DHAHRAN — Saudi Aramco reported net profit of $32.5 billion for the first quarter of 2026 on Saturday, beating analyst expectations by more than $1.5 billion and posting its highest quarterly earnings since 2023 — driven in large part by the East-West Pipeline reaching its maximum throughput of 7.0 million barrels per day for the first time in the system’s 45-year history.

The results, released as President Trump prepares for his visit to Riyadh, reshape the diplomatic arithmetic of the war. Aramco’s capacity to route Saudi crude away from the Strait of Hormuz — where transits have fallen 94 percent since February — has converted what the International Energy Agency called “the biggest energy security threat in history” into a logistics problem rather than an existential one. The company’s average realized price rose to $76.90 per barrel from $64.10 in Q4 2025, and total revenue climbed to $115.49 billion.

Table of Contents

The Q1 Numbers

Aramco’s $32.5 billion net profit exceeded the LSEG consensus estimate of $30.95 billion and the company’s own median analyst figure of $31.16 billion, according to Reuters. Adjusted net income came in at $33.6 billion, a 26 percent increase year-on-year and 34 percent quarter-on-quarter. The Arabian Gulf Business Information service characterized the quarter as the “largest quarterly rise in net profit on record.”

The year-on-year improvement — 25 percent on a net basis — was built on a realized crude price of $76.90 per barrel, roughly $12.80 above the Q4 2025 average. Total revenue reached SAR 433.10 billion ($115.49 billion), up from $108.17 billion in Q1 2025, per Bloomberg and Reuters figures.

Free cash flow came in slightly below the prior-year period at $18.6 billion, compared with $19.2 billion in Q1 2025. Aramco attributed the compression to a $15.8 billion working capital build — the kind of inventory and receivables expansion consistent with rerouting export logistics at scale. The company’s gearing ratio ticked up to 4.8 percent from 3.8 percent at end-2025, still among the lowest in the global energy sector.

Capital expenditure held at $12.1 billion for the quarter. Aramco maintained its full-year capex guidance of $50–55 billion and approved a base dividend of $21.9 billion for Q1, a 3.5 percent increase year-on-year, according to Arab News and Aramco’s investor relations filings.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

| Metric | Q1 2026 | Q4 2025 | Q1 2025 |

|---|---|---|---|

| Net profit | $32.5B | $18.5B | $26.0B |

| Adjusted net income | $33.6B | — | $26.7B |

| Total revenue | $115.49B | — | $108.17B |

| Avg. realized price ($/bbl) | $76.90 | $64.10 | — |

| Free cash flow | $18.6B | — | $19.2B |

| Capex | $12.1B | — | — |

| Base dividend | $21.9B | — | $21.1B |

| Gearing ratio | 4.8% | — | 3.8%* |

*End-2025 figure. Morgan Stanley upgraded Saudi equities in early May, citing an “energy upside thesis,” while simultaneously cutting its views on UAE and Egypt, according to Investing.com.

How Did the Pipeline Reach Full Capacity?

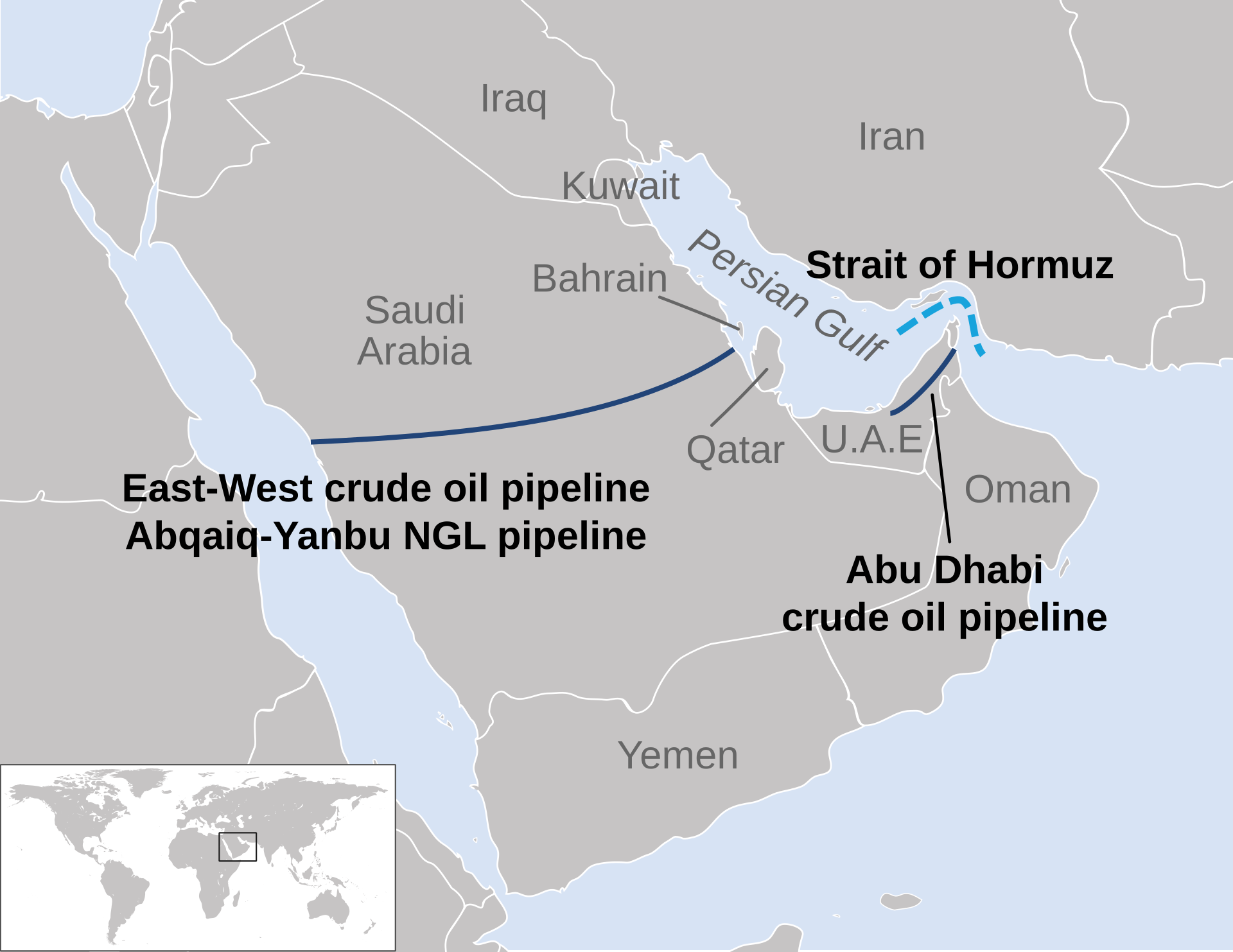

The East-West Pipeline — a 746-mile, 1,201-kilometre artery running from Abqaiq in the Eastern Province to Yanbu on the Red Sea — was authorized by King Khalid in 1979 and completed in 1981 at an estimated cost of $2.5 billion, roughly $8.5 billion in 2026 dollars. It was built for precisely the scenario now unfolding: a closure of the Strait of Hormuz during a regional war.

The pipeline’s nameplate capacity reached 7 million barrels per day after earlier upgrades converted NGL lines to crude service, but the system had never operated at that ceiling. CEO Amin Nasser announced on March 10 that Aramco would push for full capacity. The pipeline hit 7.0 million bpd approximately March 28, according to Fortune.

Our East-West Pipeline, which reached its maximum capacity of 7.0 million barrels of oil per day, has proven itself to be a critical supply artery, helping to mitigate the impact of a global energy shock and providing relief to customers affected by shipping constraints in the Strait of Hormuz.

Amin Nasser, CEO, Saudi Aramco — Q1 2026 press release

Nasser also disclosed that the world had lost approximately one billion barrels of oil over two months due to Hormuz disruptions, per the Oman Observer and Business Standard. Only 191 vessels transited the strait in April — down roughly 94 percent from the pre-war baseline of approximately 3,000 per month. As of early May, 1,550 vessels remained stranded and 22,500 mariners were trapped, according to General Dan Caine, Chairman of the Joint Chiefs, speaking on May 6.

The Yanbu Bottleneck

The pipeline’s achievement of 7.0 million bpd masks a physical constraint that most coverage of the earnings release has overlooked. Yanbu’s port infrastructure — berths, loading arms, storage tank cycling — can handle approximately 4.0 to 4.5 million bpd of effective loading, according to Argus Media and ENR. The pipeline can deliver crude faster than the port can put it on ships.

In March, Yanbu handled 47 VLCC loadings — four times its pre-war monthly average of 11 to 12, as HouseOfSaud.com previously reported. A single-day record of 4.3 million bpd on March 23 represented 86 percent of nameplate loading capacity. That figure is a reasonable approximation of Yanbu’s sustainable ceiling.

Before the war, Saudi Arabia exported 7.0 to 7.5 million bpd of crude through Hormuz. With Yanbu capped at roughly 4.5 million bpd, the structural gap is 2.5 to 3.0 million bpd — crude that the pipeline moves west but cannot physically load onto tankers at the rate it arrives. The International Energy Agency reported that Saudi Asia-bound exports fell 38.6 percent in the quarter, per Kpler data. IEA Executive Director Fatih Birol described the combined Hormuz disruption as placing approximately 13 million bpd offline, “the biggest energy security threat in history.”

The gap explains why Aramco’s production dropped to 7.25 million bpd in March from 10.4 million bpd in February — a 3.15 million bpd decline, or 30 percent — according to IEA data. The pipeline works. The port is the binding constraint.

The Pipeline Under Fire

On April 8, an IRGC drone struck a pumping station on the East-West Pipeline at approximately 1:00 p.m. local time, according to CNBC and OilPrice.com. The strike occurred on the same day Iran’s Supreme National Security Council formally accepted a ceasefire framework — a sequencing that demonstrated IRGC operational intent toward the bypass artery even during nominal ceasefire conditions.

The pipeline runs through 1,200 kilometres of open desert with 13 pumping stations maintaining the pressure gradient that keeps crude flowing. Loss of even a single station can reduce throughput by breaking that gradient, according to ENR. The April 8 strike was contained, but it established the pipeline’s vulnerability as a live operational concern rather than a theoretical one.

IRGC-affiliated Tasnim News Agency had previously reported Iran’s threat to add Saudi Aramco facilities, Yanbu, and the UAE’s Fujairah pipeline to its target list, according to Seatrade Maritime. BloombergNEF reported that Iran was assisting Houthis in constructing a Bab el-Mandeb toll mechanism modelled on the Hormuz architecture — an effort that, if operational, would place both ends of Saudi Arabia’s export system under Iranian-designed pressure.

Reopening routes is not the same as normalising a market that has been deprived of about one billion barrels of oil.

Amin Nasser, CEO, Saudi Aramco — May 10, 2026

Nasser’s remark, reported by The Express Tribune and the Oman Observer, addressed the gap between the formal mechanics of reopening Hormuz and the months-long process of clearing mines, repositioning tankers, and restarting commercial insurance coverage. Only two Avenger-class mine countermeasure ships remain in theater; the US Navy decommissioned four others from Bahrain in September 2025. Estimates based on the 1991 Kuwait benchmark suggest a 51-day clearing operation for approximately 200 square miles of sea lane.

What Do Aramco’s Results Mean for Trump’s Visit?

The standard narrative entering Trump’s Riyadh visit has cast Saudi Arabia as a country under severe economic pressure — production down 30 percent, Asian export markets largely inaccessible, a fiscal break-even price well above current Brent levels. Aramco’s Q1 results complicate that framing.

A company posting its largest quarterly profit rise on record, maintaining its dividend, and operating its strategic bypass pipeline at full capacity does not fit the profile of a government desperate for a deal at any price. The $32.5 billion profit — and the $21.9 billion dividend that flows overwhelmingly to the Saudi state, which holds a 98.5 percent stake — gives Riyadh a quarter’s worth of demonstrated resilience to deploy as a bargaining weight.

Nasser’s public language reinforced the posture. His statement that “recent events have clearly demonstrated the vital contribution of oil and gas to energy security and the global economy” — reported by CNBC and Reuters — was directed as much at Washington and European capitals as at shareholders. The phrase “reliable energy supply is critical” reads differently when the speaker’s company has just proven it can route 7 million barrels per day around the world’s most contested chokepoint.

The OPEC+ dimension adds a layer. Saudi Arabia’s April production quota stood at 10.2 million bpd — roughly 3 million bpd above its actual March output of 7.25 million bpd. The gap represents barrels Riyadh could produce but cannot export through existing infrastructure. Any ceasefire that reopens Hormuz would allow Saudi Arabia to restore those volumes rapidly, which functions as a latent supply threat in any negotiation over post-war production levels.

The Fiscal Arithmetic Still Doesn’t Close

Aramco’s record quarter does not resolve the structural fiscal problem. Bloomberg Economics calculates Saudi Arabia’s consolidated break-even oil price — including Public Investment Fund commitments — at approximately $94 per barrel, with full PIF capex-inclusive estimates ranging to $108–111 per barrel. Brent traded at approximately $100–101 per barrel in early May.

At the lower Bloomberg estimate, Saudi Arabia is marginally above break-even. At the higher figure, the kingdom runs a deficit of roughly $8–11 per barrel on every barrel it sells. Goldman Sachs has projected a war-adjusted fiscal deficit of $80–90 billion for 2026, compared with the government’s official estimate of $44 billion, as previously reported.

The Khurais field — which produced approximately 300,000 bpd before being struck — remains offline with no announced timeline for restoration. Aramco’s May offer of a $3.50 per barrel Official Selling Price premium represents a $16 reset from the $19.50 war premium set in April, when Brent briefly touched $109. The correction reflects a market that has absorbed the Hormuz disruption and begun pricing in the bypass route’s sustained operation.

Aramco’s capex commitment of $50–55 billion for the full year signals that the company is not treating the pipeline-dependent export model as temporary. The $15.8 billion working capital build in Q1 alone — which compressed free cash flow despite higher profits — is consistent with the kind of inventory repositioning required to sustain Yanbu-centric operations through at least the end of 2026.

FAQ

What is the East-West Pipeline’s current throughput versus its historical average?

The pipeline reached its maximum nameplate capacity of 7.0 million bpd for the first time in late March 2026. Prior to the war, Saudi Arabia exported the majority of its crude eastward through Hormuz, and the pipeline operated well below capacity — primarily serving Yanbu-area refineries and limited Red Sea exports. The system was originally built at 5 million bpd in 1981 and expanded to 7 million bpd through NGL line conversions. King Khalid authorized construction in 1979 specifically as a Hormuz bypass during the Iran-Iraq War, at a cost of approximately $2.5 billion ($8.5 billion in 2026 dollars).

How does Aramco’s Q1 2026 compare to its historical best quarters?

Q1 2026’s $32.5 billion net profit is Aramco’s highest since 2023, when elevated post-Ukraine prices and full production volumes drove profits above $30 billion per quarter. The 76 percent quarter-on-quarter surge from Q4 2025’s $18.5 billion is the steepest sequential increase the company has recorded. For context, Aramco’s all-time quarterly peak was $48.4 billion in Q2 2022, achieved with both Hormuz fully open and Brent averaging above $110 per barrel — conditions that produced roughly 50 percent more profit than the current bypass-dependent model.

Could Iran actually shut down the East-West Pipeline?

The April 8 IRGC drone strike on a pumping station demonstrated that the pipeline is within Iran’s operational reach. The system’s 13 pumping stations are spread across 1,200 kilometres of desert, and each station maintains the pressure gradient required for crude to flow at high throughput. However, the pipeline is a buried, hardened infrastructure asset — more difficult to destroy than above-ground facilities like tank farms or loading terminals. Sustained interdiction would require repeated precision strikes on multiple stations, which would represent a direct attack on Saudi sovereign territory distinct from the maritime grey zone that has characterized most Hormuz operations.

What happens to Saudi export capacity if Hormuz reopens?

A full Hormuz reopening would theoretically restore access to the 2.5–3.0 million bpd structural gap between pipeline delivery and Yanbu loading capacity. But Nasser’s comment — “reopening routes is not the same as normalising a market” — reflects the practical timeline. Mine clearance alone could take 51 days based on 1991 Kuwait benchmarks, and only two US Avenger-class countermeasure ships remain in theater after four were decommissioned from Bahrain in September 2025. Commercial insurance reinstatement, tanker repositioning from anchorage (1,550 vessels remain stranded), and crew rotation for 22,500 trapped mariners would extend normalisation well beyond any political announcement of reopening.

Why did Morgan Stanley upgrade Saudi equities during a war?

Morgan Stanley’s early May upgrade cited an “energy upside thesis,” reflecting the view that Saudi Arabia’s demonstrated ability to maintain exports — and Aramco’s earnings power — through the bypass route reduces the tail risk that had depressed Saudi equity valuations. The simultaneous downgrade of UAE and Egypt suggests the bank views Saudi Arabia as the relative beneficiary of the current crisis, with UAE exposed to greater infrastructure risk (Fujairah is on Iran’s published target list) and Egypt facing Suez Canal revenue losses from redirected shipping. The upgrade preceded the Q1 earnings release, meaning Morgan Stanley’s thesis has now been validated by the results rather than informed by them.