JEDDAH — Ali Akbar Velayati, the man who has advised Iran’s Supreme Leader for three decades, announced on April 20 that the Resistance front now treats Bab el-Mandeb exactly as it treats Hormuz — a strait to be weaponized at will. Every major outlet covered the threat as a shipping story, a global trade disruption, a supply-chain headache for European importers. They missed the target. Bab el-Mandeb is not primarily a shipping story. It is the threat that breaks Saudi Arabia’s war economy.

The kingdom’s entire fiscal survival since the effective closure of the Strait of Hormuz depends on a single workaround: pumping crude through the 1,200-kilometre East-West Pipeline to the Red Sea port of Yanbu, then loading tankers that sail south through Bab el-Mandeb to reach Asian buyers. If Iran and its Houthi partners restrict that second chokepoint — even partially, even for weeks rather than months — the arithmetic of Saudi state solvency collapses. SAMA reserves are already draining at $17 billion a month, Brent sits below the kingdom’s fiscal break-even, and the pipeline itself cannot push enough oil through Yanbu’s terminals to replace what Hormuz once carried. Iran does not need to close Bab el-Mandeb. It just needs to make it expensive enough that the last corridor stops paying for itself.

Table of Contents

- Velayati’s Declaration and the Dual-Chokepoint Doctrine

- What Is Bab el-Mandeb and Why Can’t the Navy Simply Keep It Open?

- The Pipeline Works — The Port Doesn’t

- How Fast Do Saudi Reserves Drain Under a Dual Blockade?

- What Can the Houthis Actually Do at Bab el-Mandeb?

- Jeddah’s Other Vulnerability: Food

- The 1973 Precedent That Wasn’t

- Why Iran Waited Until Now

- Can Saudi Arabia Survive a Two-Strait War?

- Frequently Asked Questions

Velayati’s Declaration and the Dual-Chokepoint Doctrine

Velayati’s statement on April 20 was not a casual threat delivered through an intermediary or leaked by an unnamed official to a sympathetic outlet. It was a formal declaration carried simultaneously by PressTV, CNN, and Fox News, delivered by a figure who has served as senior adviser to the Supreme Leader since 1997 and as foreign minister for sixteen years before that. “The unified command of the Resistance front views Bab al-Mandeb as it does Hormuz,” Velayati said. “If the White House dares to repeat its foolish mistakes, it will soon realize that the flow of global energy and trade can be disrupted with a single move.” The language was calibrated for attribution — not deniable, not ambiguous, not conditional in any way that would allow Washington to pretend it hadn’t been said.

The timing matters as much as the words. Velayati spoke two days after the ceasefire’s nominal expiry on April 22, hours after Trump’s social media posts derailed the latest nuclear text, and exactly one week after the US naval blockade of Iranian ports went into full effect. Mohammad Bagher Ghalibaf, the Parliament Speaker and former IRGC Aerospace Force commander, had already telegraphed the move on April 3 when he posted a single rhetorical question to social media: “What share of global oil, LNG, wheat, rice, and fertilizer shipments transits the Bab-el-Mandeb Strait?” It was the kind of question that answers itself — roughly 12-15 percent of global trade, depending on how you count, and approximately 25 percent of the world’s oil and gas supply when combined with Hormuz, according to Al Jazeera and Time.

What Velayati formalized is what Iranian strategic thinkers have discussed since the war’s first week: the two-chokepoint doctrine, in which Hormuz and Bab el-Mandeb function as a single system rather than two separate pressure points. Tasnim News, the IRGC-affiliated outlet, had already framed the logic in March, quoting an unnamed military source who warned that “if the Americans intend to take action regarding the Strait of Hormuz, they should be careful not to add another strait to their challenges.” The Houthis’ Abdul-Malik al-Houthi confirmed on March 29 that his group was “ready to act and is coordinating with Iran,” calling a Bab el-Mandeb blockade a “key option.” Iran’s strategy has never been to close one chokepoint. It has been to make one closure intolerable by threatening the bypass route through the other.

What Is Bab el-Mandeb and Why Can’t the Navy Simply Keep It Open?

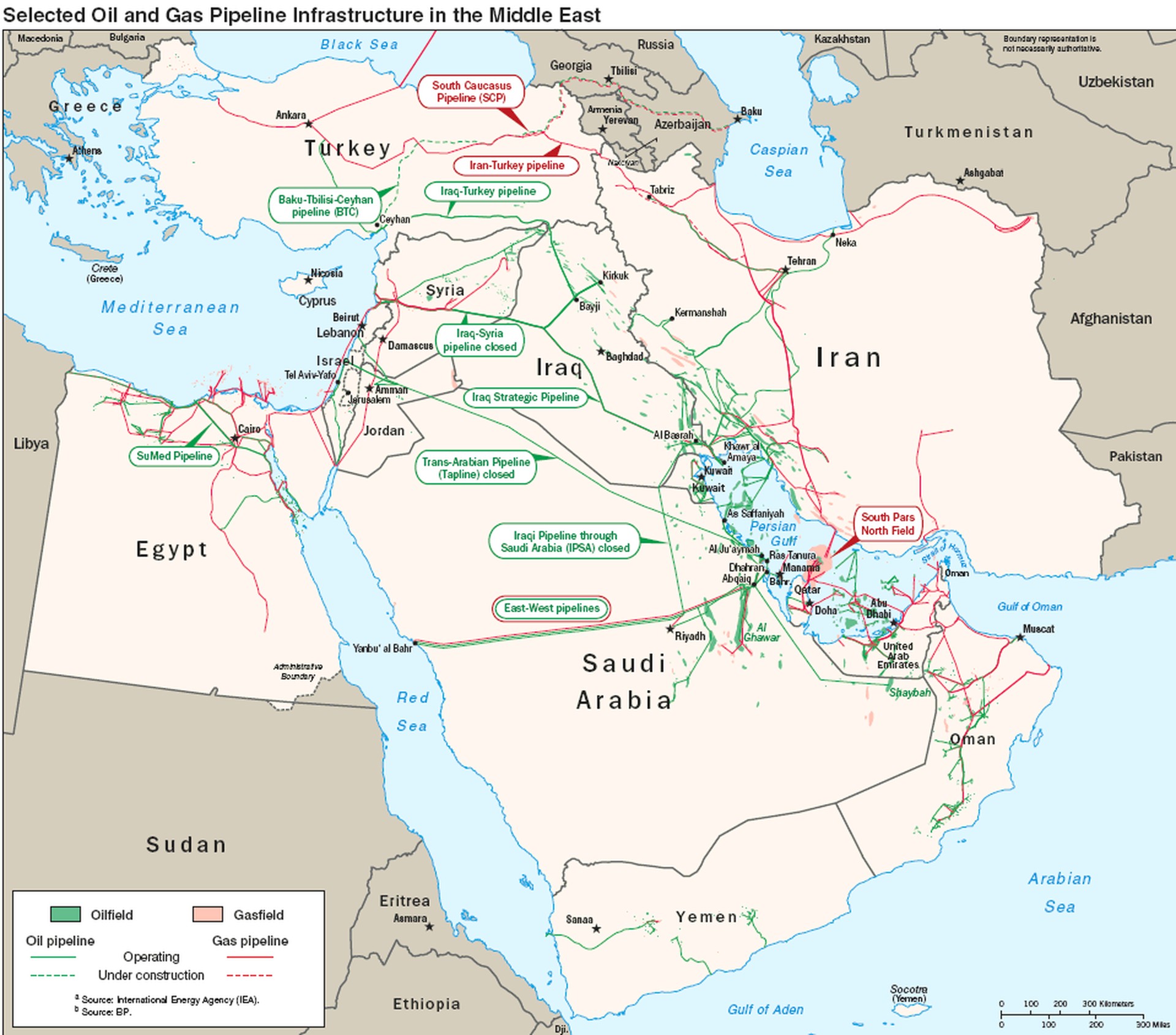

Bab el-Mandeb — Arabic for “Gate of Tears” — is a 29-kilometre gap between Yemen and Djibouti at the southern entrance to the Red Sea. Perim Island, controlled by Yemen, divides it into two channels: a 16-mile western passage roughly 650 feet deep that carries international shipping, and a two-mile eastern channel too shallow and narrow for commercial traffic. Before the Houthis began their campaign in November 2023, approximately 9 million barrels of oil per day transited the strait. That figure has since collapsed to 4.1-4.2 million bpd — a 50 percent reduction achieved without a single day of full physical closure, according to EIA data compiled by RFERL.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The US Navy cannot simply keep Bab el-Mandeb open because the Houthis proved in 2024 that you do not need to close a strait to shut it down. You need to make the insurance unaffordable. Hapag-Lloyd already charges a war-risk surcharge of $1,500 per TEU and $3,500 per reefer container for Arabian Gulf routes, as reported by The National and Al Jazeera in March. The majority of the world’s major carriers rerouted via the Cape of Good Hope starting in late 2023, adding 10-15 days per voyage. Elisabeth Kendall of Cambridge University told Al Jazeera in early April that simultaneous restrictions on both Hormuz and Bab el-Mandeb would create a “nightmare scenario” that could “disrupt, if not cripple, trade toward Europe.” Nabeel Khoury, a former US diplomat, described a full Houthi blockade as their “red line weapon of choice if fully entering the conflict.”

The geographic reality compounds the naval challenge. No single state commands both shores of Bab el-Mandeb — the western channel falls in a zone of Yemeni and Djiboutian jurisdictional overlap — which means full physical interdiction would require confronting Djibouti, home to military bases operated by the US, France, China, Japan, and Italy. The IISS assessed the Iran-Houthi relationship as “a partnership rather than a direct command structure,” but concluded that “if Iran were to put significant pressure on them, there is the chance that they could do what they did in 2024, which is effectively close the strait.” What the Houthis demonstrated in 2024, against a concerted US-UK naval response, is that closing a strait commercially is far easier than closing it physically — and far harder for a navy to prevent.

The Pipeline Works — The Port Doesn’t

Saudi Arabia’s East-West Pipeline, running 1,200 kilometres from Abqaiq in the Eastern Province to Yanbu on the Red Sea coast, is the engineering achievement that was supposed to make Hormuz irrelevant. Before the war it carried a leisurely average of roughly 750,000 bpd. Since Hormuz closed, Aramco has pushed it to its full 7-million-bpd design capacity — a technical success that, according to Argus Media and Bloomberg, represented the fastest ramp-up in the pipeline’s history. When an Iranian drone struck a pumping station on April 9, throughput dropped 700,000 bpd; engineers restored it within three days. The pipeline works. The problem is what happens at the other end.

Yanbu’s combined crude export terminals — North and South — can load approximately 5 million bpd of crude oil. Add refined products at roughly 900,000 bpd and the total Red Sea export ceiling reaches approximately 5.9 million bpd, per Argus Media’s terminal-capacity data. Saudi Arabia’s pre-war Hormuz crude throughput alone was 7-7.25 million bpd. The gap — at least 2 million bpd of crude that the pipeline can carry but Yanbu cannot ship — is structural, physical, and permanent short of years of terminal construction. No competing outlet has identified this distinction between pipeline capacity and terminal-loading ceiling. The pipeline’s 7 million bpd figure appears in every analysis; the port’s 5 million bpd bottleneck appears in almost none.

This is the number that turns Iran’s Bab el-Mandeb threat from a shipping disruption into an existential fiscal problem. Saudi Arabia was already exporting at a volume 2 million bpd below its pre-war capacity before anyone mentioned the Red Sea. If Houthi activity reduces Yanbu’s effective throughput by even 1-2 million bpd — through insurance costs, route diversions, or direct attacks on laden tankers in the southern Red Sea — the kingdom’s export capacity drops to levels that cannot fund the government, the military, the Vision 2030 programme, or the sovereign wealth fund’s $71 billion in committed disbursements. The IEA already called the March production collapse — 7.25 million bpd versus February’s 10.4 million — “the largest disruption on record.”

How Fast Do Saudi Reserves Drain Under a Dual Blockade?

The fiscal mathematics require no speculation — only arithmetic applied to published figures. The IMF’s central-government fiscal break-even for Saudi Arabia is $86.60 per barrel. Bloomberg Economics’ PIF-inclusive estimate, which accounts for the sovereign wealth fund’s $71 billion in committed disbursements across NEOM, the Entertainment Authority, Qiddiya, and the Diriyah Gate, runs between $108 and $111 per barrel. Brent crude sits below $95 as of April 22. WTI closed at $89.33. Both prices are well below the PIF-inclusive threshold that determines whether the Saudi state can meet its total obligations.

SAMA’s foreign reserves stood at $434 billion in February 2026, down from $451 billion in January — a $17 billion monthly drawdown that predates the worst fiscal impact of the war, which began registering in March and April billing cycles. Goldman Sachs estimates the kingdom’s war-adjusted 2026 fiscal deficit at 6.6 percent of GDP, double the official forecast of 3.3 percent. Goldman projects the actual deficit at $80-90 billion versus the government’s published $44 billion figure. At the current trajectory — and this assumes no further deterioration in export volumes or oil prices — Saudi Arabia would hit the informal rating-agency floor of approximately $350 billion in reserves within 12 months of the February baseline. That floor is not a number picked at random; it is the level below which sovereign credit-rating agencies have historically signalled downgrades for Gulf states, and the level at which the riyal’s dollar peg comes under sustained speculative pressure.

| Metric | Pre-War (Feb 2026) | Current (Apr 2026) | Dual-Blockade Scenario |

|---|---|---|---|

| Crude production (bpd) | 10.4M | 7.25M (IEA, March) | ~6-7M (constrained by demand) |

| Crude export capacity via Hormuz | 7-7.25M bpd | ~0 (blockade) | ~0 |

| Yanbu crude loading ceiling | ~750K bpd (avg utilisation) | ~5M bpd (max) | 3-4M bpd (Houthi disruption) |

| Brent ($/barrel) | ~$80 | <$95 | $110-115 (JP Morgan +$20 estimate) |

| PIF-inclusive break-even | $108-111/bbl | $108-111/bbl | $108-111/bbl |

| SAMA reserves | $451B (Jan) | $434B (Feb) | ~$350B floor in 10-12 months |

| Goldman deficit estimate | — | $80-90B (6.6% GDP) | $100B+ (editorial estimate) |

JP Morgan has estimated that a Bab el-Mandeb disruption alone could add $20 per barrel to oil prices, according to ABC News. On the surface, that should help Saudi Arabia — higher prices mean higher revenue per barrel exported. But the interaction between price and volume is where the trap closes. A $20 price spike caused by Bab el-Mandeb disruption would push Brent toward $115, above the fiscal break-even, but only if Saudi Arabia can actually export enough barrels at that price. If Houthi activity reduces Yanbu throughput from 5 million to 3-4 million bpd of crude, the kingdom loses 1-2 million bpd in volume. At $115 per barrel, that is $115-230 million per day in lost revenue — $42-84 billion annualised — more than enough to overwhelm the benefit of higher prices on the barrels that do get through. The price spike helps everyone who can still export. Saudi Arabia, locked into a single corridor under threat, may not be one of them.

What Can the Houthis Actually Do at Bab el-Mandeb?

The Houthi arsenal is no longer a matter of intelligence estimates leaked to sceptical journalists. It has been operationally demonstrated across eighteen months of sustained campaign against commercial shipping. Anti-ship cruise missiles, ballistic missiles with Iranian-supplied terminal guidance, underwater explosive drones, loitering munitions, explosive-laden small boats, and — in several documented cases — commercial vessels repurposed as drone-launch platforms have all been deployed against targets transiting the southern Red Sea and Gulf of Aden. The Houthis’ deputy information minister has stated on the record that his forces are “in joint coordination with our brothers in Iran, Lebanon, and Iraq,” with IRGC personnel present in Yemen “supervising intelligence, drone and missile capacities,” as reported by Middle East Monitor and the Times of Israel.

What made the 2023-2024 Houthi campaign so effective was its targeting logic. The Houthis did not need to sink ships — they needed to raise insurance premiums to the point where rerouting via the Cape of Good Hope became commercially rational despite adding 10-15 days to every voyage. That calculus flipped for the majority of global container lines within weeks of the campaign’s start, and it has not flipped back. The 2024 campaign, critically, was conducted against a standing US-UK naval task force (Operation Prosperity Guardian) that failed to restore commercial confidence despite striking Houthi launch sites repeatedly. A Houthi senior military commander, Abed al-Thawr, told PressTV in March: “We will use the trump card of closing the Bab al-Mandab Strait to American and Israeli ships.”

The difference between the 2024 campaign and what Velayati is now signalling is scope. In 2024, the Houthis targeted vessels linked to Israel, the US, and the UK — a selective campaign that allowed most commercial traffic to continue, albeit at higher cost and risk. Velayati’s language — “the flow of global energy and trade can be disrupted with a single move” — implies an indiscriminate posture: all traffic, including Saudi-laden tankers departing Yanbu southbound for Asian markets. PressTV’s own framing on April 3 described the Houthi posture as aligned with Iranian strategic signalling, not an independent decision by Sanaa. If the scope expands from Israeli-linked vessels to all commercial traffic, the insurance market would effectively shut Bab el-Mandeb overnight — precisely as it has done, in practice, for Hormuz.

Jeddah’s Other Vulnerability: Food

The oil export problem dominates the strategic conversation, but Saudi Arabia’s Red Sea exposure extends far beyond crude. Jeddah Islamic Port handles 130 million tonnes of cargo annually and 7.5 million TEU of container traffic, making it the kingdom’s primary maritime gateway, according to Janes’ port analysis. Saudi Arabia imports more than 80 percent of its food. The overwhelming majority of that food arrives by sea, and the overwhelming majority of seaborne food imports transits through Jeddah — which sits squarely on the Red Sea coast, north of Bab el-Mandeb, dependent on the same strait that Velayati has now declared equivalent to Hormuz.

A disruption to Bab el-Mandeb does not merely threaten Saudi oil exports heading south. It threatens food imports heading north. Rice from South and Southeast Asia, wheat from Australia and India, processed food from East Africa — all of it enters the Red Sea through Bab el-Mandeb. The alternative, routing food shipments around the Cape of Good Hope and up through the Suez Canal, adds weeks and cost to every cargo, assuming the Suez Canal itself remains unaffected by the broader regional instability. Saudi Arabia has strategic food reserves, but they were designed for short-term disruptions, not for a sustained blockade of the kingdom’s primary import corridor during a war that has already consumed 86 percent of its PAC-3 interceptor stockpile and fractured its GCC alliance structure.

The war-risk surcharges already in place tell part of the story. Hapag-Lloyd’s $1,500 per TEU for Arabian Gulf routes, imposed after the Hormuz effective closure, would likely increase further — or extend to Red Sea routing — if Bab el-Mandeb escalates from its current degraded state to full disruption. Container shipping operates on margins thin enough that surcharges at that level alter trade flows, delay orders, and force importers to seek alternative suppliers. For a nation that overwhelmingly depends on seaborne food imports during a war, with 1.2-1.5 million Hajj pilgrims arriving in the coming weeks, the food corridor is not a secondary concern. It is the concern that MBS cannot outsource to any ally.

The 1973 Precedent That Wasn’t

Iran’s apologists and several Western analysts have invoked the 1973 Yom Kippur War as proof that Bab el-Mandeb can be effectively closed. The comparison is instructive mainly for what it reveals about the limits of historical analogy. During the October 1973 war, Egyptian and South Yemeni warships conducted targeted interdiction of vessels bound for the Israeli port of Eilat — a narrow, specific campaign against a single destination. They did not attempt to close the strait to all traffic, and the interdiction was lifted on November 18, 1973, after the ceasefire. As Horn Review noted in an April 2 analysis: “No full closure of Bab el-Mandeb has ever occurred — not during the 1973 war, not during subsequent decades of conflict in Yemen, not during the current Houthi campaign.”

The 1973 comparison actually strengthens the case for Iran’s current strategy rather than weakening it. Egypt and South Yemen achieved their objective — pressuring Israel via Eilat — with targeted interdiction, not total closure. The Houthis demonstrated in 2024 that targeted interdiction of commercial shipping, backed by a credible missile and drone threat, can reduce throughput by 50 percent without ever physically sealing the waterway. Iran does not need a historical precedent for full closure because full closure is not the strategy. The strategy is commercial disruption at a scale sufficient to choke Saudi export volumes below the fiscal break-even — a threshold that, thanks to the structural gap between pipeline capacity and Yanbu’s terminal ceiling, is already uncomfortably close.

Why Iran Waited Until Now

Velayati’s April 20 declaration was not impulsive. The sequencing reveals a strategy that has been assembling itself across the war’s 53 days, each move creating the conditions for the next. Iran first established control over Hormuz through the IRGC Navy’s “full authority” declaration, forcing Saudi Arabia onto the East-West Pipeline as its sole export route. Then IRGC drones struck a pipeline pumping station on April 9, demonstrating that even the bypass was vulnerable — and simultaneously revealing, by the speed of the repair, exactly how dependent the kingdom had become on that single corridor. The US blockade of Iranian ports, effective April 13, provided the casus belli: Iran could now frame Bab el-Mandeb escalation as a proportional response to American economic warfare, not unprovoked aggression against neutral shipping.

The ceasefire’s April 22 expiry date — today — completes the strategic logic. With the ceasefire lapsing, the already tenuous legal and diplomatic restraints on Iranian proxy operations in Yemen dissolve. Ghalibaf cannot negotiate the Hormuz question because the IRGC controls it outside the civilian government’s authority; by the same token, Velayati’s invocation of the “unified command of the Resistance front” signals that Bab el-Mandeb decisions will be taken by the same military-intelligence apparatus that has overridden every diplomatic initiative since February 28. Iran waited until the moment when all three conditions aligned: Hormuz closed, the pipeline at maximum dependence, and the legal framework for restraint expired.

The US blockade, ironically, may have accelerated the threat it was designed to deter. By cutting off Iranian ports, Washington gave Tehran the one thing it lacked: a symmetric grievance. Iran can now tell every non-aligned capital — Beijing, Delhi, Islamabad, Ankara — that its Bab el-Mandeb posture is retaliatory, a blockade answered with a blockade. The Foundation for Defense of Democracies estimated the US blockade’s damage to Iran at $435 million per day. Saudi Arabia’s exposure to a Bab el-Mandeb disruption, measured in lost export revenue alone, would exceed that figure within the first week.

That grievance became official diplomatic vocabulary on April 20, when Foreign Minister Araghchi formally labelled the US naval blockade an “act of war,” cancelled Iran’s participation in a second Islamabad round, and aligned Tehran’s diplomatic framing with the IRGC’s operational posture — closing the authorization ceiling gap that had kept Iran’s civilian and military voices on separate tracks.

Can Saudi Arabia Survive a Two-Strait War?

The honest answer is: not at current prices, not at current export volumes, and not for long. Saudi Arabia’s March production of 7.25 million bpd — already down 30 percent from February’s 10.4 million — represents the kingdom producing into a corridor that can ship, at maximum, 5.9 million bpd. The remaining 1.35 million bpd either goes into storage or feeds domestic refineries. If Bab el-Mandeb disruption reduces Yanbu’s effective throughput to 3-4 million bpd, Saudi Arabia would be exporting at roughly 40 percent of its pre-war capacity. Kpler data already showed Asia-bound Saudi exports down 38.6 percent in March, before any Bab el-Mandeb escalation.

The kingdom has three theoretical options, and none of them solve the problem on the timeline the reserves require. First, it could negotiate directly with Iran for Red Sea passage — but Pezeshkian’s own admission that the IRGC overrides civilian diplomacy means there is no reliable interlocutor, and Saudi Arabia’s FM Faisal calling Araghchi on blockade day (April 13) suggests Riyadh already understands this. Second, it could request US naval escort for Yanbu-laden tankers through Bab el-Mandeb — but Operation Prosperity Guardian’s failure to restore commercial insurance confidence in 2024 suggests that naval presence does not solve the insurance problem, and the US Navy is already stretched across both chokepoints simultaneously. Third, Saudi Arabia could attempt to build overland export capacity through pipelines to Oman’s Arabian Sea coast or Jordan’s Aqaba port, bypassing both straits entirely — but those projects would take years, not months, and the reserves are draining now.

“The unified command of the Resistance front views Bab al-Mandeb as it does Hormuz. If the White House dares to repeat its foolish mistakes, it will soon realize that the flow of global energy and trade can be disrupted with a single move.”— Ali Akbar Velayati, senior adviser to the Supreme Leader, April 20, 2026

The structural trap is this: higher oil prices, normally Saudi Arabia’s greatest strategic asset, become irrelevant when the barrels cannot reach the market. A 20 percent price increase on 40 percent fewer exported barrels leaves the kingdom worse off, not better — and Iran has found precisely that configuration. The indefinite ceasefire that Trump proposed would freeze this configuration in place — Saudi Arabia exporting at diminished capacity through a threatened corridor, burning reserves at $17 billion a month, while Iran suffers the blockade’s $435 million daily cost but retains the option to escalate at Bab el-Mandeb whenever the pressure becomes useful.

The question that Riyadh will not answer publicly — and that no allied capital has yet asked on the record — is what happens when the reserves hit $350 billion. The riyal peg, fixed at 3.75 to the dollar since 1986, has survived every oil crash since its inception because SAMA always held enough reserves to defend it. A speculative attack on the peg, triggered by visible reserve depletion in a dual-blockade scenario, would force Saudi Arabia to choose between defending the currency (by selling reserves faster) and funding the war (by spending those same reserves on arms, food imports, and PIF commitments). That choice, if it arrives, will not be made by Mohammed bin Salman alone. It will be made by the bond market, the rating agencies, and the currency traders who watch SAMA’s monthly reserve disclosures like a countdown clock.

Iran’s Bab el-Mandeb threat is, in the end, a bet on time — a bet that Saudi Arabia’s reserves will run out before Iran’s tolerance for the US blockade does, before the Houthis’ arsenal depletes, before Washington finds a diplomatic formula that satisfies an IRGC command structure that has overridden every formula offered so far. The 1973 comparison, the shipping-lane analysis, the naval-capability assessments — none of them capture what is actually at stake. What is at stake is whether Saudi Arabia can remain solvent while exporting through a corridor that its principal adversary can degrade at will, at prices below its fiscal needs, with reserves falling at a rate that gives it roughly a year before the floor gives way. Velayati, who has watched Gulf power dynamics longer than most of his counterparts have been alive, appears to believe the answer is no.

Frequently Asked Questions

Has Bab el-Mandeb ever been fully closed to shipping?

No. Horn Review’s comprehensive analysis confirms that no full closure has ever occurred — not during the 1973 Yom Kippur War (when Egyptian and South Yemeni warships conducted targeted interdiction against Israel-bound vessels only, lifted November 18, 1973), not during the North-South Yemen civil wars, not during the Saudi-led intervention from 2015, and not during the current Houthi campaign that began in November 2023. The Houthi achievement was commercial disruption through risk escalation: throughput fell 50 percent without any physical seal of the waterway, which is what makes the tactic so difficult for navies to counter and so relevant to the current Saudi export corridor.

Could higher oil prices from a Bab el-Mandeb crisis actually help Saudi Arabia?

Only if the kingdom can maintain export volume, which is precisely what the dual-chokepoint strategy is designed to prevent. The interaction between Saudi Arabia’s Yanbu terminal ceiling (5 million bpd crude maximum) and the Houthi threat to reduce that further creates an asymmetric trade-off: a 20 percent price increase paired with a 30-40 percent volume reduction leaves net revenue lower, not higher. By contrast, producers who export through unaffected routes — the US, Brazil, Guyana, Canada — capture the price benefit with no volume penalty, which is why Saudi Arabia’s competitive position deteriorates even as headline crude prices rise in response to the disruption the kingdom itself is suffering.

What is the difference between pipeline capacity and Yanbu loading capacity?

The East-West Pipeline can carry 7 million bpd from Abqaiq to Yanbu — its design maximum, now fully utilised. But Yanbu’s combined North and South crude terminals can physically load only approximately 5 million bpd onto tankers, with an additional 900,000 bpd in refined products for a total Red Sea ceiling of 5.9 million bpd (Argus Media). The 1.1-million-bpd gap between what the pipe delivers and what the port can ship is a physical constraint — berth space, loading arms, draft depth — that cannot be resolved without multi-year terminal expansion. This distinction, absent from virtually all competing analysis, is what makes the Saudi bypass structurally incomplete even before any Bab el-Mandeb disruption.

How long could Saudi Arabia sustain current reserve drawdowns?

At the February 2026 drawdown rate of $17 billion per month — which predates the full fiscal impact of March-April production losses — SAMA’s reserves of $434 billion would reach the informal rating-agency floor of approximately $350 billion within 12 months, or roughly by February-March 2027. This estimate assumes the drawdown rate does not accelerate, which is optimistic given that Goldman Sachs’ war-adjusted deficit of 6.6 percent of GDP ($80-90 billion) implies monthly draws could increase as deferred costs (OPEC+ quota obligations, PIF disbursements, Sadara and SABIC liabilities, arms procurement) come due in the second half of 2026. The riyal peg’s defence would consume additional reserves if speculative pressure builds as the floor approaches.

Why can’t the US Navy protect Saudi tankers through Bab el-Mandeb?

Operation Prosperity Guardian — the US-UK naval task force deployed to the Red Sea in December 2023 — conducted sustained strikes against Houthi launch sites throughout 2024 without restoring commercial shipping confidence or reducing insurance premiums to pre-disruption levels. The fundamental problem is that naval escorts protect individual vessels but cannot eliminate the distributed, mobile, land-based launch infrastructure that the Houthis operate across western Yemen. Insurance underwriters price risk based on the threat environment, not the escort presence, which is why premiums remained elevated throughout the 2024 campaign despite continuous naval operations. With the US Navy now simultaneously committed to the Hormuz blockade and carrier operations across the broader theater, the capacity to mount a second sustained escort operation through Bab el-Mandeb would require either redeploying assets from the Hormuz mission or surging additional carrier groups — neither of which is operationally straightforward during an active regional war.

The IRGC’s escalation of its Hormuz enforcement regime — from administrative rejections to physical seizure of European-linked vessels — is documented in IRGC Seizes Two Ships in 72-Hour Retaliation Cycle, which traces the fourth documented tit-for-tat cycle and its implications for the remaining exit corridors analysed here.

Saudi Arabia’s strategic response to the dual-chokepoint threat described here — accelerating a northern rail corridor through Jordan and Syria to Turkish Mediterranean terminals — is examined in full in The Hejaz Railway Reversed: Saudi Arabia’s Northern Rail Corridor as Wartime Chokepoint Bypass.

The Custodian title trap that makes Saudi Arabia unable to cancel Hajj even as air defence stocks fall below 15 percent of pre-war levels — and as the ceasefire expired on April 22 itself — is examined in full in The Hajj Opens Under an Expired Ceasefire: MBS’s Custodian Title Becomes a Trap.