DHAHRAN — Brent crude above $100 per barrel was supposed to be Saudi Arabia’s windfall. Instead it is the price tag on a trap the Kingdom helped construct and cannot escape. President Trump’s admission on Fox News on April 12 that American gasoline prices may remain “around the same, or maybe a little bit higher” through November has done something no prior US president attempted: publicly anchored a blockade’s domestic cost to an electoral calendar seven months away. For Saudi Arabia, the implications are immediate and punishing — a Yanbu export ceiling of 4.4 to 5.0 million barrels per day means 1.1 to 2.3 million barrels of daily production cannot reach a tanker, at a Brent price still $8 to $16 below the Kingdom’s PIF-inclusive fiscal breakeven of $108 to $111.

The duration question has been answered, at least from Washington. The blockade runs through November. Iran has already absorbed its revenue compression. Saudi Arabia has not begun to acknowledge publicly what the arithmetic makes plain: at current export volumes and current prices, the Kingdom is losing money relative to where it stood before a single missile was fired.

Table of Contents

- Trump’s November Anchor

- What Is Saudi Arabia’s Actual Export Ceiling Through Yanbu?

- The Revenue Arithmetic That No One in Riyadh Will Say Aloud

- Why Has No US President Done This Before?

- Iran’s Counter-Framing and the Gas-Price Weapon

- The May OSP Problem and the June Repricing Cliff

- How Long Can Saudi Arabia’s Air Defenses Hold?

- Three Calendars, No Alignment

- The Reserve Burn Rate

- FAQ

Trump’s November Anchor

The exchange on “Sunday Morning Futures” lasted fewer than thirty seconds. Maria Bartiromo asked whether gasoline prices would fall by the November midterms. Trump’s answer — “It could be, or the same, or maybe a little bit higher, but it should be around the same” — was delivered with the flatness of a man who had already decided the political cost was acceptable. The national average stood at $4.15 per gallon, up 39 percent from $2.98 before the war began on February 28, according to AAA data from the same day.

Within hours, Trump announced via Truth Social that the US Navy would “immediately” blockade ships entering or leaving the Strait of Hormuz. CENTCOM’s subsequent clarification narrowed the target set to Iranian ports and toll-paying vessels rather than all Hormuz traffic, but the signal was structural: the United States was escalating the blockade’s enforcement, not winding it down. Senator Ron Johnson, a Republican ally, told reporters that achieving US aims “could take a long time.” Senator Mark Warner asked the question Riyadh would not: “How is that going to ever bring down gas prices?” The CENTCOM naval blockade announced April 12 formally took effect at 10 AM ET on April 13, deploying two carrier strike groups and 18 warships to enforce a cordon around Iranian ports while explicitly preserving Hormuz transit for non-Iranian-bound vessels.

The answer, from Trump’s posture, is that it won’t — and that he has decided this is survivable through November. Every US president since the 1973 Arab oil embargo has treated sustained gasoline-price increases as a political emergency requiring immediate visible action. Trump has treated this one as a line item.

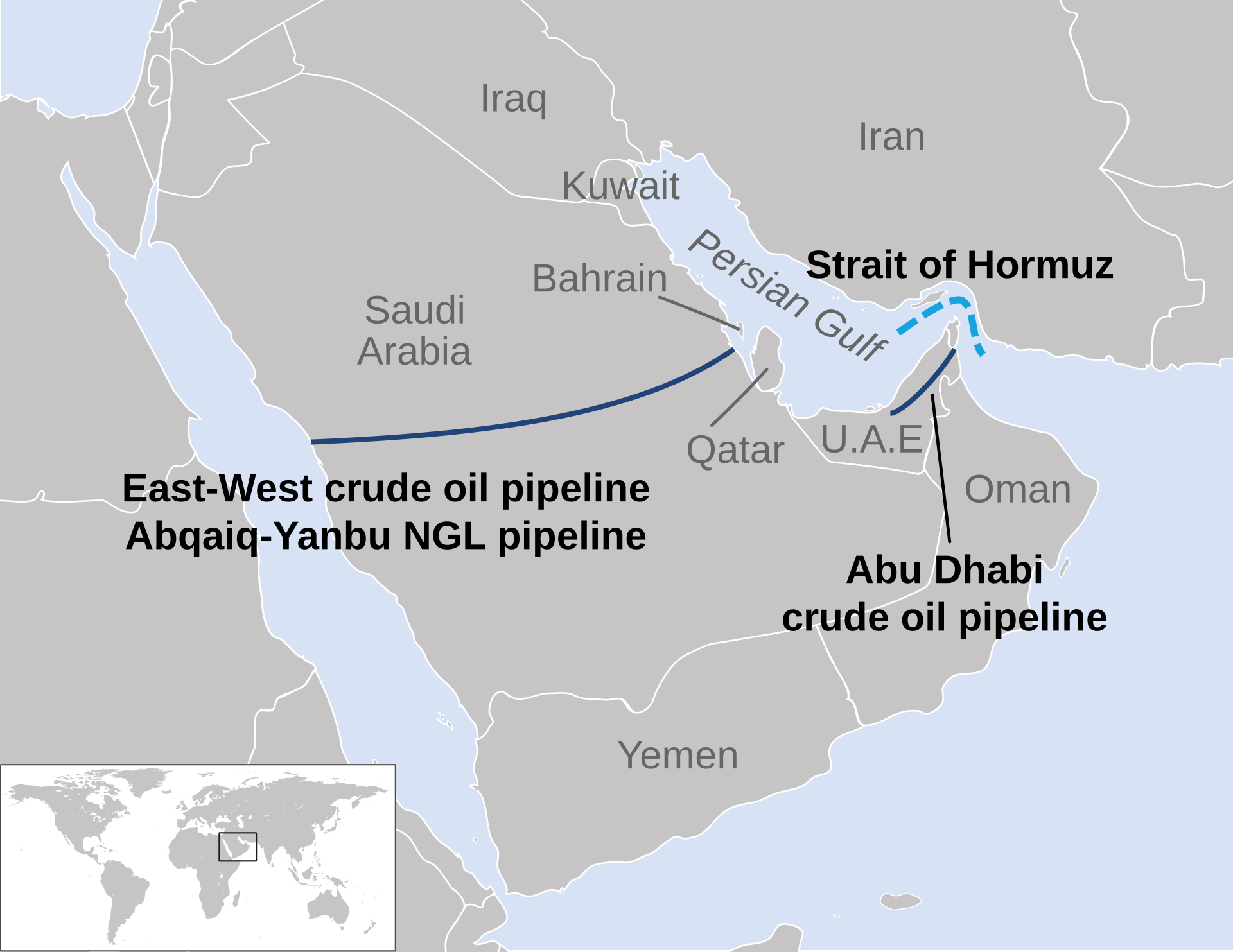

What Is Saudi Arabia’s Actual Export Ceiling Through Yanbu?

The East-West pipeline was restored to its full 7 million barrel-per-day pumping capacity by April 12, after repairs to the IRGC-damaged Manifa and Khurais facilities (each accounting for roughly 300,000 bpd of lost output). Bloomberg, Al Jazeera, and The National all confirmed the restoration. Riyadh framed this as a return to full capability — a narrative the pipeline’s operational history supports on throughput alone.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The throughput figure is not the export figure. Approximately 2 million barrels per day of what the pipeline moves feeds Saudi domestic refineries — SAMREF at Yanbu, plus allocations to Jeddah and the western grid. What arrives at Yanbu’s loading berths for export is 4.4 to 5.0 million bpd in crude, plus an additional 700,000 to 900,000 bpd in refined products. Kayrros, the satellite-based cargo tracking firm, estimated the crude loading ceiling at 4.4 million bpd. Fortune, citing an industry source with direct knowledge of terminal operations, put the figure closer to 5 million bpd in crude alone.

Monica Malik, chief economist at Abu Dhabi Commercial Bank, captured the gap between Riyadh’s framing and the market’s observation: “Certainly if they can export 7 million bpd, the fiscal position is set to strengthen. But so far the data that’s available on tanker movements from last week is much lower than 7 million.” Kpler analyst Reid I’Anson modeled the maximum at 4 to 4.5 million bpd. Saudi crude exports to Asia — the Kingdom’s dominant market — fell 38.6 percent in a single month, from 7.108 million bpd in February to 4.355 million bpd in March.

Pre-war Saudi crude exports through Hormuz ran at 6.0 to 6.7 million bpd. The structural gap between what the Kingdom was exporting and what Yanbu can load ranges from 1.0 to 2.3 million bpd. That gap does not close with pipeline repairs. It closes with Hormuz reopening — an event Trump has just placed, at minimum, seven months away.

The Revenue Arithmetic That No One in Riyadh Will Say Aloud

The instinct — shared by several analysts in the first week of the war — was that a Brent price above $100 would rescue Saudi Arabia’s budget. AGBI published a piece in March headlined to that effect. The arithmetic seemed simple: lower volume, higher price, roughly a wash or better. Tim Callen, former IMF mission chief to Saudi Arabia, framed the tension correctly at the time: “The budget depends on both oil prices and oil production. As exports are hit by shipping difficulties, this will impact production. Ultimately the price up versus production down will determine the impact.”

The price went up. The volume went down further. And the breakeven moved.

| Scenario | Volume (bpd) | Brent ($/bbl) | Daily Revenue | vs. Pre-War Baseline |

|---|---|---|---|---|

| Pre-war (Feb 2026) | 6.7M | $75 | ~$502M | Baseline |

| Yanbu ceiling (high est.) | 5.0M | $100 | ~$500M | Roughly flat |

| Yanbu ceiling (Kayrros est.) | 4.4M | $100 | ~$440M | -12.4% |

| Yanbu ceiling at current Brent | 4.4M | $95 | ~$418M | -16.7% |

| Goldman worst case Q3 | 4.4M | $120 | ~$528M | +5.2% |

The table reveals the trap. Saudi Arabia reaches pre-war revenue parity only if Brent exceeds $114 per barrel at the Kayrros volume estimate, or if Yanbu loads consistently at 5.0 million bpd and Brent holds above $100. Goldman Sachs’s worst-case scenario — Brent at $120 in Q3 — barely clears the pre-war baseline at constrained volumes, and that scenario also implies Hormuz is still shut, which means the volume constraint persists. The price that rescues the budget requires the condition that prevents the budget from being rescued.

Saudi Arabia’s fiscal breakeven tells the rest of the story. The IMF’s central-government-only estimate is $87 per barrel. Bloomberg Economics, incorporating the Public Investment Fund’s spending commitments, puts the consolidated figure at $108 to $111. Brent at $95 to $100 — where it sat on April 13 — remains $8 to $16 below that consolidated threshold. The price Saudi Arabia cannot collect is also, at current levels, the price that would not have been sufficient anyway.

Beyond the revenue shortfall at current Brent levels, Aramco’s own pricing formula may prevent it from capturing the Asia supply vacuum the blockade created — a structural problem compounding the fiscal trap this article examines.

Why Has No US President Done This Before?

Richard Nixon understood gasoline as a gut-level political issue well before the 1973 embargo made it one. He imposed price controls in August 1971 — partly to manage inflation ahead of the 1972 election — and the controls backfired catastrophically when the Arab embargo hit in October 1973. The artificially suppressed price created shortages that manifested as gas lines, and Nixon spent his final months in office managing both Watergate and a fuel crisis his own policy had worsened.

Jimmy Carter inherited the wreckage. His “moral equivalent of war” speech in April 1977 asked Americans to accept energy sacrifice as shared national duty. Two years later, the Iranian Revolution sent crude from $15.85 to $39.50 per barrel, gasoline lines returned, and Carter’s presidency was finished. The 1979 oil shock was not the only cause of his 1980 loss to Reagan, but it was the one voters felt every time they filled a tank.

Reagan’s tolerance during Operation Earnest Will — the 1987-88 tanker escort mission in the Persian Gulf — is the closest precedent to Trump’s current posture, but the comparison collapses on scale. Oil spiked to $22.75 per barrel in July 1987. The US national average gasoline price was approximately $0.90 per gallon. Reagan was absorbing a Gulf war premium on cheap oil. Trump is absorbing a 39 percent consumer price increase on gasoline that was already expensive by historical standards. Adjusted for inflation, Reagan-era motorists paid roughly $2.20 in 2026 dollars; Trump-era motorists are paying $4.15 and have been told to expect it through the fall.

The structural novelty of Trump’s April 12 statement is that he did not announce measures to reduce the price. He did not invoke the Strategic Petroleum Reserve. He did not call on OPEC+ for additional output. He acknowledged the price, characterized it as roughly stable through November, and moved on to the blockade announcement. The political bet is legible: the blockade’s purpose — pressure on Iran — is popular enough to absorb the blockade’s cost.

Iran’s Counter-Framing and the Gas-Price Weapon

Mohammad Bagher Ghalibaf, speaker of Iran’s parliament and former IRGC Aerospace Force commander, responded within hours of Trump’s blockade announcement. “Enjoy the current pump figures,” he said. “Soon you’ll be nostalgic for $4 to $5 gas.” The framing was deliberate: Iran argues that the blockade hurts American consumers more than Iran’s already-compressed export revenue, and Ghalibaf — who understands military logistics from his IRGC career — is positioning Iran as the party with less to lose from duration.

The Iranian parliament passed a maritime fee bill on March 31, creating a legal architecture for Hormuz transit charges that gives Tehran a parallel revenue stream from the blockade itself. The $2 million per VLCC toll, processed through Kunlun Bank and USDT on the Tron network, partially compensates for crude export losses by monetizing the chokepoint directly. Iran earned approximately $139 million per day in oil revenue in March 2026 despite the war — a figure that reflects resilience through higher realized prices on reduced volumes. The same arithmetic applies to Saudi Arabia, with worse results: Iran’s cost structure is lower and its export infrastructure less damaged than its rhetoric suggests.

The asymmetry is duration tolerance. Iran’s economy was already under maximum-pressure sanctions before the war. Its population has absorbed economic pain for decades. The US, per Trump’s own framing, can absorb $4.15 gasoline through November. Saudi Arabia’s tolerance has not been tested publicly — and the Kingdom has not made a single statement acknowledging that its export revenue is structurally below pre-war levels at a price that appears, on its face, to be a bonanza.

The May OSP Problem and the June Repricing Cliff

Aramco set its May Official Selling Price for Arab Light crude to Asia at a premium of $19.50 per barrel above the Oman/Dubai benchmark — the highest differential in the company’s modern pricing history. The decision was made on approximately April 6, when Brent was trading at $109 per barrel. By April 13, Brent had recalibrated to the $95 to $100 range, placing the May OSP $11 to $19 above prevailing spot prices.

Asian refiners — Indian, Chinese, South Korean, Japanese — have three options: accept the premium and process crude at a loss, reduce nominations on term contracts (triggering penalties and risking future allocation cuts), or seek alternative supply from sources not subject to Hormuz constraints. Several have already moved toward bilateral deals that circumvent the OSP entirely, a development that threatens Aramco’s benchmark pricing power in ways that may outlast the war itself.

The June OSP decision falls around May 5. If Brent remains in the $95 to $100 range, Aramco must either cut the premium sharply — acknowledging that the war price is not the collection price — or hold the premium and watch nominations collapse. Either outcome reduces actual revenue below the headline figures that analysts are using to project Saudi fiscal health.

How Long Can Saudi Arabia’s Air Defenses Hold?

Saudi Arabia’s PAC-3 Missile Segment Enhanced interceptor stockpile stands at approximately 400 rounds, down from roughly 2,800 before the war — an 86 percent depletion in forty-four days of conflict. At pre-ceasefire consumption rates, the remaining stockpile would be exhausted in six to seven days of sustained Iranian bombardment.

Lockheed Martin’s Camden, Arkansas facility produces PAC-3 MSE rounds at a rate of approximately 620 per year. The planned production ramp to 2,000 rounds annually will not be reached until 2030. Poland refused a Patriot battery transfer request on March 31. The $16.5 billion emergency arms package approved by Congress went to the UAE, Kuwait, and Jordan — not Saudi Arabia.

The connection between air defense stocks and oil revenue is direct. Every major Saudi oil facility within range of Iranian ballistic missiles — Ras Tanura, Abqaiq, Jubail, Khurais — sits in the Eastern Province, on the wrong side of the pipeline from Yanbu. If the ceasefire collapses and Iran resumes strikes, Saudi Arabia lacks the interceptor depth to protect those facilities for more than a week. The Sadara petrochemical complex already entered force majeure in late March after SABIC’s Jubail facilities took missile debris damage. The pipeline to Yanbu does not help if the production feeding it is offline.

Three Calendars, No Alignment

Saudi strategic planning is now subject to three clocks that do not synchronize. The ceasefire expires April 22 — nine days away — with no extension mechanism identified by the Soufan Center or any public mediator. Hajj arrivals begin April 18 — five days away — with Pakistan’s 119,000 pilgrims among the first wave and Indonesia’s 221,000 departing on April 22 itself. The US midterm elections fall in November — seven months away — and Trump’s Fox News statement has now made that date the implicit horizon for the blockade’s political sustainability.

Saudi Arabia’s fiscal incentive is early resolution. Every day the Hormuz blockade continues, the Kingdom loses $60 to $84 million in uncollectable revenue — the gap between what it could export through the Strait and what Yanbu can load, multiplied by Brent. Over seven months, that compounds to $12.6 to $17.6 billion in foregone revenue, a figure roughly equal to the entire PIF write-down on suspended megaprojects.

But Saudi Arabia committed no naval assets to the Hormuz coalition. The UAE sent corvettes, missile boats, and patrol vessels. Riyadh’s silence on the US blockade announcement was total — no endorsement, no condemnation, no statement of any kind. The Kingdom that loses the most from a seven-month blockade has positioned itself as the party with the least influence over its duration. The 1973 parallel is instructive in reverse: King Faisal wielded the oil embargo as a weapon because Saudi Arabia controlled both the tap and the price. In 2026, MBS controls neither — the tap is constrained by terminal infrastructure, and the price is set by a blockade Washington declared and Tehran provoked.

| Calendar | Date | Days Away | Saudi Exposure |

|---|---|---|---|

| Ceasefire expiry | April 22 | 9 | PAC-3 stockpile insufficient for resumed conflict |

| Hajj first arrivals | April 18 | 5 | Custodian title, 2M+ pilgrims in theater |

| US midterms | November 2026 | ~200 | $12.6-17.6B foregone revenue if blockade holds |

| June OSP decision | ~May 5 | 22 | Benchmark pricing credibility |

| Sadara debt grace period | June 15 | 63 | $3.7B potential default |

The Reserve Burn Rate

Saudi Arabia entered 2026 with $438.5 billion in foreign exchange reserves, according to AGBI. Goldman Sachs projects the war-adjusted 2026 fiscal deficit at $80 to $90 billion — roughly double the official $44 billion estimate and equivalent to 6.6 percent of GDP against the government’s stated 3.3 percent. Deutsche Bank, Emirates NBD, and ADCB cluster their estimates at 5.0 to 5.3 percent of GDP, suggesting Goldman’s figure represents the upper bound but that even conservative projections are materially above Riyadh’s published budget assumptions.

At $65 to $80 billion per year in deficit spending, the Kingdom consumes $5 to $7 billion monthly from reserves — a rate that, if sustained through November, would draw down $35 to $49 billion from the cushion by year’s end on the deficit alone. The $438.5 billion cushion sounds large until measured against both the deficit and the PIF’s capital commitments — $30 billion in construction spending (down from $71 billion pre-war), plus the NVIDIA, AMD, AWS, and other technology partnerships totaling $23 billion that form the core of the Humain AI initiative. The PIF cannot simultaneously fund Vision 2030’s digital pivot and backstop a fiscal deficit that is consuming reserves at twice the budgeted rate.

JP Morgan’s projection of $120 per barrel Brent if full Hormuz recovery is delayed to July — with a $150 overshoot risk if the strait stays shut into mid-May — would help on the price side. But $120 Brent at 4.4 million bpd yields $528 million per day, only 5 percent above the pre-war baseline. And a $150 spike, if it materialized, would likely trigger demand destruction and a coordinated IEA strategic reserve release that collapses the price within weeks, as happened in 2022. Goldman’s Daan Struyven and team acknowledged as much: “The situation remains fluid. We continue to see the risks to our price forecast as skewed to the upside.” Skewed to the upside for price. Not for Saudi fiscal health.

FAQ

Why can’t Saudi Arabia simply increase Yanbu’s export capacity?

Yanbu’s loading berths are a fixed-infrastructure constraint. The terminal’s jetties, storage tanks, and VLCC loading arms have a hard throughput ceiling — Kayrros estimates 4.4 million bpd; industry sources place it closer to 5 million. Expanding that capacity would require new berth construction measured in years, not months. The Saudis studied a Red Sea terminal expansion in 2019 and shelved it when Hormuz risk appeared to recede — a decision that now sits as one of the more consequential infrastructure choices of the last decade.

Could the US Strategic Petroleum Reserve offset the blockade’s price impact?

The SPR held approximately 395 million barrels as of early April 2026 — already at its lowest level since 1983 after the Biden administration’s 2022 drawdown of 180 million barrels. A sustained release of 1 million bpd (matching the 2022 rate) would deplete the reserve to emergency-minimum levels within roughly twelve months and has historically provided only temporary price relief. Trump’s decision not to invoke the SPR on April 12 is itself a data point: the administration has calculated that the political cost of $4.15 gasoline is lower than the strategic cost of further depleting the reserve during an active Gulf conflict.

What happens to Saudi Arabia’s Asian market share if the blockade continues through November?

Saudi crude’s share of Indian imports had already fallen from 16 percent to 11 percent before the war, partly due to the India-Iran OFAC General License U waiver. A seven-month blockade would accelerate substitution: Iraqi crude via the Turkish Mediterranean terminal at Ceyhan, Kazakh CPC blend through the Black Sea, US shale exports from the Gulf of Mexico, and Brazilian pre-salt cargoes. Each month of disrupted term-contract fulfillment erodes the buyer relationships that Aramco has spent decades building, and the OSP premium structure — designed for a seller’s market with reliable delivery — becomes a liability when delivery is constrained to a single Red Sea terminal.

Is Iran actually hurt by the blockade?

Less than the headline numbers suggest. Iran’s pre-war budget was built on sanctions-era assumptions — fiscal breakeven around $70 to $75 per barrel at much lower export volumes — giving it considerably more cushion than Saudi Arabia’s $108 to $111 consolidated breakeven at structurally constrained exports. Tehran’s maritime fee architecture on Hormuz transit (the $2 million per VLCC toll) also converts the chokepoint from a cost into a revenue source, a mechanism Saudi Arabia has no equivalent of. The asymmetry is that Iran planned for austerity and Saudi Arabia planned for abundance.

What does Goldman Sachs project for Brent if Hormuz reopens gradually?

Goldman’s base case, assuming immediate gradual traffic recovery, projects Brent at $82 in Q3 and $80 in Q4 2026. That scenario — the optimistic one — places Brent below Saudi Arabia’s IMF breakeven of $87 and well below the Bloomberg PIF-inclusive breakeven of $108 to $111. In other words, the only Brent path that resolves the Yanbu export constraint also eliminates the price premium that made the constraint appear tolerable on paper. Saudi Arabia’s fiscal math does not have a winning quadrant in Goldman’s scenario matrix.