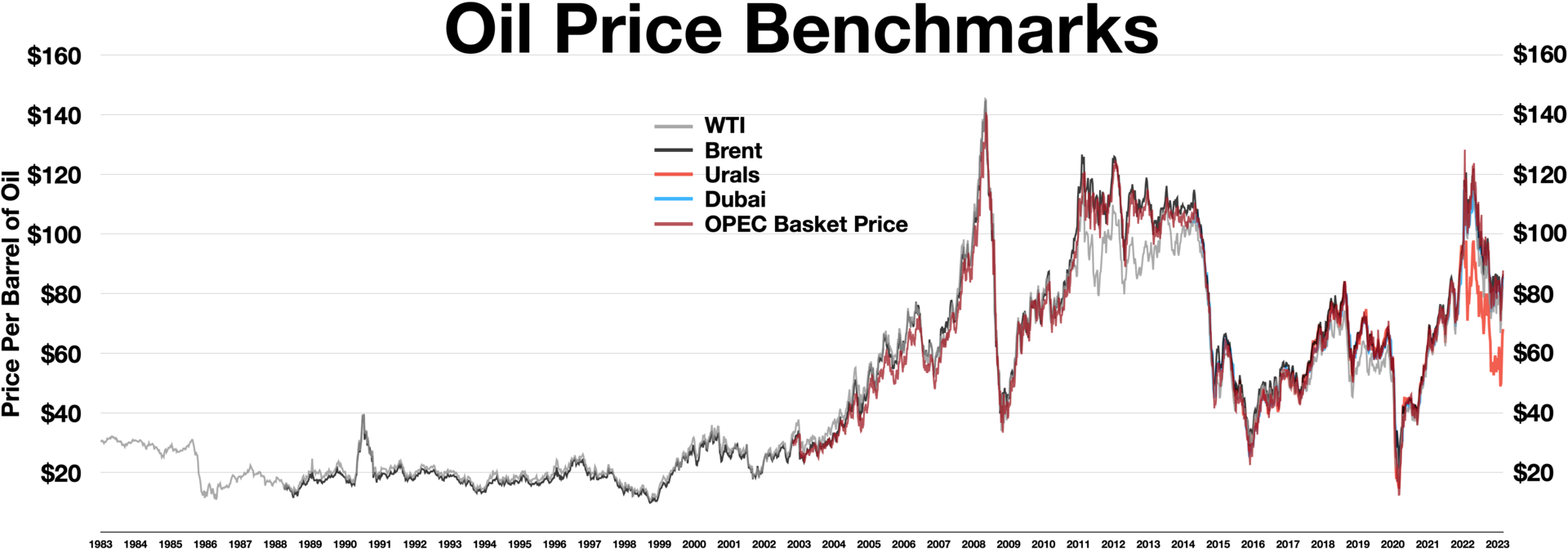

DHAHRAN — On the morning of June 12, U.S. forces shot down two Iranian one-way attack drones over the Strait of Hormuz, fired at commercial vessels attempting transit. Within the same news cycle, Donald Trump told ABC News a ceasefire deal could be signed “as early as this weekend, possibly in Europe.” Brent crude fell 3.83% to $84.35 a barrel on the headline — an eight-week low.

Iran’s foreign minister posted on X that “there is NO ‘agreement’” on anything. Sadara Chemical Company, all 26 Jubail units offline since March with zero revenue and $3.7 billion in guaranteed debt, watched its restructured grace period tick toward expiration on Monday, June 15 — indifferent to whatever Trump signs in whichever European capital.

On June 12, the White House named Vice President JD Vance to sign the MOU in Geneva on Sunday, June 14, and four C-17 transport aircraft departed for Europe carrying advance delegation equipment — while Iran’s Foreign Ministry denied any approved text existed and Fars News Agency reported that no MOU had been authorized by the Supreme Leader.

Saudi Arabia now operates under two calendars. The diplomatic calendar promises resolution “this weekend.” The operational calendar — drone attacks on commercial shipping, Hormuz carrying 2% of its pre-war traffic, war risk premiums at 60 times pre-crisis rates — runs on physics, actuarial tables, and creditor syndicate patience. Only one of these calendars has jurisdiction over Sadara’s $3.7 billion, and it is not the one controlled from Washington.

Table of Contents

- What Did Trump Promise on ABC News?

- What Happened Over Hormuz This Morning?

- Why Is Iran Denying the Deal While Firing on Ships?

- Why Can’t a Ceasefire Reopen the Strait?

- What Does $84 Oil Cost Saudi Arabia?

- Sadara — Seventy-Two Hours to a Decision Aramco Cannot Delay

- Where Is Saudi Arabia in This Deal?

- Frequently Asked Questions

What Did Trump Promise on ABC News?

Trump told ABC News on June 12 that an Iran ceasefire deal could be signed “as early as this weekend, possibly in Europe,” with oil prices falling “like a rock” once signed. Iran’s foreign minister denied any agreement existed. The instrument under discussion is a non-binding MOU in which Hormuz reopening occurs 30 days after signing, not immediately.

Trump told ABC News Senior Political Correspondent Rachel Scott on June 12 that a ceasefire deal with Iran could be signed “as early as this weekend, possibly in Europe.” When Scott pressed on why this attempt would succeed where prior claims had failed, he answered with four words: “Because they’ve taken a pounding.” On whether the deal would reopen the Strait of Hormuz, the president was equally certain: “Yes, that’s part of the deal, and you’ll have oil prices dropping like a rock.”

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The instrument under discussion is a memorandum of understanding — Trump confirmed that designation himself from the Oval Office — not a treaty, not a binding agreement under international law, and not the kind of document that triggers automatic implementation timelines. Mehr News Agency, the Iranian state outlet that has published the most detailed account of the draft text, reported a 14-point structure in which the specifics diverge sharply from the president’s rhetoric. Hormuz reopening, per the draft, occurs “within 30 days” of signing — not at the moment of signing as Trump’s language implied, but a full month afterward. That 30-day clock assumes Iran ratifies the text in its current form, which as of June 12 it has not agreed to do.

Brent crude responded to the headline, not the footnote. Oil crashed through the $86.50 floor to settle at $84.35, an eight-week low, while WTI dropped below $84. The market priced in a deal that Iran’s own foreign minister was publicly denying at the same hour the price moved. Earlier this week, oil fell to $89 on a deal Saudi Arabia had not confirmed; now it has fallen further on a deal Iran has explicitly rejected, widening the kingdom’s per-barrel fiscal deficit to between $23.65 and $26.65 against the Goldman Sachs breakeven estimate of $108-111.

As of now, there is NO ‘agreement’ on any ceasefire or cessation of military operations.— Abbas Araghchi, Iranian Foreign Minister, posted on X, June 12, 2026

What Happened Over Hormuz This Morning?

U.S. forces shot down two Iranian one-way attack drones fired at commercial vessels attempting Hormuz transit on June 12. The engagement was routine enforcement of Iran’s standing shoot-on-sight order issued June 1-2. The strait carries roughly 2% of its pre-war traffic. Hapag-Lloyd has stated it is “currently refraining” from transit entirely.

U.S. forces intercepted two Iranian one-way attack drones over the Strait of Hormuz on the morning of June 12, both fired at commercial vessels attempting transit. A senior U.S. official confirmed the engagement: “It appears Iran has attempted to strike commercial ships transiting the Strait of Hormuz tonight.” Iranian state media offered a different framing — a tanker had attempted passage “without coordinating with authorities” and was fired upon until it “complied with the ban.” Both accounts confirm the same physical event: the IRGC fired on commercial shipping in the world’s most consequential energy chokepoint, and the U.S. military shot down the projectiles before they reached their targets.

The “ban” is not rhetorical. Khatam al-Anbiya, Iran’s joint forces command, declared the strait closed to unauthorized traffic and imposed a shoot-on-sight protocol in its June 1-2 operational order. The drones that U.S. forces intercepted this morning were doctrine execution — the routine enforcement of a standing military directive — not a provocation timed to embarrass diplomacy. From the IRGC’s operational perspective, any commercial vessel transiting without Iranian authorization is a legitimate target under the declared rules of engagement, and this morning’s engagement was as unremarkable as a traffic stop. RFE/RL was the only major outlet to explicitly juxtapose both events in a single headline: “US Shoots Down Two Iranian Drones Near Hormuz, As Trump Hails Impending Peace Deal.”

The cost arithmetic of Hormuz enforcement is as lopsided as any in modern warfare. Each Shahed drone costs Iran under $50,000 to manufacture and launch. Each U.S. intercept runs approximately $4 million in Gulf base defense expenditure — an 80-to-1 cost ratio that Tehran can sustain indefinitely. The strait currently carries roughly 2% of its pre-war traffic, down from approximately 21 million barrels per day to around 420,000. Hapag-Lloyd, among the world’s largest container shipping lines, has stated it is “currently refraining” from Hormuz transit entirely. The IRGC has reportedly charged some tankers up to $2 million for passage, converting a global maritime commons into a toll road under military administration.

This is the calendar that governs Saudi Arabia’s fiscal reality: not the one measured in diplomatic press conferences, but in barrels per day, intercept costs, and insurer refusals. Hormuz had no ceasefire to collapse before this morning’s drone attack. After it, the distance between what Trump promised on ABC News and what is physically happening at the strait is wider than at any point in the 105-day war.

Why Is Iran Denying the Deal While Firing on Ships?

Iran’s military and diplomatic tracks operate independently. The IRGC enforces the Hormuz closure as standing doctrine, unrelated to negotiation status. The Foreign Ministry denies premature concessions to protect leverage. Foreign Minister Araghchi posted on X that there is “NO ‘agreement.’” Tasnim told markets to apply a discount rate to Trump’s word.

Iran’s diplomatic and military tracks look contradictory only if you assume they share a destination. They do not. The IRGC enforces the declared Hormuz closure as a matter of standing operational doctrine — the drones fired this morning were not a diplomatic signal but a military routine, indistinguishable in kind from yesterday’s enforcement or last week’s. The Foreign Ministry, on a separate and parallel track, manages the international narrative: denying premature concessions, preventing market-moving confirmations that would weaken Tehran’s leverage at the table, and accusing Washington of “lawless conduct” and “changing deal text” after the framework was circulated.

Foreign Minister Araghchi’s denial on X was unambiguous and capitalized for emphasis. Spokesman Esmail Baghaei reinforced it through IRNA: “Iran has not reached a final decision regarding any agreement.” Tasnim, the IRGC-linked news agency that functions as the clearest public window into Revolutionary Guard thinking, delivered the most pointed message of the three — directed not at Washington but at the markets and governments inclined to take Trump’s word as actionable intelligence.

Until any potential understanding or agreement is officially announced by Iran, any statements from Trump on this matter should be viewed in the same light as his previous claims.— Tasnim News Agency (IRGC-linked), June 12, 2026

That final clause — “his previous claims” — does the operative work. Tehran is telling every trading desk, every insurer, and every tanker operator in the Gulf to apply a discount rate to the president’s word based on the track record of his prior announcements. The 14-point draft MOU reported by Mehr News remains actively contested, with Iran accusing Washington of adding conditions after the text was shared and of attempting to extract concessions outside the agreed framework. Whether a deal materializes this weekend or not, Tehran has built a position from which no one can credibly claim Iranian consent was given before Iran gave it — and the IRGC continues enforcing the strait closure at the chokepoint the deal is supposed to reopen, because no deal exists from Tehran’s operational standpoint until Iran says it does.

Why Can’t a Ceasefire Reopen the Strait?

Reopening Hormuz requires five sequential steps after signing: mine clearance (30 days minimum per draft MOU), lifting the U.S. naval blockade, JWC conflict-zone removal, tanker operator decisions to resume, and war risk premium normalization. The JWC requires consecutive incident-free quarterly reviews — making mid-2027 the earliest realistic reclassification date.

A ceasefire announcement does not reopen a maritime chokepoint. Between “MOU signed in Europe” and oil flowing through Hormuz at pre-war volumes, at least five sequential steps must occur, none of which can be compressed by rhetoric or executive order. Iran must physically clear mines from the strait — the draft MOU itself allocates 30 days for this process. The U.S. naval blockade must be lifted under terms both sides accept.

The Joint War Committee of Lloyd’s Market Association must remove its conflict-zone designation from the Arabian Gulf. Commercial tanker operators, each making independent corporate risk assessments, must decide to resume transit. And war risk insurance premiums must normalize to levels at which commercial shipping is economically viable rather than financially suicidal.

The JWC designated the entire Arabian Gulf a conflict zone on March 3, 2026, under JWLA-033, within 48 hours of the US-Israeli strikes that opened the war. Removing that designation requires multiple quarterly review cycles with zero maritime incidents during each period — a condition that this morning’s IRGC drone attack on commercial shipping just reset to zero. Willis Towers Watson, one of the world’s largest insurance brokers, has stated plainly that war risk rates are “unlikely to fall after ceasefire” because the insurance industry “measures in years, not press conferences.” Under the most optimistic scenario — immediate signing, immediate compliance, no further incidents — the earliest realistic JWC reclassification is mid-2027, more than twelve months away.

This creates a circular dependency that no diplomatic instrument can break. Reopening the strait requires commercial traffic to flow through it. Commercial traffic requires affordable war risk insurance. Affordable insurance requires a sustained record of incident-free transit — which cannot be established while the strait remains closed and the IRGC fires on vessels that attempt to use it. A ceasefire will not lower the premium; it merely establishes the first precondition for a multi-quarter normalization process that might, under favorable conditions and zero backsliding, eventually bring rates down. The April 8 and April 17 ceasefire announcements earlier in this war offer the relevant test case: neither produced any measurable change in operator behavior, no major shipping line resumed Hormuz transit, and no oil major rerouted cargo through the strait after either one.

The 1984-1988 Tanker War provides the closest historical precedent, and it counsels patience measured in seasons rather than weekends. Over 540 commercial vessels were struck during that conflict, and insurance normalization took months after the ceasefire was signed. That war never involved a full strait closure — only attacks on individual vessels within an otherwise functional waterway. The current situation is structurally more severe: the IRGC has declared the strait entirely closed, is enforcing the closure with live fire including this morning’s drone engagement, and has converted transit into a toll system requiring Iranian authorization and per-passage fees.

No previous Hormuz crisis has produced conditions this restrictive, and no previous resolution has been instantaneous. Trump told ABC News that oil prices would drop “like a rock” once a deal was signed. The actuarial tables that govern whether tankers actually sail through the strait operate on a timeline that has never once aligned with a president’s weekend plans.

What Does $84 Oil Cost Saudi Arabia?

Goldman Sachs estimates Saudi Arabia’s fiscal breakeven at $108-111 per barrel. Brent settled at $84.35 on June 12. The per-barrel arithmetic requires no modeling: Saudi Arabia is losing between $23.65 and $26.65 on every barrel it manages to sell, measured against the price required to balance a national budget that Goldman projects could run a deficit of SAR 300-330 billion for the full fiscal year. At current production of approximately 8 million barrels per day — down from roughly 10 million before the war disrupted Gulf export infrastructure — the daily revenue shortfall against fiscal breakeven runs between $189 million and $213 million.

The production constraint compounds the price problem and operates independently of any deal. Saudi Arabia’s East-West Pipeline routes crude to Yanbu terminals on the Red Sea, bypassing Hormuz entirely, with a throughput capacity of roughly 5 million barrels per day. But the bypass ends in a blockade zone where Houthi forces have declared a “complete and total ban” on Israeli-linked maritime navigation and where Aramco has already slashed official selling prices by $6 per barrel for Asian customers and $10 for European and Mediterranean destinations. Of the 8 million barrels Saudi Arabia currently produces, between 1.1 and 2.1 million barrels per day cannot be routed to any accessible market at all — neither through Hormuz, which is closed, nor through Yanbu, where the discount required to attract buyers in a declared war zone consumes what remains of the revenue margin.

| Milestone | Diplomatic Calendar | Operational Calendar |

|---|---|---|

| Deal signed | “This weekend” (Trump, ABC News) | “NO agreement” (Araghchi, June 12) |

| Hormuz mine clearance | Implied immediate | 30 days minimum (14-point MOU draft, Mehr News) |

| Commercial transit resumes | “Oil dropping like a rock” | 2% of pre-war volume; Hapag-Lloyd “refraining” |

| War risk premiums normalize | Not addressed | Mid-2027 at earliest (JWC/Willis Towers Watson) |

| Sadara creditor deadline | Not addressed | June 15 — Monday — 72 hours |

| Saudi fiscal breakeven | Not addressed | Requires $108-111/bbl; Brent at $84.35 |

A deal signed “this weekend” changes none of these numbers by Monday. The best-case reading of the 14-point draft — Iran begins mine clearance immediately, the JWC initiates its first quarterly review cycle, tanker operators cautiously test the water — still leaves Saudi Arabia facing a minimum of 30 additional days of full Hormuz closure, months of elevated war risk premiums that suppress tanker traffic regardless of the military situation on the surface, and a JWC reclassification process extending deep into 2027. The per-barrel deficit narrows only when physical cargo moves through insurable waters, and physical cargo does not move until insurers agree to cover it at rates that leave something resembling a margin. Oil prices moved within minutes of Trump’s words on June 12; the barrels Saudi Arabia needs to sell respond to nothing except ships in water and policies in underwriting offices.

Sadara — Seventy-Two Hours to a Decision Aramco Cannot Delay

Sadara Chemical Company’s restructured grace period expires on Monday, June 15 — 72 hours from the time of publication. All 26 of Sadara’s Jubail industrial units have been offline since late March, generating zero revenue against $3.7 billion in outstanding debt. The company’s April 2026 filing with the Saudi Exchange disclosed that it “cannot provide, at the present time, an estimate for the return to production, as this is contingent on domestic and international factors.” Those factors — a war in the Gulf, a closed strait, a national budget bleeding $189-213 million per day against breakeven — have deteriorated in every measurable dimension since April.

The guarantee structure is contractually precise and personally consequential for Aramco. The national oil company backs $2.405 billion of the debt at 65%; Dow Chemical backs $1.295 billion at 35%. The creditor syndicate spans more than 25 institutions, including HSBC, JPMorgan, and several Saudi commercial banks. No public creditor communication has been reported since Sadara’s units went offline — no restructuring proposal, no extension request, no indication of how the syndicate intends to handle a borrower with zero revenue, zero production, and a majority guarantor that has said nothing publicly about the approaching deadline.

Aramco holds approximately $53.3 billion in post-dividend cash, having paid its $21.89 billion quarterly distribution on June 9. The company could technically honor the $2.405 billion guarantee. But calling it is not a check-writing exercise — it is a public confirmation that Sadara has no viable restart path, a disclosure with immediate implications for Aramco’s credit profile, bond spreads, and the willingness of international investors to treat the company’s debt as quasi-sovereign. Sadara’s accumulated losses exceeded 100% of share capital by end-2025, before the war shut production entirely, meaning the guarantee call would be made on a company that was already technically insolvent before losing its final revenue stream.

The most probable outcome is a second restructuring: more than 25 banks asked to extend grace on a borrower producing nothing, earning nothing, and unable to name a date when either condition changes. The original grace period was restructured in March 2021 with a five-year runway that expires in three days. Whether Donald Trump signs a memorandum of understanding in Europe this weekend, the 30-day mine-clearance timeline in the draft MOU would not restore Sadara’s Jubail feedstock supply before mid-July at the earliest — and that assumes every prior step in the reopening sequence executes without a single delay, which no prior phase of this war has managed. Geneva Will Not Reopen Jubail sets out in full why the MOU’s phase one contains zero provisions affecting Sadara’s debt service or Jubail’s operating status. A separate analysis maps out the SEC and Tadawul rules that explain the regulatory silence from both guarantors as the deadline arrives.

Where Is Saudi Arabia in This Deal?

Saudi Arabia has no seat at the negotiating table and no instrument that could alter what emerges from it. Trump called Saudi Arabia an “approver” of the deal framework on Truth Social, listing the kingdom among twelve nations. Riyadh has not confirmed, denied, or commented on that designation. Saudi MOFA has issued no public statement on the Iran war during the current news cycle, maintaining a pattern of institutional silence that has persisted through the conflict’s most consequential escalations. The kingdom’s involvement, such as it exists, consists of inclusion on a consultative call with Trump and Muslim leaders — a briefing, not a seat — and it has not been invited to the June 22 Washington follow-on meeting where implementation details are expected to be discussed.

All three active mediation tracks bypass Riyadh entirely. Oman operates the formal diplomatic channel to Tehran. Pakistan runs the IRGC back-channel through Army Chief Munir’s direct correspondence with Mojtaba Khamenei. Qatar’s Tehran delegation consulted Washington before departing, not Saudi Arabia. Each channel was built on bilateral relationships and institutional access that the kingdom does not possess — no direct Tehran line, no IRGC back-channel, no intermediary with credibility on both sides of the table. Riyadh’s nuclear deal with Washington, which waives enrichment safeguards the IAEA has just demanded from Tehran, compounds the structural asymmetry: Saudi Arabia has accepted terms for its own nuclear future that are less restrictive than what the international community is demanding of Iran, a position that offers Tehran zero incentive to treat the kingdom as a peer interlocutor.

The result is a country that absorbs more fiscal, military, and industrial consequence from this war than any other Gulf state, yet cannot influence the terms that might end it. The diplomatic calendar Trump described on ABC News — “this weekend, possibly in Europe” — unfolds in rooms where Mohammed bin Salman is not present, on a timeline Riyadh cannot adjust, producing an instrument the kingdom cannot amend. The operational calendar does not pause for European signing ceremonies. On Monday morning, more than 25 banks in Sadara’s creditor syndicate will need an answer about $3.7 billion in debt held against a company with no revenue, no production timeline, and no restart path — an answer that no memorandum of understanding, signed in any capital, can provide.

Frequently Asked Questions

What is the 14-point draft MOU between the US and Iran?

The draft memorandum of understanding, first reported by Mehr News Agency in early June 2026, covers 14 points spanning Hormuz reopening, sanctions relief sequencing, frozen asset releases, and nuclear provisions. An MOU is not a treaty — it does not require ratification by the U.S. Senate or Iran’s Majlis, carries no binding force under international law, and can be abandoned by either party without legal consequence. The 30-day Hormuz reopening timeline is one point among fourteen; remaining points address conditions Iran considers prerequisites, including the release of frozen assets that Tehran has valued at $12 billion at signing and $24 billion over the full implementation period.

Can Aramco afford to call Sadara’s $3.7 billion guarantee?

Aramco’s post-dividend cash reserves of approximately $53.3 billion cover the $2.405 billion guarantee in absolute terms. However, the company’s most recent quarterly free cash flow of $18.6 billion provided only 0.85x coverage of the $21.89 billion dividend it paid on June 9, meaning Aramco distributed more to shareholders than it earned. Calling the Sadara guarantee would require either drawing down reserves that are already declining quarter-over-quarter or signaling future dividend reductions — the latter carrying outsized consequences because PIF holds approximately 98.5% of Aramco’s shares and depends on the dividend stream to fund sovereign spending obligations including Vision 2030 commitments and ongoing defense procurement.

What happened after previous ceasefire announcements during this war?

Trump declared a ceasefire on April 8, 2026, and a separate cessation framework was announced on April 17. Neither produced any change in physical conditions at Hormuz. No major shipping line resumed strait transit, no oil major rerouted cargo, and the JWC did not alter its conflict-zone designation or initiate a review cycle. Brent briefly rallied on both occasions before falling back within days once markets recognized that operational conditions at the strait were unchanged. The June 12 announcement follows the same pattern — diplomatic headline, immediate price movement, Iranian denial — and is now the third iteration of a cycle in which markets respond to words and then correct against physical reality.

Why does the JWC designation matter more than a ceasefire announcement?

The Joint War Committee operates under Lloyd’s Market Association in London, and its conflict-zone designations are what determine whether marine insurers will write war risk policies at standard rates. A vessel entering a JWC-listed zone faces war risk premiums that can exceed 1-2% of hull value per transit — for a VLCC insured at $120 million or more, that translates to $1.2-2.4 million per single passage through the strait, a cost borne by the vessel operator regardless of whether a ceasefire is nominally in effect. Removal from the JWC conflict list requires consecutive quarterly review cycles with zero maritime incidents in the designated zone, making it structurally impossible for a weekend signing ceremony to affect insurance costs before the third quarter of 2027 at the earliest.