RIYADH — The International Monetary Fund cut Saudi Arabia’s 2026 real GDP growth forecast to 1.7 percent on July 8 — the third consecutive downgrade in six months, from 4.5 percent in January to 3.1 percent in April to a number now less than half what the economy posted in 2025. The revision, published in the Fund’s July World Economic Outlook Update, explicitly attributes the loss to war-related disruption of oil exports and non-oil activity including logistics, transport, and tourism.

The Fund simultaneously raised its 2027 Saudi growth projection to 5.5 percent, up from 4.5 percent in April — but attached a condition that transforms the upgrade from a forecast into a deadline. IMF Chief Economist Pierre-Olivier Gourinchas told reporters the rebound assumes “the Strait of Hormuz will begin reopening in mid-July, with conditions gradually returning to their prewar state by March 2027,” a timeline no party to the conflict has endorsed and that Brent crude, trading twelve dollars below the Fund’s own embedded price assumption, has already begun to undercut.

Table of Contents

Three Cuts in Six Months

In January 2026, the IMF projected Saudi Arabia would grow at 4.5 percent — a rate consistent with the 4.5 percent the Kingdom actually posted in 2025, according to the Fund’s own Article IV mission completed in May. By April, with war disruptions already visible in shipping insurance markets and oil export data, the Fund cut the figure to 3.1 percent, citing “oil GDP downgraded by a little bit over 3 percentage points, reflecting lower production related to disruptions from the war.” The July update brought it down again, with the cumulative six-month revision — 2.8 percentage points — now larger than the forecast itself.

| Forecast | 2026 Growth (%) | 2027 Growth (%) | 2026 Revision (pp) |

|---|---|---|---|

| January 2026 WEO | 4.5 | — | — |

| April 2026 WEO | 3.1 | 4.5 | −1.4 |

| July 2026 WEO Update | 1.7 | 5.5 | −1.4 |

The regional picture is considerably worse. The IMF slashed its 2026 Middle East growth forecast to 0.7 percent, down 1.2 percentage points from April, with Iraq, Kuwait, and Qatar — economies with near-total dependence on Hormuz for hydrocarbon exports — facing what the Fund described as “sharp contractions” in 2026 before double-digit rebounds in 2027, according to AGBI. Saudi Arabia’s 1.7 percent, by that measure, represents relative resilience within a region in acute distress — a distinction the Fund itself acknowledged, noting that the Kingdom “has been able to absorb much of the shock thanks to its more diversified export routes.”

The Article IV mission, led by Azim Sadikov between April 28 and May 13, described an economy “proving resilient in the face of the war” but conceded the conflict had “disrupted its momentum, curtailing oil exports and weighing on non-oil activity and confidence.” The estimated capacity loss from the Hormuz closure alone exceeds 10 million barrels per day of oil and approximately 500 million cubic metres per day of natural gas across the region, according to the WEO Update — volumes no pipeline network can replace, and disruptions the Fund says extend well beyond crude into “logistics, transport and tourism,” the sectors Riyadh had built as its non-oil growth engine.

What Does the Rebound Require?

The 5.5 percent growth the IMF projects for Saudi Arabia in 2027 is not a forecast in the conventional sense but a conditional scenario built on an assumption Gourinchas spelled out at the July 8 press briefing. The baseline assumes Hormuz begins reopening this month and returns to its prewar state by March 2027 — giving the Kingdom roughly eight months to see the strait fully normalised, a process requiring not just a cessation of hostilities but the dismantling of Iran’s naval posture, the restoration of war-risk insurance from the current 2 percent of hull value (eight times pre-crisis levels) to commercial norms, and the return of shipping traffic from 27 AIS-tracked vessels per day to the 84-ship baseline that prevailed before Hormuz recorded zero transits.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The Strait of Hormuz will begin reopening in mid-July, with conditions gradually returning to their prewar state by March 2027.

Pierre-Olivier Gourinchas, IMF Chief Economist, July 8, 2026

The PGSA — the Persian Gulf Shipping Agreement — adds a deadline within the deadline. Its $253 million outstanding liability, accruing at $5.5 million per day, reaches its August 18 expiry squarely within the window the IMF assumes reopening begins, and if that date passes without resolution, the legal and insurance framework governing strait transit enters uncharted territory at the precise moment the Fund’s model requires it to normalise.

The price assumption buried in the forecast compounds the risk. The Fund’s commodity price baseline was locked using market data as of June 10, implying an average oil price of $89 per barrel for 2026, confirmed in the WEO press briefing. Brent crude closed July 9 at $76.58 — having failed to recover the war premium even after the Asaluyeh strike — meaning the actual price environment is already $12 per barrel below the assumption underpinning the IMF’s numbers. The US Energy Information Administration’s Short-Term Energy Outlook projects Brent averaging $65 per barrel in 2027, a figure that would gut the fiscal basis of even the most optimistic growth scenario. At Saudi Arabia’s IMF-calculated fiscal breakeven of $86.60 per barrel — or the Bloomberg composite of $108 to $111 when PIF off-balance-sheet spending is included — neither the current spot price nor the forward curve can support the revenue base the 5.5 percent rebound requires.

The Deficit That Ate the Budget

The fiscal position makes the growth downgrade tangible in a way that percentage points alone cannot. Saudi Arabia recorded a deficit of SAR 125.7 billion ($33.5 billion) in Q1 2026, according to Ministry of Finance data analysed by the Arabian Gulf States Institute — the largest quarterly shortfall on record, consuming 76 percent of the full-year SAR 165 billion deficit projection in 90 days. The December 2025 budget, built at SAR 1.285 trillion in spending against SAR 1.120 trillion in revenue, was assembled on pre-war assumptions that have since collapsed alongside the oil price and export volumes.

The spending breakdown tells its own story: Q1 military expenditure rose 26 percent year-on-year, goods and services surged 52 percent, subsidies jumped 170 percent, and investment-project outlays climbed 56 percent, according to AGSI analysis — a wartime spending pattern coexisting with 1.7 percent GDP growth. Goldman Sachs estimates the war-adjusted full-year deficit will reach 6.6 percent of GDP, roughly double the government’s official 3.3 percent target. At the Q1 run rate, the annualised deficit approaches SAR 500 billion — more than three times what the budget anticipated.

Oil production has compounded the revenue squeeze, falling from approximately 10 million barrels per day pre-war to 6.879 million bpd by April, according to AGSI data, while Saudi oil exports to Asian markets dropped 38.6 percent in Q1 based on Kpler tracking. Aramco’s free cash flow now covers just 0.85 times its dividend obligation, meaning the state oil company is effectively borrowing to maintain shareholder returns. Public debt rose SAR 150 billion in 90 days, and the NEOM megaproject’s 2026–2030 construction phase has been cancelled outright, saving an estimated $16 billion in what reads less as fiscal prudence than forced triage. The OPEC+ quota hikes Saudi Arabia cannot afford continue regardless, with a fifth consecutive 188,000 bpd increase set for August into a market already carrying an IEA-estimated 3.84 million bpd surplus.

Can the Export Bypass Absorb the Loss?

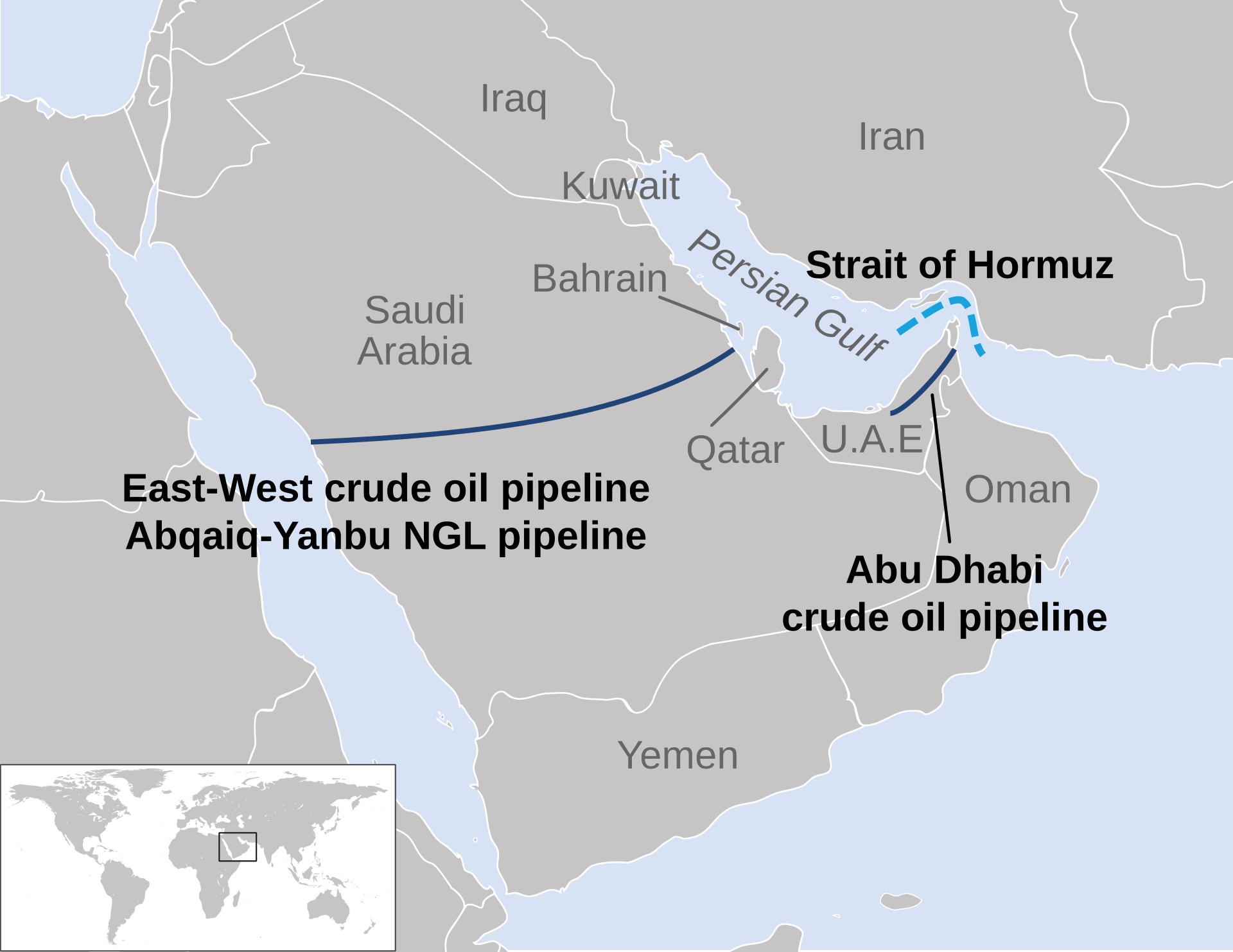

The IMF credits Saudi Arabia’s “diversified export routes” as the primary reason the Kingdom’s 1.7 percent figure is not a contraction, and as far as that goes, the Fund is correct. The Petroline East-West pipeline, running from Abqaiq on the Gulf coast to Yanbu on the Red Sea, hit its physical maximum of 7 million barrels per day on March 11 after an emergency conversion of NGL capacity, bypassing Hormuz entirely. But pipeline throughput and port throughput are not the same constraint — Yanbu’s loading infrastructure is physically capped at 3 to 4 million bpd under wartime conditions, according to Vortexa and Argus estimates, which means the bypass the IMF credits as a buffer is already running at its operational ceiling with no expansion path available on any timeline relevant to the Fund’s 2027 rebound window.

The demand side is eroding in parallel. Aramco’s August Arab Light Official Selling Price fell to negative $1.50 versus the Oman/Dubai benchmark, down from a $19.50 premium at the May peak — a $21-per-barrel collapse in pricing power within 60 days that reflects buyer resistance as much as oversupply. Sinopec, Saudi Arabia’s largest single crude customer, has posted zero Saudi purchases for the second consecutive month. Net foreign direct investment fell 2.4 percent year-on-year in Q1 to $6.1 billion, running at a fraction of the Ministry of Investment’s $46 billion annual target. The buffer exists, but it is full, and the demand for what flows through it is shrinking.

The Iran Inversion

The same July WEO Update that cut Saudi Arabia’s forecast by 1.4 percentage points raised Iran’s 2026 growth projection by 0.7 points to 5.4 percent, citing “some relaxation of export restrictions and better results for exports in March and April,” according to The National. The asymmetry is not incidental — Iran’s upward revision derives from export performance that is independent of Hormuz reopening, meaning the country that imposed the strait closure is recovering on terms that do not require the same condition the IMF has set as the prerequisite for Saudi Arabia’s rebound. Tehran has no economic incentive to validate the Fund’s March 2027 normalisation timeline before that date arrives, and every incentive to let the deadline lapse.

The structural gap extends beyond headline growth rates. Saudi Arabia faces a fiscal breakeven shortfall of roughly $10 per barrel on the IMF’s on-budget calculation and more than $30 per barrel on the Bloomberg composite — gaps that widen with every week of constrained production. Iran, operating under a lower cost structure and benefiting from resumed sales facilitated by what the IMF calls export-restriction relaxation, is running a trajectory that improves the longer Hormuz stays constrained. The Fund’s own earlier analysis identified the tension between needing Hormuz closed for its price model and open for its growth model; the July update resolves that contradiction by splitting the outcome between the two countries, with the Kingdom absorbing the growth cost of closure while Iran captures the export benefit of partial reopening through alternative routes.

Background

Saudi Arabia’s GDP has traced wide swings in recent years — 8.7 percent growth in 2022 on post-pandemic demand and oil prices above $100, negative 0.8 percent in 2023 under voluntary OPEC+ production cuts, a modest 1.3 to 1.8 percent in 2024 with oil GDP contracting 4.4 percent, and then 4.5 percent in 2025 as quota unwinding and non-oil acceleration converged. The 2025 outturn exceeded the Fund’s own prior forecast of 4.0 percent, which makes the collapse to 1.7 percent a 2.8 percentage-point single-year reversal from an economy that appeared to have regained its stride.

Non-oil GDP now accounts for approximately 57 percent of total output and had been the structural story of the Vision 2030 era, with the transformation programme targeting sustained 4 to 5 percent annual growth in those sectors to meet employment and revenue goals. The July downgrade confirms that the conflict has penetrated the sectors Riyadh spent a decade building as insulation against precisely this kind of commodity shock — not just a war on oil revenue but a war on the diversification model that was supposed to make the oil price irrelevant.

The Brent price trajectory the IMF embedded in its revised forecasts has since encountered a further test: a 10-day ceasefire proposal announced on July 21 includes a Hormuz reopening condition that would unlock approximately $1.1 billion per day in collective GCC oil revenue. An analysis of how a flat Brent price signals market confidence in the ceasefire — and why that confidence could unwind puts the IMF’s 1.7 percent growth assumption in the context of a Hormuz reopening that Saudi Arabia cannot negotiate directly but cannot afford to see fail.

Frequently Asked Questions

How does Saudi Arabia’s 1.7 percent compare to other Gulf states?

Saudi Arabia’s growth forecast, while sharply reduced, is the least severe among major Gulf oil exporters. The IMF projects Iraq, Kuwait, and Qatar will suffer “sharp contractions” in 2026, with double-digit rebounds in 2027, reflecting their near-total dependence on Hormuz transit for hydrocarbon exports, according to AGBI. Saudi Arabia’s Petroline bypass, despite its capacity constraints, is the structural differentiator that keeps the Kingdom’s number positive where its neighbours face outright contraction. The broader Middle East region was cut to 0.7 percent growth for 2026, with a projected 6.5 percent rebound in 2027, per The National.

What did the IMF say about Saudi Arabia’s financial reserves?

The Fund’s Article IV mission, completed in May 2026, assessed that “the Saudi economy benefits from solid buffers, supported by the strength of its fundamentals, including low levels of government debt, ample reserves, the strong financial position of the Public Investment Fund, and the resilience of the banking sector.” PIF assets under management stood at $1.21 trillion at end-2025, up 5 percent year-on-year, with an 80 percent domestic allocation target raised from the previous 70 percent. The language suggests the Fund views Saudi Arabia as having balance-sheet depth to absorb the war’s costs — but says nothing about the duration that balance sheet can sustain current burn rates.

How has the Saudi stock market reacted?

The Tadawul All Share Index closed at 10,854 on July 8, down 3.76 percent year-on-year — a relatively muted decline given the severity of the GDP revision and fiscal deterioration. Institutional investors appear to be pricing the conditional 5.5 percent rebound rather than the current deficit trajectory. The broader cost of the conflict has weighed on sentiment since Q1, but the market reaction suggests participants view Saudi Arabia’s buffers as providing a floor beneath equity valuations that does not exist in smaller Gulf markets where Hormuz dependence is total.

What does this mean for Vision 2030 targets?

Vision 2030 requires sustained non-oil private sector growth to deliver employment and diversification milestones by 2030. With net FDI running at $6.1 billion annually against a $46 billion ministerial target, and war disruption hitting the tourism, logistics, and transport sectors the programme depends on, the shortfall is no longer cyclical. The NEOM cancellation removed the largest single infrastructure employment driver outside of Riyadh. The IMF Article IV mission assessed the Kingdom’s buffers as solid but did not revise the Vision 2030 targets downward — a gap between the Fund’s macro assessment and the programme’s structural requirements that grows wider with every quarter at sub-target growth. On July 11, Fitch Ratings affirmed Saudi Arabia’s A+ sovereign credit rating while publishing a 2026 growth forecast of just 0.6 percent — nearly three times more pessimistic than the IMF’s own 1.7 percent, with the divergence rooted in Fitch’s more conservative assumptions about Hormuz reopening and fiscal recovery pace.