Table of Contents

- The 57% Profit Surge on 30% Less Oil

- How Does Aramco Actually Pay the Saudi State?

- The IPO Split: When Company Profit Stopped Equalling State Revenue

- Why Can’t Saudi Arabia Simply Sell More Oil?

- Three Revenue Streams, Three Different Wars

- Where Does PIF’s $14 Billion Actually Go?

- The Break-Even Mirage: $86, $94, or $111?

- $57.86 Billion in Borrowing Against a Profitable Company

- What Iran and the West Both Get Wrong

- FAQ

DHAHRAN — Saudi Aramco is about to report what analysts expect will be its best quarter in two years — SAR 108.8 billion ($29 billion) in net profit, a 57% jump from the previous quarter — and yet the kingdom that owns 98% of the company is borrowing $57.86 billion this year to keep the lights on. The paradox is not a rounding error or a timing mismatch. It is the first real-world stress test of a corporate structure that was deliberately designed to separate Aramco’s profitability from Saudi Arabia’s fiscal health, and the Iran war has exposed every seam in that design.

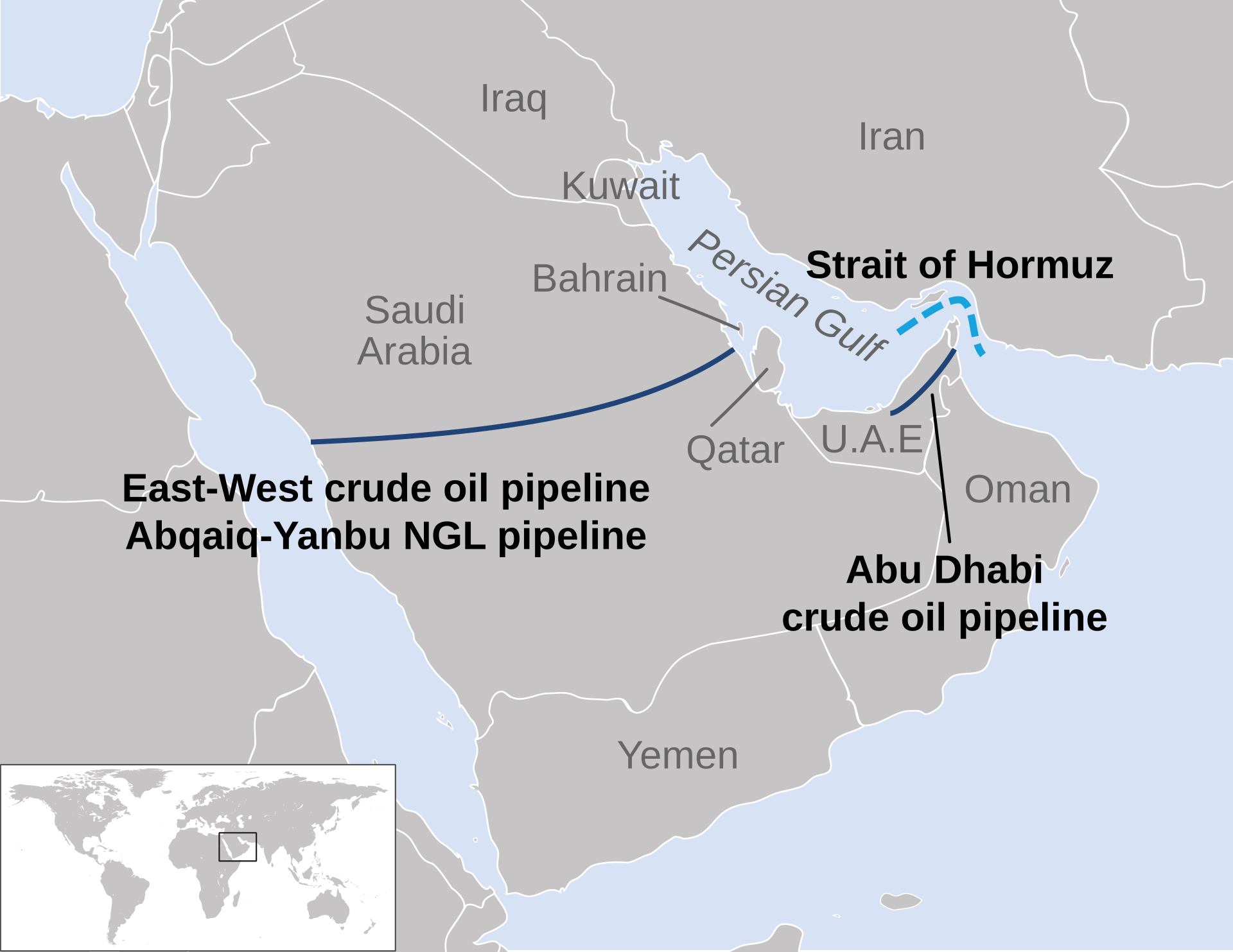

The mechanism at the centre of this disconnect is the 2019 IPO itself. When Mohammed bin Salman partially floated Aramco and later transferred 8% of the company’s equity to the Public Investment Fund, he created an architecture in which war-price windfalls flow primarily into equity value and dividend streams that do not directly fund the Ministry of Finance budget. The central government’s revenue still depends overwhelmingly on production volume — barrels loaded onto tankers and shipped — and that volume collapsed by 3.15 million barrels per day when Iran’s war shut the Strait of Hormuz and forced Saudi exports through the East-West Pipeline to Yanbu, a port that can handle barely half of what the kingdom was shipping before the first missile struck.

The 57% Profit Surge on 30% Less Oil

AlJazira Capital, the Riyadh-based brokerage, published its Q1 2026 Aramco forecast on April 23 and the headline figures read like a company thriving in wartime. Revenue of SAR 455.3 billion, up 9.4% from Q4 2025. Net income of SAR 108.8 billion ($29.01 billion), up 56.7% quarter-on-quarter and 13.8% year-on-year. The driver was crude prices: Brent surged 24.8% between quarters as the Hormuz disruption tightened global supply. AlJazira maintained an “Overweight” rating with a target price of SAR 29.6 per share, and its full-year 2026 net income forecast of SAR 427 billion (~$114 billion) assumed an average oil price of roughly $86 per barrel — well below where Brent is trading today.

But the production line tells a different story. Saudi output fell from 10.4 million barrels per day in February 2026 — the pre-war peak — to 7.25 million bpd by March, according to the International Energy Agency. That is a 30% drop, the largest single-country supply disruption the IEA has ever recorded. Crude exports to Asia alone fell 38.6% month-on-month, according to Kpler tracking data.

The mathematics of the paradox are straightforward. Aramco earns profit on every barrel it sells, and the price per barrel has risen faster than production has fallen — in profit terms. But Saudi Arabia the state earns revenue through a more complex set of channels, several of which are volume-dependent and cannot be offset by price alone. Aramco’s profit is a single number. The kingdom’s fiscal health runs on three separate revenue streams, each reacting differently to the war.

How Does Aramco Actually Pay the Saudi State?

Aramco transfers money to the Saudi state through three channels: tiered royalties on every barrel produced, a 50% income tax on upstream profits, and dividends distributed quarterly to shareholders. The first two channels are volume-dependent and hit the Ministry of Finance directly. The third is where the post-IPO architecture introduces a structural break — and where the war-price paradox originates.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The first channel is royalties. Aramco pays the Saudi government a tiered royalty on every barrel of crude it produces: 15% on oil priced below $70 per barrel, 45% on the portion between $70 and $100, and 80% on everything above $100. With Brent at $101.73, that top tier is active — but it applies only to barrels actually produced and sold. A 30% production drop means 30% fewer barrels generating royalties, regardless of the price tier. The 80% rate on the $1.73 above $100 does not compensate for the loss of 3.15 million barrels per day at every tier.

The second channel is income tax. Aramco pays a 50% tax rate on upstream profits and 20% on downstream operations. Higher prices push upstream profit higher, but the tax yield still depends on volume flowing through the system. The third channel — and the one the IPO restructured most dramatically — is dividends.

The IPO Split: When Company Profit Stopped Equalling State Revenue

Before the 2019 IPO, Aramco’s relationship with the Saudi treasury was essentially a direct pipeline. In 2018, the company transferred $58 billion in dividends directly to the state — roughly 24% of total public revenues that year. The company existed, for practical purposes, as a division of the government that happened to have its own balance sheet.

The IPO changed the plumbing. Today, the Saudi government holds approximately 81.5% of Aramco through the Ministry of Finance directly. The Public Investment Fund holds 16% — a stake that grew by 8 percentage points in early 2024 when MBS transferred equity from the government’s direct holding to PIF. The remaining 2.5% is the public float, traded on the Tadawul exchange and held by institutional and retail investors worldwide.

That 8% transfer was not a paper shuffle. Karen E. Young of the Arab Gulf States Institute and Columbia University’s Center on Global Energy Policy described it as a “zero-sum game” for the central government budget. When those shares moved to PIF, the dividends they generated — roughly SAR 35 billion ($9.3 billion) per year — stopped flowing into the Ministry of Finance’s revenue line and started flowing into PIF’s balance sheet instead. The Saudi Finance Minister had been explicit about this in 2019, telling a Carnegie Endowment forum that “the PIF’s investment policy is medium and long-term oriented; therefore, short-term revenues for the state budget are not to be expected.”

That was a statement of design intent, not a bug report. MBS wanted PIF to function as a sovereign wealth fund with patient capital, not as a supplementary budget line. The problem is that patient capital and wartime fiscal emergencies occupy opposite ends of the time horizon.

Why Can’t Saudi Arabia Simply Sell More Oil?

Because Hormuz is closed and Yanbu cannot absorb the volume. The East-West Pipeline can theoretically carry 7 million barrels per day to the Red Sea coast, but Yanbu’s combined port capacity tops out at roughly 4.5 million bpd under normal conditions and closer to 4.0 million bpd under wartime loading pressure, according to Argus Media. The gap — between 2.5 and 3.0 million bpd — cannot be loaded onto ships regardless of what Aramco produces inland.

Before the war, Saudi Arabia was exporting roughly 7 million bpd through multiple terminals — the majority via Ras Tanura and Ju’aymah on the Persian Gulf coast. Those terminals are within range of Iranian missiles and have already been struck. The Yanbu ceiling means the pipeline capacity that remains intact cannot be fully utilised, leaving the revenue shortfall at $93 million per day below the pre-war baseline even with Brent above $100.

The arithmetic is unforgiving. Pre-war Saudi oil revenue ran at approximately $832 million per day: 10.4 million bpd multiplied by roughly $80 Brent. Today’s figure is approximately $739 million per day: 7.25 million bpd at $101.91 Brent. For Saudi Arabia to match its pre-war daily revenue at current production levels, Brent would need to reach $114.76 per barrel — a price not seen since the immediate aftermath of the Hormuz closure.

Three Revenue Streams, Three Different Wars

The clearest way to understand the Aramco-Saudi disconnect is to track each revenue stream separately under war conditions. The table below shows how each channel differs in price sensitivity, volume sensitivity, and — critically — which part of the Saudi fiscal architecture absorbs the impact.

| Revenue Stream | Who Receives It | Price Sensitivity | Volume Sensitivity | War Impact |

|---|---|---|---|---|

| Royalties (tiered: 15%/45%/80%) | Ministry of Finance (direct) | High — 80% tier active above $100 | Directly proportional — per barrel | Net negative: volume loss exceeds price gain |

| Income tax (50% upstream) | Ministry of Finance (direct) | High — larger profit base | High — less oil = less upstream activity | Mixed: higher margins but lower throughput |

| Dividends (81.5% MoF share) | Ministry of Finance (via Aramco board) | Moderate — board sets payout | Indirect — affects free cash flow | Positive but lagged by one quarter |

| Dividends (16% PIF share) | PIF balance sheet | Moderate | Indirect | Does NOT enter MoF budget |

| Dividends (2.5% public float) | External shareholders | Moderate | Indirect | Leaves the kingdom entirely |

The first two streams — royalties and income tax — flow directly into the Ministry of Finance and are the backbone of Saudi Arabia’s operational budget. They fund salaries for 1.3 million public-sector employees, military procurement, subsidies, and the day-to-day machinery of the state. Both are volume-dependent. When production drops 30%, the direct fiscal hit is immediate and proportional, regardless of what the Brent benchmark does.

The third stream — dividends — is where the IPO architecture creates the paradox. Aramco’s total 2025 dividends were $85.5 billion, down from $124 billion in 2024. Of that $85.5 billion, roughly $70 billion (81.5%) went to the government and roughly $14 billion (16%) went to PIF. The expected total for 2026 is $87.6 billion. But the performance-linked component of the dividend — the additional payout that Aramco made during the high-price years of 2022-2024 — has effectively collapsed. Fitch Ratings noted in December 2025 that it assumed “no performance-linked dividends for 2026-2028.” The Q4 2025 performance-linked payout was $219 million, down from multi-billion quarterly payouts in the prior two years.

The base dividend arrives quarterly, with a structural lag. It cannot substitute for the daily royalty and export revenue shortfalls in real time. A finance ministry running nearly $100 million per day below its pre-war baseline cannot wait 90 days for a dividend cheque to partially close the gap.

Where Does PIF’s $14 Billion Actually Go?

The Public Investment Fund received approximately $14 billion from Aramco dividends in 2025 and will receive a similar amount in 2026. That money sits on PIF’s balance sheet, available for long-term deployment into Vision 2030 megaprojects, international investments, and portfolio diversification. It does not enter the Ministry of Finance budget. It cannot be used to pay civil servant salaries, fund military operations, or cover the gap between oil revenue and government expenditure.

This is not an accident or an oversight — it is the structural purpose of the post-IPO architecture. PIF was designed to be insulated from short-term fiscal pressures precisely so that it could make long-term investments without being raided every time the oil price dropped or a crisis hit the budget. The Carnegie Endowment warned in 2019 that this created “a parallel budget” outside Ministry of Finance accountability, and that warning has aged remarkably well.

But insulation works both ways. PIF’s cash reserves stood at roughly $15 billion in late 2024 — the lowest level since 2020, according to PIF disclosures — while its total assets under management reached $941.3 billion. AUM is not cash. The 2030 target of $2.67 trillion requires $1.73 trillion in additional growth, a trajectory that depends on continued capital deployment at scale, not on diverting quarterly dividends to plug budget shortfalls. Any formal consolidation of PIF into government accounts would undo the post-IPO separation that MBS spent five years constructing — and with it, the governance credibility that underpins Aramco’s Tadawul valuation.

The megaproject pipeline is already contracting under the pressure. The Line — NEOM’s signature 170-kilometre linear city — was suspended in September 2025 with only 2.4 kilometres of foundation complete, barely 1.4% of the planned length. Saudi construction contracts collapsed from $71 billion in 2024 to below $30 billion in 2025, a 60% decline, and PIF’s share of those contracts fell from 38% to 14%. An $8 billion write-down was recorded in PIF’s 2026-2030 strategy. The fund is being squeezed on both sides: its income from Aramco is stable but trapped on a balance sheet it cannot share with the treasury, while its expenditure commitments are being slashed to conserve cash that the treasury cannot access.

The Break-Even Mirage: $86, $94, or $111?

Saudi Arabia’s fiscal break-even oil price is one of the most frequently cited and least consistently defined numbers in energy economics. The answer depends entirely on what you include in the calculation, and the war has made the gap between definitions financially dangerous.

| Break-Even Definition | Price per Barrel | Source | What It Includes | Brent Margin at $101.73 |

|---|---|---|---|---|

| IMF central government only | $86.60 | IMF Fiscal Monitor | MoF budget expenditures | +$15.13 (appears solvent) |

| Bloomberg Economics consolidated | $94.00 | Bloomberg Economics | MoF + PIF operational costs | +$7.73 (tight) |

| Full PIF capex inclusive | $108-111 | Goldman Sachs | All sovereign spending incl. Vision 2030 | -$6.27 to -$9.27 (deficit) |

| Revenue-matching at war output | $114.76 | Derived from IEA/Aramco figures | Price needed at 7.25M bpd to match pre-war revenue | -$13.03 (deep deficit) |

The IMF figure — $86.60 — is the one most often cited in financial media and analyst reports, and it makes the kingdom look comfortable at current prices. But it counts only central government expenditures administered through the Ministry of Finance. It excludes PIF’s capital expenditure programme, which runs billions of dollars annually even in its contracted state. Bloomberg Economics pushed the figure to $94 by incorporating PIF’s operational costs. Goldman Sachs, running a full consolidation of sovereign spending including Vision 2030 project commitments, arrived at $108-111 per barrel.

Every one of these break-even calculations assumes pre-war production levels. At 7.25 million bpd — the IEA’s March 2026 figure — the actual revenue per dollar of oil price is 30% lower than these models assume. The IMF break-even of $86.60 was calculated on the assumption that Saudi Arabia could produce and export roughly 10 million bpd. At current output, the effective break-even is dramatically higher across every definition.

Goldman Sachs estimated the war-adjusted deficit at 6.6% of GDP — roughly $80-90 billion — compared to the official 2026 budget deficit projection of 3.3% ($44 billion). The official figure was set in December 2025, before the war, using assumptions of $72 per barrel oil and 10.1 million bpd production. Both assumptions are now catastrophically wrong, but in opposite directions: oil is $30 higher than budgeted, while production is 2.85 million bpd lower. The price overshoot cannot compensate for the volume shortfall.

“There would be catastrophic consequences for the world’s oil and markets the longer the disruption goes on, and the more drastic the consequences for the global economy.”

— Amin Nasser, CEO, Saudi Aramco, Q4/FY2025 earnings call, March 10, 2026

$57.86 Billion in Borrowing Against a Profitable Company

The Saudi government’s response to the fiscal gap has been to borrow. The kingdom’s full 2026 borrowing plan stands at $57.86 billion, including a $4.52 billion five-tranche sukuk issuance in April. The 2025 full-year deficit hit SAR 276.6 billion ($73.7 billion), up from SAR 115.6 billion in 2024. The fourth quarter of 2025 alone produced a SAR 94.9 billion ($25.3 billion) deficit — the largest quarterly deficit since the pandemic year of 2020.

The borrowing is happening against the backdrop of a company that, on paper, is enormously profitable. Aramco’s expected 2026 net income of $114 billion would make it one of the most profitable corporations on earth. Its base dividend of $87.6 billion exceeds the GDP of most countries. And yet the state that owns 98% of this company is issuing debt at a pace that suggests it cannot access enough of that profit quickly enough to cover its obligations.

This is the structural consequence of the IPO architecture under stress. Aramco’s profits flow through three channels — royalties, taxes, and dividends — each with different timing, volume sensitivity, and destination. The channel that responds fastest to production cuts (royalties) hits the Ministry of Finance directly and is the worst affected. The channel that benefits most from high prices (dividends) is partly diverted to PIF and partly delayed by quarterly payout schedules — and the government cannot accelerate those payments without overriding Aramco’s board at the cost of the equity valuation that makes PIF’s balance sheet work.

Rory Johnston of Commodity Context noted that a Hormuz reopening would drop Brent “$10-20 immediately” before stabilising at an “$80-90 range.” If that happens, Aramco’s profit surge evaporates — but Saudi Arabia’s production volumes could recover to pre-war levels, potentially restoring the royalty and tax revenue that funds the actual budget. The kingdom’s fiscal interest and Aramco’s corporate interest are, under current conditions, pointing in opposite directions: the state needs volume to restore royalties and taxes, while the company is thriving precisely because volume constraints are keeping prices elevated.

What Iran and the West Both Get Wrong

PressTV and Iranian state media have spent weeks framing the Hormuz disruption as proof that Western economies run on a “vibe economy” — that oil price volatility demonstrates the fragility of sentiment-driven financial systems. The framing treats Aramco’s corporate profit and Saudi state revenue as synonymous, presenting every Aramco earnings beat as evidence that Saudi Arabia is profiting from the war at the expense of global consumers.

Western progressive media has made the same conflation from the opposite direction. The Guardian and Common Dreams reported in April that the top 100 oil and gas companies were making “$30 million per hour” from the Iran war, with Aramco estimated to earn $25.5 billion in war-specific profit in 2026. The framing positions Aramco’s windfall as a Saudi windfall — as though every dollar of corporate profit lands in the state treasury.

Both framings collapse under the structural reality of the post-IPO architecture. Aramco the corporation is indeed having a strong quarter. But the royalties and taxes that fund Saudi Arabia’s budget depend on volume, not just price. The dividend streams that benefit from high prices are split between the Ministry of Finance (81.5%), PIF (16%), and external shareholders (2.5%), with PIF’s share explicitly walled off from the operational budget. And the performance-linked dividend component — already suspended by Aramco’s board with Fitch projecting zero such payouts through 2028, as detailed above — was specifically designed for exactly this kind of price environment.

The irony is structural. Iran’s war has created the exact conditions under which the separation between Aramco and the Saudi state — engineered by MBS himself — matters most. If Aramco were still a wholly state-owned entity with direct treasury transfers, the war-price windfall would flow unimpeded into government coffers. The IPO, the PIF equity transfer, and the performance-linked dividend suspension have created a set of filters that trap a significant portion of the upside in corporate equity and institutional balance sheets rather than the national budget.

Amrita Sen of Energy Aspects observed that oil prices now have “a higher floor” due to the disruption, with shippers remaining “super cautious” even if the strait were to reopen. Bob McNally of Rapidan Energy argued that markets were “delaying price signals” that could push political resolution. Both assessments reinforce the central paradox: the longer the war keeps prices elevated, the better Aramco looks on paper and the worse Saudi Arabia’s fiscal position becomes in practice.

The Stress Test Nobody Planned For

The 2019 Aramco IPO was designed to solve a problem that had nothing to do with war. MBS wanted to create a mechanism for monetising Saudi Arabia’s oil reserves without selling them — converting a portion of Aramco’s future cash flows into present-day capital for PIF to deploy across Vision 2030 megaprojects, international portfolio investments, and economic diversification. The architecture assumed that oil production would remain broadly stable, that export routes would remain open, and that the primary variable would be oil price fluctuations within a normal range. The Arab Gulf States Institute warned in 2025 — before the first missile — that “the 2025 dividend payout will likely be the last year the higher dividend can be paid in the absence of higher oil prices, asset sales, or debt issuance.” The war delivered higher prices. It also severed the production volumes needed to translate those prices into the royalties and taxes the budget actually depends on.

AlJazira Capital’s SAR 29.6 target price for Aramco shares reflects a genuine corporate-level analysis: the company is positioned to capture elevated crude prices and has flexible export routes through the western coast. That assessment is correct for Aramco the corporation. It tells you almost nothing about Saudi Arabia the state, which has watched its construction pipeline shrink 60% and is borrowing at a pace — $57.86 billion this year — that no profitable company’s balance sheet would appear to require.

MBS designed a wall between Aramco and the treasury, and the wall has held. The question now is whether it protects the kingdom’s long-term investment vehicle from short-term political raiding — or whether it traps war-price upside on the wrong side of the balance sheet while the state borrows to survive on the other.

FAQ

When does Aramco officially report Q1 2026 results?

Aramco has not confirmed an exact date for its Q1 2026 earnings release, but the company typically reports quarterly results in the first two weeks of the month following quarter-end — meaning early to mid-May 2026 is the expected window. The AlJazira Capital forecast discussed here is an analyst consensus estimate published April 23, not official results. Aramco’s investor relations calendar, available on its corporate website, will confirm the exact date once set by the board.

Could Saudi Arabia force PIF to return Aramco dividends to the state budget?

Legally, yes — the king could issue a royal decree reversing the 2024 equity transfer or mandating PIF dividend pass-through to the Ministry of Finance. Practically, doing so would undermine the entire corporate governance framework that supports Aramco’s equity valuation on the Tadawul, potentially triggering a selloff among international institutional investors who bought into the IPO on the promise of governance independence. It would also signal to credit rating agencies that PIF is not an independent sovereign wealth fund but a budget supplement — a classification that would affect both PIF’s and Saudi Arabia’s sovereign borrowing costs.

How do Aramco’s wartime profits compare to other major oil companies?

ExxonMobil, Shell, and BP are all expected to report strong Q1 2026 results driven by the same Brent price surge, but none face the production-volume paradox confronting Aramco. The Western majors have diversified upstream portfolios across multiple geographies unaffected by the Hormuz closure, meaning their production volumes have remained stable or increased to fill the Saudi supply gap. Aramco’s profit-per-barrel margin may be higher due to ultra-low lifting costs (under $3/barrel in the Eastern Province), but total revenue is constrained by the Yanbu export ceiling in a way that no other major faces.

What happens to Aramco’s dividend if Hormuz reopens and prices crash?

Aramco’s board declared the $87.6 billion base dividend for 2026 before the war and treats it as a contractual commitment to shareholders — protected even if quarterly free cash flow temporarily falls short by drawing on the company’s $29 billion cash position or issuing short-term debt. A price crash would reduce Aramco’s corporate profit but would not automatically trigger a dividend cut below the base level. Saudi Arabia’s fiscal position, by contrast, would improve on a price crash if production volumes recovered simultaneously, because royalties and taxes would flow again at volume — which is what the budget actually runs on.

Has the Aramco IPO model been tested by crisis before?

The COVID-19 pandemic in 2020 was the first shock to the post-IPO structure, but it was a demand crisis that reduced both price and volume simultaneously. Aramco cut its dividend from $75 billion to $70 billion and the government drew on reserves. The Iran war is structurally different: it is a supply crisis that raises price while cutting volume, creating the specific conditions under which the IPO’s revenue-bifurcation design produces divergent outcomes for the company and the state. The 2019 Abqaiq-Khurais drone attack briefly disrupted 5.7 million bpd of production but was resolved within weeks — too fast to test the fiscal architecture. The diplomatic dimension of that gap is visible in Japan PM Takaichi’s direct call to MBS requesting expanded crude supply — a request the Yanbu terminal ceiling structurally cannot fulfil.

The capital-allocation response to the production-revenue bifurcation is now explicit: PIF’s 2026–2030 strategy elevates Oxagon as the wartime industrial priority and cuts international exposure from 30 percent to 20 percent — the Oxagon pivot that quietly replaced The Line as the fiscal foundation of Vision 2030.