Washington Wants to Pay $20 Billion to Make Iran’s Uranium Disappear — Then Ask Saudi Arabia to Give Up the Same Right for Free

WASHINGTON — The Trump administration is negotiating to unfreeze approximately $20 billion in Iranian assets held in China in exchange for Tehran surrendering its 440.9 kg stockpile of highly enriched uranium — a deal that, if concluded on anything resembling the terms leaked to Axios on April 17, will make the pending US-Saudi 123 Agreement politically unsignable. The structural problem is not hypocrisy, though there is plenty of that. It is that Washington is about to establish a price — $20 billion, plus a time-limited enrichment moratorium of somewhere between five and twenty years — for an enrichment capability it simultaneously expects Saudi Arabia to voluntarily forgo under a civil nuclear agreement whose own draft text does not even prohibit Riyadh from enriching.

That asymmetry is not a footnote to the Iran negotiations. It is the central fact that will determine whether Saudi Arabia’s $80 billion, 16-reactor nuclear power program proceeds under American partnership or pivots irreversibly toward alternatives — China, South Korea, Russia — that will not ask Riyadh to surrender rights Washington is paying Tehran to temporarily pause.

Table of Contents

- Introduction

- What Is the $20 Billion Iran Deal and Where Does the Money Come From?

- Trump’s Three Positions in 24 Hours

- Why Does the Iran Deal Threaten the US-Saudi 123 Agreement?

- The Moratorium Gap: 5 Years, 20 Years, or Permanent?

- The UAE Domino No One in Washington Is Discussing

- How Does This Repeat the JCPOA Gulf Exclusion?

- Saudi Arabia’s Leverage Is Larger Than Washington Admits

- What Happens If the 123 Agreement Dies?

- Frequently Asked Questions

What Is the $20 Billion Iran Deal and Where Does the Money Come From?

The $20 billion under discussion represents frozen Iranian oil revenues and trade receivables held in Chinese financial institutions — the single largest country-specific tranche of Iran’s global frozen asset portfolio, which Al Jazeera reported on April 15 exceeds $100 billion across multiple jurisdictions. China holds roughly $20 billion. India holds approximately $7 billion. Iraq holds $6 billion in restricted energy-payment accounts. Qatar-administered accounts contain roughly $6 billion originally transferred from South Korean banks. Japan holds $1.5 billion. The United States itself has approximately $2 billion in directly frozen Iranian funds, with additional holdings scattered across EU jurisdictions, Luxembourg, the UAE, Singapore, Turkey, and Hong Kong-registered shell entities.

The Axios scoop, published April 17, confirmed that US and Iranian negotiators are actively discussing “what will happen to the stockpile” of enriched uranium and “how much of Iran’s assets will be unfrozen.” Iran’s counter-demand, per the same report, is $27 billion — a $7 billion gap that both sides appear willing to negotiate across. The proposed exchange: Tehran surrenders its 440.9 kg of uranium enriched to 60% — material the IAEA last physically verified on February 28, 2026, before Iran terminated inspector access — and Washington releases the Chinese-held frozen funds.

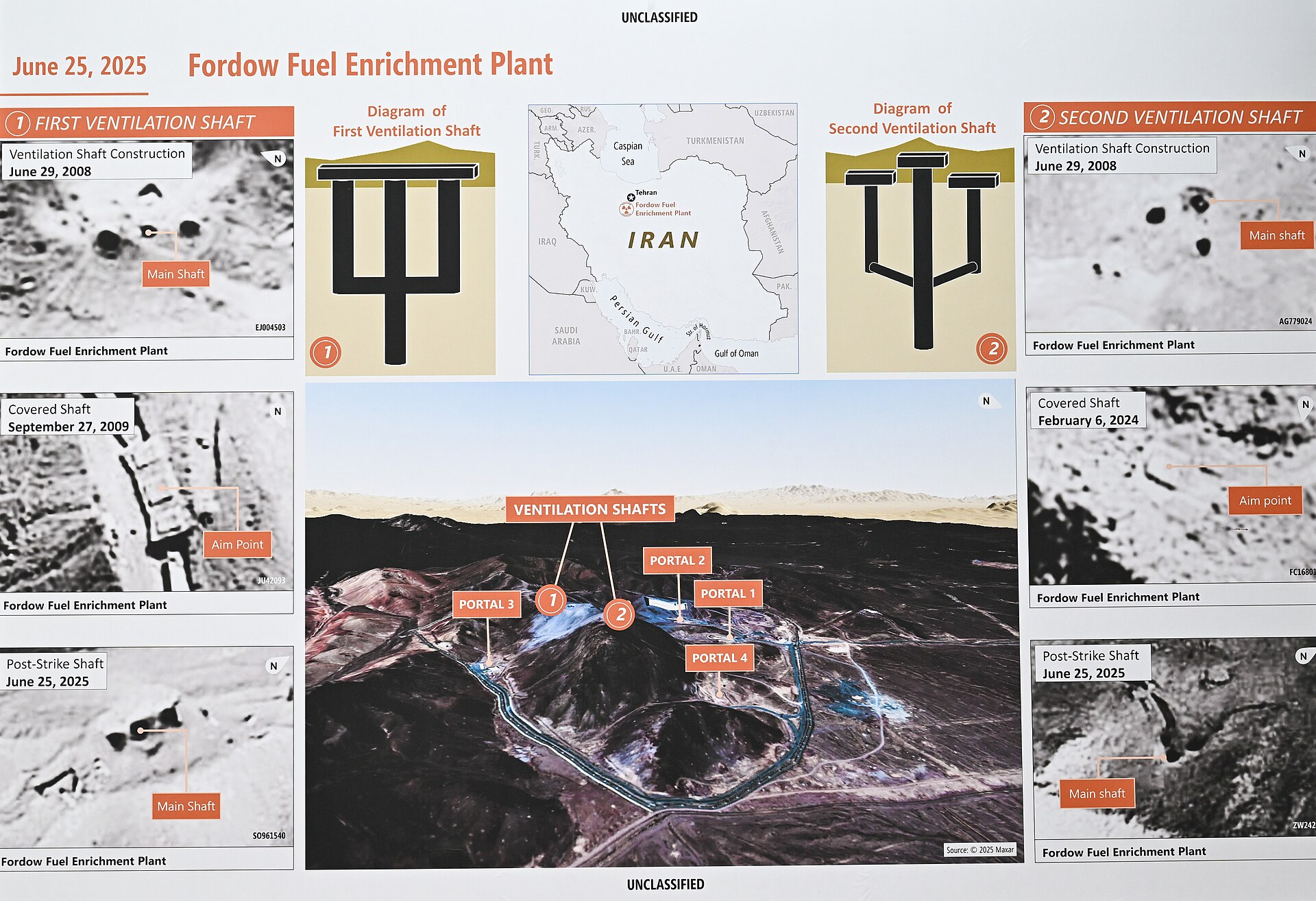

The mechanism for uranium transfer remains the deal’s most unresolved element. Russia proposed taking custody of the HEU under IAEA monitoring, first in March 2026 and again on April 13. Trump rejected the Russian option in a March 13 phone call with Putin. Iran proposed domestic dilution — blending the 60% material down to reactor-grade levels inside its own facilities under IAEA supervision — which the US considers insufficient. Trump himself told Reuters the US would “go down and start excavating with big machinery” to retrieve the uranium from the underground complexes at Isfahan where it was entombed following Operation Midnight Hammer in June 2025.

That 440.9 kg, if further enriched via Iran’s operational IR-6 cascades, could yield material for approximately 11 nuclear devices within an estimated 25 days — a breakout timeline that explains Washington’s urgency but does not explain why that urgency should require paying for what the IAEA’s own inspectors cannot currently verify still exists in recoverable form.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

| Jurisdiction | Estimated Holdings | Status |

|---|---|---|

| China | ~$20 billion | Under negotiation for release |

| India | ~$7 billion | Frozen; GL U expired April 19 |

| Iraq | ~$6 billion | Restricted energy-payment accounts |

| Qatar (ex-South Korean transfer) | ~$6 billion | Restricted; Biden blocked access |

| United States | ~$2 billion | Directly frozen |

| EU / Luxembourg | ~$1.6 billion | Frozen under reimposed sanctions |

| Japan | ~$1.5 billion | Frozen |

| Other (UAE, Singapore, Turkey, HK) | Undisclosed | Various restrictions |

Sources: Al Jazeera, April 15, 2026; Axios, April 17, 2026; US Treasury OFAC records

Trump’s Three Positions in 24 Hours

Within a single news cycle following the Axios report, President Trump articulated three mutually exclusive positions on the deal’s financial terms. On Truth Social, he wrote: “The U.S.A. will get all Nuclear ‘Dust’…No money will change hands in any way, shape, or form.” In a Reuters interview published the same day, he described sending American personnel to “go down and start excavating with big machinery” — implying physical seizure of Iranian uranium from underground facilities inside sovereign Iranian territory under IRGC guard. And Axios, sourced to officials directly involved in the negotiations, confirmed that the financial terms — how much of the $20 billion, under what conditions, with what monitoring — are the active subject of negotiation.

The contradictions are not cosmetic. If no money changes hands, there is no deal — Iran’s negotiating position, consistent since the JCPOA and reaffirmed in the current round, conditions any nuclear concession on asset release. If the US plans to physically excavate uranium from Iranian soil, that is not a negotiation but an invasion. And if the administration is simultaneously telling its own negotiators to price the HEU transfer while telling the public no money is involved, the gap between diplomatic reality and domestic messaging will collapse the moment any agreement text surfaces.

This internal incoherence matters for Riyadh because Saudi negotiators tracking the 123 Agreement cannot determine what precedent the Iran deal will actually set. A $20 billion cash-for-uranium arrangement establishes that enrichment capability has a buyout price. A permanent enrichment ban — Trump’s stated demand — establishes that Washington will not tolerate any regional enrichment under any circumstances. A 5-to-20-year moratorium establishes that enrichment rights are negotiable and temporary. Each outcome produces a different 123 Agreement calculus, and the Trump administration is publicly committed to all three simultaneously.

Why Does the Iran Deal Threaten the US-Saudi 123 Agreement?

The US-Saudi 123 Agreement, as submitted to Congress via formal notification in November 2025, employs language that applies “additional safeguards and verification measures to the most proliferation-sensitive areas of potential nuclear cooperation between the Kingdom of Saudi Arabia and the United States” — covering “enrichment, conversion, fuel fabrication, and reprocessing.” What the draft does not do is prohibit Saudi enrichment. The distinction is critical. The text creates a monitoring and safeguards framework around enrichment activity without requiring Riyadh to forgo the activity itself.

Kelsey Davenport, Director for Nonproliferation Policy at the Arms Control Association, warned in February 2026 that the Trump administration “has not carefully considered the proliferation risks posed by its proposed nuclear cooperation agreement with Saudi Arabia or the precedent this agreement may set.” Her assessment was sharper on the enrichment question: “Once the bilateral safeguards agreement is in place, it will open the door for Saudi Arabia to acquire uranium enrichment technology or capabilities — possibly even from the United States.”

The $20 billion Iran deal destroys this carefully ambiguous architecture. If Washington pays Iran to surrender enriched uranium while accepting a time-limited enrichment moratorium — any duration short of permanent — it has established three precedents simultaneously. First, that regional enrichment is a negotiable commodity with a price. Second, that the appropriate response to enrichment capability is compensation, not prohibition. Third, that enrichment freezes are temporary instruments, not permanent conditions. Each precedent runs directly against the implied expectation — never contractually specified — that Saudi Arabia will voluntarily abstain from enrichment under the 123 Agreement.

Saudi Energy Minister Prince Abdulaziz bin Salman stated publicly in January 2023 that Saudi Arabia intends to develop the full nuclear fuel cycle, including enrichment for domestic use and export. KACARE’s program envisions 16 reactors generating 17.6 GW of nuclear electricity by 2040, at a cost of approximately $80 billion, with domestic uranium resources — surveyed under a Saudi Geological Survey-CNNC memorandum of understanding — of approximately 90,000 recoverable tonnes. This is not an abstract aspiration. It is a funded, surveyed, and publicly declared industrial program that the 123 Agreement’s own text does not require Riyadh to abandon.

The structural trap for Washington is that any Iran deal short of permanent, verified dismantlement — which no party to the current negotiations expects to achieve — makes the 123 Agreement’s enrichment ambiguity politically untenable in Riyadh. Saudi negotiators will face a binary question from their own principals: why should the Kingdom voluntarily forgo a right that the agreement text does not prohibit, that Washington just paid Iran $20 billion to temporarily suspend, and that Saudi domestic uranium reserves make technically feasible?

The Moratorium Gap: 5 Years, 20 Years, or Permanent?

The enrichment moratorium is the variable that converts the $20 billion deal from a nonproliferation achievement into a 123 Agreement killer. US negotiators led by Vice President JD Vance proposed a 20-year enrichment moratorium during the Islamabad talks. Trump publicly rebuked the proposal, telling reporters: “I don’t like the 20 years. I don’t want them to feel like they have a win.” Iran countered with a five-year suspension, which the US rejected. Trump’s stated position is a permanent enrichment ban — a demand that no Iranian faction, including the civilian government Pezeshkian has already confessed he cannot control, has the authority or willingness to accept.

The three-way gap — five years (Iran), twenty years (Vance), permanent (Trump) — means the moratorium will land, if it lands at all, on a compromise duration that satisfies nobody’s nonproliferation logic. A five-year freeze is operationally meaningless given that Iran can reconstitute enrichment capacity within months of expiry. A twenty-year freeze pushes the problem past Trump’s political relevance but not past Saudi Arabia’s nuclear timeline — KACARE’s 16-reactor program extends to 2040, fourteen years from now. A permanent ban is not achievable through negotiation with an Iranian government whose supreme leader has been absent for 45 days and whose IRGC commanders have demonstrated repeatedly that they will override any commitment the foreign ministry makes.

For Saudi 123 Agreement negotiations, the moratorium duration produces a specific and calculable asymmetry. If Iran accepts a 20-year freeze, it retains the legal right to enrich after that period — meaning Washington will have paid $20 billion to rent a temporary enrichment suspension while asking Saudi Arabia to accept an enrichment framework that, while not explicitly prohibitive, carries the implicit expectation of permanent abstention. If the moratorium is five years, the asymmetry is grotesque: Iran gets $20 billion and resumes enriching in 2031, while Saudi Arabia is expected to maintain voluntary restraint indefinitely under a 123 Agreement whose congressional review window is 90 days.

| Position | Duration | Proponent | Impact on Saudi 123 |

|---|---|---|---|

| Iran’s offer | 5 years | Iranian negotiators | Makes voluntary Saudi abstention politically impossible |

| US negotiators | 20 years | VP Vance / Witkoff | Creates a ticking clock that outlasts no Saudi government |

| Trump’s demand | Permanent | President Trump | If achieved, strengthens 123 rationale — but unachievable |

| Likely compromise | 10-15 years (est.) | N/A | Validates enrichment as a negotiable, time-limited commodity |

The Foundation for Defense of Democracies, which argued in its April 15 analysis that only “permanent verified dismantlement” is sufficient, identified the core problem without drawing the Saudi conclusion: any moratorium short of permanent creates what it called a “sunset trap” — the same structural flaw hawks attributed to the JCPOA. That the same administration is building the same sunset into a deal it claims is superior to the JCPOA is an irony that requires no editorial commentary. The dates speak.

The UAE Domino No One in Washington Is Discussing

The 2009 US-UAE 123 Agreement contains an annex — the “Agreed Minute” — with a clause that permits Abu Dhabi to renegotiate its voluntary enrichment renunciation if “any other countries in the region are granted that right.” Simon Henderson, Baker Senior Fellow at the Washington Institute for Near East Policy, has identified this clause as the structural domino that a Saudi enrichment concession or an Iran enrichment deal could activate.

The UAE’s renunciation was voluntary and unprecedented — the so-called “gold standard” in nonproliferation circles. Abu Dhabi agreed to forgo enrichment and reprocessing in exchange for US nuclear cooperation, including the Barakah plant, which now operates four APR-1400 reactors generating 5.6 GW. The Agreed Minute escape clause was the UAE’s insurance policy: if Washington later granted enrichment rights to another regional state, Abu Dhabi’s voluntary sacrifice would become a competitive disadvantage rather than a nonproliferation credential.

The $20 billion Iran deal activates this clause through two separate mechanisms. First, if Iran retains any enrichment rights after a moratorium — five, ten, or twenty years — the clause’s condition is met: a regional country has been “granted” (or, more precisely, been paid to temporarily suspend and then permitted to resume) enrichment capability. Second, if the Saudi 123 Agreement proceeds without an explicit enrichment prohibition — which the current draft does not contain — the UAE’s relative position shifts from gold-standard partner to disadvantaged competitor that gave up rights its neighbors retained.

The cascading effect is not hypothetical. Saudi Arabia has 90,000 tonnes of recoverable uranium. The UAE’s Barakah plant imports all its fuel. If Riyadh develops domestic enrichment under a 123 Agreement that permits it, and Iran resumes enrichment after a moratorium, Abu Dhabi will face domestic and strategic pressure to invoke the Agreed Minute — not because it needs enrichment capacity, but because the political cost of being the only Gulf state that permanently surrendered a sovereign right will become untenable.

How Does This Repeat the JCPOA Gulf Exclusion?

The structural parallel to 2015 is not approximate. It is precise. The P5+1 negotiations that produced the JCPOA excluded Saudi Arabia from every stage — the secret Oman channel that began in 2012, the interim Geneva agreement of 2013, the Lausanne framework of 2015, and the final Vienna text. Saudi Arabia was not a party, could not propose amendments, was not consulted on enrichment terms, and learned of the Oman channel late.

President Obama attempted to compensate with a May 2015 Camp David summit for Gulf leaders. The meeting produced a joint statement and no treaty commitments. King Salman’s response was to send Crown Prince Mohammed bin Nayef in his place — a deliberate protocol rebuke that communicated Riyadh’s assessment of the summit’s seriousness without requiring a public statement. The $116 billion in arms sales Obama subsequently offered the Gulf states did not resolve the underlying grievance: Washington had negotiated the region’s nuclear architecture without the region’s largest state at the table.

The current round reproduces this exclusion with additional complications. Saudi Arabia is not a party to the Islamabad talks. Saudi Foreign Minister Prince Faisal bin Farhan called Iranian counterpart Araghchi on April 13 — the same day the US blockade took effect — in what amounted to a parallel channel that confirmed Riyadh’s awareness it is being structurally excluded from negotiations that will directly determine its nuclear options. The ceasefire expires April 22. The 123 Agreement’s 90-day congressional review window has not yet begun. And the $20 billion deal, if concluded, will set the enrichment precedent before Congress reviews the Saudi agreement — sequencing that gives Riyadh no mechanism to condition its 123 acceptance on the Iran deal’s final terms.

The difference from 2015 is that Saudi Arabia now has alternatives. In 2015, KACARE’s nuclear program was aspirational. In 2026, it has surveyed domestic uranium, signed MOUs with Chinese and South Korean nuclear entities, and operates under a 123 Agreement draft that its own negotiators ensured did not contain an enrichment prohibition. MBS’s 2018 statement to CBS — “if Iran developed a nuclear bomb, we will follow suit as soon as possible” — was a declaratory warning. The 123 Agreement’s enrichment-permissive language is the institutional preparation.

Saudi Arabia’s Leverage Is Larger Than Washington Admits

The conventional framing of the US-Saudi 123 Agreement treats Riyadh as the supplicant — a country that needs American nuclear technology and will accept Washington’s nonproliferation conditions to get it. This framing is outdated by approximately three years. Saudi Arabia’s nuclear leverage operates across four dimensions that the $20 billion Iran deal has made more, not less, potent.

The first is supplier competition. China National Nuclear Corporation has been surveying Saudi uranium deposits under a bilateral MOU since 2017. South Korea’s KEPCO, which built Barakah for the UAE, has actively bid on Saudi reactor contracts. Russia’s Rosatom, despite the war in Ukraine, maintains commercial nuclear relationships across the Gulf. France’s EDF has signaled interest. Saudi Arabia does not need the United States to build nuclear reactors. It needs the United States to build American reactors — a distinction that matters to Westinghouse’s order book but not to Saudi energy security.

The second is domestic uranium. The 90,000-tonne recoverable resource surveyed by the Saudi Geological Survey, in cooperation with CNNC, transforms Saudi Arabia from a fuel importer to a potential fuel-cycle state. Under NPT Article IV, Saudi Arabia has the legal right to enrich domestically under IAEA safeguards. The 123 Agreement does not abrogate this right. It creates a bilateral framework within which the right might be exercised — or might not be, depending on what Riyadh decides, not what Washington demands.

The third is the oil-for-nuclear linkage that neither side discusses publicly. Saudi Arabia remains the world’s swing oil producer. The Trump administration needs Saudi cooperation on production levels, pricing, and the post-war supply recovery that will determine whether crude prices stabilize below or above the US consumer pain threshold. Conditioning nuclear cooperation on enrichment renunciation while simultaneously needing Saudi oil cooperation creates a negotiating dependency that runs in Riyadh’s favor, not Washington’s.

The fourth is the 2018 statement. MBS told CBS’s Norah O’Donnell: “Saudi Arabia does not want to acquire any nuclear bomb, but without a doubt if Iran developed a nuclear bomb, we will follow suit as soon as possible.” This was not an offhand remark. It was a declaratory policy statement by a head of government on American television, and it has functioned since 2018 as Riyadh’s nuclear insurance policy — a public commitment that any Iran deal leaving enrichment capability intact will trigger a Saudi response. The $20 billion deal, by accepting a time-limited moratorium rather than permanent dismantlement, keeps MBS’s conditional trigger permanently armed.

What Happens If the 123 Agreement Dies?

The 123 Agreement’s death would not be dramatic. It would be procedural — a congressional review that expires without ratification, or a Saudi decision to pursue nuclear cooperation through non-American partners who do not condition agreements on enrichment restrictions. Senator Ed Markey has already issued a statement accusing the Trump administration of “caving to the Saudis on nuclear nonproliferation” — framing that positions the agreement for a hostile congressional reception regardless of its terms.

The consequences would be structural and largely irreversible. Without a 123 Agreement, US nuclear firms — primarily Westinghouse — lose access to the largest prospective nuclear construction market in the Middle East. KACARE’s program would proceed under Chinese, South Korean, or Russian partnership agreements that do not require enrichment renunciation, do not contain UAE-style Agreed Minutes, and do not subject themselves to US congressional review. Saudi Arabia would acquire nuclear technology without American safeguards preferences, American reactor designs, or American oversight.

This outcome is not theoretical. It is the trajectory the 123 Agreement was designed to prevent — and which the $20 billion Iran deal, by establishing that enrichment capability is a temporary, purchasable commodity rather than a permanent red line, has made considerably more likely. Davenport’s warning that the 123 draft “will open the door for Saudi Arabia to acquire uranium enrichment technology or capabilities” did not anticipate that the door would be opened not by the agreement’s own terms but by a separate Iran deal that destroyed the nonproliferation logic the 123 framework depends on.

IAEA Director-General Rafael Grossi’s observation that “the widespread assumption is that the material is still there” — referring to Iran’s entombed HEU — carries a secondary implication for the 123 Agreement. If the US pays $20 billion for uranium it cannot currently verify exists in recoverable form, the transaction’s nonproliferation value is uncertain. If the nonproliferation value is uncertain, the precedent it sets for Saudi enrichment restrictions is built on unverified foundations. Riyadh’s negotiators will note the gap between what Washington is paying for and what Washington can confirm it is receiving.

The deeper risk is temporal. The 123 Agreement’s congressional review window has not begun. The Iran deal’s enrichment moratorium terms are unresolved. The IRGC has already demonstrated it will override diplomatic commitments made by Iran’s civilian government. And the ceasefire expires April 22 — four days from now — with no extension mechanism identified by any party. If the Iran deal collapses, the 123 Agreement’s enrichment ambiguity may survive. If the Iran deal closes on a time-limited moratorium, the 123 Agreement becomes a document that asks Saudi Arabia to accept permanently what Iran accepted temporarily, for payment, and may not honor.

“Saudi Arabia does not want to acquire any nuclear bomb, but without a doubt if Iran developed a nuclear bomb, we will follow suit as soon as possible.”

— Crown Prince Mohammed bin Salman, CBS 60 Minutes, 2018

The Authorization Ceiling Makes the Deal Undeliverable

Even if the financial and enrichment terms converge, the deal faces a delivery problem that the $20 billion price tag cannot solve. Iran’s authorization ceiling — the structural gap between what civilian negotiators can agree to and what IRGC commanders will implement — means any uranium transfer commitment requires ratification by authorities who have actively sabotaged the negotiating process.

Pezeshkian publicly accused SNSC Secretary Ali Akbar Ahmadian’s deputy Vahidi and Khatam al-Anbiya commander Abdollahi on April 4 of deviating from the delegation’s mandate during the Islamabad talks — the most direct acknowledgment by an Iranian president that he does not control his own nuclear negotiating team. Vahidi demanded that sanctioned IRGC figure Zolghadr join the Islamabad delegation and refused to include missile negotiations in any framework. The IRGC Navy declared “full authority to manage the Strait” on April 5 and again on April 10, while Araghchi was physically present in Islamabad attempting to negotiate its reopening.

Under Article 110 of Iran’s constitution, the president has no authority over IRGC operations. Supreme Leader Khamenei has been absent from public view for 45 days. His son Mojtaba has communicated only via audio. The FDD’s assessment that “five men are running Iran” — none of them Pezeshkian — reflects a command structure in which the person authorized to sign a $20 billion deal is not the person authorized to deliver the uranium it purchases.

For Saudi 123 Agreement calculations, the authorization ceiling compounds the precedent problem. If Washington pays $20 billion for a commitment that Iran’s civilian government cannot enforce against its own military establishment, Riyadh is being asked to calibrate its enrichment position against a deal whose implementation depends on institutions that have already demonstrated they will not comply. The nonproliferation precedent is not just time-limited — it is structurally unenforceable.

Frequently Asked Questions

What is the current status of Iran’s highly enriched uranium stockpile?

Iran holds approximately 440.9 kg of uranium enriched to 60%, last physically verified by IAEA inspectors on February 28, 2026, the day Iran terminated inspector access. The material is believed to be located in underground complexes at Isfahan, with possible additional quantities at Fordow and Natanz, where it was consolidated following US-Israeli strikes during Operation Midnight Hammer in June 2025. IAEA Director-General Grossi has stated publicly that the IAEA relies on “the widespread assumption” that the material remains in place, but has no independent verification mechanism currently available. The breakout estimate from 60% to weapons-grade assumes Iran’s IR-6 cascades remain operational — a condition the IAEA also cannot verify since February 28. If the material has degraded, been moved, or partially consumed in civilian applications since inspectors departed, the $20 billion price tag is being set against an unaudited inventory.

Has any country successfully used a cash-for-uranium exchange as a nonproliferation tool?

The closest precedent is not a cash transaction but a negotiated dismantlement. Libya’s 2003 voluntary surrender of its nuclear program to the United States and United Kingdom involved no direct financial compensation — Tripoli exchanged its weapons program for diplomatic normalization and the lifting of sanctions. Ukrainian denuclearization under the 1994 Budapest Memorandum involved security guarantees from Russia, the US, and the UK, not asset transfers. The 2015 JCPOA unfroze approximately $100 billion in Iranian assets plus a separate $1.7 billion settlement of a pre-revolutionary arms debt, but did not purchase specific nuclear material — it traded sanctions relief for enrichment limitations. The Biden administration’s 2023 $6 billion Oman/Qatar escrow transfer, restricted to humanitarian purchases as part of a hostage deal, is structurally closest to the current proposal but was one-third the size and did not involve uranium transfer. The $20 billion proposal would be the first direct asset-for-fissile-material exchange in nonproliferation history.

Can Saudi Arabia legally enrich uranium under international law?

Yes. As a signatory to the Nuclear Non-Proliferation Treaty, Saudi Arabia retains the right under NPT Article IV to develop nuclear energy for peaceful purposes, including uranium enrichment, provided it operates under IAEA safeguards. The pending US-Saudi 123 Agreement does not abrogate this right. Its draft language monitors enrichment activity without prohibiting it — an architecture Saudi negotiators deliberately preserved by rejecting explicit prohibition language Washington sought during earlier negotiating rounds. The distinction between what the 123 Agreement actually requires and what Washington implicitly expects is the central tension the $20 billion Iran deal has now forced into the open: one party is paying $20 billion to temporarily halt enrichment; the other is expected to halt it voluntarily, permanently, and for free.

What is the UAE Agreed Minute and why does it matter for this deal?

The Agreed Minute is an annex to the 2009 US-UAE 123 Agreement containing a renegotiation clause: if “any other countries in the region are granted” enrichment rights, the UAE may seek to renegotiate its voluntary enrichment renunciation. The clause was the UAE’s insurance against competitive disadvantage — an acknowledgment that Abu Dhabi’s “gold standard” renunciation was conditional on regional symmetry. Henderson and former IAEA Deputy Director-General Olli Heinonen have identified this clause as the mechanism through which a Saudi enrichment concession or an Iran enrichment deal could trigger a cascade of renegotiations across Gulf nuclear partnerships. The $20 billion deal threatens to activate the clause twice: once if Iran retains post-moratorium enrichment rights, and again if Saudi Arabia proceeds with enrichment under a 123 Agreement that does not prohibit it.

Why did Trump attack the JCPOA’s financial terms if his deal uses the same mechanism?

Trump called the JCPOA “catastrophic” in part because of its financial provisions — the unfreezing of an estimated $100 billion-plus in Iranian assets and a separate $1.7 billion cash settlement. His specific objections included the assertion, repeated throughout his 2016 campaign and first term, that the US “gave Iran $150 billion” (a figure that combined unfrozen assets with the cash settlement and was disputed by independent analysts). The current $20 billion proposal uses the identical mechanism — unfreezing sovereign assets held in foreign jurisdictions — from a different pool (Chinese-held rather than broadly distributed). CNN’s April 17 headline captured the parallel directly: “Trump administration considers unfreezing $20 billion in Iranian assets after lambasting Obama for a similar move.” The administration has not publicly addressed the structural equivalence between the two transactions, and Trump’s Truth Social assertion that “no money will change hands” contradicts reporting from Axios, which his own officials briefed.

Despite Trump’s public assertion that Iran had agreed to surrender its enriched uranium, Bloomberg’s reporting and Iran’s Foreign Ministry both subsequently contradicted that framing. The gap between presidential claims and the actual negotiating position is documented in Trump Says Iran Will Hand Over “Nuclear Dust.” Bloomberg Says Deal Is in Limbo, which confirms the nuclear issue remained unresolved at the time of publication.