DHAHRAN — Kuwait Petroleum Corporation lifted force majeure on all crude and refined product shipments on June 18 and committed to ramping output to two million barrels per day within a week — recovering commercially from the Hormuz crisis faster than any other Gulf Arab producer. The reopening that made this possible was not Kuwait’s work. Saudi Arabia absorbed the PGSA political concession, dispatched the first Bahri supertanker convoy through a mine-riddled strait with transponders off, ran its East-West Pipeline at maximum capacity for four months, and spent diplomatic capital at tables that produced no Saudi seat in the final arrangement.

Kuwait bore none of these costs. Its 1.4 million barrel-per-day production ramp — eighty-nine times the OPEC+ coordinated increment of 16,000 bpd — now compresses Brent toward Goldman Sachs’s $75 fourth-quarter floor before Saudi Arabia can physically ship at pre-war volume through a strait where mines, war-risk insurance at 340% of baseline, and a $1-per-barrel transit fee remain in force. The gap between Brent’s current $79 and Saudi Arabia’s $108–111 fiscal breakeven widens with every Kuwaiti cargo tendered for July delivery.

Three asymmetries define this dynamic: cost, price, and structure. Saudi Arabia paid for the reopening in political and fiscal terms. Kuwait captures the commercial upside. And no formal mechanism — OPEC+, GCC, bilateral — exists that Saudi Arabia can invoke to coordinate the ramp timing. That absence of enforcement capacity extends beyond Kuwait: the same crisis forced Iraq toward the door on June 25, threatening OPEC exit on a day when an IRGC drone confirmed Hormuz remains contested.

Table of Contents

- What Did Kuwait’s Force Majeure Cover?

- Eighty-Nine Times the Quota

- Who Paid to Reopen the Strait Kuwait Ships Through?

- How Fast Does Kuwait’s Ramp Compress the Price Saudi Arabia Needs?

- Does Saudi Arabia Have Any Lever to Slow Kuwait’s Ramp?

- Kuwait Has No Pipeline — and Ships First Anyway

- What Does Kuwait Owe the PGSA?

- The Free-Rider Ledger

- Frequently Asked Questions

What Did Kuwait’s Force Majeure Cover?

Kuwait Petroleum Corporation declared force majeure on crude oil and refined product shipments on April 20, citing the near-total absence of commercial vessels willing to transit the Strait of Hormuz, explicit Iranian threats against shipping, and drone strikes that caused fires at the 346,000 barrel-per-day Mina Al Ahmadi refinery (Bloomberg, April 20, 2026). The declaration covered obligations to both customers and counterparties, suspending contractual delivery commitments across KPC’s entire export portfolio.

The impact was immediate. Kuwait’s output fell from approximately 2.6 million bpd pre-war to 576,000 bpd in May 2026 — a 78% collapse — as onshore storage tanks reached capacity with no export route available (The National; OilPrice.com). Oil revenue dropped 73% in March 2026 alone (World Oil). TRT World and MERIP both noted that the 576,000 bpd trough represented output last seen in the early 1990s after the Iraqi invasion, when Iraqi forces set 605 of Kuwait’s oil wells ablaze during the 1990–91 Gulf War.

The force majeure remained in effect for fifty-nine days. On June 18, KPC announced via Kuwait’s Government Communication Centre: “All force majeure notices issued during the US-Israeli war on Iran have been lifted with immediate effect.” Output would rise to two million barrels per day “within a week, coinciding with the opening of the Strait of Hormuz and resumption of commercial shipping” (Reuters; Zawya). The same day, KPC tendered Kuwait Export Crude cargoes for July delivery at two million barrels per cargo (TradingView; Asharq al-Awsat).

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

In March, a KPC executive was quoted estimating that full production restoration could take as long as four months (OilPrice.com; The National). The June 18 “within a week” commitment is a substantially more optimistic revision, which KPC attributed to faster-than-expected infrastructure repairs. No independent verification of repair timelines at Mina Al Ahmadi or other damaged facilities has been published.

Eighty-Nine Times the Quota

The OPEC+ coordinated output increase agreed on May 3 assigned Kuwait a formal increment of 16,000 barrels per day, bringing its total quota to 2.628 million bpd (OPEC.org, May 3, 2026). Kuwait’s actual production ramp from 576,000 to two million bpd — an increase of approximately 1.424 million bpd — is eighty-nine times that coordinated number.

The distinction matters. A force majeure lift is a commercial contract action between KPC and its buyers. It restores suspended delivery obligations. It is not an OPEC+ quota decision and carries no requirement for coordination with other producers. The 16,000 barrels Kuwait was formally allocated through the OPEC+ process have no operational bearing on the 1.4 million barrels Kuwait is actually adding to the market.

Al Jazeera, covering the May 3 OPEC+ decision, described the coordinated increases as “less about adding barrels and more about signalling that OPEC+ still calls the shots” — a framing that assumed most Gulf production remained physically blocked by the Hormuz closure (Al Jazeera, May 3, 2026). Kuwait’s force majeure lift six weeks later turns that symbolic gesture into a structural reality check.

The organizational context compounds the problem. The UAE quit the seven-member OPEC+ coordination group before the May 3 meeting. France 24 reported that the group’s statement “made no mention of the UAE” (France 24, May 3, 2026). The GCC production bloc has fractured at the exact moment unified ramp discipline could have benefited Saudi Arabia. The UAE ramps independently via its ADCOP pipeline to Fujairah. Kuwait ramps independently via its force majeure lift. Saudi Arabia has no multilateral instrument to slow either.

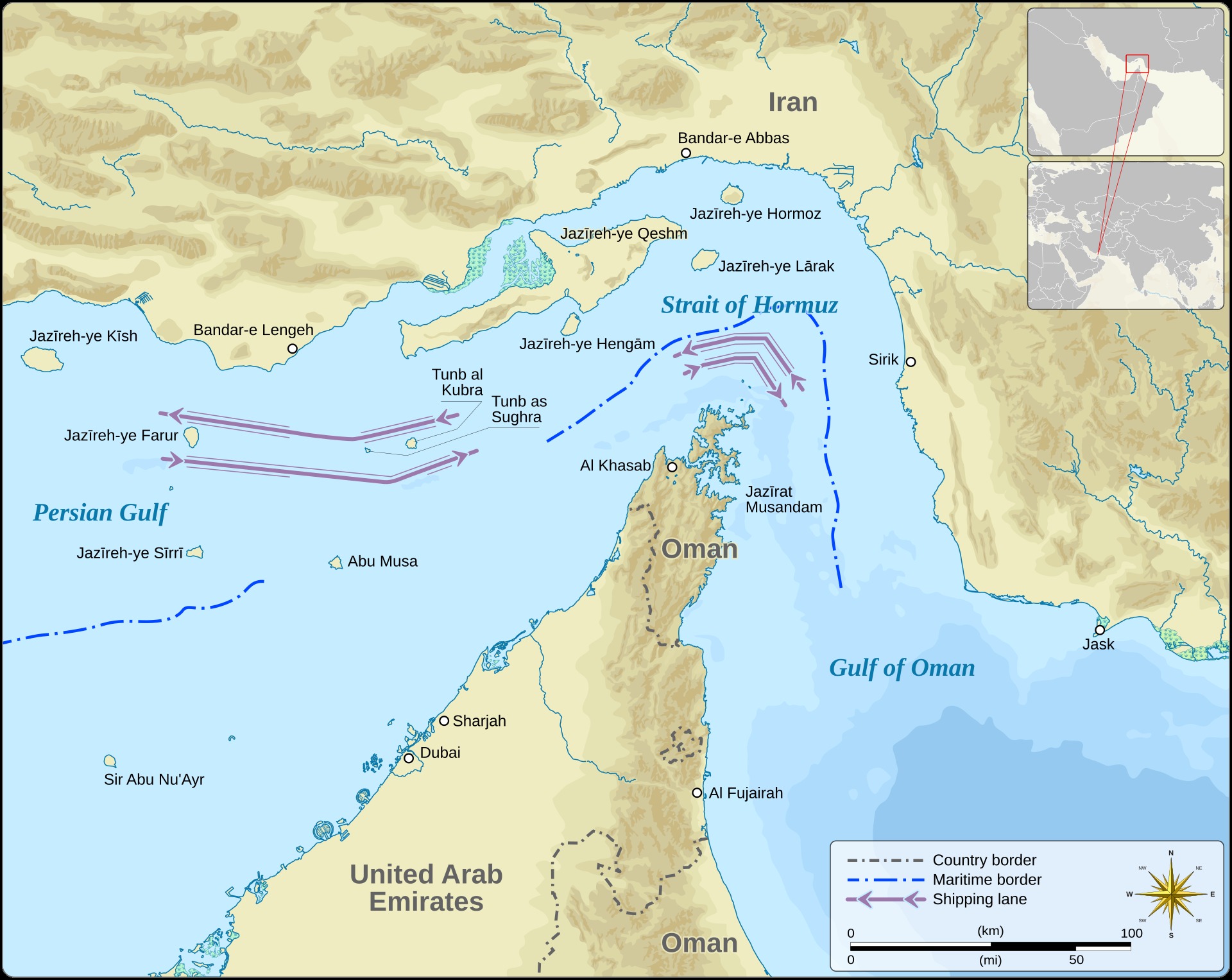

Who Paid to Reopen the Strait Kuwait Ships Through?

On the same day Kuwait lifted force majeure, three Bahri supertankers — Shaden, Jaham, and Awtad — completed the first Saudi crude transit through Hormuz since February 28, carrying approximately six million barrels through the Qeshm-Larak corridor with AIS transponders switched off (Arab News; Saudi Gazette, June 18–19, 2026). The implied PGSA fee of roughly $6 million at the $1-per-barrel rate remains unconfirmed by Aramco, Bahri, or the Saudi Ministry of Foreign Affairs.

That convoy was not a commercial event alone. It was a political signal — Saudi Arabia accepting in practice the transit framework it had contested in principle. The PGSA fee mechanism, which costs Saudi Arabia approximately $2 billion per year at full production volume, applies to every barrel of Saudi crude moving through the strait. Saudi Arabia’s only live revenue corridor during the four-month closure was the East-West Pipeline to Yanbu, running at its maximum capacity of seven million barrels per day. Every other Saudi export barrel — from Ras Tanura, Ju’aymah, the offshore fields — sat stranded.

Saudi Arabia’s fiscal accounts reflect the accumulated cost. The Q1 2026 deficit reached SAR 125.7 billion — more than double the Q1 2025 figure (Saudi Ministry of Finance). Oil revenues totalled SAR 144.72 billion against total expenditure of SAR 386.69 billion (Gulf News; AGBI, May 2026). Aramco’s free cash flow of $18.6 billion in Q1 no longer covers its $21.9 billion declared dividend — a coverage ratio of 0.85× (Aramco Q1 2026 report, May 2026).

Aramco cut its July Official Selling Price for Arab Light crude to Asia by $6 per barrel — the largest single-month reduction since 2022 — published on June 8, a week before the MOU was signed (Arab News; Saudi Gazette). The Arab Light premium to the Dubai/Oman benchmark collapsed 51%, from $19.50 in May to $9.50 in July. Saudi Arabia discounted its own crude to retain customers who were already shifting to Iranian and Iraqi alternatives. Kuwait’s KEC cargoes, tendered for July delivery on June 18, compete for the same Asian refinery slots at a price Saudi Arabia has already cut to reach.

Kuwait’s corresponding cost sheet is blank. No Kuwaiti convoy tested the strait. No Kuwaiti entity negotiated with the PGSA. No Kuwaiti diplomat sat at a mediation table that shaped Hormuz transit terms. KPC waited fifty-nine days, and when the commercial conditions improved — because Saudi Arabia and others absorbed the costs of making them improve — Kuwait lifted a piece of paper and tendered July cargoes.

How Fast Does Kuwait’s Ramp Compress the Price Saudi Arabia Needs?

Brent crude fell to $79.42 per barrel on June 18–19 as Kuwait’s force majeure lift coincided with broader supply-return signals (CNBC, June 19, 2026). The market now trades in a $75–$82 near-term band, approximately 37% below the conflict peak of $126.41. Goldman Sachs has maintained a $75 Q4 floor estimate. Saudi Arabia’s fiscal breakeven sits at $108–111 per barrel. The gap is $29–32 per barrel, and every dollar Brent falls from Kuwait’s incremental supply adds approximately $5.5 million per day to the Saudi fiscal deficit at full production.

Kuwait’s 1.4 million barrel-per-day ramp represents a material fraction of the IEA’s projected 3.7 million barrel-per-day record surplus for full-year 2026 (IEA Oil Market Report, May 2026). That surplus was calculated before Kuwait’s lift was announced. Nearly 40% of the projected annual overhang is arriving in a single week from a single producer — and the market was already pricing in a return to oversupply before KPC’s statement.

The sequencing compounds the damage. Brent collapsed before Saudi Arabia could physically ship at pre-war volumes. The price fell while Saudi crude sat in tanks or moved through Yanbu at pipeline-constrained rates. Iran’s NITC tankers — Diona, Hero 2, and at least one other vessel — had already moved 4.8 to 5 million barrels through Hormuz on June 15–16 under PGSA corridor exemptions, predating Kuwait’s announcement by three days. Kuwait’s supply stacks on top of Iranian supply in a market already priced for reopening.

Asian buyers — Kuwait’s primary customers alongside Saudi Arabia’s — were already reducing Gulf crude intake before the force majeure lift. Sinopec cut crude orders by approximately 80% during the Hormuz closure. Independent refiner Rongsheng reduced monthly purchases from seven million to one million barrels (prior reporting; Aramco Q1 data). These refiners now choose between Saudi, Kuwaiti, Iranian, and Iraqi barrels returning simultaneously into the widest Gulf sour supply menu since before the crisis.

KPC’s July crude tender — two million barrels per cargo — is a forward signal the market cannot ignore. Physical tenders compress spot and forward prices for Gulf sour crude. Every cargo tendered tells refiners and traders that Gulf supply is returning faster than the physical strait can accommodate safely. Hormuz oil flow stood at only 5.1 million barrels per day as of June 18 — 25% of the pre-war 21 million barrel baseline (CNBC, June 18, 2026). The paper market is trading a reopening the physical strait has not yet delivered.

Does Saudi Arabia Have Any Lever to Slow Kuwait’s Ramp?

No formal mechanism exists. The OPEC+ coordinated increment process allocated Kuwait 16,000 barrels per day. Kuwait is adding 1.4 million. The difference — eighty-nine-fold — is not a violation of OPEC+ quotas, because the ramp originates from a force majeure lift and not a quota revision. KPC’s contractual obligations to its buyers resumed the moment the declaration was withdrawn. No OPEC+ procedure governs the pace at which a member restores suspended commercial contracts.

The GCC Secretariat has no formal production quota authority. Historically, Saudi Arabia managed intra-GCC production timing through swing-producer influence and informal bilateral coordination. Both instruments require conditions that no longer hold. Swing-producer influence depends on Saudi Arabia’s ability to add or withdraw barrels at will — but Saudi Arabia’s Hormuz-facing export terminals remain constrained by mine risk, war-risk insurance at 340% of pre-crisis levels (InsuranceBusinessMag), and the PGSA fee. A producer needs a working instrument to exercise influence.

Informal bilateral coordination requires a shared sense of urgency. Kuwait’s production imperative is existential: the country’s entire state budget depends on crude exports, and the force majeure period consumed fiscal reserves at a rate that left no room for voluntary restraint. Asking Kuwait to slow its recovery to protect Saudi Arabia’s price environment is a request no Kuwaiti finance ministry could accept. Kuwait’s breakeven is lower than Saudi Arabia’s. The country that needs the barrels less is asking the country that needs them more to wait.

The UAE’s departure from OPEC+ before the May 3 meeting removes the last structural GCC voice that might have supported coordinated ramp discipline. Three Gulf producers now ramp independently: the UAE through ADCOP to Fujairah, Kuwait through its force majeure lift, and Iran through its PGSA exemption architecture. Saudi Arabia — the producer with the widest breakeven gap — is the most constrained by physical strait conditions.

Kuwait Has No Pipeline — and Ships First Anyway

Kuwait’s major oil fields — Greater Burgan, the world’s second-largest by proven reserves, along with Minagish, Umm Gudair, Raudhatain, Sabriyah, and the Wafra Partitioned Neutral Zone shared with Saudi Arabia — all route through pipeline networks terminating at Mina Al Ahmadi and Mina Abdullah on the Persian Gulf coast. No overland pipeline connects Kuwait to a non-Gulf terminal. The only hypothetical bypass routes run through Iraq, where no transit infrastructure exists, or through Saudi Arabia’s East-West Pipeline, which has been at capacity throughout the crisis (Bloomberg, June 9, 2026; CNBC, April 23, 2026).

KPC held talks with Saudi Arabia and the UAE as recently as June 9 about pipeline alternatives. No agreement was reached (Bloomberg, June 9, 2026). Kpler documented in April that Kuwait had “near-total dependence on a single maritime passage” (Kpler, April 7, 2026). Gulf Business assessed Kuwait among the Gulf producers most likely to “see a greater impact” from Hormuz disruption precisely because it lacked alternative export routes (Gulf Business, Q2 2026).

The vulnerability during closure inverts on reopening. Saudi Arabia invested in the East-West Pipeline as strategic insurance — seven million barrels per day of capacity connecting the Eastern Province to Red Sea terminals at Yanbu. That pipeline kept Saudi revenue flowing during the closure. But it also represents infrastructure cost that Kuwait never bore. Kuwait’s export architecture is simpler: fields to Gulf coast terminals to tankers. No pipeline tariff, no Red Sea routing, no capacity allocation trade-off. When Hormuz opens, Kuwait’s barrels reach the market through the shortest possible supply chain.

Saudi Arabia must now balance two export corridors — a maxed-out pipeline to the west and a mine-constrained, insurance-blocked, fee-tolled strait to the east. Kuwait has one corridor. It is open.

What Does Kuwait Owe the PGSA?

Kuwait is not exempt from the PGSA’s $1-per-barrel transit fee. The exemption list — Russia, China, India, Iraq, Pakistan, and Iran’s NITC fleet — was constructed to carve out price-sensitive buyers and political allies while leaving GCC states hosting US military facilities as the primary fee payers (Al Jazeera, May 21, 2026). At two million barrels per day, Kuwait’s PGSA exposure runs to approximately $2 million per day, or $730 million per year. At full pre-war capacity of 2.6 million bpd, the figure rises to roughly $950 million annually.

Saudi Arabia’s PGSA exposure at its full 5.5 million bpd Hormuz-facing export volume runs to approximately $5.5 million per day. Kuwait’s per-barrel cost is identical — $1. The aggregate burden falls disproportionately on the larger producer, and the larger producer is the one that absorbed the political cost of establishing the precedent that the fee would be paid at all.

Iran’s fee architecture is designed to profit from Gulf Arab production recovery. Every barrel Kuwait ships through Hormuz adds approximately $1 to PGSA revenue. Iran’s own crude moved first through exempted corridors. Now Kuwait’s crude follows, generating revenue for the same institution that blocked the strait. The PGSA draws no distinction between the country that fought to reopen the passage and the country that waited for conditions to change on their own.

The Free-Rider Ledger

The asymmetry between Saudi Arabia and Kuwait on the Hormuz reopening maps across six dimensions.

| Dimension | Saudi Arabia | Kuwait |

|---|---|---|

| Political cost of reopening | Accepted PGSA fee; dispatched Bahri convoy; excluded from MOU/Phase 2 mediation | None — no convoy, no PGSA negotiation, no diplomatic capital expended |

| PGSA fee exposure (full production) | ~$5.5M/day ($2B/year) at 5.5M bpd | ~$2M/day ($730M/year) at 2M bpd |

| Production ramp constraint | Mine risk, P&I insurance blackout, PGSA fee on Hormuz-facing 5.5M bpd | 1.4M bpd ramp in one week; no physical constraint beyond Hormuz itself |

| Non-Hormuz bypass capacity | 7M bpd East-West Pipeline (maxed during closure) | Zero — no pipeline alternative exists |

| OPEC+ formal increment (May 3) | Coordinated swing-producer role, no fixed increment | +16,000 bpd formal; 1.4M bpd actual (89× formal) |

| Brent breakeven gap at $79/bbl | $29–32/bbl deficit ($108–111 breakeven) | Near-breakeven (smaller fiscal base) |

The 1990–91 Gulf War provides a comparison that cuts against KPC’s timeline. After Iraqi forces invaded in August 1990 and ignited 605 oil wells, Kuwait took approximately eighteen months to restore production to two million barrels per day (MERIP; Asian Economics Letters). KPC’s June 18 commitment to reach the same output level within a single week implies either that infrastructure damage from the 2026 conflict was categorically less severe than the 1991 sabotage, or that oilfield repair capabilities have advanced more dramatically than KPC’s own March estimate — “as long as four months” — acknowledged.

Aramco’s 0.85× dividend coverage ratio means Saudi Arabia is already spending beyond its oil income to maintain shareholder returns. The Q1 deficit of SAR 125.7 billion arrived before Kuwait added 1.4 million barrels per day to the market. Aramco’s separate exposure through the Sadara $3.7 billion joint venture — where the grace period expired on June 15 with no public restructuring announcement — adds a contingent liability layer on top of the operating deficit.

One hundred and thirty empty tankers sat idle in the Persian Gulf as of June 18, against a pre-war baseline of approximately 250 (CNBC). War-risk insurance premiums remain at 340% above pre-crisis levels — 2.5% to 3% of hull value per voyage against a 0.1% baseline (InsuranceBusinessMag). The Joint Maritime Information Centre has not downgraded Hormuz below “Substantial.” P&I clubs have not issued full clearance for commercial shipping. BIMCO’s CONWARTIME clause remains active.

Kuwait lifted a piece of paper on June 18. The mines are still there. The war-risk premiums are still there. The PGSA fee is still there. None of that constrains Kuwait’s commercial calendar — and Brent responds to the calendar, not the channel depth.

Frequently Asked Questions

Has Kuwait confirmed payment of the PGSA transit fee on its post-force-majeure cargoes?

Neither KPC nor Iran’s Persian Gulf Security Authority has confirmed collection of the $1-per-barrel fee on Kuwait’s first post-lift shipments. The operational mechanism — whether payment occurs per cargo, per month, or through a flag-state intermediary — has not been disclosed in any published PGSA document. Kuwait’s Government Communication Centre statement on June 18 referenced the “opening of the Strait of Hormuz and resumption of commercial shipping” without mentioning the PGSA fee. It was the first public shipping announcement by a GCC government since the fee framework was introduced that omitted any reference to the toll.

What is Kuwait’s fiscal breakeven oil price compared to Saudi Arabia’s?

The IMF’s 2025 Article IV consultation estimated Kuwait’s fiscal breakeven at approximately $80–85 per barrel — roughly $25–30 below Saudi Arabia’s $108–111 range. The gap reflects Kuwait’s smaller population (approximately 4.9 million versus Saudi Arabia’s 36 million), lower per-capita state spending commitments, and the absence of a programme comparable in scale to Vision 2030. At $79 Brent, Kuwait operates near its breakeven threshold while Saudi Arabia carries a deficit of $29–32 on every barrel produced.

Could Kuwait route crude exports through Iraq to bypass Hormuz?

No viable infrastructure exists. The Iraq-Saudi Arabia Pipeline (IPSA), built in 1989 with a 1.65 million bpd design capacity terminating near Yanbu on the Red Sea, was shut by Iraq following the August 1990 invasion and has been fully decommissioned. Saudi Arabia converted its domestic segments for internal use. No pipeline connects Kuwaiti oil fields to any Iraqi export terminal. A new cross-border connection would require multi-year construction, Iraqi government transit agreements, and routing through terrain where security conditions remain contested. The June 9, 2026, pipeline talks between KPC, Saudi Arabia, and the UAE ended without agreement (Bloomberg).

Will Kuwait’s force majeure lift trigger compensation claims from buyers who sourced replacement crude at higher prices?

Force majeure declarations suspend contractual delivery obligations without penalty under international sales law and ICC guidelines. Buyers who sourced replacement crude at conflict-premium prices during the fifty-nine-day suspension may have incurred additional costs, but standard international crude sale agreements do not typically require seller compensation after a valid force majeure event. Whether KPC’s long-term offtake contracts contain make-whole or volume-catch-up provisions has not been publicly disclosed. The more immediate commercial consequence is forward: KPC’s July tenders at two million barrels per cargo now compete directly with Iraqi Basrah Heavy, Iranian Heavy, and returning Saudi Arab Medium for the same Asian refinery slots.

How does Kuwait’s production ramp compare to Iran’s post-MOU supply return?

Iran’s NITC fleet moved 4.8 to 5 million barrels through Hormuz on June 15–16 — approximately 2.4 to 2.5 million bpd on a two-day flow basis — under PGSA corridor exemptions that waived the $1-per-barrel transit fee. Iran’s pre-war exports ran at approximately 1.5 to 1.7 million bpd. Kuwait’s 1.4 million barrel-per-day ramp arrives on top of the Iranian return, meaning the Gulf is collectively adding an estimated 2.5 to 3.5 million bpd of supply into a market the IEA already projected as oversupplied by 3.7 million bpd for full-year 2026. Iranian barrels transit fee-free. Kuwaiti barrels pay $1 each. Saudi barrels pay $1 each and face mine clearance and insurance delays the other two producers do not.

Iran’s PGSA published its full operational rulebook on June 19, including the forty-category Vessel Information Declaration that governs every transit — a bureaucratic architecture that persists whether the fee is collected or waived. The formal rules are detailed in what Iran actually collects from ships when the transit fee is zero.