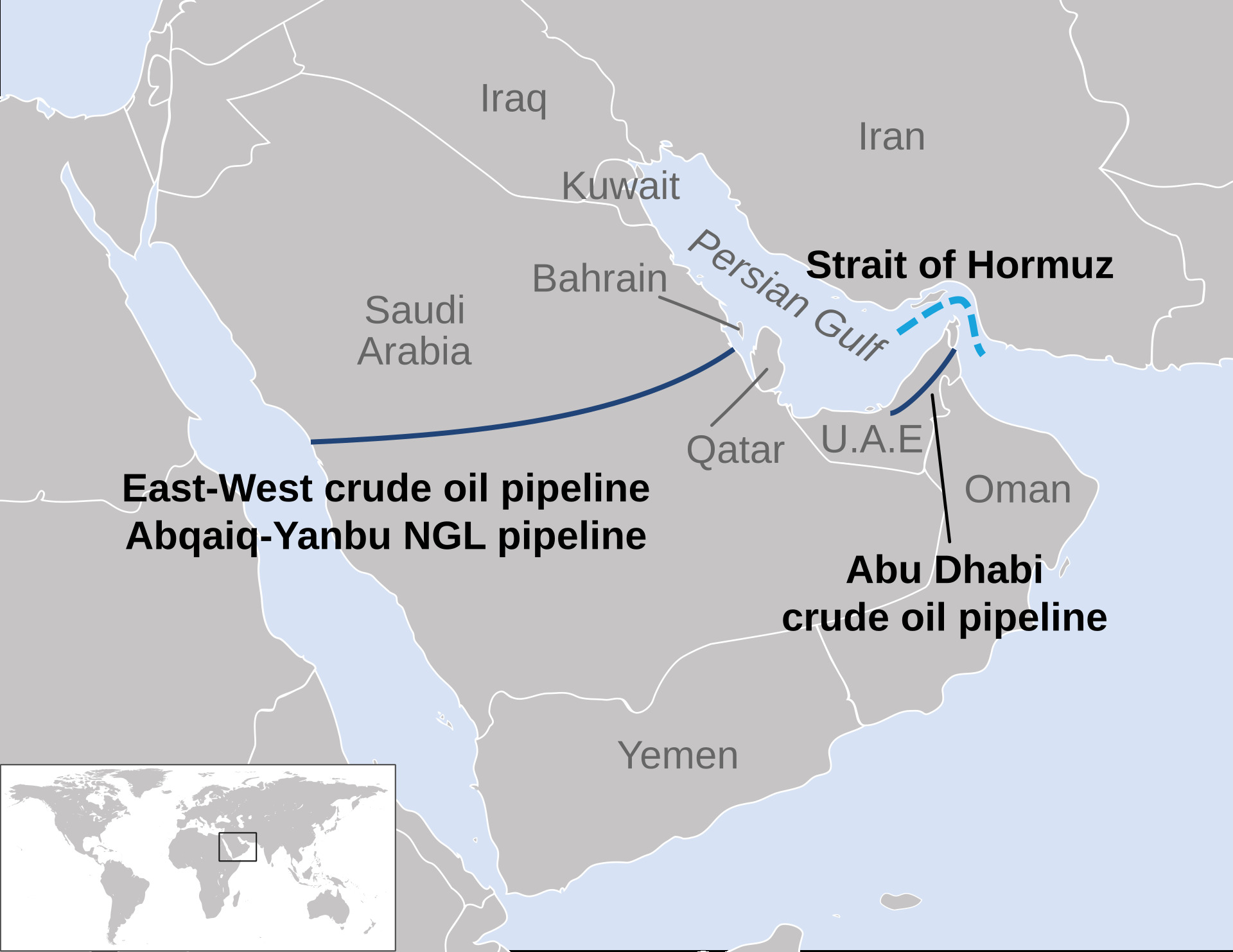

DHAHRAN — Saudi Arabia announced on April 12 that its East-West Pipeline has been restored to full 7-million-barrel-per-day pumping capacity — the same day President Trump declared a US Navy blockade of the Strait of Hormuz. The coincidence is not accidental. With the strait now closed by American warships rather than Iranian mines, every barrel of Gulf crude that reaches Asia in the coming months will flow through infrastructure that Mohammed bin Salman controls: the 1,200-kilometre Petroline to Yanbu, and the tanker berths on Saudi Arabia’s Red Sea coast. The kingdom has shifted, in forty-five days, from the war’s largest non-combatant casualty to the indispensable logistics architect of a post-blockade Gulf. The question that Asian refiners should be asking — and, according to Bloomberg, already are — is what Saudi Arabia intends to charge for that indispensability when June OSP pricing is finalized around May 5.

Table of Contents

- What Seven Million Barrels Per Day Actually Means

- The Yanbu Bottleneck

- Why a US Blockade Changes Saudi Pricing Power

- The June OSP Repricing Trap

- Can Asian Refiners Escape the Term-Contract Architecture?

- The Gulf’s Stranded Barrels

- Does Bab el-Mandeb Limit Saudi Monopoly?

- Saudi Fiscal Arithmetic at $95 Brent

- What June Pricing Reveals About the Endgame

- FAQ

What Seven Million Barrels Per Day Actually Means

The Saudi Ministry of Energy statement on April 12 was calibrated for maximum reassurance. “The facilities have recovered and regained their full operational capabilities,” the ministry said, reflecting “high operational resilience and crisis management efficiency of Saudi Aramco and the Kingdom’s energy ecosystem.” The 700,000-barrel-per-day capacity gap created by the IRGC’s April 8 strike on the East-West pumping station has been closed. The Manifa offshore field, offline since late March, is back at its 300,000-bpd plateau.

The headline figure — 7 million bpd flowing through the Petroline — is technically accurate and deserves context. The East-West Pipeline was built in 1981 to bypass tanker warfare in the Strait of Hormuz during the Iran-Iraq War. Its original design capacity was 3.2 million bpd. Saudi Arabia expanded that to 5 million bpd in 1992, then converted the parallel 48-inch NGL line to crude service in 2019, lifting the theoretical maximum to 7 million bpd. This is the first time in the pipeline’s forty-five-year history that the 7-million-bpd figure has been operationalized at sustained throughput.

Aramco CEO Amin Nasser signalled the restoration timeline in early March. “The East-West Pipeline would hit full capacity in the next couple of days,” he told S&P Global on March 10, after the initial wartime ramp-up. The April 8 IRGC strike knocked that figure back by roughly 700,000 bpd — a calibrated attack, enough to demonstrate reach against the pipeline’s pumping infrastructure, not enough to cause the kind of structural damage that would require months of repair. Engineering News-Record captured the broader infrastructure problem in a headline that read like an epitaph: “Hormuz Bypass Infrastructure Was Sized for a Short Disruption. This Is Not That.”

The one field that remains offline tells its own story. Khurais — 300,000 bpd of Arab Light, the grade that Asian refiners most need — is still under repair. Saudi Arabia restricted April liftings to Arab Light only from Yanbu, eliminating heavier grades entirely and forcing some refiners to the spot market at prices well above the already-record OSP. The combination of pipeline restoration and grade restriction is not a contradiction. It is a sequencing decision.

The Yanbu Bottleneck

The number that the Ministry of Energy statement did not mention is the one that matters most: 4.5 million barrels per day. That is the combined nominal loading capacity of Yanbu North and Yanbu South terminals, according to Argus Media. The operational tested rate is closer to 4 million bpd. The wartime effective rate — after berthing friction, security protocols, scheduling disruptions, and the tidal windows that restrict safe VLCC transit to four-hour slots twice daily — is approximately 3 to 4 million bpd depending on conditions, per Vortexa’s assessment.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The arithmetic is straightforward. The pipeline delivers 7 million bpd to the Red Sea coast. The terminals can load at most 4 to 4.5 million. Between 2.5 and 3 million barrels per day arrive at Yanbu with nowhere to go — a structural gap that no wartime improvisation can close, because the constraint is physical berth space, not pumping pressure or storage capacity.

Yanbu’s seven VLCC berths can each load approximately 132,000 barrels per hour at peak throughput. In theory, that is enough. In practice, March data from Vortexa showed 68 percent of arriving VLCCs experienced anchorage delays exceeding 36 hours, and 23 percent waited more than 72 hours. Yanbu handled 47 VLCC loadings in March — nearly four times the pre-war monthly average of 11 to 12. Breakwave Advisors noted in mid-March that “Yanbu draws wider VLCC participation as freight rates spike,” which is another way of saying that the world’s largest tankers are competing for berth time at a port designed for a fraction of the traffic it now carries.

The pre-war assessment that the East-West Pipeline bypass could cover 80 to 85 percent of Saudi exports assumed a shorter disruption and lower throughput demands. At sustained wartime volumes, the bypass covers what the port can physically load — roughly 55 to 60 percent of Saudi Arabia’s pre-war export capacity. The pipeline is not the bottleneck. The berths are.

Why a US Blockade Changes Saudi Pricing Power

Trump’s declaration of a naval blockade on April 12 followed Vice President Vance’s announcement that Islamabad peace talks had collapsed. The blockade is operationally distinct from the Iranian disruption that preceded it. Under Iranian interference — mines, IRGC naval patrols, administrative rejection of vessel transits — some ships still moved through the strait. Twenty-two transited between April 9 and 11, according to Al Jazeera, against a pre-conflict baseline of roughly 135 per day. A US Navy blockade, if enforced, reduces that trickle to zero.

The distinction matters for pricing. When Hormuz was partially obstructed, Asian refiners could model a probability-weighted recovery scenario — some percentage chance of normalization within weeks, priced into term-contract negotiations. A declared US blockade forecloses that modelling. There is no probability distribution over when an American president lifts a blockade he imposed as leverage in failed peace talks. The timeline is political, not operational, and political timelines in this administration have proven resistant to market logic.

For Saudi Arabia, the shift is structural. Under Iranian disruption, the kingdom was one of several parties trying to restore flow through Hormuz. Under an American blockade, the kingdom is the only party with an alternative export route already running at scale. The UAE’s ADCOP pipeline to Fujairah — 1.5 million bpd capacity, averaging 1.62 million bpd in March — bypasses Hormuz but exits to the Gulf of Oman, which sits inside the blockade perimeter. Iraq’s pipeline to Turkey has 1.6 million bpd of nameplate capacity and is flowing roughly 200,000 bpd. Neither substitutes for Saudi Red Sea access.

The June OSP Repricing Trap

Aramco’s May Official Selling Price for Arab Light to Asia was set on April 6 at a record premium of $19.50 per barrel above the Oman/Dubai benchmark. Bloomberg’s survey of Asian refiners and traders had anticipated a premium closer to $40 per barrel. Aramco, in other words, left approximately $20.50 per barrel on the table — a deliberate restraint that this publication examined at the time as a strategic choice to preserve Asian buyer relationships rather than extract maximum short-term rent.

That restraint was set when Brent traded near $109 and when Hormuz looked like it might partially reopen under ceasefire terms. Both conditions have changed. Brent has fallen to roughly $95 — meaning the May OSP now sits about $15 above spot rather than $10 — and Trump’s blockade has eliminated the partial-reopening scenario entirely. Buyers who signed May-June term contracts at the “restrained” Saudi price are locked in. The OSP architecture is the mechanism: Aramco sets the price once per month for the following month’s liftings, announced around the fifth of the prior month. Asian term buyers are legally committed to lift allocated volumes at whatever OSP is announced. They cannot retroactively reject the price.

June OSP is due approximately May 5. Between now and then, three variables will determine the repricing decision: whether the blockade holds or is modified, whether Hormuz transit shows any signs of normalization, and how much Asian demand has been destroyed by six weeks of constrained supply. The data on all three remains incomplete.

The December 2024 precedent cuts against aggressive repricing. MBS chose to defend market share that month rather than hold price, accepting lower revenue to maintain volume commitments to Asian buyers. The institutional memory of that decision — and the buyer relationships it preserved — is the basis for the May restraint. The counter-argument: December 2024 was a competitive market. The post-blockade Gulf is not.

| Route | Nameplate Capacity | Current Flow | Hormuz Dependent? |

|---|---|---|---|

| Saudi East-West Pipeline (Petroline) → Yanbu | 7.0M bpd | ~4.0M bpd (terminal-limited) | No |

| UAE ADCOP → Fujairah | 1.5M bpd | 1.62M bpd | Exits to Gulf of Oman — inside blockade perimeter |

| Iraq-Turkey (Kirkuk-Ceyhan) | 1.6M bpd | ~200K bpd | No |

| Strait of Hormuz (pre-war) | ~21M bpd | ~0 (US blockade) | Yes |

| Iraq southern terminals (Basra) | ~3.5M bpd | ~900K bpd | Yes |

Sources: Saudi Ministry of Energy (April 12, 2026); Argus Media; Kpler (April 7, 2026); Al Jazeera (March 27, 2026)

Can Asian Refiners Escape the Term-Contract Architecture?

Asian refiners have begun pricing US crude orders against ICE Brent rather than Dubai crude, according to OilPrice.com, a benchmark-switching behaviour driven by the wild fluctuations in the Middle Eastern benchmark caused by constrained Gulf physical supply. The shift is a workaround, not an escape. Refineries in South Korea, Japan, India, and China that were built and configured for Arab sour crude grades cannot, in any operationally meaningful timeframe, switch to light sweet alternatives without accepting yield losses, throughput penalties, and secondary-unit bottlenecks.

Bloomberg reported on March 19 that Asian buyers had begun asking Aramco to change its pricing system entirely — a request that, in forty years of OSP history, Aramco has never granted. The leverage asymmetry is the point. In 2024, 84 percent of crude flowing through Hormuz went to Asian destinations, with roughly 70 percent landing in China, India, Japan, and South Korea. Those flows are now zero through Hormuz and constrained through Yanbu. The buyers have no alternative supplier at the volume and grade specifications their refineries require.

The captive-buyer architecture extends beyond pricing. Saudi Arabia’s restriction of April liftings to Arab Light only — eliminating Arab Medium and Arab Heavy from Yanbu allocations — forced refiners configured for heavier grades to the spot market, where premiums have been running $6 to $8 per barrel above already-elevated Saudi term prices. Khurais, the primary source for Arab Light production, remains under repair at 300,000 bpd offline. The grade restriction is not a temporary wartime measure. It is the structural consequence of routing export-quality crude through a pipeline-and-port system that was not designed to handle the full spectrum of Saudi production simultaneously.

The Gulf’s Stranded Barrels

The scale of crude stranded behind the blockade is difficult to overstate. Kpler’s assessment as of April 7 — before the blockade declaration — estimated approximately 11 million bpd of production removed across Gulf producers, plus 3 million additional barrels from refinery run reductions. Iraq’s exports have collapsed from roughly 4 million bpd pre-war to approximately 900,000 bpd. Kuwait is down to 280,000 bpd. Qatar’s maritime condensate exports stand at 135,000 bpd.

The UAE presents a partial exception. ADCOP’s pipeline to Fujairah averaged 1.62 million bpd of exports in March, exceeding the pipeline’s nameplate capacity of 1.5 million bpd. But Fujairah sits on the Gulf of Oman, and tankers loading there must transit waters that a US Navy blockade can interdict. Whether the blockade will extend to Fujairah-loaded vessels carrying UAE crude is an operational question with no public answer as of April 12. The ambiguity itself suppresses traffic.

The total Gulf crude stranded without viable export route — accounting for pipeline bypasses, reduced production, and blockade-affected alternatives — sits between 8 and 11 million bpd. That figure represents roughly 8 to 11 percent of global production. Goldman Sachs has modelled the scenario: if Hormuz remains mostly shut for another month, Brent averages above $100 through 2026, with a Q3 extended-closure scenario at $120 per barrel. JP Morgan’s parallel estimate adds $15 to $20 per barrel of upside risk if full Hormuz recovery delays past July.

Does Bab el-Mandeb Limit Saudi Monopoly?

Saudi Arabia’s Red Sea monopoly position carries a qualifier that no pipeline restoration can address. Approximately 70 to 75 percent of Yanbu’s crude exports transit the Bab el-Mandeb strait en route to Asian markets. Mohammed Mansour, the Houthi government’s deputy information minister, stated the risk plainly: “Closing the Bab el-Mandeb Strait is a viable option, and the consequences will be borne by the American and Israeli aggressors.”

Iran’s two-chokepoint doctrine — demonstrated through coordinated IRGC action at Hormuz and Houthi threats at Bab el-Mandeb — means that the Saudi bypass solves one half of a geography problem. Tankers loading at Yanbu for the Suez-Asia route must transit 1,600 kilometres of Red Sea coastline within range of Houthi anti-ship missiles and drone systems that have, since 2023, repeatedly demonstrated the ability to strike commercial shipping. The alternative — routing around the Cape of Good Hope — adds 10 to 14 days to Asia-bound voyages and corresponding freight costs, partially eroding the price advantage that Saudi term contracts offer over more distant alternatives.

The Houthi threat is not hypothetical, but it is also not yet realized against Saudi-loaded tankers specifically. The operational distinction between targeting vessels bound for Israel — the stated Houthi policy since late 2023 — and targeting Saudi crude exports headed to China and India would represent a different order of escalation, one with direct consequences for the Houthi movement’s relationship with its primary backers in Tehran and its economic relationships with the same Asian powers that buy Saudi crude. The threat constrains Saudi pricing leverage not because an attack is imminent but because war-risk insurance premiums for Red Sea transits are already factored into the delivered cost of Yanbu crude at Asian destinations.

Saudi Fiscal Arithmetic at $95 Brent

The pipeline restoration announcement lands in a fiscal environment that makes June OSP pricing a genuinely consequential decision. Bloomberg’s PIF-inclusive estimate of Saudi Arabia’s fiscal break-even sits between $108 and $111 per barrel. Brent is trading at roughly $95. Goldman Sachs’s war-adjusted fiscal deficit projection for 2026 runs to $80 to $90 billion, against an official Saudi forecast of $44 billion published before the war.

The gap between break-even and market price is approximately $13 to $16 per barrel at current levels — a gap that every dollar of OSP premium partially closes. The $20.50 per barrel gap between Aramco’s restrained May OSP and Bloomberg’s market-clearing expectation, applied across 4 million bpd of Yanbu throughput, represents roughly $82 million per day in foregone revenue — approximately $2.5 billion per month.

That $2.5 billion monthly figure sits against a war-adjusted deficit running to roughly $7 billion per month on the Goldman estimate. Aggressive June OSP repricing would not close the fiscal gap — the terminal bottleneck at Yanbu prevents the volume solution — but it would reduce the deficit by roughly a third. The cost would be measured in buyer relationships rather than barrels: Asian refiners who accepted the May restraint as evidence of Saudi reliability would interpret aggressive June pricing as monopoly rent extraction, and their institutional memory of that betrayal would outlast the blockade itself.

What June Pricing Reveals About the Endgame

No direct MBS statement on Hormuz reopening has been published this week. The observable signals are in the infrastructure decisions. Pipeline restoration announced on the same day as the blockade declaration — timing that required advance knowledge of or coordination with the US announcement. April liftings restricted to the grade that commands the highest premium. Khurais still under repair while less valuable production comes back online first. Each choice is consistent with an actor who is in no hurry to see Hormuz reopen, but who cannot yet fully monetize the monopoly position because 3 million barrels per day of pipeline throughput arrive at Yanbu with no berth to load them.

The June OSP, due around May 5, is the first moment that MBS’s calculation becomes legible. A restrained June OSP — holding near the May level of $19.50 premium — would signal that Saudi Arabia is playing a longer game: preserving buyer alignment for the post-war order, accepting fiscal pain in exchange for the structural position of being the Gulf’s last reliable supplier. That position has a value that exceeds any single month’s pricing premium, and MBS’s track record since 2024 suggests he understands the compound interest on reliability.

An aggressive June OSP — moving toward the $40-per-barrel premium that Bloomberg’s survey indicated the market expected in May — would signal something different. It would signal that the blockade has been priced as durable, that the fiscal gap cannot be managed through restraint alone, and that the terminal bottleneck at Yanbu makes volume growth impossible, leaving price as the only available lever. Asian refiners would pay it, because they have no alternative at the required grade and volume. They would also remember it.

A third possibility is more granular than either extreme: differentiated pricing by destination, with restrained OSP for term buyers who maintained liftings through the disruption and elevated spot pricing for buyers who dropped allocations and are now returning. Aramco has the contractual architecture to execute this, and it would allow MBS to reward loyalty and penalize defection simultaneously — extracting rent from the margin while preserving the core relationships.

The structural irony of April 12 is that Saudi Arabia’s two announcements — pipeline restoration and blockade commencement — create opposite impressions. The pipeline headline suggests abundance: 7 million bpd restored, crisis resolved. The blockade headline suggests scarcity: Hormuz sealed, Gulf exports stranded. The reality is in between, and the gap between pipeline capacity and terminal throughput — those 2.5 to 3 million barrels per day that arrive at the Red Sea coast but cannot load — is the space in which Saudi pricing power and its limits both reside. May 5, not April 12, is the date that matters.

Frequently Asked Questions

How long would it take to expand Yanbu terminal capacity to match the pipeline’s 7-million-bpd throughput?

New VLCC berth construction at an established port typically requires 18 to 24 months under peacetime procurement and permitting conditions. Saudi Arabia would need to add four to five additional deep-water berths to close the 2.5-to-3-million-bpd gap, plus associated tank farm expansion and single-point mooring installations. Aramco has not publicly announced any Yanbu expansion project, and wartime construction timelines for port infrastructure historically run 30 to 50 percent longer than peacetime equivalents due to labour, material, and security logistics constraints.

What happens to Gulf producers who lack pipeline bypass routes if the blockade continues through Q3?

Kuwait, which is exporting 280,000 bpd against pre-war capacity of roughly 2.7 million bpd, faces the most acute pressure — the country has no pipeline bypass and its fiscal reserves, while substantial (Kuwait Investment Authority manages roughly $900 billion), have never been stress-tested against a sustained zero-export scenario. Iraq’s southern terminals at Basra account for roughly 85 percent of government revenue. Qatar’s LNG exports, which constitute 60 percent of government revenue, are routed through Hormuz and cannot be redirected by pipeline. Bahrain produces only 200,000 bpd domestically and was already running on Saudi-supplied crude via the BAPCO pipeline from Abqaiq before the war.

Could the US Navy blockade exempt certain categories of vessel traffic?

The legal and operational framework for selective enforcement has not been specified in Trump’s April 12 declaration. Historical precedents — the US “tanker escort” operations of 1987-88, the UN-mandated Iraqi oil embargo of 1990-2003 — involved formal exemption mechanisms administered through the UN Security Council or bilateral flag-state agreements. No such mechanism has been proposed for the current blockade. LNG carriers, which serve different downstream markets than crude tankers, could be candidates for exemption, but the Islamabad talks’ failure removed the diplomatic context in which such carve-outs would normally be negotiated.

Why did Brent fall from $109 to $95 despite the Hormuz closure worsening?

The price decline reflects demand destruction rather than supply optimism. Six weeks of constrained Gulf exports have forced Asian refiners to cut throughput, defer maintenance turnarounds, and draw down strategic reserves — all of which reduce near-term crude demand. China’s independent “teapot” refineries in Shandong province, which process roughly 4 million bpd and rely heavily on sanctioned Iranian and discounted Russian crude, have seen utilization rates fall to 55 percent from a pre-war average near 75 percent. The demand response is masking the supply deficit: Kpler estimates a 6-million-bpd physical shortfall that current prices do not fully reflect because forward curves are pricing eventual Hormuz reopening that the blockade has now deferred.

Has Saudi Arabia indicated whether it would support or oppose the US blockade at the UN Security Council?

Saudi Arabia has not issued a public statement on the blockade as of April 12. The kingdom’s position is structurally conflicted: the blockade benefits Saudi pricing power and Red Sea export exclusivity, but it also traps Saudi crude production that exceeds Yanbu terminal capacity and prevents the normalization of Gulf shipping lanes on which Saudi Arabia’s post-war economic recovery depends. The kingdom’s earlier co-drafting of a Hormuz reopening resolution with Bahrain — which Russia and China vetoed — suggests official Saudi policy favours restoration of transit passage, even as the blockade’s practical effect strengthens Saudi market position relative to Gulf competitors.