DHAHRAN — The United States struck targets near Asaluyeh — the processing hub for South Pars, the largest natural gas reservoir on Earth — on July 10, 2026, crossing into energy infrastructure targeting for the first time in this conflict cycle. Brent crude settled at $76.58 per barrel, down two percent from the previous session. The war premium did not return.

Four months ago, when the Israeli Air Force struck South Pars directly, oil prices surged five dollars a barrel within hours. Now the United States operates in the same target zone and the price falls. Structural oversupply has absorbed an escalation threshold no prior Gulf crisis has crossed. The market no longer prices war near the world’s most valuable gas field as a supply event — it prices the glut surrounding it.

The question is three-part: why the first US strike near Iranian energy infrastructure failed to lift prices, what the March-to-July price delta reveals about war premium exhaustion, and why Saudi Arabia now faces a paradox without modern precedent — host and partial beneficiary of a conflict that keeps lowering its own oil price.

Table of Contents

- What Did the US Strike Near Asaluyeh on July 10?

- Why Did Oil Prices Fall After an Energy Infrastructure Strike?

- The March Precedent and the Price That Disappeared

- How Large Is South Pars and Why Does It Matter?

- Can Saudi Arabia Benefit From South Pars Degradation?

- The Structural Surplus That Swallowed the War

- What Does Asaluyeh Tell Markets About the Next Strike?

- Frequently Asked Questions

What Did the US Strike Near Asaluyeh on July 10?

US forces struck sites near the port city of Asaluyeh in Bushehr Province on July 10, 2026, with explosions reported across Bushehr, Asaluyeh, and Bandar Abbas according to Gulf News and IRNA. CENTCOM described a second wave of operations targeting “90 military targets along Iran’s coast.” The strikes included a fishing pier in the village of Bonood in Asaluyeh County, where the Bushehr Province deputy governor confirmed that residents’ fishing boats caught fire, according to IRNA.

Asaluyeh is not an ordinary coastal town. It is the onshore terminal for South Pars, where twenty-four processing phases convert raw gas from the world’s largest field into pipeline-grade fuel, liquefied petroleum gas, and condensate. The town sits at the base of an industrial corridor that supplies 70 to 75 percent of Iran’s domestic gas consumption, according to the Middle East Council on Global Affairs. A strike on Asaluyeh’s perimeter is a strike on the infrastructure that keeps Iran’s grid, petrochemical plants, and residential heating network operational.

This marks the first time US forces have struck near Iranian energy production infrastructure in this conflict cycle. The Israeli Air Force hit South Pars directly on March 18, damaging sections accounting for approximately 12 percent of Iran’s total gas production and halting two refineries with combined capacity of 100 million cubic metres per day, according to Iran International. The July 10 US strikes brought American ordnance into the same target zone — not hitting the processing facilities themselves, but operating within the security perimeter of the world’s most valuable gas complex.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Iranian state media separated the damage into civilian and military categories. IRNA and Fars News Agency focused on the Bonood fishing pier, destroyed boats, and lost livelihoods — with no state acknowledgment of damage to energy infrastructure on July 10. IranWire, the independent Iranian outlet, reported that “residents say civilian livelihoods destroyed” while noting CENTCOM’s 90-target description. The gap between the two framings is consistent with a pattern in which Iranian state media isolates “civilian” from “military/industrial” reporting to control the escalation narrative.

The strikes followed four days of IRGC attacks on US bases across the region. Iran struck Kuwait and Bahrain on July 8, then Qatar and Jordan on July 9, hitting targets including the AN/GSC-52B(V5) meteorological satellite dish at Al Udeid — a $15 million system and the first of its kind deployed outside the continental United States — and firing ten missiles at Muwaffaq Salti Air Base in Jordan, eight of which were intercepted by MIM-23 Hawk batteries. Prince Sultan Air Base, already locked down since Saudi Arabia’s Operation Project Freedom grounded 43 US warplanes in May, remained the only major US installation in the region not struck.

Why Did Oil Prices Fall After an Energy Infrastructure Strike?

Brent crude fell because structural oversupply in global oil markets has become a stronger price-setting force than escalation risk. The US Energy Information Administration’s July Short-Term Energy Outlook, published the same week, forecast Brent at $70 per barrel for Q4 2026 and $65 for full-year 2027 — a downward revision of $15 per barrel from the June outlook. The EIA noted that “rising oil production is expected to result in the market shifting back to the pre-conflict state of oversupply” by 2027.

Three factors compounded on July 10 to suppress the price response. First, President Trump told reporters that Iran had “reached out to make a deal” — Bloomberg reported the statement drove market confidence that the situation would stabilise. Second, OPEC+ had just confirmed its sixth consecutive monthly quota increase of 188,000 barrels per day for August. Third, GL X1 sanctions reimposed on July 7 after Iran attacked commercial shipping had already been absorbed without price effect. The United Against Nuclear Iran tracker documents 47 tankers departing the Gulf of Oman carrying approximately 58 million barrels of Iranian crude worth $4.5 billion since the June 14 MOU — sanctions paper, Iranian oil moving.

The traditional war-premium mechanism requires that military action imply a supply gap the market cannot fill. In prior Gulf crises — the 1990 Iraqi invasion of Kuwait, the 2019 Abqaiq-Khurais drone attack — spare capacity was thin enough that any disruption commanded immediate pricing. In 2026, the International Energy Agency projects a global oil surplus approaching five million barrels per day by 2027, a structural buffer that absorbs disruptions that would have added ten dollars to the barrel price in any prior cycle.

When Hormuz recorded zero transits earlier this week, Brent barely moved. When GL X1 sanctions came back, the price did not budge. When the United States struck within kilometres of the world’s largest gas field, oil fell. The market has priced every available escalation pathway and found none sufficient to offset the glut.

The March Precedent and the Price That Disappeared

The March 18 Israeli Air Force strike on South Pars was the threshold-crossing event. The attack — which damaged sections accounting for 12 percent of Iran’s total gas output and shut down two refineries — drove oil from approximately $103 to $108 per barrel within hours. The five-dollar spike reflected the market’s recognition that energy infrastructure had entered the target set for the first time.

President Trump reinforced the threshold the following day. In a Truth Social post reported by CNBC, Time, and Euronews on March 19, he wrote that “the United States of America, with or without the help or consent of Israel, will massively blow up the entirety of the South Pars Gas Field at an amount of strength and power that Iran has never seen or witnessed before” if Qatar’s liquefied natural gas infrastructure were attacked again. The threat was explicit, unambiguous, and addressed to the single most valuable energy asset in Iranian territory. It established the outer boundary of American escalation in terms the market understood.

Then the price disappeared. By early July, Brent had fallen below its pre-war level of $72.48, settling at $70.82 before recovering slightly to $76.58 on July 10. The five-dollar March premium did not persist for five weeks. The Stimson Center had characterised the South Pars strike as marking a transition “from kinetic confrontation to energy warfare, in which infrastructure becomes a primary instrument of coercion.” The market accepted the characterisation — and priced it at zero.

The 2019 Abqaiq-Khurais attack provides a comparison that makes the 2026 case more striking. Houthi drones temporarily removed 5.7 million barrels per day of Saudi production — five percent of global supply, according to CSIS — and Brent jumped from $60 to $69. The price fell back below pre-attack levels within two weeks as Saudi Arabia restored output. The lesson of 2019 was that single-facility damage against a producer with spare capacity creates only transient spikes.

The lesson of 2026 is harsher. South Pars is under ongoing military assault with no restoration timeline, Hormuz transit has partially collapsed, and prices are still falling. The surplus has overridden not just the spike but the sustained premium that ongoing conflict should theoretically generate.

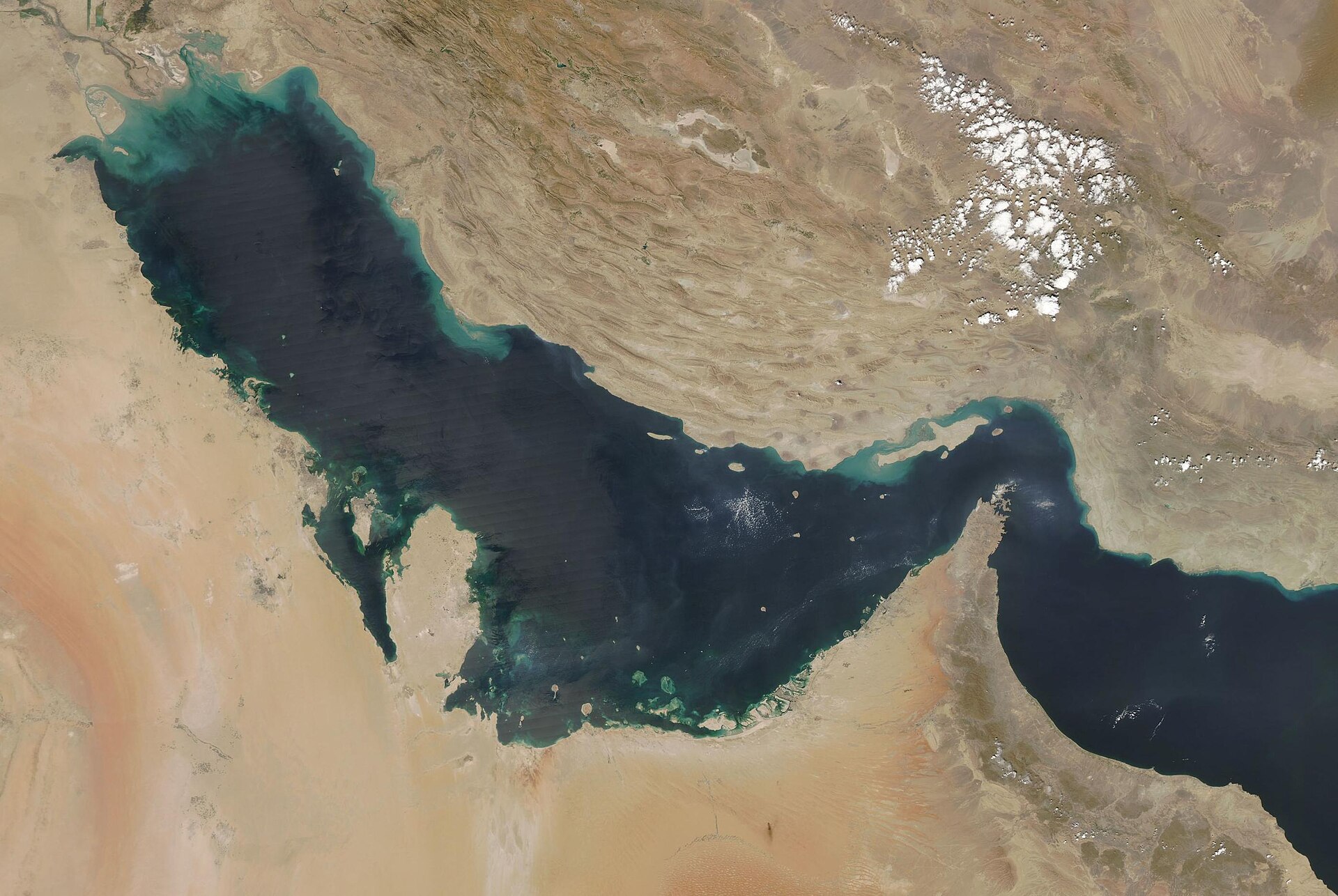

How Large Is South Pars and Why Does It Matter?

South Pars holds 500 trillion cubic feet of natural gas in place, with 360 trillion cubic feet recoverable, making it the largest natural gas field ever discovered. The Iranian side — it shares the reservoir with Qatar’s North Dome field — spans 28 production blocks across 24 operational phases and produced 716 to 730 million cubic metres per day before the conflict began, according to Offshore Technology.

The field’s economic significance matches its geological scale. NS Energy Business estimates daily production value at $272 million, with projected annual value at full development reaching $90 billion. GlobalSecurity.org estimates South Pars has generated approximately $450 billion in cumulative wealth for Iran. The field feeds power generation, heating, and the petrochemical sector across a country of 88 million people — a dependency that makes South Pars degradation an instrument of internal economic pressure rather than a conventional supply-disruption play.

The geological interconnection with Qatar’s North Dome introduces a cross-border dimension. The shared reservoir operates at 300 to 400 bar of well pressure, according to the Middle East Council on Global Affairs. Wellhead or subsurface damage from military strikes could cause “uncontrolled methane releases lasting weeks.” Iranian production from the joint field is already forecast to decline 30 percent or more over the next decade due to existing reservoir pressure fall — a trajectory that combat damage accelerates. The distinction matters: South Pars strikes impose costs on Iran’s domestic energy supply while carrying geological risks that extend into Qatari sovereign territory.

The Columbia Center on Global Energy Policy captures the structural paradox of Iran’s gas position: Iran holds “among the world’s largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.” Three major LNG export projects — Iran LNG, NIOC LNG, and Pars LNG — have been cancelled or indefinitely suspended since 2010. Nearly all South Pars output is consumed domestically. Damaging South Pars does not remove gas from the global market so much as it destabilises Iran’s internal energy grid — a distinction that helps explain why oil traders treat South Pars strikes as geopolitically significant but commercially contained.

Can Saudi Arabia Benefit From South Pars Degradation?

Saudi Arabia holds a narrow competitive advantage from South Pars degradation through two channels: the Petroline East-West pipeline, operating at full capacity of 7 million barrels per day since March 2026, which routes crude exports to the Red Sea and avoids Hormuz entirely; and reduced Iranian competition in the LNG market, where Rystad Energy projects a cumulative loss of approximately 120 billion cubic metres of supply from 2026 to 2030 due to combined damage at Qatar’s Ras Laffan (17 percent capacity reduction under force majeure) and South Pars.

The Columbia Center on Global Energy Policy confirmed the routing advantage in concrete terms. Saudi Arabia “saw increases in revenue” during the conflict while Qatar, Iraq, Kuwait, and the UAE — all unable to avoid the Strait of Hormuz — “saw declines.” The Petroline gives Saudi Arabia a structural edge that no other Gulf producer possesses. China’s friendly-nation carve-out for Hormuz transit fees further complicates the competitive position of other Gulf exporters while leaving Saudi Arabia’s Red Sea route untouched.

But the Brent floor problem dominates the upside calculus. Saudi Arabia’s fiscal breakeven sits at $86.60 per barrel according to the IMF — more than ten dollars above the July 10 settlement price. Aramco’s August Arab Light official selling price fell to negative $1.50 versus the Oman/Dubai benchmark, down from a peak of $19.50 in May — a swing that costs approximately $900 million per month in forgone revenue at current production levels. The Q1 2026 fiscal deficit reached SAR 125.7 billion. Aramco’s free cash flow covers only 0.85 times its dividend obligation.

The paradox is structural and may prove inescapable. Saudi Arabia benefits from South Pars degradation competitively — fewer Iranian molecules, more market share for Aramco’s own gas expansion at the Jafurah field — but loses from the Brent price trajectory that the same conflict produces. The war is destroying the oil price Saudi Arabia needs to fund it. The kingdom bears those costs through OPEC+ quota hikes that depress the barrel further and Persian Gulf Security Agreement payments of $5.5 million per day ($253 million outstanding through August 18). The Petroline advantage is real. It is also insufficient when the barrel itself is priced ten dollars below the budget.

Trump’s threat to seize Kharg Island sharpens the same constraint: why Saudi Arabia cannot afford the windfall Kharg created — the Petroline ceiling that caps safe export capacity and the IRGC’s 2:1 retaliation doctrine combine to ensure that the market share freed by Kharg’s closure cannot be safely loaded at the Gulf-facing terminals already within Iranian strike range.

The Structural Surplus That Swallowed the War

The IEA’s June 2026 Oil Market Report projects global oil supplies surging approximately eight million barrels per day to 110 million barrels per day by 2027 against demand of 105.3 million barrels per day. The resulting surplus of nearly five million barrels per day — which the IEA characterised as a transition “from supply shock to oil glut” — exceeds the total production of Iraq and represents the largest projected oversupply since the late 1990s.

OPEC+ has contributed directly to the surplus through six consecutive monthly quota increases of 188,000 barrels per day each since April. The hikes reflect an internal logic — maintaining market share against non-OPEC supply growth from the United States, Brazil, and Guyana — that has decoupled OPEC+ output decisions from the war premium they theoretically should protect. The IMF’s own modelling requires Hormuz closed for its price forecast but open for its growth forecast, an incoherence that OPEC+ mirrors by hiking output into a conflict that should command restraint.

Rystad Energy estimates the total repair cost for Gulf energy infrastructure at up to $58 billion, revised upward from $25 billion in March. Oil and gas facilities alone account for up to $50 billion. Full LNG recovery across the region could take five years, according to Rystad’s post-ceasefire assessment. But the repair bill is denominated in the very commodity whose price the war has failed to elevate. At $65 per barrel — the EIA’s 2027 forecast — the economics of multi-billion-dollar infrastructure restoration in a sanctioned, conflict-affected jurisdiction become prohibitive. The damage may prove semi-permanent not because it is irreparable but because the revenue to fund repairs no longer exists at prevailing prices.

The 1986 oil price collapse offers a structural analogy. Saudi Arabia’s decision to abandon its swing producer role and flood the market dropped prices from $27 to $10 within months, devastating producers who depended on high prices to fund state budgets. In 2026, the flood comes not from a deliberate Saudi strategy but from the collision of OPEC+ unwinding, non-OPEC growth, and a war that has knocked supply offline without tightening the market. Thirty-four million barrels are moving on dark fleets and state tankers outside conventional tracking — enough to fill any gap the market perceives before the gap registers in price.

| Indicator | Value | Source |

|---|---|---|

| Brent crude, July 10 settlement | $76.58/bbl | Bloomberg |

| Brent, March 18 post-South Pars strike | ~$108/bbl | Al Jazeera / Iran International |

| EIA Brent forecast, Q4 2026 | $70/bbl | EIA July 2026 STEO |

| EIA Brent forecast, full-year 2027 | $65/bbl | EIA July 2026 STEO |

| IEA projected 2027 surplus | ~5 mb/d | IEA June 2026 OMR |

| OPEC+ monthly hike, August 2026 | 188k bpd (6th consecutive) | OPEC+ |

| Saudi fiscal breakeven | $86.60/bbl | IMF |

| Gulf infrastructure repair cost | Up to $58B | Rystad Energy |

| South Pars daily production value | $272M | NS Energy Business |

| LNG cumulative loss, 2026–2030 | ~120 bcm | Columbia CGEP / Rystad |

What Does Asaluyeh Tell Markets About the Next Strike?

The July 10 strikes establish that the United States is willing to operate within the security perimeter of South Pars — the world’s most valuable energy asset — without targeting the processing facilities directly. This is a proximity threshold, not yet a destruction threshold, but it repositions Trump’s March 19 threat to destroy “the entirety of the South Pars Gas Field” as a demonstrated operational capability rather than rhetorical escalation. The gap between striking within kilometres of a facility and striking the facility itself is measured in targeting decisions, not logistics.

The Stimson Center’s March framing — energy infrastructure as a primary instrument of coercion — now applies to American operations as well as Israeli ones. The US has demonstrated it can place ordnance within the South Pars industrial zone while maintaining the formal distinction between military targets and energy infrastructure. Whether that distinction survives the next IRGC escalation depends on a calibration no one in Washington has publicly defined.

For markets, Asaluyeh offers a new calibration point of its own. If a US strike on the perimeter of the world’s largest gas field cannot move the price of oil, the threshold for a price-moving event has shifted upward and may now require a scenario — direct destruction of South Pars processing, full Hormuz closure, or both — that lies beyond what any combatant has yet attempted. A direct hit on South Pars processing facilities remains untested. But the market has already absorbed the Israeli precedent of direct South Pars damage in March and reversed the price impact within weeks. The asymmetry between escalation and price has inverted: the strikes keep getting closer to energy infrastructure and the price keeps falling.

For Saudi Arabia, the signal is the most uncomfortable of all. The kingdom sits at the intersection of every pressure generated by this conflict: a war it partially hosts but cannot end, an oil price below its fiscal breakeven, a defence architecture dependent on US systems whose resupply has become a coercive instrument, and a competitor whose energy infrastructure is being degraded in ways that should benefit Saudi market share but cannot overcome the barrel-price floor. South Pars degradation may eventually shift the global gas balance toward Saudi Arabia as the Jafurah field enters production. But “eventually” is funded by current revenue. And current revenue is $76.58 per barrel and falling. Trump’s July 13 declaration of a 20 percent Hormuz cargo toll adds a third pressure layer — an analysis of Trump’s 20% Hormuz toll and Saudi Arabia’s $59 million daily exposure details how the US fee stacks on Iran’s PGSA charge against barrels Riyadh cannot reroute through Yanbu.

Frequently Asked Questions

Has the US previously struck Iranian energy infrastructure?

The last US military strike on Iranian energy infrastructure was Operation Praying Mantis on April 18, 1988, when US Navy forces destroyed the Sassan and Sirri oil platforms in the Persian Gulf in retaliation for the mining of USS Samuel B. Roberts. The July 10, 2026 strikes near Asaluyeh represent the first time in 38 years that US military operations have occurred in the immediate vicinity of major Iranian energy processing facilities. The distinction between the two cases is target scale: Sassan and Sirri were small offshore platforms producing a few thousand barrels per day, while South Pars processes 70 to 75 percent of Iran’s total domestic gas supply.

How much of South Pars output reaches international markets?

Virtually none. Three planned LNG export projects tied to South Pars — Iran LNG, NIOC LNG, and Pars LNG — were cancelled or indefinitely suspended between 2010 and 2015 under sanctions pressure. Iran’s only functioning gas export from the field is a pipeline to Turkey carrying approximately 10 billion cubic metres per year, frequently disrupted by Kurdish militant attacks in eastern Anatolia. South Pars output is consumed almost entirely by Iran’s domestic power grid, industrial sector, and residential heating network. Full destruction of the field would be catastrophic for Iran’s internal economy but would remove almost zero molecules from international gas trade — a structural fact that partially explains the market’s muted response to strikes in the target zone.

Could military damage to South Pars affect Qatar’s North Dome production?

The geological risk is real but operates on a timeline of years rather than days. South Pars and North Dome share reservoir pressure at 300 to 400 bar across a single geological formation, but Qatar’s production wells are drilled from separate surface infrastructure on the Qatari side of the maritime boundary. The immediate cross-border risk is environmental — uncontrolled methane releases from damaged Iranian wellheads could alter reservoir dynamics over time — rather than a direct production impact. Qatar’s North Dome output of approximately 77 billion cubic metres per year has not been affected by either the March Israeli or July US strikes. Qatar’s LNG losses stem from the separate Ras Laffan facility damage, not reservoir effects.

Does Saudi Arabia have gas reserves comparable to South Pars?

Saudi Arabia’s Jafurah unconventional gas field holds an estimated 200 trillion cubic feet of reserves — substantial but roughly 40 percent of South Pars’s 500 trillion cubic feet in place. Aramco plans to invest over $100 billion in Jafurah development through 2030, targeting 2 billion cubic feet per day of sales gas. The strategic purpose differs fundamentally: Jafurah is designed to displace crude oil currently burned for domestic power generation, freeing barrels for export rather than serving as an export gas play. Saudi Arabia currently flares or reinjects significant volumes of associated gas. Jafurah is a fuel-switching and decarbonisation project, not a competitor to South Pars in the traditional sense.

When was the last time a military strike on energy infrastructure failed to raise oil prices?

The July 10 case appears to be without direct precedent. The January 2020 Iranian missile strikes on Ain al-Asad air base in Iraq produced a brief oil spike that reversed within hours, but those targeted military rather than energy infrastructure. The September 2019 Abqaiq-Khurais drone attack produced a nine-dollar spike ($60 to $69) that reversed in two weeks once Saudi Arabia restored production. In every documented case involving energy targets — the 1990 Iraqi invasion of Kuwait, the Iran-Iraq “tanker war” of 1984-1988, the Abqaiq attack — some upward price response was recorded. The absence of any upward movement on July 10 reflects a market in which structural oversupply has broken the historical relationship between energy infrastructure targeting and commodity pricing. That structural decoupling continued through July: when CENTCOM disabled the M/T Belma on July 15, Saudi Arabia’s OSP cut showed how Riyadh priced its oil during the blockade — treating the removal of Iranian and Russian supply as a volume opportunity rather than a market shock.