DHAHRAN — Aramco has invited banks to pitch for a stake in its sulfur storage and export terminals, a business the company values at up to $7 billion under the internal codename Project Yellowstone. Reuters reported in June 2026 that no formal sale process is expected before 2027. The company’s planned $25 billion sale of oil export terminal infrastructure — the largest single asset in its monetization pipeline — remains on hold. Sources told Reuters that Aramco is waiting for regional tensions to ease.

The Hormuz disruption that began in late February 2026 removed the Gulf’s share of global seaborne sulfur from the market — concentrating what remained behind terminals that Aramco now wants to sell. The same disruption has blocked Saudi crude exports through the strait since February. Brent has fallen 40% from its conflict peak while Saudi tankers wait.

Aramco’s first-quarter free cash flow was $18.6 billion against a declared base dividend of $21.9 billion. Saudi Arabia posted a quarterly fiscal deficit of SAR 125.7 billion. The sulfur terminals are one component of a five-asset-class infrastructure monetization pipeline Reuters and News.az have documented at up to $50 billion.

Table of Contents

- The Asset Aramco Can Sell

- Why Is Sulfur Worth Seven Billion Dollars in June 2026?

- The Pipeline That Moved and the One That Did Not

- How Does Aramco’s Leaseback Model Work?

- The Dividend Arithmetic

- What Does Sulfur Scarcity Mean for Global Fertilizer Supply?

- Disclose the Asset, Defer the Liability

- Can the Yellowstone Valuation Survive a Hormuz Reopening?

- Frequently Asked Questions

The Asset Aramco Can Sell

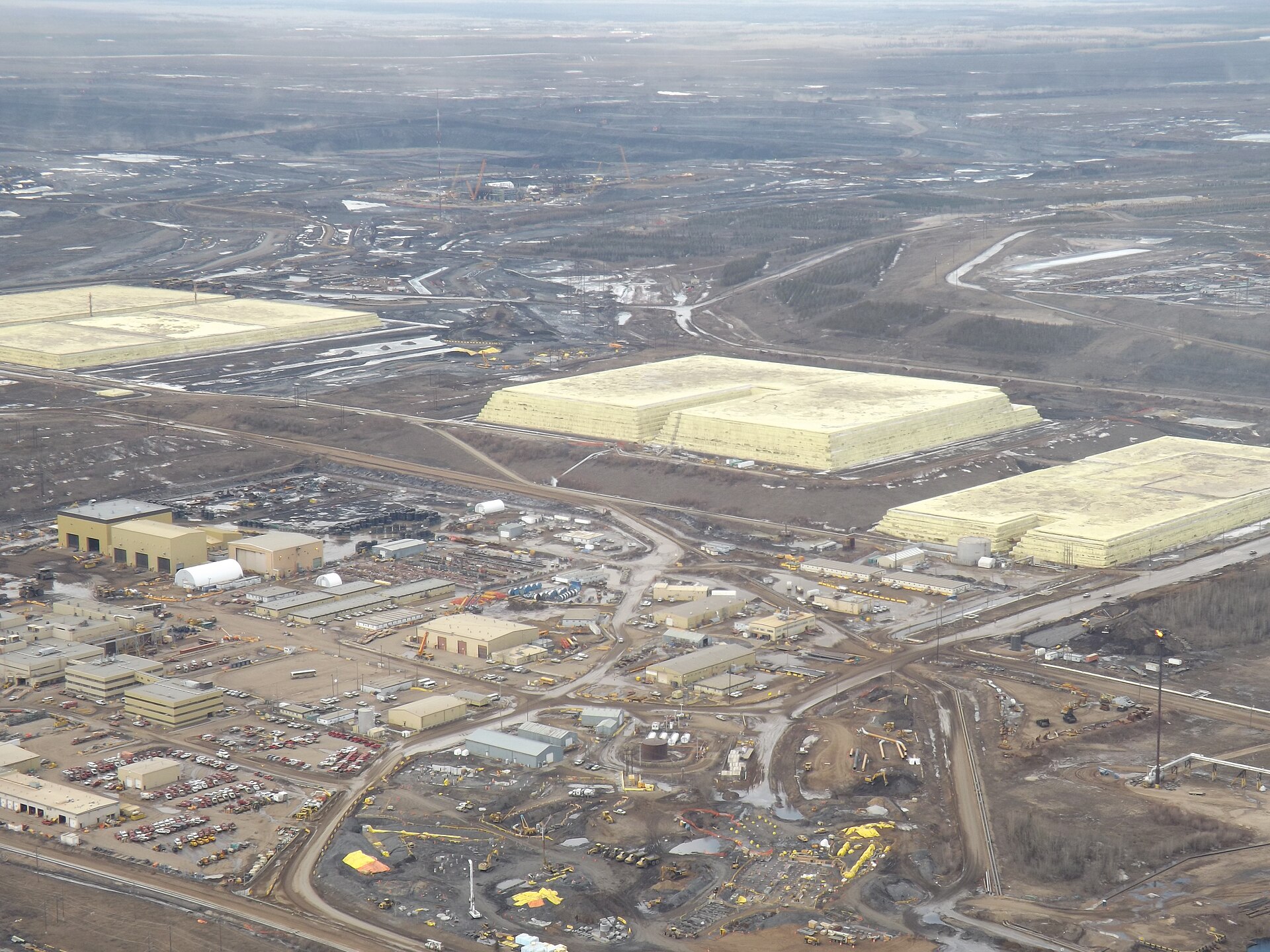

Project Yellowstone covers Aramco’s sulfur storage and export terminal network — the infrastructure used to store and ship sulfur recovered during the treatment of Saudi Arabia’s sour gas streams. Hydrogen sulfide is stripped from raw gas during processing. The recovered sulfur is stored, handled, and exported through the terminals that Aramco is now inviting investors to value.

Aramco Trading Company, which manages the commercial side of these operations, describes itself as “one of the prime exporters of sulfur in the Arabian Gulf and Red Sea region.” The terminal network handles both export logistics and storage for the domestic petrochemical sector. The physical assets — port infrastructure, covered storage, loading systems, and the rail and road connections feeding them — are the revenue-generating base that Yellowstone packages for investors.

Reuters reported that Aramco “invited banks to pitch last month for the sulphur deal, known internally as Project Yellowstone, and could raise up to $7 billion.” The total infrastructure monetization pipeline across all asset classes “could reach around $50 billion.” The sulfur terminals sit within a broader portfolio that includes oil export terminals, real estate, power plants, and a water infrastructure project coded Hydro.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The Yellowstone structure is expected to follow Aramco’s established leaseback template: sell a minority stake, retain operational control and the majority position, and offer investors contracted returns against the terminals’ cash flows. Aramco has used this structure twice before — for gas pipelines in 2021 and for Jafurah gas processing in 2025. Yellowstone would be the third.

Why Is Sulfur Worth Seven Billion Dollars in June 2026?

Sulfur is a processing byproduct with no independent supply response. No producer increases output because sulfur prices have risen — recovery rates are a function of the sulfur content of the hydrocarbons being processed, not of market signals. Stellarix, the commodities intelligence firm, described the post-Hormuz sulfur market as “a supply shock with no short-term supply response mechanism — a rare and particularly dislocating dynamic.”

The Tampa benchmark for sulfur started 2025 at $116 per long ton. By June 2026 it had reached $270 — a trajectory documented in the USGS Mineral Commodity Summaries 2026. Sulfur futures in China surged above CNY 6,700 per tonne, a record. The year-over-year increase across global benchmarks approached 170%, according to Stellarix and IMARC data.

The supply side is unambiguous. Persian Gulf countries account for 44% of global seaborne sulfur exports, per the NDSU Agricultural Trade Monitor. Kpler reported on June 4, 2026, that global sulfur exports had fallen 45% below end-February levels following the Hormuz closure. Morocco’s OCP Group — the world’s largest phosphate fertilizer exporter, dependent on roughly 3.7 million metric tons of Gulf sulfur annually — received its last Middle East Gulf cargo on April 10. OCP has since sourced Russian sulfur under constrained conditions.

The Gulf supply gap has been compounded by policy restrictions elsewhere. Russia extended its sulfur export ban through June 2026. Turkey restricted exports during the second and third quarters. China imposed its own export limitations. Qatar suspended sulfur production after facility damage earlier in the year. Each restriction further concentrates the remaining supply behind fewer export points — including the terminals that Yellowstone covers.

The infrastructure bottleneck is the commercial variable. No one can process more sulfur into the market by building new terminal capacity overnight. The constraint is physical: storage, port access, loading logistics. The terminals that control access to existing supply are the assets whose throughput economics have shifted. At $270 per long ton, the revenue per unit handled is 2.3 times what it was at $116.

The Pipeline That Moved and the One That Did Not

Aramco’s infrastructure monetization program encompasses five asset classes. Reuters and News.az reported the following breakdown:

| Asset | Estimated Value | Status (June 2026) |

|---|---|---|

| Oil export terminals | $25 billion | On hold — “waiting for regional tensions to ease” |

| Sulfur terminals (Project Yellowstone) | $7 billion | Bank pitches invited; formal process not before 2027 |

| Real estate portfolio | $10 billion | In preparation |

| Power plants | $4 billion | In preparation |

| Project Hydro (water infrastructure) | $500 million | In preparation |

The $25 billion oil terminal sale was the centerpiece of the pipeline — the largest single asset and the most directly tied to Aramco’s core crude export business. Sources told Reuters that Aramco is “waiting for regional tensions to ease before launching the process, likely in the second half of the year.” The terminals are designed to load crude for transit through Hormuz. Saudi crude has not transited the strait at commercial scale since late February. No institutional buyer will underwrite a $25 billion revenue stream predicated on strait access that does not exist.

Yellowstone, by contrast, advances into a market where the disruption has improved the asset’s commercial position. Gulf sulfur is scarce. The terminals that handle whatever supply remains are operating at premium throughput economics. Aramco invited banks to pitch in May, four months into the disruption.

The remaining three asset classes — real estate, power plants, and water infrastructure — are less directly connected to the Hormuz disruption and appear to be proceeding on independent timelines. The real estate portfolio, valued at $10 billion, encompasses non-hydrocarbon properties. Project Hydro, at $500 million, covers water desalination and distribution infrastructure. Neither depends on strait access or commodity war premiums for its base valuation.

How Does Aramco’s Leaseback Model Work?

Aramco’s infrastructure monetization model sells a minority stake — typically 49% — in physical infrastructure to institutional investors while retaining operational control and the majority position. Investors receive contracted, bond-like returns backed by the infrastructure’s cash flows over terms of 20 years or more. Aramco receives upfront liquidity without ceding control of assets embedded in its hydrocarbon processing chain.

The first iteration was the 2021 gas pipeline deal. A BlackRock-led consortium paid $15.5 billion for a 49% stake in Aramco’s gas pipeline network, structured as a 20-year lease. Aramco continued operating the pipelines and retained 51% ownership. The consortium collected contracted cash flows indexed to throughput.

The second iteration was the 2025 Jafurah leaseback. BlackRock’s Global Infrastructure Partners paid $11 billion for a stake in gas processing infrastructure at the Jafurah field — one of the largest unconventional gas plays in the Middle East, with 229 trillion standard cubic feet of raw gas and 75 billion stock tank barrels of condensate. White & Case, which served as legal counsel, described the transaction as “landmark.” Chinese banks provided lending for the deal, though Chinese sovereign and state-owned funds largely declined to participate as equity investors — a distinction Reuters reported at the time, and one that narrows the effective buyer universe for Gulf infrastructure assets with geopolitical risk embedded in the valuation.

A complication has surfaced in the original deal. Bloomberg and Investing.com reported in 2025 that BlackRock was in talks to sell its 2021 gas pipeline stake back to Aramco. If completed, Aramco would be buying back assets from the first iteration of the leaseback model while simultaneously selling new assets in the third. The 2021 deal was struck in a different rate environment and a pre-disruption geopolitical context. The exit dynamics — what happens when the infrastructure fund’s hold period ends, or when market conditions shift — are being tested for the first time.

Yellowstone would apply the same template to the sulfur terminals. Aramco would retain operational control. The buyer would receive returns linked to terminal throughput volumes, storage fees, and loading economics — returns calculated against sulfur prices that have more than doubled since January 2025.

The Dividend Arithmetic

Aramco’s Q1 2026 results quantified the fiscal pressure that the infrastructure monetization pipeline is designed to address. Free cash flow was $18.6 billion. The declared base dividend was $21.9 billion. The coverage ratio — 0.85x — meant Aramco distributed $3.3 billion more in dividends than it generated in cash during the quarter.

The gearing ratio rose to 4.8% at March 31, 2026, from 3.8% at the end of 2025. Aramco’s Q1 interim report attributed the increase to a $15.8 billion working capital build. The company’s balance sheet absorbed the shortfall rather than its dividend policy.

The crude pricing environment has compressed further since Q1 close. Aramco’s July OSP for Arab Light to Asia was cut $6 per barrel — the largest reduction since 2022. The premium collapsed from $19.50 to $9.50 between May and July, a 51% decline in the markup Aramco charges above the benchmark. The OSP was published June 8 — seven days before the MOU signing, eleven days before the Geneva ceremony. It priced a market where Saudi crude could not reach buyers through Hormuz and where Asian refiners had alternatives.

Saudi Arabia’s fiscal position mirrors the corporate shortfall. The Q1 deficit of SAR 125.7 billion ($33.5 billion) already exceeded the full-year plan. The revised full-year deficit projection stands at SAR 165 billion ($44 billion), more than double the original SAR 65 billion. The fiscal breakeven — the oil price required to balance the budget — remains at $108-111 per barrel. Brent has traded around $80.

Kuwait’s production ramp — 1.4 million barrels per day following its June 18 force majeure lift — has added supply into the same market. The IEA projects a surplus reaching 3.7 million barrels per day for the full year, with further deterioration expected if OPEC+ discipline fractures. Aramco’s dividend coverage is under pressure from forces that extend well beyond the Hormuz disruption itself.

The $50 billion infrastructure pipeline fills a specific role in this arithmetic. It converts physical assets into upfront cash that can supplement operating cash flow and support dividends at a time when the core crude export business cannot cover them alone. Yellowstone’s $7 billion represents 14% of the pipeline. The $25 billion oil terminal sale — paused until regional tensions ease — would cover more than a full year of the current quarterly FCF shortfall.

What Does Sulfur Scarcity Mean for Global Fertilizer Supply?

Sulfur is the first input in a processing chain that ends in global food production. Sulfuric acid, produced from elemental sulfur, is the primary reagent for phosphate rock processing into DAP and MAP fertilizers. Without adequate sulfuric acid supply, phosphate fertilizer production falls — a constraint that cannot be resolved by substitution at the processing stage.

The FAO’s Chief Economist warned in 2026 of “severe global food security risks from disruption to Strait of Hormuz trade corridor.” IFPRI published an analysis of “the Iran war’s impacts on global fertilizer markets and food production.” Both assessments identified the sulfur-to-fertilizer chain as the primary transmission mechanism from the Hormuz disruption to agricultural markets.

OCP Group — based in Morocco, the world’s largest phosphate fertilizer exporter — processes approximately 3.7 million metric tons of Gulf sulfur annually. Its last Middle East Gulf cargo arrived April 10; it has since relied on Russian supply, but Russia’s own sulfur export ban, extended through June, constrains that alternative. India, another major sulfur importer for fertilizer production, has also scrambled for non-Gulf sources, according to Morocco World News reporting in March 2026.

Fertilizer prices have responded to the physical absence of Gulf sulfur. The benchmark exceeded $650 per tonne — up roughly 30% since the disruption began. Urea reached $850 per metric ton in April 2026, an 80% increase from February levels, per World Bank data.

| Indicator | Pre-Disruption | Post-Disruption (Jun 2026) | Change | Source |

|---|---|---|---|---|

| Tampa sulfur benchmark | $116/long ton (Jan 2025) | $270/long ton | +133% | USGS |

| Sulfur futures (China) | — | >CNY 6,700/tonne | Record high | Stellarix/IMARC |

| Global sulfur exports vs. Feb | Baseline | -45% | -45% | Kpler |

| Fertilizer benchmark | ~$500/tonne | $650+/tonne | ~+30% | World Bank |

| Urea | ~$472/metric ton | $850+/metric ton | +80% | World Bank |

| OCP last Gulf sulfur cargo | Regular deliveries | April 10, 2026 | Ceased | Kpler |

Aramco is inviting investors to value terminal infrastructure that controls access to a commodity whose scarcity has been documented as a food security risk by both the FAO and IFPRI. The terminals are worth $7 billion in a market where the sulfur passing through them reaches fewer buyers at higher prices.

Disclose the Asset, Defer the Liability

Aramco’s public posture toward Project Yellowstone contrasts with its treatment of Sadara Chemical Company, the 65/35 joint venture with Dow that represents its most visible distressed liability. Yellowstone is a disclosure event: Aramco invited banks, allowed Reuters to report the codename and valuation range, and positioned the sulfur terminals within a broader monetization pipeline.

Sadara is a silence event. The company’s 2025 annual report recorded a net loss of SAR 5.793 billion. Accumulated losses exceeded 100% of share capital. The $3.7 billion in syndicated debt — held across a 28-bank consortium — hit its grace period expiry on June 15, 2026, with no filing from Aramco, Dow, or the lenders. Dow’s most recent public characterization of the exposure was that “tail risk” had been “removed” — applied to $292 million in guarantees linked to an entity whose losses exceed its entire capital base. Aramco has not offered a corresponding characterization.

The sulfur terminals are war-premium assets: their value is elevated because the disruption has concentrated global supply through fewer export points, and Aramco is surfacing that value for investors. Sadara is a war-compounded liability: the petrochemical joint venture’s losses have deepened as regional conditions have deteriorated.

The Jafurah and gas pipeline leasebacks were transparent transactions in stable markets — infrastructure deals backed by long-cycle hydrocarbon fundamentals. Yellowstone packages infrastructure whose commercial position has been reshaped by a four-month-old conflict. Sadara’s $3.7 billion debt maturity passed during the same conflict without a single regulatory filing from Aramco, Dow, or the 28-bank syndicate.

Can the Yellowstone Valuation Survive a Hormuz Reopening?

The $7 billion valuation attributed to Project Yellowstone reflects sulfur market conditions in mid-2026 — record prices and a 45% supply contraction driven by the Hormuz closure. If the strait reopens and Gulf sulfur exports resume at pre-disruption volumes, the supply shock unwinds. Tampa benchmarks would decline toward pre-disruption levels. The terminal infrastructure remains physically unchanged; the revenue per unit handled does not.

Aramco’s decision not to launch a formal sale before 2027 positions the deal at a moment of maximum uncertainty about the strait’s status. Pentagon assessments have placed the full mine clearance timeline at up to six months. The strait has so far opened for Iranian crude only — NITC tankers transited the Qeshm-Larak corridor under PGSA exemption while Saudi and other Gulf crude remained blocked. The MOU signed in Geneva opens a 60-day Phase 2 negotiation window, but physical reopening to commercial traffic at pre-disruption volumes requires mine clearance, insurance market normalization, and resolution of the PGSA transit fee structure — none of which the MOU delivers on its own terms.

The sequence runs in a circle. The Hormuz disruption reduces Gulf hydrocarbon processing. Reduced processing means less recovered sulfur. Less sulfur supply inflates prices. Inflated prices inflate terminal valuations. Aramco moves to monetize. If the disruption resolves, the circle breaks at the first link. Processing resumes, sulfur supply normalizes, and the 2027 term sheet prices a different market than the 2026 bank pitch.

Iran’s PGSA introduces an additional variable. The same disruption driving sulfur scarcity generates fee revenue for Tehran — an estimated $1 per barrel on all non-Iranian transit through the strait, administered by an entity that was OFAC-designated on May 27 and EU-designated on June 8. The 300-plus non-Iranian vessels that have filed pre-clearance with the PGSA since May represent a compliance surface that intersects with Aramco’s crude export logistics and, through processing volumes, with the sulfur throughput that underwrites Yellowstone’s cash flow projections.

For a prospective buyer, the diligence question is binary. Are you pricing terminal infrastructure against a permanent shift in global sulfur logistics — fewer Gulf processing centers, persistent export restrictions from Russia and China, OCP and Indian buyers diversified away from Gulf supply? Or are you pricing a war premium that will deflate when mines are cleared, P&I clubs restore coverage, and Gulf sulfur re-enters the market at scale? The 2021 gas pipeline deal and the 2025 Jafurah leaseback priced stable hydrocarbon infrastructure with multi-decade fundamentals. Yellowstone prices a byproduct terminal network in a market shaped by a conflict that began in February.

Frequently Asked Questions

What specific infrastructure does Project Yellowstone include?

Yellowstone covers Aramco’s sulfur storage and export terminal network, including port loading facilities, covered and open storage areas, and the logistics chain connecting gas processing plants to export berths. Aramco Trading Company operates the commercial side across both Arabian Gulf and Red Sea export points — a geographic spread that gives the terminal system access to Atlantic and Asian sulfur markets through different shipping routes. The Red Sea terminals, which do not depend on Hormuz transit, have carried additional strategic value since the strait closure, as they provide an alternative export path for sulfur produced at processing facilities connected to the western pipeline network. This dual-coast positioning is part of the $7 billion valuation that Reuters reported — it partially insulates the asset from the Hormuz disruption risk that has frozen the oil terminal sale.

Has Aramco monetized byproduct infrastructure before?

Aramco’s prior leaseback transactions — the 2021 gas pipeline deal and the 2025 Jafurah leaseback — covered primary hydrocarbon infrastructure, not byproduct handling. Yellowstone would be the first time Aramco applies the model to a secondary processing output. The distinction matters commercially: sulfur terminal revenues are a function of gas processing throughput at upstream facilities, meaning the buyer’s returns depend not only on terminal operations but on processing decisions made elsewhere in Aramco’s value chain. If Aramco reduces sour gas processing at any connected facility — whether for maintenance, field decline, or market reasons — the sulfur volume flowing through Yellowstone’s terminals declines proportionally, and with it the contracted cash flows backing investor returns. This upstream dependency did not apply to the gas pipeline or Jafurah deals, where the infrastructure itself was the production asset.

Why did Aramco choose the codename Yellowstone?

Neither Aramco nor Reuters has explained the codename publicly. In investment banking convention, project codenames are selected to be memorable and unrelated to the deal’s substance in order to maintain confidentiality during the pitch process. Yellowstone National Park — situated above one of the world’s largest volcanic sulfur deposits, with active hydrothermal features that release sulfur dioxide and hydrogen sulfide — may or may not be a deliberate reference. What Reuters’s sourcing confirms is that the codename was internally established before the bank pitch began, indicating that Aramco’s advisory team had structured the deal concept and preliminary valuation framework prior to inviting external interest.

How does the PGSA transit fee affect Yellowstone’s economics?

Iran’s Persian Gulf Security Authority charges non-Iranian vessels transiting the Qeshm-Larak corridor an estimated $1 per barrel. Whether this fee structure extends to sulfur carriers, LNG vessels, and other non-crude commodity shipments has not been publicly clarified by the PGSA or Iranian authorities. If PGSA fees are applied to sulfur export cargoes from Aramco’s Gulf-side terminals, they would add a per-shipment cost that compresses the terminal’s net throughput economics. The PGSA’s OFAC designation (May 27) and EU designation (June 8) create a sanctions compliance layer for any Western infrastructure investor evaluating Yellowstone returns. Approximately 95% of the global tanker fleet carries EU-originated insurance, meaning the designation has direct implications for vessel traffic serving Yellowstone’s Gulf export berths. A buyer conducting diligence on Yellowstone’s Gulf terminals would need to model both the PGSA fee exposure and the sanctions risk — neither of which applies to the Red Sea terminals within the same portfolio.