RIYADH — When OPEC+ ministers convene on April 5, Saudi Arabia will sit at the table as three countries at once — the cartel’s swing producer, a war participant burning through fiscal reserves, and a state whose largest refinery took an Iranian drone 48 hours ago. Each identity demands a different production decision, and the three decisions are mutually exclusive. The result is the most structurally paradoxical quota meeting in OPEC’s 65-year history, not because the variables are complex but because every available lever pulls against the others.

Brent crude spot trades at $141.36 per barrel. Futures for December delivery sit at $112.42. That $28.94 gap between physical cargo and paper contract is a market-priced confession: traders believe this crisis ends, but the oil moving on water today costs $29 more than the promise of oil six months from now. Riyadh must decide tomorrow whether to pump more into a chokepoint that Iran has sealed, hold steady while its own infrastructure absorbs fire, or abandon production discipline entirely to satisfy Washington 24 hours before Donald Trump’s deadline threatening total destruction of Iran’s energy sector.

Table of Contents

- The Three Identities That Cannot Share a Production Target

- What Is OPEC+ Actually Deciding on April 5?

- The Volume Trap: Why More Barrels Cannot Leave the Ground

- Can Yanbu Replace Hormuz as Saudi Arabia’s Export Route?

- The Fiscal Geometry of a War Budget at Wartime Prices

- Why Does Russia Have a Conflict of Interest Inside OPEC+?

- 1973, 1990, 2022 — and What April 5 Breaks

- The Three Postures and Their Contradictions

- What Happens the Day After the Meeting?

The Three Identities That Cannot Share a Production Target

Saudi Arabia occupies three roles inside the Gulf war economy, and each one demands a production posture that sabotages the other two. As swing producer, Riyadh’s institutional reflex is to manage price — cut when demand softens, add barrels when markets overheat. As war participant, the kingdom needs maximum revenue to fund a defense budget that climbed to $74.76 billion in 2026, up from $72.5 billion the year before, while the Public Investment Fund’s capital expenditure pushes the consolidated fiscal breakeven toward $94 per barrel according to Bloomberg Economics. As a target — an oil state whose export infrastructure is under live Iranian drone and missile attack — Saudi Arabia cannot guarantee delivery of whatever volume it pledges.

The swing producer wants price stability. The war participant wants maximum revenue. The target state cannot promise supply — and these three imperatives do not overlap at any production number. A cut satisfies the price manager but starves the war chest. An increase satisfies the revenue need and Washington’s political pressure but means nothing if the barrels cannot physically reach tankers. A freeze acknowledges reality but satisfies nobody, least of all the IEA’s Fatih Birol, who warned on April 1 that “the next month, April, will be much worse than March.”

No OPEC meeting has ever convened under all three conditions simultaneously. Members have faced war before, infrastructure attacks before, chokepoint closures before. But the structural novelty of April 5 is that a single member state — the cartel’s most powerful — is experiencing all three at once, and the mathematics of the situation generate a decision space with no equilibrium point.

What Is OPEC+ Actually Deciding on April 5?

OPEC+ is deciding whether to proceed with a previously agreed 206,000 barrel-per-day production increase, hold it, reverse it, or abandon the entire framework of voluntary output cuts in favor of maximum output. The decision carries a military dimension because it arrives one day before Trump’s April 6 deadline threatening Iran over the Strait of Hormuz closure.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The March 1 communique from the group’s last meeting already approved the 206,000 bpd addition for April, with the explicit caveat that the increase could be paused or reversed. Emily Ashford, head of energy research at Standard Chartered, wrote on April 2 that the meeting “could result in abandonment of voluntary output cuts and compensation cuts” — a scenario in which members would pursue “increased output where possible.” The phrase “where possible” carries the weight of the entire crisis, because what is possible depends on whether tankers can leave port and whether refineries remain standing.

Standard Chartered estimates that 7.4 to 8.2 million barrels per day of global supply are currently offline. The IEA has already executed a 400-million-barrel strategic reserve release, the largest in the institution’s 50-year history, and it has not arrested prices. Birol’s assessment is blunt: “The biggest problem today is the lack of jet fuel and diesel.” OPEC+ is not managing a price cycle. It is managing a physical shortage compounded by war.

The Volume Trap: Why More Barrels Cannot Leave the Ground

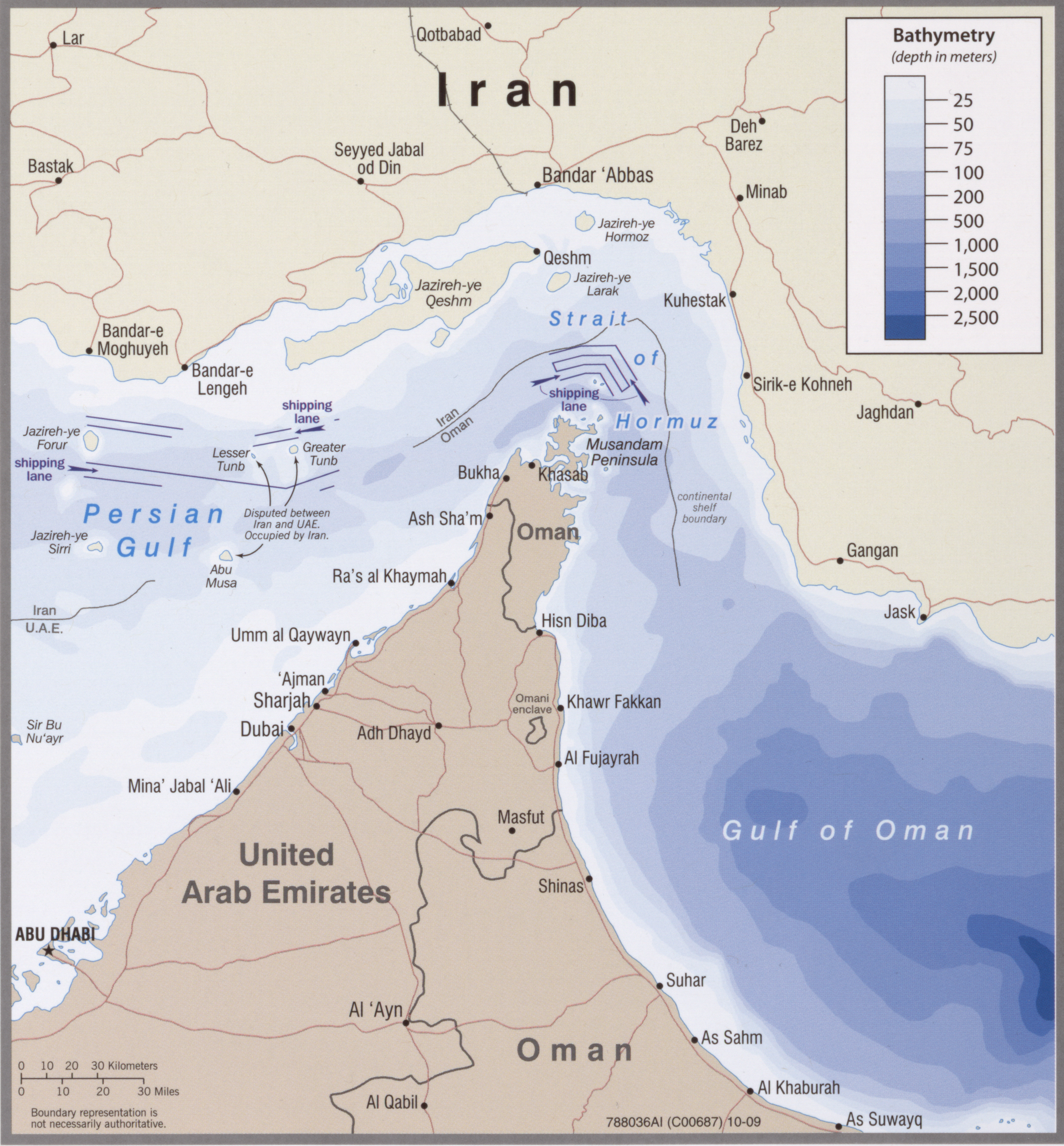

Saudi Arabia exported 6.99 million barrels per day in January 2026, according to the Joint Organisations Data Initiative, the last clean month before the Hormuz closure. Riyadh’s maximum sustained capacity sits at approximately 12.2 million bpd. OPEC+ spare capacity across the group is around 3.5 million bpd, concentrated in Saudi Arabia and the UAE. On paper, the kingdom has room to add barrels. On the map, it does not.

The IRGC closed the Strait of Hormuz on March 27 to vessels sailing to or from US, Israeli, and allied ports, removing roughly 20 million bpd — about 20 percent of global supply — from the market in a single naval action. Mojtaba Khamenei declared on April 1 that the “leverage of blocking the Strait of Hormuz must still be used.” Iran exports almost no oil through Hormuz, making the closure asymmetrically costless for Tehran: it sacrifices nothing while Saudi Arabia, Iraq, Kuwait, and the UAE lose their primary export artery.

The arithmetic of the trap is unforgiving. If the Yanbu terminal on the Red Sea can deliver 2 to 3 million bpd — Kate Dourian of the Arab Gulf States Institute puts the current ceiling at “maybe two million barrels out a day, maybe three” — then Saudi Arabia faces an export suppression of 4 to 5 million bpd against its January baseline. At $141.36 per barrel, that is approximately $566 million per day in foregone revenue, or roughly $17 billion per month. Any OPEC+ production increase that Saudi Arabia votes for but cannot physically deliver is not an oil decision. It is a diplomatic telegram.

Can Yanbu Replace Hormuz as Saudi Arabia’s Export Route?

Yanbu cannot replace Hormuz in the short term. The East-West Pipeline connecting Saudi Arabia’s eastern oil fields to its Red Sea coast at Yanbu has a theoretical capacity of 7 million barrels per day, but actual throughput is constrained by pumping and downstream infrastructure well below that ceiling.

Actual throughput surged from 770,000 bpd in January-February to 2.9 million bpd by late March, according to Al Jazeera. Dourian’s assessment of 2 to 3 million bpd as a realistic ceiling reflects both pumping constraints and the condition of downstream infrastructure. The SAMREF refinery at Yanbu — a 400,000 bpd joint venture between Aramco and ExxonMobil — was struck by an Iranian drone on April 3. George Voloshin, an independent energy analyst, noted that exposed fixed infrastructure is inherently vulnerable to a determined adversary. The Red Sea bypass that Saudi Arabia has treated as its insurance policy against Hormuz disruption is now itself under fire, and every barrel Riyadh pumps westward travels through approximately 1,200 kilometers of exposed desert pipeline before reaching a terminal that Tehran has already demonstrated it can reach.

The East-West Pipeline was built in the 1980s precisely for this scenario — an Iranian threat to Hormuz. But the pipeline was designed to operate as a temporary bypass during a naval standoff, not as the kingdom’s primary export route under sustained aerial attack. Tim Callen, former IMF Mission Chief to Saudi Arabia, put the fiscal consequence directly: “The budget depends on both oil prices and oil production. As exports are hit by shipping difficulties, this will impact production.” Monica Malik, chief economist at Abu Dhabi Commercial Bank, framed the uncertainty more sharply: “If they can export 7 million bpd, the fiscal position is set to strengthen. But data on tanker movements from last week is much lower.”

The Fiscal Geometry of a War Budget at Wartime Prices

Saudi Arabia entered 2026 with SAR 1.78 trillion — approximately $475 billion — in SAMA foreign exchange reserves, a six-year high. The pre-war IMF fiscal breakeven price was $81.20 per barrel. Bloomberg Economics, factoring in PIF spending, puts the consolidated breakeven at $94 per barrel. Add full PIF capital expenditure and the number climbs to $111. Brent spot at $141 suggests comfort. But the breakeven calculation assumes barrels actually leave the country, and they are not leaving at pre-war volumes.

Rachel Ziemba of Ziemba Insights distilled the bind: “Volumes are down and disrupted and other spending needs are likely up.” Defense spending at $74.76 billion already absorbs a commanding share of the budget, and the first two months of the year saw $12 billion in Defense Security Cooperation Agency arms purchases — a procurement pace consistent with a state at war, not a state monitoring one. Goldman Sachs models a wartime GDP contraction of 3.0 percent if fighting persists through April, against a pre-war IMF forecast of 4.5 percent growth — a 7.5 percentage point swing that would be the largest single-year revision in the kingdom’s modern economic history.

The macro-fiscal strain has now found its first measurable transmission into Saudi Arabia’s private sector. The war’s first measurable impact on Vision 2030’s diversification targets arrived with the March 2026 non-oil PMI reading of 48.8 — the first contraction in 66 months — as Hormuz-dependent supply chains registered their worst disruption indicators since the COVID-19 lockdowns. The three levers OPEC+ ministers could not reconcile in Vienna are now producing downstream consequences in Saudi Arabia’s own private sector economy.

The $475 billion in reserves provides approximately 27 months of cover at the current rate of export suppression, before accounting for accelerated military expenditure. That buffer looks comfortable in peacetime. In a war where rising prices and falling volumes cancel each other out, it functions less as a cushion and more as a clock. Every month the Hormuz closure persists, the fiscal arithmetic tightens regardless of where Brent trades.

| Metric | Pre-War Baseline | Current Wartime | Source |

|---|---|---|---|

| IMF fiscal breakeven (oil price) | $81.20/bbl | $81.20/bbl | IMF |

| Bloomberg consolidated breakeven (incl. PIF) | $94/bbl | $94/bbl | Bloomberg Economics |

| Full PIF capex breakeven | $111/bbl | $111/bbl | Bloomberg Economics |

| Brent spot price | $74–82/bbl (2025 range) | $141.36/bbl | CNBC, April 2 |

| Crude exports | 6.99M bpd | ~2–3M bpd (est.) | JODI / AGSI |

| SAMA FX reserves | $475B | $475B (Feb 2026) | SAMA / Arab News |

| Defense budget | $72.5B (2025) | $74.76B (2026) | ResearchAndMarkets |

| GDP forecast | +4.5% | -3.0% (if war persists) | IMF / Goldman Sachs |

Why Does Russia Have a Conflict of Interest Inside OPEC+?

Russia’s conflict of interest inside OPEC+ is structural and unresolvable by communique. The Hormuz closure has doubled Urals crude from $45 to $90 per barrel, generating an estimated $8.5 billion per month in additional revenues for Moscow. Russia exports none of its oil through Hormuz — every day the strait stays closed, Moscow gains while Riyadh bleeds.

Sergey Vakulenko of the Carnegie Russia Eurasia Center stated it without diplomatic padding: “The Kremlin stands to gain much from war in the Persian Gulf.” The financial windfall is direct and requires no policy change from Moscow — it accrues automatically as long as Gulf supply stays offline and global prices stay elevated. Russia’s Arctic LNG-2 project, which struggled for buyers when Asian spot LNG was cheap, is back in play as Asian importers scramble for non-Gulf hydrocarbon sources. The war has accomplished for Russian energy export diversification what years of sanctions diplomacy could not.

Inside the OPEC+ framework, this creates a structural misalignment that no communique language can resolve. Saudi Arabia needs Hormuz reopened to export its oil. Russia benefits from Hormuz staying closed. Both sit at the same table voting on production targets. When Ashford describes a scenario of “increased output where possible,” the words land differently in Riyadh and Moscow — for Saudi Arabia, “where possible” means the Red Sea bottleneck determines everything; for Russia, it means every pipeline to Europe and Asia is open and running at capacity. Any production increase approved on April 5 will mechanically benefit Russia more than Saudi Arabia, because Russia can deliver its barrels and Saudi Arabia largely cannot.

1973, 1990, 2022 — and What April 5 Breaks

Three historical precedents frame what Saudi Arabia has done when oil production and geopolitical pressure collided, and all three break down against the specifics of April 5. In 1973, Ahmed Zaki Yamani, then oil minister, recalled King Faisal’s instinct: “The king still wanted to give America a chance to stay out of the fighting. So we agreed to cut back production by just 5 percent per month.” The Saudi default was conservative — start small, escalate incrementally, keep the diplomatic channel open. But in 1973, Saudi infrastructure was not under direct attack, and the embargo was a weapon Riyadh chose to deploy, not a constraint imposed by an adversary.

In 1990, after Iraq invaded Kuwait, Saudi Arabia ramped production from 5.4 to roughly 7.7 million bpd within months, filling the gap left by Kuwaiti and Iraqi barrels. That response is the template most analysts reach for when modeling what Riyadh will do under supply disruption. But the 1990 analogy collapses at a foundational point: Saudi Arabia was not the military target. The US-led coalition provided direct security guarantees for Saudi oil infrastructure before Riyadh opened the taps. In 2026, Saudi oil infrastructure is absorbing strikes, and the coalition partner asking for more production — Washington — has not secured the kingdom’s export routes.

The 2022 precedent cuts differently. When the US pressured OPEC+ to increase production during the Russia-Ukraine war to bring down fuel prices, Saudi Arabia did the opposite — cutting 2 million bpd and absorbing the White House’s accusation that “OPEC+ is aligning with Russia.” Riyadh chose revenue over alliance management. But in 2022, Saudi Arabia was not a co-belligerent alongside the US in a shooting war, and the production cut was a voluntary choice, not a forced outcome of infrastructure damage. April 5 sits outside all three templates because the kingdom cannot fully execute any production posture it announces — the physical constraints imposed by Hormuz and by Iranian strikes on Yanbu override whatever number appears in the communique.

| Crisis | Saudi Decision | Saudi Infrastructure Under Attack? | Chokepoint Closed? | Saudi a Belligerent? |

|---|---|---|---|---|

| 1973 Arab-Israeli War | 5% monthly cut (embargo) | No | No | No (weapon deployed voluntarily) |

| 1990 Gulf War (Iraq invades Kuwait) | Ramped 5.4 to 7.7M bpd | No (US security guarantee) | No | Yes (coalition member) |

| 2022 Russia-Ukraine War | Cut 2M bpd against US pressure | No | No | No |

| 2026 Iran-US Gulf War (April 5) | TBD | Yes (SAMREF struck April 3) | Yes (Hormuz closed March 27) | Yes (active target, US coalition) |

The Three Postures and Their Contradictions

The first option — holding production steady or cutting — would signal that Riyadh takes the demand destruction and war-risk premium seriously. The argument for a hold is that the war has already imposed a de facto production cut through infrastructure damage and export route closure; formalizing what physics has already dictated carries a certain logic. But a hold or cut sends a dangerous signal to Tehran: it tells Iran that the high prices generated by Hormuz’s closure are tolerable to the Gulf producers, reducing any economic incentive for Iran to negotiate the strait’s reopening. It also leaves Trump empty-handed the day before his deadline, when Washington has already failed diplomatically to reopen the waterway.

The second option — proceeding with the pre-agreed 206,000 bpd increase — is what markets currently price as the consensus outcome. It signals institutional continuity and a measured confidence that supply conditions will stabilize. The problem is arithmetic: if Yanbu can move 2 to 3 million bpd and the eastern terminals are blockaded, an additional 206,000 bpd exists only on the spreadsheet. Nikolay Kozhanov of Qatar University described the broader credibility risk when he called the Hormuz shock “an existential challenge” to GCC states’ reliability as suppliers. A production increase that cannot be delivered does not challenge that assessment — it confirms it.

The third option — Ashford’s scenario of abandoning compensation cuts entirely and maximizing output “where possible” — is the most politically charged because it converts the OPEC+ quota system from a price-management tool into a supply-guarantee signal aimed at consuming nations and, specifically, at the White House before April 6. Saudi Arabia would be saying: we will pump everything we can, as fast as we can, through whatever infrastructure still functions. The gesture would resonate in Washington. But it would not change the physical flow of oil through the Red Sea, and it would expose the gap between Saudi Arabia’s 12.2 million bpd capacity and the 2 to 3 million bpd it can actually get to market — a gap that, once officially acknowledged in a communique, cannot be unseen by traders, insurers, or adversaries calculating the cost of further strikes on Yanbu.

What Happens the Day After the Meeting?

Whatever OPEC+ decides on April 5 becomes immediately subordinate to what happens on April 6, when Trump’s deadline for “total destruction of Iran’s energy sector” either materializes as military action against Iranian oil infrastructure or dissolves into another round of maximum-pressure rhetoric with no kinetic follow-through.

If Trump strikes Iranian oil infrastructure, the OPEC+ decision is moot — global supply loses whatever Iran still exports through non-Hormuz routes, and the market reprices around a two-front infrastructure war. If Trump does not strike, the OPEC+ communique becomes the market’s primary signal, and traders will parse whether the production number reflects genuine physical capacity or political performance for a Washington audience.

The deeper structural question is whether OPEC+ as an institution can function when its most powerful member cannot guarantee delivery of its own quota. The cartel’s architecture assumes sovereign control over production — that a government which promises barrels can deliver them. Saudi Arabia’s maximum sustained capacity of 12.2 million bpd is an engineering fact. Its ability to export those barrels is now a military question, determined by Iran’s posture at Hormuz and the IRGC’s drone and missile inventory. Production policy has become inseparable from force protection, and OPEC+ has no institutional mechanism for that convergence.

“Pipelines and pumping stations are static, high-value targets.”

— George Voloshin, independent energy analyst, Al Jazeera

The April 5 meeting will produce a number. The number will appear in a communique. Ministers will speak about market stability and responsible supply management. None of that will change the three facts that make this meeting structurally unlike any before it: the swing producer is under fire, the chokepoint is closed, and the cartel’s second-largest non-Gulf member is profiting from the crisis the cartel was designed to manage. Saudi Arabia holds every lever in the OPEC+ apparatus and cannot pull any of them without making its own position worse. That same paralysis extends into the political domain: an analysis of the kingdom’s options as the April 6 deadline approaches maps four decision branches, none of them clean.

Frequently Asked Questions

How much oil does Saudi Arabia need to export daily to cover its wartime budget?

At the Bloomberg Economics consolidated breakeven of $94 per barrel and current Brent spot of $141.36, Saudi Arabia would need to export approximately 4.6 million bpd to cover budget obligations without drawing on reserves. That figure is still above Dourian’s 2-to-3-million-bpd estimate of current Yanbu throughput capacity. The math only works if Hormuz reopens or Yanbu capacity expands beyond current constraints, neither of which Saudi Arabia controls unilaterally.

Has OPEC ever held a meeting where a member’s export infrastructure was under active military attack?

OPEC meetings have taken place during wars involving member states — Iraq attended meetings during the Iran-Iraq War (1980-1988), and Libya maintained nominal OPEC membership during the 2011 NATO intervention — but no meeting has convened where the cartel’s swing producer simultaneously faced export infrastructure strikes, primary chokepoint closure, and belligerent status. Iraq’s production was disrupted during the 1980s, but Iraq was not the cartel’s price-setting member. The April 5 meeting is structurally unprecedented because the member under attack is the one whose production decisions set the floor and ceiling for global markets.

What is Russia’s current oil export capacity through non-Hormuz routes?

Russia exports its crude and refined products entirely through non-Hormuz infrastructure: the Druzhba pipeline to Europe, the Eastern Siberia-Pacific Ocean pipeline to China and Asian markets, Baltic Sea terminals at Primorsk and Ust-Luga, and Black Sea ports including Novorossiysk. None of these routes are affected by the Hormuz closure, which is why Russian Urals crude has doubled from $45 to approximately $90 per barrel — Moscow captures the global price increase without suffering any of the export disruption hitting Gulf producers. Carnegie estimates this generates $8.5 billion per month in additional revenues, a windfall that gives Russia zero incentive to pressure Iran toward reopening the strait.

Could Saudi Arabia bypass both Hormuz and Yanbu using alternative export routes?

Saudi Arabia has limited alternatives beyond the East-West Pipeline to Yanbu. The kingdom’s only other cross-country pipeline infrastructure is the decommissioned Trans-Arabian Pipeline (Tapline), which once carried oil to Lebanon and has been non-operational since 1990. Aramco operates a network of internal pipelines connecting fields to processing facilities, but all eastern terminal exports — Ras Tanura, Ju’aymah, Ras al-Khair — require passage through the Persian Gulf and thus through or near the Hormuz chokepoint. The Red Sea coast, specifically Yanbu and the smaller Rabigh terminal, represents the only currently viable non-Gulf export option, making its security a single point of failure for Saudi oil revenue during the Hormuz closure.

What happens to OPEC+ quotas if member states physically cannot produce their allocated volumes?

The OPEC+ framework includes a “compensation mechanism” under which members that overproduce relative to their quota in one period must cut in subsequent periods to compensate. The inverse — underproduction due to force majeure — has no formal mechanism. During the Libyan civil war, OPEC exempted Libya from quotas entirely. The 2026 crisis is different because underproduction is not confined to a minor member but affects the swing producer and potentially Iraq, Kuwait, and the UAE simultaneously. If multiple members cannot produce to quota because of Hormuz and infrastructure attacks, the quota system becomes a fiction — numbers on paper disconnected from physical reality. The April 5 communique may be the first to implicitly acknowledge this gap.

The oil market paradox the April 5 meeting could not resolve has now collided with the April 6 deadline. The analysis of Saudi Arabia’s exposure at the April 6 deadline details how the WTI-Brent inversion and the toll law debate intersect with each of Trump’s three remaining action paths. Trump subsequently shelved his April 6 ultimatum — the third postponement of the Hormuz deadline — after Iran acknowledged the US message via Pakistan and a downed WSO was recovered; the full account is at Trump Shelves Hormuz Ultimatum for Third Time.