900K bpd (Kpler) | ~900K bpd (unchanged) |

| Bypass pipeline capacity (Saudi + UAE) | ~6.5M bpd export-ready | ~6.5M bpd (at max) | ~6.5M bpd (at max) |

800 Vessels, 70 Empty Tankers, and a Four-Week Voyage

Even if the strait were to open fully tomorrow, the physical fleet is out of position. Bloomberg reported on April 8 that approximately 800 vessels remain trapped inside the Persian Gulf, with another 400 anchored in the Gulf of Oman. An estimated 3,200 ships carrying 20,000 seafarers have been affected by the conflict’s maritime restrictions since February 28. The restrictions have not deterred all traffic equally: shadow fleet tankers that continued transiting while commercial shipping stalled — including the Russian-flagged VLCC Arhimeda, which sailed toward Kharg Island on April 9-10 — illustrate how Moscow’s commercial oil interests operated inside the same enforcement perimeter its UNSC veto helped construct.

The scale of the physical blockage has been put to numbers by the highest-ranking commercial official in the Gulf: ADNOC CEO Sultan Al Jaber’s count of 230 loaded tankers waiting outside Hormuz as of April 9, drawn from ADNOC’s own logistics data, represents the loaded-cargo subset of the wider fleet that Bloomberg tallied as 800 vessels trapped inside the Gulf. On the demand side, the tanker shortage is acute. Henning Gloystein, managing director for energy, industry, and resources at Eurasia Group, told CBS News that “there are currently at least 70 large empty crude oil tankers anchored off the eastern coast of Singapore and Malaysia,” representing “at least 100 million barrels of crude oil” in stranded carrying capacity. The voyage time from Southeast Asia to the Persian Gulf is approximately four weeks. Even if those VLCCs departed on April 8, the earliest they could load at Ras Tanura or Basra would be early May.

Oil markets will remain undersupplied, even with some increase in shipping through the Strait of Hormuz.

— Henning Gloystein, Managing Director, Energy, Industry and Resources, Eurasia Group

The ceasefire created a psychological event — the perception that Hormuz was reopening — and the market traded on perception. The physical event — tankers loading, transiting, and delivering crude — operates on a timeline measured in weeks, not hours. The gas-lane opening that allowed Qatari LNG carriers through in early April took days to produce even a single confirmed transit. Scaling to 138 ships per day, across a waterway still under IRGC naval coordination, is a different order of problem.

Background

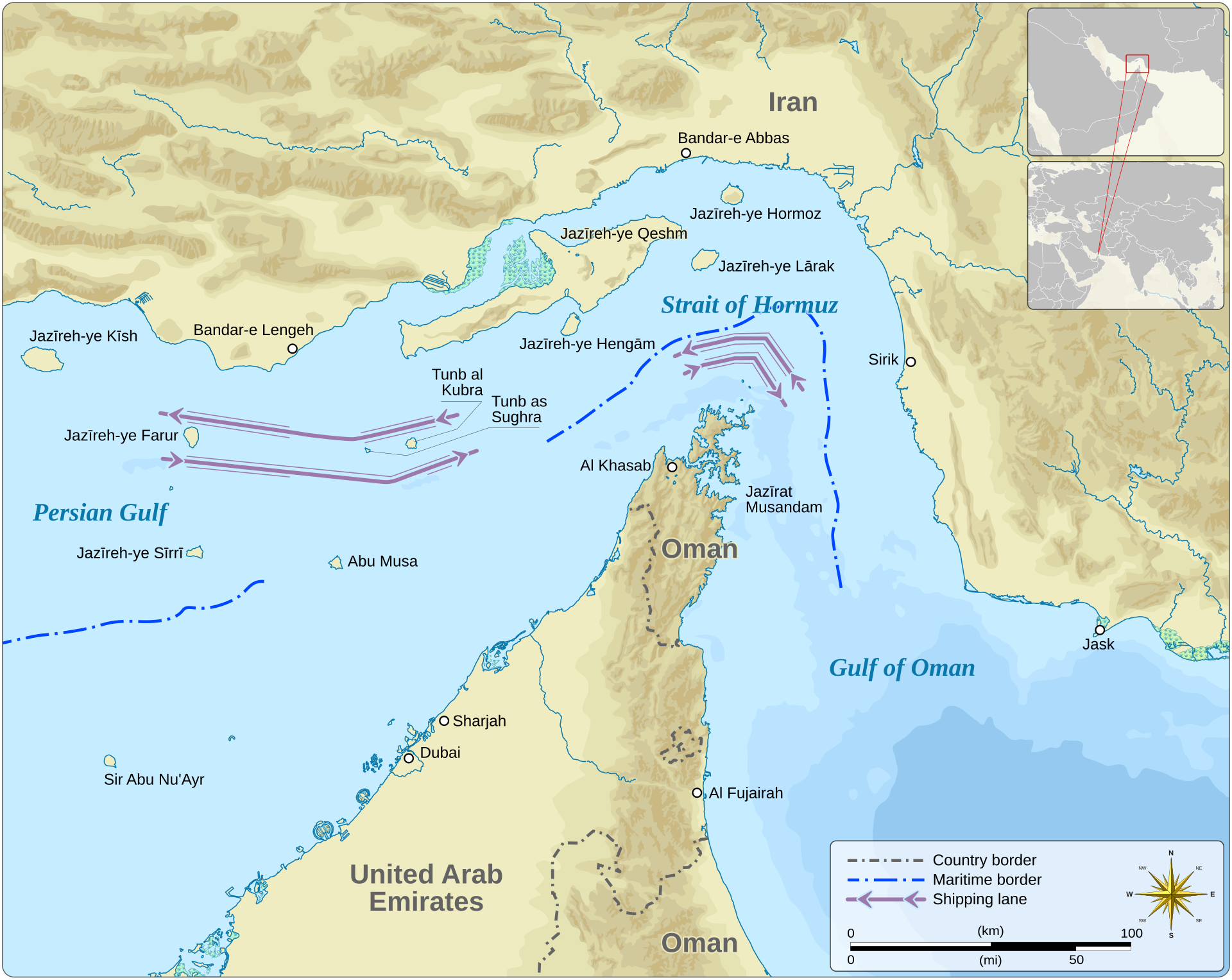

The Strait of Hormuz, 21 nautical miles wide at its narrowest point, carried approximately 20 percent of global petroleum consumption before Iran began restricting transit on February 28, 2026. The restrictions followed the outbreak of hostilities between Iran and a US-led coalition, with Saudi Arabia hosting American military assets — including fighter wings, Patriot batteries, and THAAD systems — at Prince Sultan Air Base, Al Dhafra, and other Gulf installations.

Iran’s approach to Hormuz during the conflict was not a conventional naval blockade. Tehran operated a selective franchise model — granting transit to vessels with prior Iranian commercial relationships, exempting Iraqi shipping, and negotiating individual clearances with specific flag states. The IRGC Navy maintained physical control of the transit lanes while Iran’s diplomatic apparatus managed exceptions. The ceasefire has formalized this arrangement rather than dismantled it. The practical consequence — that Saudi Arabia now faces two incompatible operating systems simultaneously controlling the strait it depends on — is examined in detail in the dual-track Hormuz architecture.

The Tanker War of 1984–88, the most commonly cited precedent, saw the US escort reflagged Kuwaiti tankers through the strait under Operation Earnest Will beginning in 1987. Even at that conflict’s most restricted point, no managed-access fee regime existed. Iran’s current model — legislating fees, coordinating with Oman, and maintaining military oversight of transit — has no modern precedent in international maritime practice. The model was confirmed operational on April 9, when the MSG tanker completed the first confirmed post-ceasefire Hormuz transit under IRGC permission — $2 million paid, boarding party accepted, the Guards declaring it a permanent new phase of Strait management.

Frequently Asked Questions

How long does the ceasefire transit window last?

Araghchi’s statement specifies a two-week period for “safe passage via coordination with Iran’s Armed Forces.” That window began April 7 and would expire around April 21 absent extension or a broader diplomatic agreement. The Witkoff-Araghchi framework discussed before the ceasefire envisioned a 45-day Phase 1 ceasefire with Hormuz status deferred to Phase 2 negotiations, but the final ceasefire text appears to have compressed the initial transit commitment to 14 days. What happens at expiry has not been publicly addressed by either side.

What would the Hormuz transit fees cost per vessel?

The fee structure has not been finalized. Gharibabadi indicated it would vary by vessel type, cargo, and conditions, with Oman administering the protocol. Earlier reporting during the conflict referenced figures in the range of $2 million per transit for large tankers, with payments routed through Kunlun Bank or USDT on the Tron blockchain to circumvent sanctions infrastructure, as reported by CryptoBriefing. Whether the ceasefire-era protocol maintains those mechanisms or establishes a more conventional payment channel is unknown as of April 8.

Could the US Navy escort commercial vessels through without Iranian coordination?

Approximately 20,000 US troops are deployed in the theater, according to the Soufan Center, and the USS Eisenhower carrier strike group has operated in the Arabian Sea throughout the conflict. Escorted convoy operations are technically feasible — the 1987–88 Earnest Will precedent demonstrated the model. But escorting vessels through a strait where Iran has laid mines, positioned fast-attack craft, and established shore-based anti-ship missile batteries would risk restarting hostilities hours into a ceasefire. The IRGC mine chart published on April 9 made the physical reality explicit: the standard Traffic Separation Scheme is marked as a “danger zone,” with the Larak corridor as the only authorized alternative, running entirely within Iranian territorial waters. The Biden-era and now Trump-era posture has been to avoid direct naval confrontation in the strait itself, concentrating instead on air operations against Iranian military infrastructure on the mainland.

What share of global LNG supply transits Hormuz?

Qatar, the world’s largest LNG exporter, ships virtually all of its output through the strait. Qatar’s liquefaction capacity is approximately 77 million tonnes per annum, with the North Field expansion adding further volume. During the war, the first confirmed laden LNG transit was the Al Daayen on April 6, moving at 8.8 knots toward China under what appeared to be a Beijing-intermediated arrangement. JKM (Japan Korea Marker) spot LNG prices reached $19.83–19.97/MMBtu during the conflict. Qatar’s LNG exports represent roughly 25 percent of global seaborne LNG trade, and the 12.8 million tonnes per annum that went offline during the conflict caused downstream shortages in Japan, South Korea, and Pakistan.

What is the insurance situation for vessels transiting under the ceasefire?

War-risk insurance premiums for Hormuz transit surged above 5 percent of hull value during the conflict, up from a peacetime rate below 0.05 percent, according to Lloyd’s market sources cited by the Financial Times. For a VLCC valued at $120 million, that translates to a single-transit premium exceeding $6 million — on top of whatever fee Iran charges. Whether underwriters will reduce war-risk rates in response to the ceasefire, or maintain them until sustained safe transit is demonstrated over weeks, will directly affect the economics of resuming Gulf exports. Several P&I clubs have issued advisories recommending members wait for further clarity before entering the strait. Iran’s Point 3 in its 10-point peace proposal — which Trump called “workable” on April 7 — would make this selective-transit system permanent in international law, giving Tehran sovereign authority over the strait it has functionally controlled since March 3: the implications for Saudi Arabia’s security architecture are analyzed here. The premium calculation shifted further on April 8, when a US-Iran bilateral toll regime proposed by Trump introduced the prospect of institutionalized fees replacing war-risk surcharges — a transition with no precedent in modern maritime insurance. The throughput problem has no near-term military solution either: NATO’s written mine-clearance plans, requested within days by Washington, cannot be executed because the alliance has zero mine countermeasure ships in the theater. On the diplomatic side, the throughput problem remained live on April 9, when Netanyahu authorized direct Israel-Lebanon negotiations at the State Department — a move Iran immediately deemed insufficient to reopen the strait, since Tehran’s condition is a halt to strikes, not a commencement of talks. The market dislocation this throughput gap has created is quantified in Brent Drops 10% While Zero Tankers Clear the Strait, which shows that futures markets have priced in a Hormuz deal that physical tanker data does not support. The throughput calculus is further complicated by the Houthi threat to the alternative Red Sea route: 90 percent of crude loaded at Yanbu exits via Bab al-Mandab, which the Islamabad Accord left entirely unaddressed. The full strategic analysis of why the bypass corridor cannot survive a Houthi Red Sea closure — and what that means for Saudi export arithmetic — is in Saudi Arabia Solved the Wrong Chokepoint: The Yanbu Bypass Ends in Houthi Territory. That calculus shifted further on April 10, when Iran’s declaration of a new Hormuz transit stage introduced destroy-on-sight orders alongside the diplomatic framework — widening the gap between futures pricing and physical throughput. That gap has a physical dimension no ceasefire text can bridge: U.S. officials say Iran cannot locate all of the mines it deployed in the strait, meaning mine clearance cannot begin even if Iran cooperates.

The supply-side dimension of that throughput gap sharpened on April 11, when Aramco’s first wartime grade allocation confirmed that reduced Hormuz transits have already reshaped what Saudi Arabia can physically offer Asian term buyers.

The pricing structure underlying that offer is fractured: by April 10, the gap between dated Brent and ICE front-month futures had widened to $35 — a super-contango that quantifies in dollar terms how little the physical market believes in the ceasefire timeline that futures pricing assumes.

The throughput deficit at Hormuz has since been compounded by a new US enforcement posture: CENTCOM’s April 16 declaration of a “regardless of location” seizure doctrine extends interdiction authority to any suspected Iran-linked vessel anywhere — including the Red Sea corridor carrying Saudi Arabia’s bypass exports through Yanbu. How that doctrine threatens the one export route Saudi Arabia built specifically to survive Hormuz disruption is analyzed here.