The IRGC Just Declared the Entire Persian Gulf a Kill Zone — and Markets Shrugged

DHAHRAN — The Islamic Revolutionary Guard Corps on April 18 declared that no vessel of any kind may move from its anchorage anywhere in the Persian Gulf or the Sea of Oman, and that any ship approaching the Strait of Hormuz will be “considered as cooperation with the enemy” and targeted. This is not a transit restriction. It is a no-movement order covering approximately 251,000 square kilometers of water — water in which Saudi Arabia’s three largest Gulf oil terminals sit exposed, and in which 826 commercial vessels were anchored as of April 17 with no insured exit. Brent crude closed at $91.71 on April 19, a price that implies the declaration is bluster. The same market made the same bet 48 hours earlier when Foreign Minister Araghchi declared Hormuz “completely open,” only to watch the IRGC reverse him within hours and fire on the very ships it had cleared to transit.

The ceasefire expires on April 22. Goldman Sachs projects Brent above $100 through 2026 if the closure holds for another month. The IRGC’s April 18 declaration is conditioned explicitly on the end of the US naval blockade — which Washington has shown no inclination to lift — and carries no built-in expiration. Saudi Arabia has now privately demanded exactly that: according to reporting on April 19, Riyadh warned the US that maintaining the blockade risks triggering a Houthi closure of Bab el-Mandeb — the kingdom’s sole remaining export corridor — a demand the White House has not publicly acknowledged. Saudi Arabia’s private demand to lift the Hormuz blockade reflects a growing recognition in Riyadh that the weapon Washington deployed on its behalf has become the trigger for a second chokepoint it cannot afford. The question is not whether the IRGC means what it says. The question is whether the market will require a struck VLCC at Ras Tanura to price in what the IRGC has already declared in plain language.

Contents

- What the IRGC Actually Said — and What It Supersedes

- From Chokepoint to Basin: Why the Geographic Expansion Matters

- The Sanmar Herald Test Case

- Does Iran Have Any Legal Basis for a Gulf-Wide Targeting Zone?

- How Exposed Are Saudi Gulf Terminals?

- Can Yanbu Cover the Gap?

- What Happens to Insurance When Anchored Vessels Become Targets?

- Why Is the Market Mispricing This?

- The April 22 Hard Deadline

- Frequently Asked Questions

What the IRGC Actually Said — and What It Supersedes

The IRGC’s April 18 warning, carried by Iran’s Student News Agency and Tasnim News and subsequently reported by PBS NewsHour, Al Jazeera, and NBC News, reads: “We warn that no vessel of any kind should move from its anchorage in the Persian Gulf and the Sea of Oman, and approaching the Strait of Hormuz will be considered cooperation with the enemy, and the offending vessel will be targeted.” Two components deserve separate attention — they represent a material escalation from everything the IRGC has said since the war began on February 28.

The first is the phrase “from its anchorage.” Previous IRGC declarations — including the April 5 and April 10 “full authority” announcements covered previously — concerned vessels transiting the Strait. The April 18 order extends the threat to vessels that are not moving. A VLCC at anchor off Jubail, 800 kilometers from Hormuz, is now inside the targeting perimeter merely by weighing anchor.

The second is the geographic expansion. The inclusion of the Sea of Oman — the body of water between Oman, Iran, and Pakistan connecting the Arabian Sea to the Strait — extends the declared zone beyond any waters over which Iran has a colorable sovereignty claim. The Sea of Oman is international water; Iran’s 12-nautical-mile territorial sea covers a sliver of its northern coast. The remainder is high seas under customary international law.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

This expansion was telegraphed. On April 15, Maj. Gen. Ali Abdollahi, commander of Khatam al-Anbiya Central Headquarters — the IRGC’s joint command responsible for integrated military operations — warned that “the powerful armed forces of Iran will not allow any exports or imports to continue in the area of the Persian Gulf, the Sea of Oman and the Red Sea” if the US blockade continued. Abdollahi’s statement covered three theaters; the April 18 operationalization covered two. The Red Sea threat remains in reserve, a deferred escalation option the IRGC can activate without issuing a new declaration. Khatam al-Anbiya is the same command that Pakistani ISI chief Lt. Gen. Asim Munir visited on April 16 — a meeting supposed to secure enforcement pressure for the ceasefire that instead preceded the most expansive IRGC threat of the war.

The April 18 declaration also supersedes a prior IRGC statement that was itself a reversal. On April 17, Foreign Minister Abbas Araghchi told reporters that the Strait of Hormuz was “completely open for all commercial vessels.” More than a dozen commercial ships transited successfully on the morning of April 18 on the strength of that assurance. By evening, the IRGC had reversed Araghchi and begun firing on the ships it had cleared.

Parliament Speaker Mohammad Bagher Ghalibaf — himself a former IRGC Aerospace Force commander — subsequently declared that “the Strait of Hormuz is under the control of the Islamic Republic” and called the US blockade “a clumsy and ignorant decision.” The civilian foreign ministry opened the strait; the military closed it; the parliament speaker validated the closure. The authorization ceiling that this publication has tracked since the war’s first week is no longer a structural ambiguity — it is settled. The IRGC commands Hormuz and, as of April 18, the entire Gulf basin.

Ghalibaf’s statement went further than a validation — it converted the IRGC’s operational posture into a formal parliamentary precondition, structurally closing the door to any ceasefire extension that does not include US blockade removal. How Ghalibaf’s reciprocity doctrine makes the April 22 deadline structurally unextendable is analyzed here.

From Chokepoint to Basin: Why the Geographic Expansion Matters

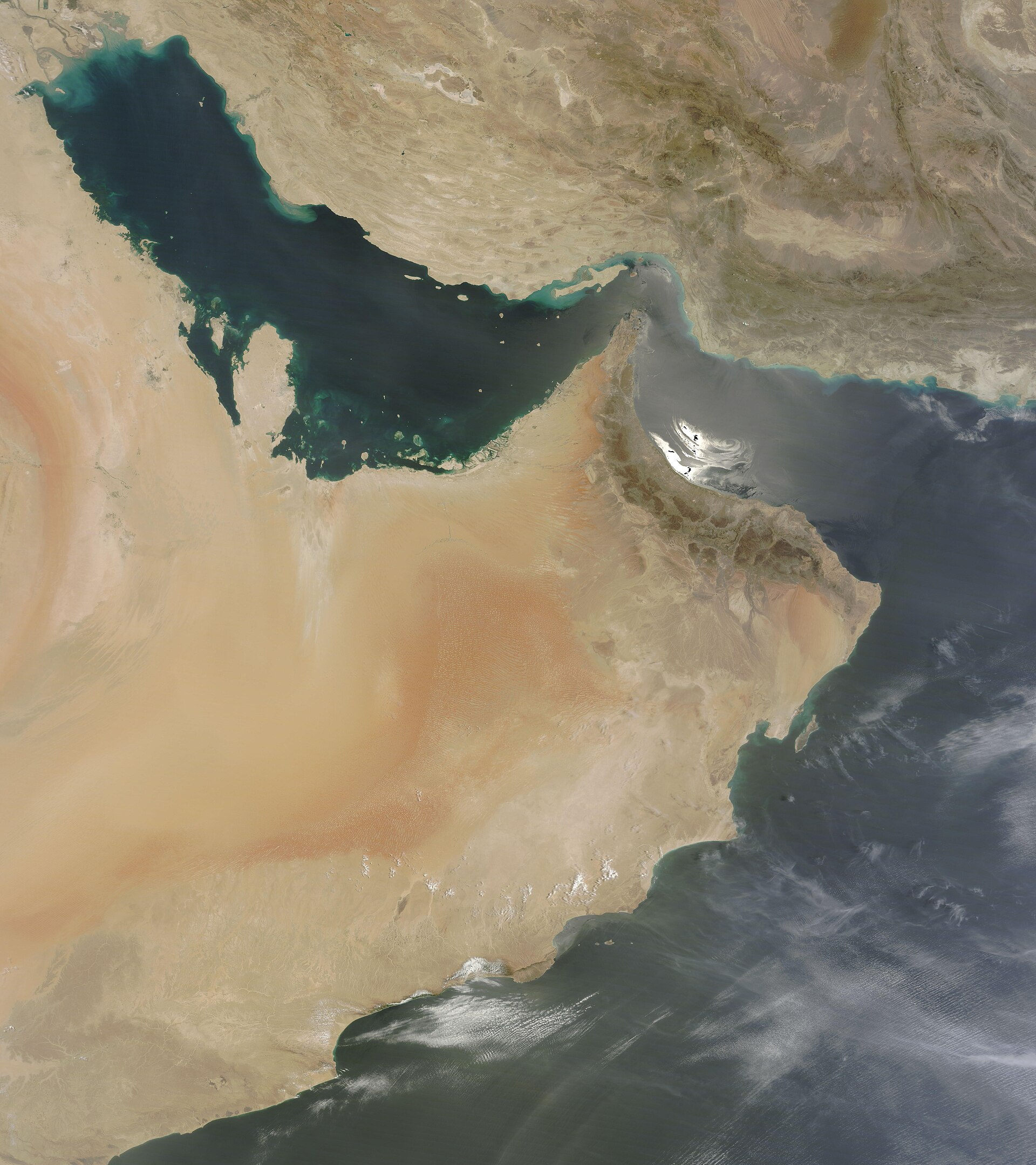

For the first 49 days of the war, the Hormuz crisis was a chokepoint problem. The IRGC controlled a 33-kilometer-wide passage through which roughly 20 percent of global oil supply had to transit. Chokepoint problems have chokepoint solutions: reroute through Yanbu, convoy with naval escorts, negotiate transit corridors. The April 18 declaration converted the chokepoint problem into a basin problem. The Persian Gulf is approximately 989 kilometers long and 56 to 338 kilometers wide; the Sea of Oman extends another 560 kilometers to the Arabian Sea. The IRGC has declared targeting authority over the entire combined body of water — a zone roughly the size of Germany.

Every Saudi, Kuwaiti, Bahraini, Qatari, and Emirati port sits inside this zone. Ras Tanura, Saudi Arabia’s largest crude oil terminal, is approximately 300 to 350 kilometers northwest of the Strait of Hormuz. Jubail, the kingdom’s primary petrochemical export facility, is 50 kilometers north of Ras Tanura. Dammam, the commercial port serving as the logistics hub for the Eastern Province, sits between them. None of these ports is anywhere near the Strait. A loaded VLCC departing Ras Tanura must travel the entire length of the Persian Gulf southeast toward Hormuz, passing within range of Iranian naval, missile, and drone assets for over 600 kilometers before reaching the Strait — which is itself closed.

The operational implication is that Yanbu, the Red Sea terminal fed by the East-West Pipeline, is now Saudi Arabia’s only functioning export corridor. This was already the case in practice: Jubail bookings were suspended as of April 16, according to Windward AI maritime intelligence, and 826 vessels were anchored in the Gulf on April 17 — a crisis high — with 162 dark activity events suggesting vessels switching off transponders to avoid detection. The April 18 declaration converted a de facto commercial freeze into a declared military one. The distinction matters for insurance, which prices risk based on declared threat environments, not merely observed ones.

The Sanmar Herald Test Case

If the April 18 declaration were purely aspirational, it would join a long history of Iranian threats that moved markets briefly and then faded. It is not aspirational. Hours after the declaration, the IRGC demonstrated enforcement against a vessel it had explicitly authorized to transit. The VLCC Sanmar Herald, an Indian-flagged tanker carrying nearly two million barrels of Iraqi crude — not Iranian crude, not US-affiliated cargo, but goods from a country Iran considers friendly — was approached by two IRGC gunboats approximately 20 nautical miles northeast of Oman. There was no VHF challenge. The gunboats opened fire. Bridge windows were damaged. Audio captured from the Sanmar Herald’s crew, subsequently published by multiple outlets, recorded the captain shouting: “You gave me clearance to go! You are firing now! Let me turn back!”

A second Indian-flagged vessel, the Jag Arnav, was intercepted and forced to retreat westward. The same hours also saw the French-flagged CMA CGM Everglade struck — the first NATO-member-state vessel hit in the crisis — demonstrating that the IRGC’s April 18 declaration applied without distinction to flag states from the Atlantic alliance as much as to neutral Asian shippers. India’s Foreign Secretary Vikram Misri summoned Iranian Ambassador Mohammad Fathali to convey “deep concern at the shooting incident” and urged Iran to “resume at the earliest the process of facilitating India-bound ships across the Strait.” India is not a US ally in this conflict. India purchased Iranian crude under OFAC General License U until the license expired on April 19. India is, if anything, a state that Iran needs as a customer. The IRGC fired on Indian ships anyway. The clearance process and the targeting process are operationally disconnected — a consequence of the headless IRGC Navy command that has persisted since Rear Admiral Alireza Tangsiri was killed on March 30 with no successor publicly named.

The Sanmar Herald incident also reveals the operational reach of the April 18 declaration. The firing occurred 20 nautical miles northeast of Oman — in the Sea of Oman, not the Strait, not Iranian territorial waters, not any zone where Iran has recognized jurisdiction. The IRGC enforced its declared zone in international waters against a neutral-flagged vessel carrying neutral cargo. That India responded with diplomatic remonstration rather than military escalation tells you something about the coercive weight of the IRGC’s position: even states with blue-water navies are choosing to absorb the hits rather than challenge the closure. The audio evidence from the Sanmar Herald documents the architectural reason why: as IRGC command fragmentation at Hormuz shows, the clearance registry and the tactical patrol units operate on entirely separate command loops with no mechanism to synchronise them in real time.

Does Iran Have Any Legal Basis for a Gulf-Wide Targeting Zone?

No. The legal architecture of maritime passage is unambiguous on this point, and the scholarly consensus has not wavered since the war began. Iran has not ratified the United Nations Convention on the Law of the Sea, but UNCLOS provisions on transit passage through international straits reflect customary international law that binds all states regardless of treaty ratification. Article 37 establishes that transit passage through straits used for international navigation “shall not be impeded.” The San Remo Manual on International Law Applicable to Armed Conflicts at Sea — the foundational 1994 treatise on naval warfare — provides in Rule 27 that belligerents cannot suspend transit passage through international straits even during armed conflict.

Michael Schmitt of the University of Reading and Rob McLaughlin of the University of Wollongong and the US Naval War College have written that transit passage through neutral waters in straits “cannot be hampered even during armed conflict” and that Iran “cannot lawfully” completely close the Strait. Naval mines, they concluded, cannot “effectively prevent or suspend transit passage for neutral vessels through international straits.” Tammy Caner and Pnina Sharvit Baruch of Israel’s Institute for National Security Studies wrote in Insight No. 2120 that “coastal states, including Iran, have no authority to prevent, restrict, or disrupt the regular passage of vessels, even during hostilities” and that “creating a dangerous environment that deters passage by engaging in attacks, making threats, or using naval mines violates international law, even without an official declaration.”

The April 18 declaration fails the San Remo Manual’s own test for a lawful blockade on at least three of four criteria. A lawful blockade must be declared and notified (met); applied impartially (failed — Iran has selectively permitted Chinese-intermediated transits while blocking others); effective (questionable — Iran lacks the naval capacity to enforce across the entire Sea of Oman after losing significant assets); and must not bar neutral states from access to their own ports (failed — Bahrain, Kuwait, Qatar, and the UAE are all denied access to their own territorial waters under the declaration). The gap between Iran’s legal position and international consensus is not a matter of interpretation. It is a matter of enforcement: the IRGC can declare whatever it wants, and the Sanmar Herald answers whether anyone will stop it.

Iran’s stated legal position is that the CENTCOM naval blockade of Iranian ports constitutes an illegal “act of piracy” under international law, and that the Hormuz closure is a proportional act of self-defense. The Supreme National Security Council tied the targeting zone explicitly to blockade continuation, framing it as a ceasefire enforcement mechanism. PressTV headlined the declaration as “Iran’s legal command replaces US bluff in Strait of Hormuz.” The framing elides the distinction between Iran’s 12-nautical-mile territorial waters — where Tehran has some claim to regulatory authority under the “innocent passage” standard it prefers — and the Sea of Oman, where it has none.

How Exposed Are Saudi Gulf Terminals?

Ras Tanura, Jubail, and Dammam collectively handled the majority of Saudi Arabia’s pre-war crude, refined product, and petrochemical exports. All three are on the western shore of the Persian Gulf, inside the IRGC’s declared targeting zone, and within demonstrated range of Iranian ballistic missiles, cruise missiles, and drone swarms. Ras Tanura was already struck by an Iranian drone in early March 2026; the refinery, with 550,000 barrels per day of processing capacity, sustained damage that has not been fully disclosed. Jubail bookings were suspended as of April 16 — a commercial decision made two days before the IRGC formalized the threat. The industry’s risk assessment ran ahead of the IRGC’s public posture.

The vessel accumulation problem compounds the terminal exposure. The 826 vessels present in the Gulf as of April 17 cannot transit Hormuz southward under the no-movement order. They cannot load cargo at Gulf ports without insurers pricing the anchorage as a declared military zone. They cannot switch off transponders without triggering the 162-and-rising dark activity alerts indicating potential hostile intent. A VLCC worth approximately $138 million is sitting in a declared kill zone with no insured exit route, no authorized destination, and no clear resolution timeline.

Saudi Arabia’s March production data, analyzed previously, showed output crashing to 7.25 million barrels per day from 10.4 million in February — a 30 percent decline. The IEA called it “the largest disruption on record.” Asia-bound exports fell 38.6 percent according to Kpler tracking data. Khurais, a 300,000-barrel-per-day field, went offline with no announced restoration timeline. The April 18 declaration does not create a new problem for Saudi exports. It formalizes and expands the existing one, while eliminating the residual possibility that selective IRGC permits might allow some Gulf-side loading to resume.

Can Yanbu Cover the Gap?

The short answer is no. The East-West Pipeline, which connects the Eastern Province oil fields to Yanbu on the Red Sea, was restored to its nameplate capacity of 7 million barrels per day on April 12 after repairs from an IRGC strike on a pumping station on April 8 — a strike that occurred after the ceasefire was nominally in effect. Pipeline capacity, however, is not the binding constraint. Yanbu’s port loading infrastructure — the jetties, single-point mooring buoys, storage tanks, vessel scheduling capacity — has a practical ceiling of 4 to 5.9 million barrels per day depending on vessel mix and turnaround time. Pre-war Saudi Gulf throughput ran at 7 to 7.5 million barrels per day. The structural export gap is 1.1 to 1.6 million barrels per day even at maximum Yanbu utilization.

This gap cannot be closed by operational optimization. It requires physical infrastructure — additional mooring points, expanded tank farms, deepwater channel dredging — that takes years to build. Saudi Arabia began expanding Yanbu capacity before the war, but completion extends into 2028. At $90 Brent, 1.1 to 1.6 million barrels per day of stranded exports represents $99 to $144 million in lost daily revenue; at Goldman’s projected $100-plus sustained price, the figure rises above $160 million daily.

Saudi Arabia’s war-adjusted fiscal break-even is $108 to $111 per barrel, according to Bloomberg’s PIF-inclusive calculation. Brent at $91.71 runs $16 to $19 below that threshold. Goldman’s war-adjusted deficit projection is 6.6 percent of GDP, double the official 3.3 percent forecast. The fiscal hemorrhage is structural, not cyclical, and it is denominated in exactly the currency Saudi Arabia cannot produce from its Gulf terminals.

Yanbu also faces a threat the April 18 declaration left in reserve. Abdollahi’s April 15 warning covered the Red Sea alongside the Persian Gulf and Sea of Oman; the IRGC operationalized two of three theaters. If it activates the Red Sea component — or if Houthi-aligned forces extend their Red Sea targeting to Saudi-flagged or Saudi-bound vessels — Yanbu’s bypass function collapses entirely. Saudi Arabia would have zero functioning export corridors. The kingdom’s entire economic model depends on a single pipeline feeding a single port operating above historical norms, in a threat environment where the adversary has explicitly reserved the right to extend its targeting zone to that port’s sea lane.

What Happens to Insurance When Anchored Vessels Become Targets?

The Lloyd’s Joint War Committee expanded its high-risk listed areas to include the entire Persian Gulf and Gulf of Oman on March 3, 2026, adding Bahrain, Kuwait, Oman, Qatar, and Djibouti to existing high-risk designations. Listed-area status does not automatically cancel coverage — it requires vessel owners to notify their underwriters and pay Additional Premium, the war risk surcharge, to remain covered. Pre-war, the Additional Premium for a Hormuz transit was a rounding error. By mid-April, Dylan Mortimer, Hull War Lead at Marsh, was quoted in Lloyd’s List reporting that premiums for a single VLCC transit had reached $10 to $14 million — 7 to 10 percent of a $138 million hull value. Hapag-Lloyd imposed a War Risk Surcharge of $1,500 per TEU for standard containers and $3,500 for reefer and special equipment, effective since March 2. JPMorgan estimated approximately 329 vessels in the Persian Gulf requiring roughly $352 billion in aggregate insurance coverage that private markets were no longer fully providing.

The IRGC’s April 18 declaration introduces a coverage question that standard JWC Additional Premium procedures do not resolve. The AP framework assumes vessels are transiting through a high-risk area — moving through danger toward a destination. The IRGC’s no-movement order targets vessels at anchor. A VLCC that complied by remaining stationary at its Jubail anchorage is in a declared targeting zone but not transiting; a VLCC that weighs anchor to leave is violating the IRGC’s declared rules of engagement.

The insurer’s dilemma is existential: does the policy cover a vessel targeted for staying and targeted for leaving? The World Economic Forum reported that governments were becoming “insurers of last resort” as private war-risk coverage dried up. But sovereign backstops take months to legislate, and the ceasefire expires in three days.

The Tanker War of 1984 to 1988 offers the closest historical precedent, and it is not reassuring. Hull war risk rates peaked at 7.5 percent of vessel value in May 1984 after Iraq attacked the Saudi tanker Yanbu Pride near Kharg Island. Markets assumed de-escalation and rates halved by January 1985. Attacks resumed in May 1985 and rates doubled again — a six-month round-trip mispricing that cost underwriters billions. The July 1987 Bridgeton mining, when the US-reflagged Kuwaiti tanker hit a mine on its first Operation Earnest Will convoy, triggered a 50 percent spike in cargo rates. Total war insurance claims reached approximately $2 billion by the war’s end, with $1 billion absorbed by the Lloyd’s market alone. The current crisis has compressed that repricing cycle from years to days.

Why Is the Market Mispricing This?

Brent crude at $91.71 on April 19 reflects a specific assumption: that the IRGC’s April 18 declaration is bargaining posture that will be walked back as ceasefire negotiations continue. This is the same assumption that drove Brent down nearly 10 percent on April 17 when Araghchi declared Hormuz open — a decline fully reversed within 24 hours when the IRGC closed the strait again and fired on transiting vessels. The market is pattern-matching to prior crises in which Iranian threats preceded negotiated outcomes. It made that bet on April 17 and lost. It is making the same bet on April 19 at slightly better odds, but the underlying risk has worsened, not improved.

Goldman Sachs lowered its Q2 2026 Brent forecast from $99 to $90 per barrel after the ceasefire was announced, projecting “gradual normalization by mid-April.” Mid-April has arrived. The normalization has not. Goldman’s own scenario analysis projects Brent above $100 through all of 2026 if Hormuz remains mostly closed for another month, with Q3 at approximately $120 and Q4 at approximately $115. The EIA raised its 2026 Brent projection to $96; ANZ expects $88 by year-end on Middle East supply losses; UBS raised its price view as disruptions persist.

The analyst consensus is that current prices are too low for sustained closure — but the trading desk consensus is that closure will not be sustained. The April 18 declaration, conditioned explicitly on the end of the US blockade, carries no built-in expiration mechanism. The OFAC General License U expired on April 19 with no renewal, removing the last legal framework for Iranian oil to reach Western-aligned buyers. The incentive structure for the IRGC to reopen has weakened, not strengthened.

The mispricing also reflects a failure to distinguish between transit risk and basin risk. Pre-April 18, the market was pricing Hormuz transit risk — the probability that a laden tanker would be hit during the approximately four-hour passage through the Strait. The April 18 declaration converted this into basin risk: the probability that any vessel anywhere in the Persian Gulf will be targeted for any movement. Basin risk is structurally higher because it applies to loading, anchorage, lightering, bunkering, and every other commercial activity in the Gulf, not just the transit window. The 826 vessels in the Gulf are not at risk for four hours. They are at risk continuously, for as long as they remain inside the declared zone, with no insured exit.

VLCC spot rates at $423,000 per day — roughly ten times the pre-war level — are pricing in scarcity, not risk. The rates reflect fewer tankers willing to enter the Gulf, driving up the premium for those that do. They do not yet reflect the possibility that the IRGC will enforce its declaration against laden tankers at Saudi terminals, which would convert scarcity pricing into crisis pricing. The Tanker War’s lesson is that crisis pricing arrives late and arrives all at once: the Bridgeton mining corrected months of complacency in a single afternoon.

The April 22 Hard Deadline

The two-week ceasefire, signed on April 8 in Islamabad, expires on April 22 — three days from today. No extension mechanism exists in the agreement’s text, per analysis by the Soufan Center. The 96-hour window between April 19 and April 22 is the period in which markets will discover whether the IRGC’s declaration was a negotiating tactic or an operational posture. The behavioral evidence favors the latter. The IRGC has not walked back the April 18 declaration. Ghalibaf has reinforced it. Araghchi has reverted to characterizing the US blockade as a ceasefire violation while stating that Iran is “studying fresh US proposals” — language that implies no imminent resolution.

The Supreme National Security Council’s April 18 framing is the most revealing. The SNSC tied the targeting zone explicitly to the continuation of the US blockade, calling it “acts of piracy and maritime theft” and declaring that transit will remain closed until “full freedom of navigation for vessels travelling from Iran to their destinations and back” is restored. This condition requires the United States to lift its naval blockade of Iranian ports — a concession that would undermine the entire US pressure campaign. President Trump, who stated on April 18 that the blockade “will remain in full force” and that Iran “got a little cute,” has categorically ruled it out. The IRGC’s targeting zone is conditioned on an event that neither party expects to occur in the next 72 hours.

April 22 is also the date on which Indonesian Hajj pilgrims — 221,000 of them — begin departing for Saudi Arabia, and on which the Makkah Umrah cordon, sealed since April 18, enters its most operationally demanding phase. Saudi Arabia cannot simultaneously manage the largest peacetime religious gathering in its history and a Gulf-wide military escalation. The Custodian of the Two Holy Mosques title, which defines the Saudi monarchy’s legitimacy, depends on the physical security of millions of pilgrims. The IRGC knows this. The April 22 deadline is calibrated to the moment of maximum Saudi vulnerability — when the kingdom must choose between defending its oil infrastructure and protecting its religious mandate, knowing that failure in either domain is existential in a way that a temporary production cut is not.

Three days is not much time. It is enough time for a market that has mispriced every IRGC escalation in this war to misprice one more — or to belatedly recognize that the IRGC’s basin-wide targeting declaration is an operational fact, backed by demonstrated enforcement, conditioned on concessions that will not arrive, and expiring into a ceasefire with no extension mechanism. The last time markets assumed de-escalation in this crisis, it cost them 48 hours. The next assumption may cost considerably more.

Frequently Asked Questions

How does the April 18 declaration differ from previous IRGC Hormuz statements?

Previous IRGC declarations — on April 5 and April 10 — asserted “full authority to manage the Strait” and targeted vessels transiting through the chokepoint. The April 18 declaration extends from the Strait to the entire Persian Gulf and the Sea of Oman, covering approximately 251,000 square kilometers rather than a 33-kilometer passage. More consequentially, it targets vessels at anchor: the phrase “no vessel of any kind should move from its anchorage” means ships already inside the Gulf cannot leave without violating the order, and cannot stay without accepting they are inside a declared targeting zone. The US Maritime Administration’s advisory 2026-0001B, issued on March 6, already covered the “Strait of Hormuz, Persian Gulf, Gulf of Oman, and Arabian Sea” — suggesting US risk assessors anticipated this zone expansion six weeks before the IRGC formalized it.

Could a US naval convoy system protect Saudi Gulf exports?

A convoy system modeled on Operation Earnest Will (1987–1988) would require sustained US naval presence inside the declared targeting zone — which the IRGC has framed as “cooperation with the enemy.” CENTCOM currently has DDG-121 (USS Frank E. Petersen Jr.) and DDG-112 (USS Michael Murphy) operating in the area; both transited the Strait on April 11 and received “last warning” radio calls from the IRGC. A convoy sufficient to protect commercial traffic from Ras Tanura through 600-plus kilometers of Gulf waters would require minesweeping assets the US no longer has forward-deployed: the four Avenger-class mine countermeasures ships at Bahrain were decommissioned in September 2025. Based on the 1991 Kuwait benchmark, clearing a 200-square-mile zone takes approximately 51 days — and the declared IRGC zone is orders of magnitude larger.

What is the Mein Schiff 4 incident and why does it matter?

The cruise ship Mein Schiff 4, operated by TUI Cruises, reported a “nearby splash” off the coast of Oman on April 18 and received a VHF threat from the IRGC to “fire at and destroy the ship.” The vessel was carrying civilian passengers with no connection to any belligerent party. The incident matters because it demonstrates the indiscriminate scope of the IRGC’s targeting declaration — passenger vessels, not just commercial tankers or military ships, fall inside the perimeter. Under San Remo Manual Rule 47, targeting a passenger vessel constitutes a war crime absent military necessity. The incident has significant implications for cruise and ferry services connecting Bahrain, Kuwait, and Qatar to external destinations, where route diversion options are geographically limited compared to container shipping.

What are the conditions under which Iran says it will reopen the Gulf?

The SNSC statement of April 18 conditions reopening on “full freedom of navigation for vessels travelling from Iran to their destinations and back” — meaning the complete lifting of the CENTCOM naval blockade of Iranian ports, in effect since April 13. This condition is more expansive than a simple ceasefire: it requires the restoration of Iranian export capability, which the US blockade was specifically designed to deny. The SNSC’s characterization of the blockade as “acts of piracy and maritime theft” implies Iran considers itself entitled to remedy beyond mere lifting. Five Iranian conditions circulated earlier through SNSC channels included recognition of Iranian sovereignty over Hormuz — a demand that would effectively grant Tehran a permanent veto over Gulf maritime traffic. The gap between Iran’s stated conditions and any plausible US concession is wider on April 19 than it was on April 13 when the blockade began.

How does the current crisis compare to the 1984–1988 Tanker War in insurance terms?

The Tanker War’s repricing cycle unfolded over years — six years from the first attacks in 1981 to the full corrective triggered by the Bridgeton mining in 1987. The current crisis has compressed the same cycle to weeks. VLCC premiums of $10 to $14 million represent 7 to 10 percent of hull value, already surpassing the Tanker War’s peak rate of 7.5 percent. JPMorgan’s $352 billion aggregate insurance exposure estimate for vessels in the Gulf dwarfs the entire claims history of the earlier conflict. More structurally, the 1984–1988 war never produced a formal basin-wide targeting declaration from either belligerent; the April 18 order is without precedent in the modern law of armed conflict at sea. The private market has no template for pricing it.

The 72-hour window before the ceasefire expiry on April 22 also marks the opening days of the Hajj pilgrim inflow — with confirmed flights arriving from Pakistan, Turkey, India, Bangladesh, and Malaysia under the Makkah Route Initiative. The arrival of Hajj pilgrims on Saudi soil during the 72-hour window before ceasefire expiry is reported here.