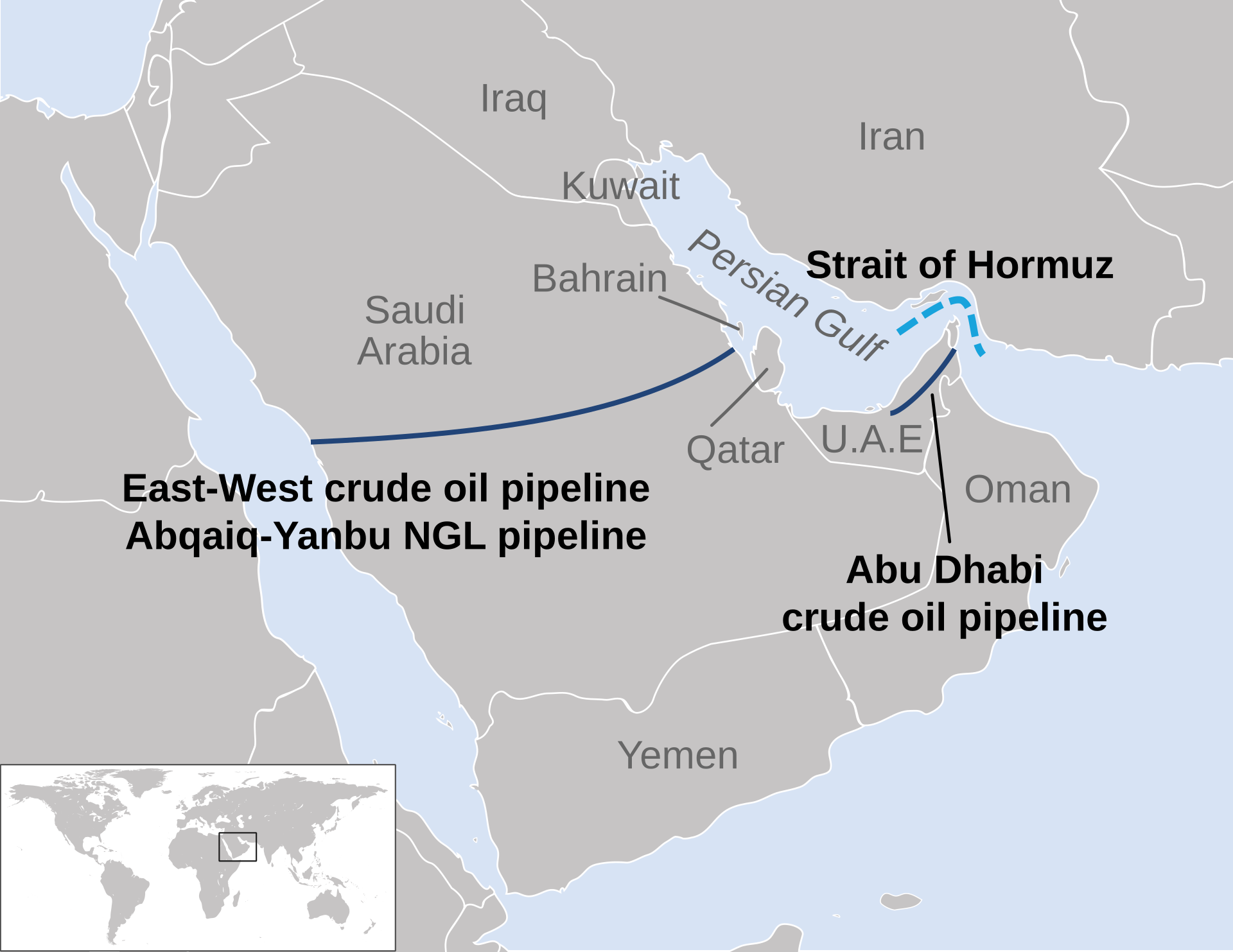

JEDDAH — Saudi Arabia spent the better part of a decade and tens of billions of dollars building a pipeline to escape the Strait of Hormuz. On April 12, when the East-West Pipeline resumed pumping seven million barrels a day toward the Red Sea port of Yanbu after repairs to the pumping station struck by an IRGC drone, that escape route still ended eighteen miles from Houthi territory.

The bypass goes nowhere the Houthis cannot reach. Every barrel of crude now flowing west must sail south through Bab al-Mandeb — the narrow gap between Yemen and Djibouti — to reach Asia, which is the only remaining buyer of scale for Saudi oil. On April 13, the USS George H.W. Bush carrier strike group declined to make that transit and routed instead around the Cape of Good Hope, the first American carrier to skip the Red Sea since December 2023. Arab officials told the Wall Street Journal the following day that Crown Prince Mohammed bin Salman had personally pressed Donald Trump to lift the Hormuz blockade because Riyadh fears Iran can override the informal Houthi assurances that Saudi tankers will be spared.

That is the admission behind the diplomacy. Saudi Arabia solved the wrong chokepoint, and the Houthis now hold the pen on the Yanbu bypass the same way the IRGC holds it on Hormuz.

Table of Contents

- The pipeline to nowhere

- Why can’t Yanbu handle seven million barrels a day?

- The eighteen-mile gap every Yanbu cargo must cross

- Can Saudi Arabia trust Houthi assurances?

- What happens if Bab al-Mandeb closes?

- Why did the US carrier go around Africa?

- The third coast Saudi Arabia never built

- Is ASPIDES enough to keep the strait open?

- Frequently asked questions

The pipeline to nowhere

The East-West Pipeline was conceived in the mid-1980s as an answer to the Tanker War, when Iraqi and Iranian missiles turned the Strait of Hormuz into a graveyard for flagged tonnage. The logic was geographic: run the crude across the peninsula, load it on the other side, and leave the Strait to burn itself out. In the forty years since, that logic has been treated as axiomatic in every Saudi energy white paper. Prior Yanbu bypass analysis set out what the pipeline could and could not do at nominal capacity; the intervening eleven days have answered the question the hard way.

What has changed is the exit. When the East-West was commissioned, Bab al-Mandeb was policed by a friendly Yemeni navy, the Horn of Africa had a functioning Somali coastguard, and Iran had no maritime proxy capable of striking past the Gulf of Oman. Today the Yemeni coastline from Hodeidah to Midi is Houthi territory; the Iran-aligned movement has fired at least 178 vessels in 2024 alone, sinking four and killing nine sailors; and Tehran’s most senior foreign-policy voice now describes the strait as part of a “unified command” with Hormuz. The pipeline still works — the geography around its exit has inverted.

Saudi planners knew this. The question is why the bypass was still being publicly sold as a Hormuz insurance policy as late as the April 8 IRGC strike on the Jeddah pumping station, when every chart in the Aramco control room shows the next chokepoint sitting one sea-lane further south. The answer, in the blunt reading of the evidence, is that Riyadh has no second answer. The bypass was marketed as redundancy because admitting it was a single point of failure was politically intolerable inside a kingdom whose fiscal break-even is already twelve to eighteen dollars a barrel above spot.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Why can’t Yanbu handle seven million barrels a day?

Yanbu’s pumps can now receive seven million barrels of crude a day from the east, but its terminals cannot load that volume onto ships. Yanbu North is rated at 1.5 million bpd nominal. Yanbu South is rated at three million. The tested effective ceiling under wartime scheduling sits closer to four million — call it four-and-a-half on a day when every berth turns, every VLCC arrives on schedule, and nothing breaks. Argus Media and Maritime Executive put the gap between pipeline throughput and terminal capacity at 2.5 to 3.0 million barrels a day, which is the volume of Saudi crude that either stays in tank or never gets pumped.

The March 2026 loading book makes the constraint visible. Yanbu handled forty-seven Very Large Crude Carrier loadings in the month, against a pre-war monthly average of eleven to twelve. More than two in three of those VLCCs sat at anchorage for over thirty-six hours before berthing, according to Vortexa tracking. Security firm Diaplous flagged “elevated risk for a potential strike targeting Yanbu,” specifying “USV, UAVs, missiles, or other forms of attack” in its March client circular. Roughly thirty tankers sit in Yanbu’s approaches on any given day, inside the demonstrated strike envelope of Houthi anti-ship systems.

| Capacity layer | Nominal rating | Tested ceiling | Gap to pipeline |

|---|---|---|---|

| East-West Pipeline pump | 7.0M bpd | 7.0M bpd | — |

| Yanbu North terminal | 1.5M bpd | ~1.3M bpd | — |

| Yanbu South terminal | 3.0M bpd | ~2.8-3.2M bpd | — |

| Combined Yanbu effective | 4.5M bpd | ~4.0-4.5M bpd | 2.5-3.0M bpd short |

| March 2026 loadings | — | ~5.0M bpd gross | Floating storage |

That 2.5-million-barrel gap sits somewhere on the water. Some volumes are held in tank; some are loaded onto VLCCs that then wait at anchorage because the next berth is not clear; some are absorbed by trading houses including TotalEnergies’ Dubai desk. The April 7 Jubail debris fire at a SABIC installation is the cautionary tale — Saudi terminals are not purely exporting facilities, they are also the point at which insurance markets, shipping lines, and petrochemical downstream all learn whether the Red Sea is a supply chain or a liability.

The eighteen-mile gap every Yanbu cargo must cross

Bab al-Mandeb means “Gate of Grief” in Arabic, and the name has always been literal. The strait is eighteen miles wide at its narrowest navigable point between the Yemeni coast and Djibouti. Perim Island, controlled by Houthi forces, splits the water into two channels; the eastern channel — the one closest to Yemen — is only three kilometres wide. Eritrea holds the African shore on the western approach. Unlike Hormuz, where the US, Iran, and Israel are all non-signatories to UNCLOS and the transit passage debate at least has an internationally recognised legal framework to argue about, Bab al-Mandeb sits outside any compellable legal architecture: the Houthis are not a recognised state, Ansar Allah is not bound by maritime law, and there is no mechanism to demand safe passage from a non-state actor holding a coastline.

Every barrel loaded at Yanbu for Asian delivery must transit that gap. Yanbu to Ulsan, South Korea, is twenty-four days via the Red Sea, Bab al-Mandeb and the Suez Canal; it is fifty-four days around the Cape of Good Hope, because the largest laden VLCCs — the 300,000-plus DWT vessels that dominate Saudi export trade — cannot transit Suez northbound under their own draft, and the economics of lightering into Suez-compatible tankers at Ain Sukhna remove the premium that makes the canal competitive. The extra month on the water is absorbed either by building a larger tanker fleet — which does not exist in the global pool — or by accepting a 125 percent increase in voyage time that structurally shrinks available tonnage by the same ratio. Shipowners do not run that math for Saudi Arabia. They run it against charter rates that are already double the December 2023 baseline.

Houthi anti-ship weaponry can cover the entire strait. The Tankil anti-ship ballistic missile — an Iranian design adapted by the Houthis — has demonstrated terminal manoeuvres against moving targets. The Mandab-2 is a subsonic anti-ship cruise missile tuned to the geography of this specific waterway. Unmanned surface vessels have struck tankers on three occasions documented by UKMTO since 2023; loitering munitions have hit vessels up to 240 kilometres offshore. The strait is not a perimeter that can be policed by warships stationed at its mouth — it is a kill zone whose launch points sit on ridgelines Saudi Arabia is not at war with.

Can Saudi Arabia trust Houthi assurances?

The Wall Street Journal reported on April 14 that Saudi Arabia secured informal assurances from the Houthis that Saudi-flagged vessels would not be targeted in any Red Sea escalation. The same report contains the qualifier Riyadh itself placed in front of that assurance: Iran can override it. Arab officials briefing the paper told it plainly that the Crown Prince’s appeal to Trump over the Hormuz blockade was motivated by the fear that a unilateral Iranian order through the IRGC’s Quds Force liaison in Saada would turn a political commitment into a dead letter overnight.

The evidence that such an order can be given sits in the public record. Houthi Deputy Information Minister Mohammed Mansour told Al Jazeera in late March that closing Bab al-Mandeb is “among our options” if the war against Iran escalates, and forecast that oil would reach two hundred dollars a barrel in that scenario. He placed the statement inside a “common action plan” with Tehran. Ali Akbar Velayati, advisor to the Supreme Leader, said on April 6 that “the unified command of the Resistance front views Bab al-Mandeb as it does Hormuz.” A senior Iranian source told Reuters on April 7: “If the situation gets out of control, Iran’s allies will also close the Bab el-Mandeb Strait.”

If Iran does want to shut down Bab al-Mandeb, the Houthis are the obvious partner to do it, and their response to the Gaza conflict demonstrates that they have the capacity to do it.Adam Baron, Fellow, New America, quoted in the Wall Street Journal, April 14, 2026

Between March 28 and mid-April, Yahya Saree, the Houthi military spokesperson, announced eight missile barrages against Israeli territory — the first strikes from Yemen on Israel since the October 2025 US-Houthi ceasefire held commercial Red Sea lanes open. Commercial shipping has not yet been attacked. The pattern is a deliberate split: fire at one adversary to demonstrate arsenal and intent, hold the other target in reserve to preserve its coercive value. As the Cambridge Middle East specialist Elisabeth Kendall put it on March 29, closure would be a “nightmare scenario” that would “disrupt, if not cripple, trade toward Europe” — and the former US diplomat Nabeel Khoury noted on the same panel that the Houthis “would need only to fire at a couple of ships” to halt all Red Sea commercial traffic.

Saudi Arabia’s assurance is therefore a three-party document, of which only two parties have signed. The Houthis have given a commitment; Iran has not. The Washington Post report that the Crown Prince privately urged Trump toward ground troops and regime change in Iran reads differently in this light. If the only guarantor of Saudi tanker safety in the Red Sea is the absence of an Iranian override order, Riyadh has a structural interest in either removing the regime that can issue the order or removing the commander who would sign it.

What happens if Bab al-Mandeb closes?

Close Bab al-Mandeb and the Yanbu bypass stops being a bypass. Every barrel pumped to Yanbu for Asian markets either sits in tank, sells at a discount to Europe and the Mediterranean, or goes around the Cape — adding ten to fourteen days to the voyage and approximately one million dollars in direct costs per round trip per vessel. Brent is currently trading at ninety-three to ninety-six dollars; the Bloomberg Economics PIF-inclusive fiscal break-even for Saudi Arabia is one hundred and eight to one hundred and eleven. The kingdom is already twelve to eighteen dollars a barrel underwater on the arithmetic that funds NEOM, the 2030 portfolio, and the standing army.

Goldman Sachs puts the war-adjusted Saudi fiscal deficit at 6.6 percent of GDP, or roughly seventy-three billion dollars annually at current prices. That number was calculated against a baseline in which Hormuz was partly closed, Yanbu was compensating, and Bab al-Mandeb remained open. Close both chokepoints simultaneously — which is the condition Velayati described on April 6 — and twenty-five percent of global oil and gas supply goes offline at once. Mansour’s two-hundred-dollar forecast is not an outlier. It is the consensus reading among analysts who have modelled a simultaneous double closure; the only debate is how long the spike lasts before demand destruction resolves it.

| Scenario | Yanbu export capability | Saudi Asia-bound volume | Brent implication |

|---|---|---|---|

| Current (Hormuz blockade, Bab open) | ~4.5M bpd | ~3.5M bpd via Suez/Cape mix | $93-96 |

| Bab al-Mandeb commercial deterrence | ~3.0M bpd (insurance flight) | ~2.0M bpd Cape-routed | $115-135 (est.) |

| Bab al-Mandeb full closure | ~1.5M bpd (Europe-only) | ~0 direct Asia delivery | $150-200 (Mansour) |

| Dual Hormuz-Bab closure | ~1.5M bpd | Cape-only, weeks-delayed | $180-220 (Velayati-scenario) |

The buyer side matters as much as the seller side. Yanbu’s main offtake market is China, South Korea, Japan, and India — all of whom are on the Asian side of Bab al-Mandeb. China has its own diplomatic channel to the Houthis via the Yemen embassy re-opened in Muscat; Beijing is the only capital that can credibly ask for exemptions, and it has already used that channel to escort Qatari LNG cargoes through Hormuz in the second week of April. Saudi Arabia does not have that relationship with Ansar Allah. It has a deniable backchannel through Oman, a prisoner exchange completed in 2023, and a four-year Riyadh-Sanaa ceasefire — none of which survived the decision to align with Washington against Tehran during the current war.

Why did the US carrier go around Africa?

The USS George H.W. Bush carrier strike group, including the guided-missile cruiser USS Leyte Gulf and two Arleigh Burke destroyers, transited the Cape of Good Hope in the second week of April and was operating off the Namibian coast as of April 13, according to USNI News. Stars and Stripes confirmed the following day that it was the first American carrier to route around Africa rather than through Bab al-Mandeb since December 2023, when the Eisenhower strike group took the Suez channel into the Red Sea at the height of the earlier Houthi campaign. The Navy has not publicly explained the routing decision.

It does not need to. The operational logic is legible on any threat-estimate briefing: a Nimitz-class carrier presents a 332-metre radar signature, its embarked air wing is the highest-value maritime air asset in the US inventory, and anti-ship ballistic missiles with terminal manoeuvring capability have a non-zero probability of a mobility kill even against Aegis defence. The calculation the Pentagon ran was the same one shipowners are running: the cost of one successful hit is too high, and the marginal deterrent value of transiting the strait is too low, when the alternative route exists. The Bush’s diversion is the US Navy conceding that the deterrent posture of a carrier in the Red Sea is no longer worth the insurance premium on the hull.

That concession has a second-order effect on Saudi Arabia that has been understated in Western coverage. A carrier in the Red Sea is the only kinetic guarantor of Yanbu’s approaches; Operation ASPIDES is mandated to defensive engagement only, and the Arab Gulf’s own naval assets — corvettes and patrol craft primarily — do not have the magazine depth to sustain an interception campaign against saturation attacks. By sending the Bush around the Cape, Washington has signalled both to Riyadh and to Sanaa that the Red Sea sea-lane is no longer under direct American protection. Saudi Arabia lost its implicit umbrella on the day that routing decision was publicly confirmed.

The third coast Saudi Arabia never built

Iraq has a pipeline to the Turkish Mediterranean. The UAE has the Abu Dhabi Crude Oil Pipeline, which exits at Fujairah outside the Strait of Hormuz, and a terminal that moved a reported 1.5 million barrels a day on peak days in 2023. Saudi Arabia has the East-West, and nothing else. There is no Red Sea-to-Gulf-of-Aqaba line, no cross-border Jordanian arrangement at scale, no Tapline revival — the 1947-built Trans-Arabian Pipeline to the Lebanese coast was shuttered in 1990 and its rights of way have been built over. Israel’s Eilat-Ashkelon pipeline offered a notional workaround in the late 2010s when the normalisation tracks were live; the current war has made that route politically radioactive and physically questionable given Houthi strikes on Eilat itself.

The third-coast option that would actually matter is a pipeline to the Arabian Sea, either through Oman to Duqm or through the UAE to the Fujairah spur. Aramco has studied both; neither has moved beyond pre-feasibility. The reasons are cost — a greenfield trans-peninsula line at current steel prices would run north of forty billion dollars — and politics, because a Duqm or Fujairah-terminated Saudi export route places Riyadh’s primary revenue stream inside the customs control of a neighbour. The East-West Pipeline was built precisely because it kept the entire value chain inside Saudi sovereignty. Every proposed alternative fails that same test.

The PIF strategy document published on April 7 contains no mention of export route diversification. NEOM, the Red Sea Project, and Humain all sit on coastline that a Bab al-Mandeb closure prices out of the global supply chain. The Line has been formally suspended — its population target cut from 1.5 million to under 300,000 — but even the reduced footprint depends on the Red Sea being a functional trade artery. Saudi Arabia’s 2030 portfolio is a bet on the waterway it is currently least able to defend.

Is ASPIDES enough to keep the strait open?

Operation ASPIDES — the European Union’s maritime escort mission in the Red Sea — had its mandate extended on March 30 to run through February 2027. Eight member states currently contribute warships; France pledged ten additional hulls on March 9, bringing the standing force to roughly fifteen to seventeen escorts on a rolling rotation. The mission is commanded from the Larissa headquarters in Greece. Its rules of engagement are defensive only: the mission can intercept inbound missiles and drones but cannot strike launch sites ashore, cannot retaliate against command nodes, and cannot close Yemen’s Red Sea coastline to Houthi movement.

The mandate matters because the threat is not inbound. Houthi anti-ship systems do not need to cross into international waters to hit a vessel; a Tankil ballistic missile launched from Hodeidah can range the full 260-kilometre Yemeni coast and reach targets near Saudi Arabia’s Farasan Islands. ASPIDES can shoot the missile down. It cannot prevent the next one being fired. The mission’s own spokesperson, quoted in The War Zone on April 1, framed the posture as wait-and-react: “In the event of a resumption of Houthi attacks to merchant vessels — which remains a possibility — we are present and ready to implement our mandate.”

Ready is not enough, and the 2024 campaign showed why. Despite a combined intercept rate that ran high in percentage terms, the ASPIDES and US Navy missions could not keep commercial insurers in the market: war-risk premiums doubled, then tripled; Maersk and every major line except those under Russian or Chinese flag suspended Red Sea transits; more than two thousand ships rerouted around the Cape. The mission kept some ships moving, but it did not keep the strait economically open. A repeat of 2024 at higher intensity — which is what Velayati’s “unified command” signals — would do the same thing again, with Saudi Arabia’s principal export outlet as the collateral.

The Saudi Navy cannot close the gap. Its Red Sea assets include four French-built Al Madinah-class frigates, six corvettes, and a patrol-boat squadron — a force adequate for anti-piracy and coastal defence but not for sustained missile-defence of a sea-lane against a peer proxy. Egyptian and Jordanian contributions are politically complicated by Gaza; the Israeli Navy has offered shadow coverage but cannot operate publicly in Saudi territorial waters. The Red Sea’s defensive architecture is therefore ASPIDES plus whatever American assets remain on station — and the American assets are now routing around Africa.

The admission Riyadh is making

The Crown Prince’s April 14 message to Trump, delivered in person and backed by Arab ambassadorial briefings to the Wall Street Journal, is the closest Saudi Arabia has come to a formal admission that its bypass architecture is incomplete. The request — lift the Hormuz blockade — reads superficially as a petition for oil-price relief. Read against the Houthi trajectory, it is something different. Riyadh is asking Washington to de-escalate the war that is currently keeping both of its sea-lanes under threat, because the kingdom does not have the leverage, the arsenal, or the diplomatic reach to close the Bab al-Mandeb scenario on its own.

Saudi Arabia is on the side of the war effort that is making its own exports unsafe. The Crown Prince’s private urging of Trump toward regime change in Tehran was a bet that a short, sharp escalation would collapse the Iranian command structure before the Houthi second front activated. Thirty-seven days into the war, that bet has not paid out. The IRGC commands Iran without Khamenei’s presence; the Pakistan-mediated ceasefire is structurally unenforceable; and the Houthis have resumed strikes on Israel while holding the Red Sea in deliberate reserve. The window in which the Bab al-Mandeb contingency remains latent is closing, not widening.

The honest reading is that Saudi Arabia’s energy security rests on Iran choosing not to fight a war it is already fighting. Yanbu’s ceiling is 4.5 million barrels a day, Bab al-Mandeb is eighteen miles wide, and the Cape of Good Hope is thirty extra days of voyage time at a million dollars a ship. The only available third coast is a pipeline that has not been built and will not be built in the window of this crisis.

Frequently asked questions

How much Saudi oil transits Bab al-Mandeb compared to Hormuz?

Under normal operating conditions, Saudi Arabia exports roughly 1.3-1.5 million barrels a day through Bab al-Mandeb from Yanbu, against 5.5-6 million bpd through Hormuz from Ras Tanura and Ju’aymah. War-time rebalancing has inverted the ratio: in March 2026, Yanbu handled roughly 5 million bpd while Hormuz throughput collapsed to 15-20 ships a day from a pre-war baseline of 138. Bab al-Mandeb therefore now carries the majority of Saudi seaborne exports for the first time since the East-West Pipeline was commissioned.

Could Saudi Arabia use Egypt’s SUMED pipeline to bypass Bab al-Mandeb?

The SUMED pipeline runs from Ain Sukhna on the Gulf of Suez to Sidi Kerir on the Mediterranean, bypassing the Suez Canal for laden VLCCs but not bypassing Bab al-Mandeb itself — a tanker still has to exit the Red Sea northbound to reach Ain Sukhna. SUMED’s 2.8 million bpd capacity provides Canal-avoidance, not strait-avoidance. In a Bab al-Mandeb closure scenario, SUMED offers no usable alternative for Saudi crude bound for Asia.

Has a US carrier ever been hit by a Houthi anti-ship missile?

No. The closest incident occurred in October 2016, when the USS Mason (DDG-87) was targeted by two Houthi-fired C-802 anti-ship cruise missiles off the Yemeni coast — both missiles fell short or were intercepted, and the destroyer was undamaged. No US carrier has been directly engaged; the USS George H.W. Bush’s decision to route around the Cape of Good Hope in April 2026 is best read as pre-emptive risk management given the maturation of Houthi anti-ship ballistic missile inventory, not as response to a specific incident.

What would Bab al-Mandeb closure do to LNG markets?

Qatar moves roughly 15 million tonnes per annum of LNG through Bab al-Mandeb to European customers — approximately 20 percent of its total exports. A closure would force those cargoes around the Cape, adding 14 days per voyage and reducing effective fleet availability by a similar percentage. European TTF prices, currently trading around EUR 55 per megawatt-hour, would be expected to spike to EUR 90-120 in a sustained closure scenario. Qatar’s US and Asian deliveries would be unaffected.

Does China have any influence over Houthi operations in Bab al-Mandeb, as it does in Hormuz?

Beijing’s leverage over Hormuz transit flows through CNPC and Sinopec equity stakes in Qatari LNG fields and the yuan settlement channel via Kunlun Bank — a structural economic relationship that gave China credibility to broker the Al Daayen transit in April 2026. No comparable arrangement exists in Bab al-Mandeb. The Houthis receive financing and weapons through Iran’s Quds Force, not through Chinese intermediaries, and China’s Yemen embassy in Muscat has been used for messaging but not for operational transit coordination. Saudi Arabia cannot replicate Beijing’s Hormuz formula in the Red Sea because the two chokepoints have entirely different brokerage architectures.