DHAHRAN — Sadara Chemical Company’s $3.7 billion guaranteed senior debt grace period expires Monday, June 15 — roughly 41 hours from this writing. As of Friday evening, neither Saudi Aramco, which guarantees $2.405 billion of that debt at its 65 percent ownership stake, nor Dow Inc., which guarantees the remaining $1.295 billion at 35 percent, has filed a material event notice with the U.S. Securities and Exchange Commission, the Saudi Exchange (Tadawul), or any securities regulator. All 26 of Sadara’s manufacturing units at Jubail Industrial City have been offline since March 31, producing zero revenue for eleven consecutive weeks, and the joint venture has posted net losses every year since 2022.

The regulatory silence from both guarantors is not an oversight. It is a structural feature of the 2021 debt restructuring agreement, of SEC disclosure rules that draw a sharp line between a grace period expiry and a “triggering event,” and of a lending syndicate composed almost entirely of institutions with reasons never to force the issue. The entire $3.7 billion exposure can approach its contractual cliff and pass through it without generating a single new line in either guarantor’s regulatory filings — as long as the 28 banks in the syndicate cooperate.

Table of Contents

- What Does SEC Form 8-K Require When a Guarantee Expires?

- What Would Force Aramco to Disclose on Tadawul?

- Who Are Sadara’s Lenders and Why Won’t They Call?

- What Did Dow Tell Its Investors About June 15?

- Aramco’s Q1 Report Said Nothing About Monday

- Five Years of Losses Under a Guarantee Nobody Has Discussed

- How Was the 2021 Restructuring Designed to Avoid This Filing?

- Frequently Asked Questions

What Does SEC Form 8-K Require When a Guarantee Expires?

Under SEC Form 8-K Items 2.03 and 2.04, a pre-existing guarantee does not require re-filing when a grace period expires. The disclosure clock starts only when a “triggering event” occurs — an event of default or acceleration under the agreement’s own terms. Grace period expiry alone does not qualify.

The practical effect is that Dow can sit on a guarantee obligation worth more than its entire Q1 2026 net income, approaching its contractual activation date, without filing a single new document — so long as the lending syndicate does not formally declare an event of default. The regulation was written to prevent disclosure overload: companies should not have to re-file on every contractual milestone of an existing obligation. But in Sadara’s case, it means a guarantee attached to a venture generating zero revenue for eleven weeks can approach expiry while the SEC’s own rules treat the countdown as a non-event.

Aramco is dually listed in New York and on Tadawul, but the SEC side applies the same logic. The guarantee was disclosed when it was created in March 2021. Until lenders act on it, no new filing is owed. The Cooley analysis of the 2004 SEC Form 8-K final rules confirms this bright line: passage of time through a contractual milestone is not equivalent to a new direct financial obligation and does not require reporting under Item 2.03.

The word “triggering” is doing an enormous amount of legal work in this structure. A fair value adjustment to an existing liability — such as the charge Dow recorded on its Sadara guarantee in Q1 2026 — is not a triggering event under the 8-K rules. Dow absorbed that charge, noted it in its earnings release, and moved on without filing a dedicated 8-K for the Sadara guarantee.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The SEC’s own Form 8-K rules draw a sharp line. Item 2.03 — Creation of a Direct Financial Obligation — applies when a new obligation is created or when a company enters into an off-balance-sheet arrangement. Item 2.04 — Triggering Events That Accelerate or Increase a Direct Financial Obligation — applies when something happens under an existing agreement that changes the company’s exposure. A grace period ticking down to zero, with no formal lender action, is neither of these — in regulatory terms, a clock running out in an empty room: audible to anyone watching, invisible to anyone reading the filings.

What Would Force Aramco to Disclose on Tadawul?

Saudi Exchange listing rules require immediate disclosure of material events that could affect share price. But Aramco’s Sadara guarantee, already disclosed as a contingent liability in audited financials, sits in a regulatory gray zone — it requires a fresh filing only when the contingency crystallizes into a formal lender demand.

Aramco’s Q1 2026 interim report, published May 11, included net income of SR 122 billion ($32.5 billion) and free cash flow of $18.6 billion. It contained no forward-looking commentary on the June 15 Sadara deadline and no updated contingent liability note specific to the approaching guarantee trigger. The number exists in the footnotes of Aramco’s audited annual financials — the guarantee was disclosed when it was created — but the approaching expiry is treated, under Tadawul rules, identically to how the SEC treats it: as a scheduled milestone of an existing obligation, not a new material event requiring fresh filing.

The Capital Market Authority (CMA) regulations governing Tadawul-listed companies do contain broad provisions requiring disclosure of “developments not in the normal course of the company’s activities.” The argument available to Aramco’s counsel is direct: a grace period expiry under a disclosed guarantee is not a development — it is the scheduled unfolding of a known contractual term, fully disclosed when the restructuring was announced in March 2021. The development, if it comes, would be a lender demand. No demand has been made.

There is a second reason for the silence, and it has nothing to do with regulation. Aramco’s quarterly dividend already exceeds its quarterly operating cash generation, and Saudi Arabia’s Q1 fiscal deficit was the largest on record. The Arab Gulf States Institute warned that “any reduction in Aramco’s dividend will have implications for the government budget and PIF, requiring either new sources of revenue, spending adjustments, or increased borrowing.”

A CMA filing drawing attention to a multi-billion-dollar contingent liability approaching crystallization would land in the worst possible fiscal context. The disclosure rules do not require it, and the financial arithmetic explains why Aramco has no interest in volunteering one.

Who Are Sadara’s Lenders and Why Won’t They Call?

Sadara’s original $12.5 billion financing was underwritten by a 28-bank syndicate dominated by Saudi state banks, Gulf sovereign institutions, and government export credit agencies. These lenders face political, commercial, and relational incentives that make a formal default call — and the disclosure cascade it would trigger — functionally impossible.

The syndicate that closed the deal in June 2013 reads less like a lending group and more like a roll call of institutions whose governments have reasons to avoid forcing a petrochemical default in the Eastern Province. It includes Saudi Arabia’s own Public Investment Fund, which provided a $1.3 billion direct loan, and APICORP, the multilateral development bank of OPEC member states. Ten Saudi national banks — Alinma, Arab National, Bank Al-Jazira, Bank Albilad, Banque Saudi Fransi, National Commercial Bank, Riyad Bank, Samba Financial Group, Saudi Hollandi Bank, and Saudi Investment Bank — fill out the domestic side, and their regulatory relationships with the Saudi central bank make a vote against Aramco’s preferred outcome structurally improbable.

Five Gulf sovereign banks — Abu Dhabi Commercial Bank, National Bank of Abu Dhabi, Gulf International Bank, Qatar National Bank, and National Bank of Kuwait — represent governments managing their own geopolitical exposure to Aramco, to Saudi crude supply, and to the war. The twelve international commercial banks — Barclays, BNP Paribas, BTMU, Citi, Crédit Agricole, Deutsche Bank, Goldman Sachs, HSBC, JP Morgan, Mizuho, SMBC, and Standard Chartered — carry relationship considerations that extend far beyond one petrochemical joint venture. These banks underwrite Aramco bond issuances, advise on sovereign deal flow, and manage Saudi institutional accounts worth multiples of the Sadara debt in question.

The government export credit agencies add a final layer of political constraint. The U.S. Export-Import Bank’s $4.975 billion direct loan was the largest in Ex-Im history when signed. UK Export Finance guaranteed $700 million, and Coface (France), Euler Hermes (Germany), and Korean agencies Kexim and K-Sure provided additional ECA tranches. Every one of these agencies would need to coordinate with its respective government before taking any action that could trigger a Sadara default — an outcome that would ripple through Jubail, Aramco’s balance sheet, Saudi fiscal accounts, and the broader Gulf petrochemical industry.

The syndicate has already shown what it does when faced with a Sadara problem: it extends. In 2021, the original maturity of 2029 became 2038. The $10 billion in shareholder completion guarantees were released and replaced with $3.7 billion in sponsor guarantees.

The grace period was set at five years. That period expires Monday, and the lending group’s composition was designed — from the first closing in 2013, reinforced in the 2021 restructuring — to guarantee a single outcome: extension.

What Did Dow Tell Its Investors About June 15?

Dow recorded a $292 million pretax charge in Q1 2026 for the change in fair value of its Sadara guarantee liability and suspended all equity loss recognition in the joint venture. CEO James Fitterling promised a restructuring update “midyear” without naming the June 15 deadline. The analyst who asked the question did not press for the date.

The charge appeared in Dow’s Q1 earnings release under an accounting category that most retail investors would need an interpreter to parse: “Loss due to change in fair value of the estimated liability associated with the Company’s guarantee of Sadara’s project financing debt.” Twenty-four words to describe a $292 million hit. The net income impact after tax was $227 million, and the earnings-per-share drag was $0.31 — material by any standard, disclosed by the letter of the rule, and functionally buried by the density of the language.

What Fitterling said on the Q1 earnings call, held April 23, was more telling for what it left out. When asked about Sadara by Fermium Research analyst Frank Mitsch, Fitterling responded: “One of the things I will continue to do as Karen takes over the CEO role is finish up these negotiations with Saudi Aramco on the restructuring of Sadara and trying to address some of the challenges that we have faced there.” He then added: “I will have more of an update for you midyear when we come back for earnings then.”

The word “midyear” was carrying careful weight in that sentence. The June 15 grace period deadline fell seven and a half weeks from the day he spoke — well within what he was describing as “midyear.” Fitterling did not name the date, did not name the grace period, and framed the entire situation as ongoing “negotiations” with a promise to report back at Q2 earnings. Mitsch did not follow up on the specific deadline, and no other analyst on the call asked about June 15 by name.

Buried deeper in Dow’s Q1 disclosures was a second revelation: the company had suspended Sadara equity loss recognition entirely, in accordance with GAAP. Dow’s cumulative equity losses in Sadara had reached $1.4 billion, matching the total value of all obligations and commitments — the threshold at which accounting rules permit a company to stop recognizing further losses through the income statement. Dow crossed that line in Q1 2026 and stopped booking losses.

But it did not stop owing money. Fitterling confirmed that Dow retains approximately $100 million per year in cash commitments to Sadara through 2038 — twelve years of ongoing exposure on a venture producing nothing.

The $292 million charge, the suspended equity recognition, and the “midyear” deflection exist in the public record for anyone determined to piece them together. But no dedicated 8-K was filed on the guarantee, and no supplemental disclosure flagged the approaching deadline. The guarantee approaches expiry having generated exactly the volume of disclosure that the SEC requires — and almost no awareness among the investors who bear the exposure.

Aramco’s Q1 Report Said Nothing About Monday

Saudi Aramco’s Q1 2026 interim report contained no forward-looking commentary on the June 15 grace period expiry, no updated contingent liability note for the guarantee, and no discussion of Sadara’s operational shutdown. Aramco’s $2.405 billion portion of the guarantee represents roughly 13 percent of the company’s Q1 free cash flow — approaching its contractual trigger date during a period of zero revenue from the underlying venture — and it was not mentioned.

The omission takes its shape against Aramco’s own financial stress. The company’s quarterly base dividend of $21.89 billion exceeded Q1 free cash flow of $18.6 billion by more than $3 billion — a coverage ratio of 0.85x that marked the first time since the pandemic that Aramco was borrowing to sustain its payout. A guarantee call, if it materialized, would represent a direct claim on Aramco’s cash at a moment when the Kingdom’s budget depends on every dollar of that cash arriving as scheduled.

Saudi Arabia’s Q1 fiscal deficit of SAR 125.7 billion ($33.5 billion) was the largest on record, driven by a 26 percent year-over-year increase in military spending and a 170 percent surge in subsidies. The Public Investment Fund’s cash reserves had fallen to $15 billion — a six-year low — against $16 billion in outstanding commitments to NEOM alone. Brent crude at $86-89 sits $20-25 per barrel below Saudi Arabia’s fiscal breakeven of $108-111, and every component of the fiscal equation is running in the wrong direction.

In this context, disclosing a guarantee crystallization would carry consequences far beyond the balance sheet. It would signal to the market that Aramco is absorbing losses from a joint venture that has not turned a profit in four years and has not produced a unit of output since March — at a moment when Hormuz transit disruption has already compressed Saudi revenues and the Iran deal collapse offers no near-term resolution. The CMA rules do not require the filing, and the political context makes volunteering one unthinkable.

Sadara’s own disclosures have been equally sparse. The company filed with Tadawul on March 31 that “the shutdown was successfully completed in accordance with Sadara’s high safety standards” and added in an April update that it “is expected to have an impact on the financial results for 2026.” Neither filing mentioned the guarantee, the grace period, or the June 15 date. The word “debt” did not appear.

Five Years of Losses Under a Guarantee Nobody Has Discussed

Sadara has posted net losses for four consecutive years since 2022, with accumulated losses exceeding 100 percent of share capital by the end of 2025 — a threshold that triggered a mandatory extraordinary general assembly under Article 150 of the Saudi Companies Law. The $3.7 billion guarantee that expires Monday was attached to a company already in severe financial distress before the war shut it down.

| Year | Net Income / (Loss) | Revenue Trend | Key Development |

|---|---|---|---|

| 2021 | SAR 3.1B profit | Recovery | Restructuring completed; includes SAR 1.05B one-time gain |

| 2022 | SAR (1.85B) loss | Decline | First post-restructuring loss year |

| 2023 | SAR (3.5B) loss | −26% YoY | Revenue contraction accelerates |

| 2024 | SAR (4.01B) loss | Continued decline | Accumulated losses exceed share capital |

| 2025 | SAR (5.793B) loss (~$1.54B) | Further decline | Losses exceed 100% of share capital; EGM triggered |

The trajectory was visible long before the IRGC named Jubail Industrial City among “direct and legitimate targets” on March 18, 2026. Sadara’s profitability window lasted exactly one year — 2021 — and even that year’s SAR 3.1 billion profit included a SAR 1.05 billion one-time gain from the restructuring itself. Strip the gain, and the single profitable year shrinks to approximately SAR 2.05 billion. Everything since has been a worsening spiral: losses nearly doubling from 2022 to 2023, exceeding share capital by 2024, and blowing past 100 percent of equity by 2025.

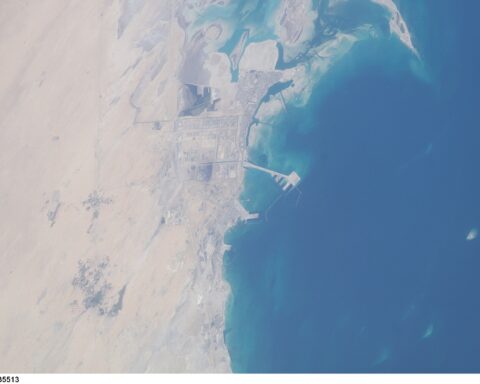

Jubail Industrial City, where Sadara’s 26 idle units sit as the single largest manufacturing complex, is not a peripheral contributor to the Saudi economy. The city produces roughly 85 percent of Saudi non-oil exports, contributes approximately 7 percent of national GDP, and accounts for 7 percent of global petrochemical output. An unnamed analyst told bne IntelliNews in April: “This is what economic chokepoint warfare looks like when it works.” The analyst was describing Jubail broadly, but Sadara — the largest venture in the complex and the only one with a $3.7 billion guarantee cliff — has become the most concrete measure of the damage.

The shutdown was attributed by Sadara to “disruption to Sadara’s supply chains” — a formulation that carefully avoided naming the IRGC threat or characterizing the closure as military in nature. Sadara added in April that the company “cannot provide, at the present time, an estimate for the return to production, as this is contingent on domestic and international factors.” The IRGC named Jubail as a target; Sadara filed a supply chain disruption. The causal link is visible to anyone reading both documents, but it is not stated — and the legal distinction between a supply chain disruption and a military attack carries different consequences for insurance, force majeure, and the guarantee structure itself.

A ceasefire or MOU signing will not reopen Jubail, even if Geneva eventually produces results. Restart depends on feedstock availability, maritime safety for petrochemical exports, and a commercial judgment that production is viable — none of which have been met. The diplomatic timeline and the debt timeline operate on different clocks, and Monday’s deadline will not wait for either.

How Was the 2021 Restructuring Designed to Avoid This Filing?

The March 2021 restructuring replaced $10 billion in completion guarantees with $3.7 billion in sponsor guarantees, extended maturity from 2029 to 2038, and set a five-year grace period ending June 15, 2026. The structure ensured that the grace period could expire without triggering mandatory disclosure from either guarantor, provided lenders agreed on a path forward.

Aramco announced the deal on March 29, 2021, framing it as a resolution to the financing challenges Sadara had faced since inception. The company and Dow agreed to guarantee up to $3.7 billion in aggregate senior debt principal, proportional to their ownership stakes, replacing the $10 billion in shareholder completion guarantees that had been released upon Sadara achieving project completion in November 2020.

The mechanics were carefully drawn: the new guarantee was not a loan and not a credit facility. It was a contingent obligation — a promise to pay if the borrower could not — sitting under SEC rules as a contingent liability rather than a direct obligation. It would become direct only when formally triggered by lender action.

The grace period gave both guarantors a five-year runway beyond the restructuring date. The maturity extension to 2038 gave lenders a new endpoint far enough in the future to justify patience. And the composition of the lending syndicate gave all parties confidence that patience was the expected outcome.

The PIF does not call guarantees on Aramco. APICORP does not force defaults on OPEC-member petrochemical ventures. Saudi national banks do not vote against the preferences of the Kingdom’s most valuable company. The international banks do not jeopardize relationship mandates for the sake of forcing a disclosure, and the ECAs answer to governments that maintain bilateral relationships with Riyadh.

The result is a structure that permits — and functionally guarantees — silent passage through the June 15 deadline. If lenders agree to a further extension before Monday, the grace period expiry becomes a contractual milestone that was navigated, not a triggering event that occurred. No 8-K is filed, no Tadawul announcement is made, and the $3.7 billion rolls forward under new terms — disclosed as a restructuring agreement rather than a default or acceleration. The 2021 template demonstrated the process: new maturity, new grace terms, no default, no disclosure drama.

Monday tests whether that template can hold a second time under conditions the 2021 negotiators could not have anticipated — a regional war, zero revenue, and accumulated losses exceeding equity. Fitterling told analysts in April that he would have “more of an update for you midyear.” Midyear is Monday. The SEC’s filing deadline for a triggering event, if one were declared, would be four business days later — Thursday, June 19. If that Thursday passes without an 8-K from either guarantor, the restructuring architecture held, and $3.7 billion in guaranteed senior debt will have expired in the regulatory equivalent of an empty room.

Frequently Asked Questions

How large was Sadara’s original project financing?

The $12.5 billion financing signed on June 16-17, 2013, was the largest multi-sourced petrochemical project finance deal in history at the time of closing. It comprised a $4.975 billion U.S. Export-Import Bank direct loan — Ex-Im’s largest ever — a $2 billion sukuk (SAR 7.5 billion, 2.6 times oversubscribed), a $1.3 billion PIF loan, a $700 million UK Export Finance-guaranteed loan, export credit agency tranches from Coface (France), Euler Hermes (Germany), and Korean agencies Kexim and K-Sure, and more than $2 billion in commercial bank lending from the 28-bank syndicate.

What is Dow’s remaining cash exposure to Sadara beyond the guarantee?

Beyond the guarantee, Dow retains approximately $100 million per year in cash commitments to Sadara running through 2038, as Fitterling confirmed on the Q1 earnings call — a twelve-year tail totaling roughly $1.2 billion in future cash outflows. Fitterling also disclosed that incoming CEO Karen Carter will inherit the Sadara restructuring negotiations, meaning the June 15 deadline arrives during a CEO transition at one of the two guarantors, with the outgoing chief executive specifically promising to assist the handover on this file.

Did the IRGC directly cause Sadara’s shutdown?

The relationship is ambiguous and legally consequential. The IRGC named Jubail Petrochemical Complex among “direct and legitimate targets” and issued evacuation orders on March 18, 2026. Sadara’s Tadawul filing thirteen days later attributed the March 31 closure to “disruption to Sadara’s supply chains” rather than to military action or the IRGC threat specifically. This distinction matters for insurance claims, force majeure provisions under the financing agreement, and the guarantee itself — a supply chain disruption and a military attack trigger different contractual consequences and different coverage under war-risk versus all-risk policies.

Could a second maturity extension avoid all disclosure?

Yes. If the lending syndicate agrees to extend the grace period or restructure the debt before a formal event of default is declared, no triggering event occurs under the SEC or Tadawul frameworks. The 2021 restructuring, which extended maturity from 2029 to 2038, was disclosed only as a commercial agreement at the time of execution — not as a default or acceleration. A second extension, negotiated consensually, would follow the same template and generate only a routine filing disclosing new terms, not a default notice.

Has the lending syndicate ever voted against Aramco’s position?

No publicly documented instance exists. The 2021 restructuring was the only prior test of the syndicate’s cohesion on Sadara, and it produced unanimous consent for a nine-year maturity extension with new sponsor guarantees. The group’s composition — ten Saudi national banks regulated by the same authority that oversees Aramco, five Gulf sovereign banks, export credit agencies answering to allied governments, and twelve international banks with broader Aramco relationship mandates — creates internal politics that have never produced a public dissent on any Aramco-related credit decision.