RIYADH — Saudi Arabia’s Vision 2030 turned ten on April 25 with a report card that would satisfy any boardroom — 93% of 390 active indicators at or above target, non-oil GDP at 55.6% of the real economy, and unemployment nearly halved — except that the plan’s tenth anniversary falls on Day 62 of a war that has cut the kingdom’s oil production by 30% and exposed the difference between diversifying an economy and diversifying a treasury.

The annual report, released the same day Crown Prince Mohammed bin Salman called the program an “exceptional transformational model,” records a decade of genuine structural change: a $1 trillion GDP economy that grew 80% since 2016, women’s workforce participation more than doubling from 17% to 36%, and a private sector that now contributes 51% of GDP. But the government budget that funds Vision 2030’s ambitions still draws 65–70% of its revenue from hydrocarbons, and Saudi crude output in March fell to 7.25 million barrels per day from 10.4 million in February — a volume collapse that no scenario model in any Saudi planning document ever anticipated.

Table of Contents

The Annual Report: What 93% Actually Means

Of 390 active key performance indicators tracked by the Vision Realization Office, 309 met or surpassed their interim targets, while another 52 achieved between 85% and 99% of their goals. Of 1,290 initiatives launched under the program, 225 have been fully implemented and 935 remain on schedule. These are not aspirational projections — they measure completed institutional reform across education, healthcare, housing, entertainment, and regulatory frameworks, backed by over 1,000 legislative changes that moved Saudi Arabia to 17th in the IMD World Competitiveness rankings, ahead of Germany and Australia.

The headline social indicators are difficult to dismiss. Saudi unemployment fell to 7.2% by end-2025, down from 12.3% when the plan launched, against a target of 7% by 2030. Women’s labor force participation hit 36%, already surpassing the original 30% target and now tracking toward a revised 40% goal. Life expectancy reached 79.9 years against an 80-year target. Home ownership rose to two-thirds of Saudi households, within reach of the 70% goal. Tourism hit 122 million visitors with SAR 300 billion in spending, and the General Entertainment Authority counted 89 million entertainment visitors across 975 active destinations — nearly double the 513 operating in 2024.

Real GDP grew 4.5% in 2025, the highest annual expansion in three years, with non-oil GDP growing 4.9%. The economy crossed $1 trillion in total output, an 80% expansion since 2016. Foreign direct investment stock rose 119% since 2017 to SAR 293.3 billion, with 2025 inflows reaching SAR 133 billion ($35.5 billion). Hamza Dweik, head of MENA trading at Saxo Bank, told Asharq Al-Awsat on April 25 that structural diversification was real but incomplete — and that reducing reliance on government support remains “the true measure of future success.” The Q1 2026 data complicates that picture further: see Al-Saif’s $46 Billion FDI Target Runs Into PIF’s Own Outflows for the latest GASTAT release showing net FDI declining even as gross flows nudged higher.

Why Does Non-Oil GDP Majority Not Fix the Budget?

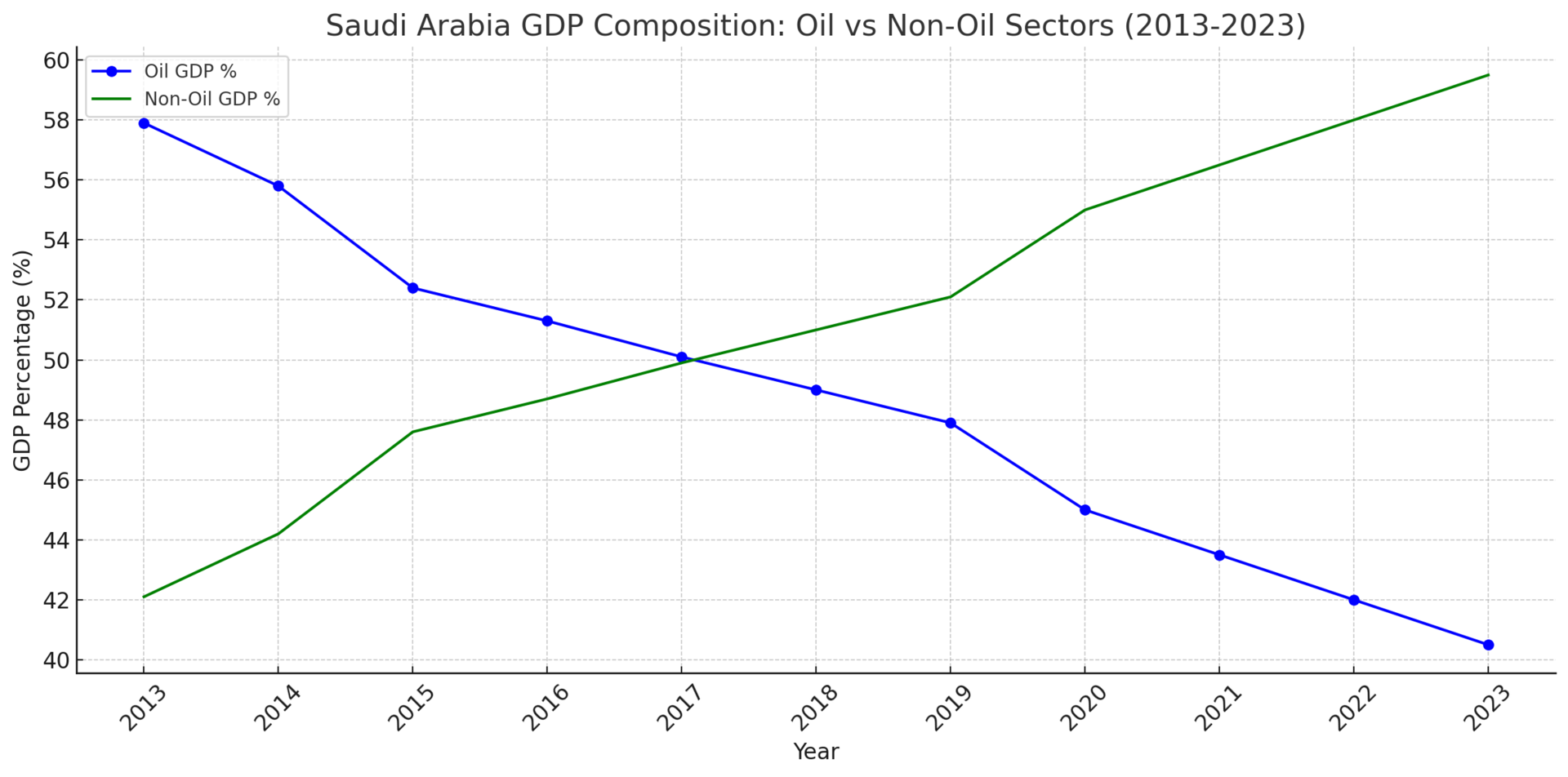

Non-oil activities reached SAR 2.6 trillion ($693 billion) in 2024, growing 6% and pushing non-oil GDP to 55.6% of the real economy, up from 45.4% a decade ago. This is the single most-cited achievement in the annual report and in the coverage that followed — Arab News, Asharq Al-Awsat, and Saudi Gazette all led with it. The number is real. It is also incomplete.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

GDP composition and fiscal composition are different measurements of different things. Saudi Arabia’s non-oil economy — tourism, entertainment, construction, logistics, financial services — generates majority economic activity but not majority government revenue. The Ministry of Finance’s own 2026 budget projects a SAR 166 billion deficit on revenue assumptions that predate the war. Goldman Sachs estimates the war-adjusted deficit at 6.6% of GDP, with a funding gap of $80–90 billion, because Brent at $90 per barrel in Goldman’s Q4 base case sits $18–21 below the $108–111 PIF-inclusive fiscal break-even. Even with Brent at $111.26 today — above the $94 plain break-even — Saudi production at 7.25 million bpd produces roughly $290 million per day in revenue versus $420 million at pre-war output, a volume-driven loss of approximately $130 million daily, or $47 billion annualized.

“Vision 2030 has clearly demonstrated the transformation of the Kingdom’s economic structure away from total reliance on oil… [but] the true measure of future success” is reducing reliance on government support.— Hamza Dweik, Saxo Bank, April 25, 2026

The distinction matters because every marquee project in the Vision 2030 pipeline — Expo 2030 in Riyadh, the 2034 FIFA World Cup, NEOM’s surviving components, the Diriyah Gate development — is funded through the Public Investment Fund or direct government capital expenditure, both of which depend on hydrocarbon cash flow. The private sector contributes 51% of GDP, up from 40% at launch, but the original target was 65% by 2030. At the current trajectory, that target is arithmetically out of reach within four years. Control Risks noted in its assessment that some targets “are likely to be softened or have different methods of measurement introduced to manage underperformance.”

The PMI Collapse and the Hormuz Assumption

The annual report’s backward-looking data captures Saudi Arabia through December 2025 — before the war reshaped every forward indicator. The most immediate evidence of what has changed sits in the March 2026 purchasing managers’ index: non-oil PMI collapsed to 48.8 from 56.1 in February, a 7.3-point monthly drop that ended a 66-month expansion streak. Only the March 2020 COVID shutdown produced a sharper single-month contraction. Export orders contracted at their fastest pace in six years. Naif Alghaith of S&P characterized the collapse as “a temporary adjustment following a strong expansion phase” linked to “short-term uncertainty from heightened geopolitical tensions.”

But what the PMI reading exposes is a structural dependency that the annual report does not acknowledge: Vision 2030’s non-oil economy was built on the assumption that the Strait of Hormuz stays open. Saudi Arabia constructed an elaborate crude-oil bypass — the East-West Pipeline to Yanbu, capable of routing 4–5.9 million barrels per day around the strait — but built zero equivalent redundancy for containerized imports, manufactured goods, or the supply chains that feed construction projects, entertainment venues, and the tourism infrastructure that the plan showcases. War risk insurance premiums surged 800%; container shipping costs into Saudi ports doubled.

Dania Thafer of the Gulf International Forum told Business Upturn that Iranian incursions “normalise volatility,” undermining Vision 2030’s “fundamental premise — that a predictable, stable operating environment attracts diversified capital.” Neil Quilliam of Chatham House flagged expatriate retention as a parallel vulnerability, noting that talent outflows directly threaten the workforce targets underpinning non-oil growth. The IMF revised its 2026 Saudi GDP growth forecast from 4.5% to 3.1%, and the FDI trajectory has reversed sharply — UNCTAD and analyst consensus project a significant Q1 2026 contraction, with war risk premiums and supply-chain disruption deterring exactly the capital the plan requires. The $100 billion annual FDI target by 2030 would require Saudi Arabia to roughly triple current inflows in each of the next four years, a trajectory that was already ambitious before the war and is now functionally implausible.

NEOM, PIF, and the Retrenchment That Preceded the War

The Vision 2030 annual report does not mention The Line by name. PIF Governor Yasir Al-Rumayyan addressed the flagship project separately on April 15, stating that “no NEOM projects have been cancelled” while adding that “spending priorities have been reassessed.” His framing was striking: “Is it necessary to have The Line by 2030? I think no. It’s good to have, but not a must-have.” The Line — originally designed as a 170-kilometer linear city — has been compressed to 2 kilometers of foundations with no superstructure erected. PIF’s domestic construction budget was cut 58%, from $71 billion to $30 billion. The 2029 Asian Winter Games, which were to be hosted at Trojena (approximately 35–40% complete), were relocated to Almaty.

These cuts preceded the war. PIF’s assets under management stand at approximately $930 billion, but the portfolio is mostly illiquid — sovereign stakes, domestic giga-projects, and long-duration infrastructure. Cash reserves fell to roughly $15 billion by late 2024. Aramco’s base dividend was cut by approximately one-third for 2025, with total dividends falling to $85.5 billion from $124.3 billion in 2024 — PIF, which holds a 98.5% stake, absorbed the bulk of that $38.8 billion reduction. The war has compressed the timeline further: OPEC’s April decision to add 206,000 barrels per day did not move the market, and Goldman’s $90 Q4 Brent forecast implies the fiscal arithmetic worsens through the year.

What remains on the PIF calendar are the two projects with immovable external deadlines: Expo 2030 Riyadh and the 2034 FIFA World Cup. These now function as the capital-allocation anchors around which everything else in the Vision 2030 portfolio is being reorganized — not because they are the highest-return investments, but because cancellation carries reputational costs that PIF’s leadership has judged worse than the capital commitment.

The Scenario That Was Never Modeled

Every previous Saudi fiscal crisis followed the same pattern. In 1986, 1998, and 2014–2016, oil prices crashed but production volumes held or increased to compensate — Saudi Arabia could pump its way through a revenue shortfall. Vision 2030 itself was born from the 2014–2016 crash, designed explicitly as the answer to price vulnerability. The plan’s scenario modeling, disclosed across multiple National Transformation Program documents and PIF strategy papers, stress-tested against oil at $40, $50, and $60 per barrel.

The Iran war delivered something different: a volume collapse while prices rose. Brent traded above $109 in March, but Saudi output at 7.25 million bpd — constrained by infrastructure damage at Khurais (300,000 bpd offline, no recovery timeline announced), the Yanbu loading ceiling, and the double blockade at Hormuz — generates less revenue than 10.4 million bpd at $80 would have. The IEA called it the “largest disruption on record.” Asia-bound exports fell 38.6% according to Kpler tracking data.

| Indicator | 2016 Baseline | 2025/2026 Actual | 2030 Target | Status |

|---|---|---|---|---|

| Non-oil GDP share | 45.4% | 55.6% | — | On track |

| Unemployment | 12.3% | 7.2% | 7.0% | Near target |

| Women’s labor participation | ~17% | 36% | 40% (revised) | Ahead |

| Private sector GDP share | 40% | 51% | 65% | Behind |

| Annual FDI | ~$7.5B | $35.5B | $100B | Behind |

| PIF AUM | ~SAR 600B | ~SAR 3.5T ($930B) | SAR 7T | Behind |

| Saudi crude production | ~10.5M bpd | 7.25M bpd (March ’26) | N/A (war) | Crisis |

| Fiscal deficit (% GDP) | — | 6.6% (Goldman est.) | Balanced | Crisis |

The result is a fiscal position that the plan was never designed to withstand. The scenario modeling stress-tested against price; it never stress-tested against physical infrastructure denial. What the Iran war has demonstrated is that Vision 2030’s dependency on hydrocarbon cash flow was not a design flaw the plan was fixing — it was the structural condition the plan was operating inside, unchanged at the foundation while everything above it was being reformed. The revenue crossover that Brent at $114.50 produced on April 29 — restoring Saudi oil income to pre-war nominal levels despite 30% production loss — illustrates the paradox precisely: how Brent at $114.50 restores Saudi oil income while $300–500 million in daily war costs consume the entire gain.

What Still Holds After Ten Years

Strip away the fiscal stress and the war overlay, and the institutional record is not manufactured. Saudi Arabia in 2026 is a different country from the one that launched Vision 2030 in April 2016 — not because of the giga-projects, most of which are behind schedule or scaled back, but because of the regulatory, social, and labor-market reforms that rarely make headlines. The entertainment sector did not exist as a formal economic category a decade ago; it is now a measurable industry with genuine revenue. Tourism volumes and women’s workforce participation both surpassed their original 2030 targets four years early — targets that were dismissed as aspirational when MBS announced them. These are structural shifts that survive the war, even if the fiscal base that funded them does not.

The 93% compliance rate across 390 KPIs is a measure of institutional execution capacity — the ability of Saudi ministries and agencies to set targets and meet them — that did not exist before the Vision Realization Office imposed it. Whether that capacity can survive the financial compression of a protracted war, with PIF cash depleted, Aramco dividends cut, and the fiscal break-even receding, is the question the eleventh year will answer. Phase 3 of Vision 2030, designated for consolidation from 2026 to 2030, was supposed to begin with the hard work of converting government-led growth into self-sustaining private economic activity. Instead, it begins with the government deciding which of its own commitments it can still afford to keep.

FAQ

How does Vision 2030 define “non-oil GDP” and does it include petrochemical refining?

Saudi Arabia’s General Authority for Statistics (GASTAT) classifies “oil activities” as crude petroleum extraction and natural gas production. Petrochemical manufacturing, oil refining, and downstream processing are categorized under industrial or manufacturing GDP — meaning they count as “non-oil” in the 55.6% figure. SABIC’s $30+ billion in annual petrochemical revenues, for instance, falls on the non-oil side of the ledger. Critics, including the IMF in its 2024 Article IV consultation, have noted that this classification flatters the diversification metric because downstream activities remain structurally correlated with upstream hydrocarbon production — when crude output drops 30%, refinery throughput eventually follows.

What happened to the SAR 7 trillion PIF target?

The original Vision 2030 framework set a target of SAR 7 trillion (approximately $1.87 trillion) in PIF assets under management by 2030. At roughly $930 billion today, the fund would need to more than double in four years. Al-Rumayyan has not publicly reaffirmed the target since 2023. The Aramco dividend cut — total dividends falling from $124.3 billion to $85.5 billion, with PIF absorbing the impact as the 98.5% shareholder — combined with domestic construction budget cuts of 58% and cash reserves at ~$15 billion, suggests the fund is managing liquidity rather than pursuing the original growth trajectory. Analysts at Fitch and S&P have shifted their PIF coverage language from “target” to “aspiration.”

Has the war affected Saudi Arabia’s 2034 FIFA World Cup preparations?

Stadium construction timelines have not been publicly revised, but the 2034 bid infrastructure requires an estimated $50–60 billion in total spending across 15 stadium venues, transport links, and hospitality capacity. PIF’s domestic construction budget cut from $71 billion to $30 billion preceded the war and already forced prioritization. The Asian Winter Games relocation from Trojena to Almaty in late 2025 demonstrated willingness to shed commitments when costs exceed projected returns. FIFA’s 2034 timeline requires venue completion by 2032 for testing events — six years away, but on a fiscal base that Goldman estimates is running an $80–90 billion annual funding gap.

Why did the non-oil PMI collapse matter more than previous dips?

The March 2026 PMI reading of 48.8 broke a 66-month expansion streak — five and a half years of consecutive growth in the non-oil private sector, the longest sustained run since Saudi Arabia began PMI tracking. Previous dips (COVID in March 2020, the 2019 Aramco drone attack) were followed by rapid recoveries because the underlying trade infrastructure remained intact. The current contraction reflects physical disruption to supply chains — container shipping cost increases, war risk insurance surcharges, and the effective closure of Hormuz to regular commercial traffic — that cannot be resolved by monetary or fiscal stimulus alone. Recovery depends on when the strait reopens, which depends on a military standoff with no negotiated end date.

Are nearly 3 million Saudis still living in poverty?

The most recent publicly available Saudi poverty data dates to 2021 and placed approximately 2.9 million citizens below the national poverty line. Vision 2030’s original framework included no poverty reduction target — an omission that has drawn criticism from the World Bank and domestic economists. The Citizen Account program and other direct transfer mechanisms have expanded since 2016, but no official poverty measurement has been published since the 2021 figure, making it impossible to assess whether the broader economic growth captured in the annual report has translated into reduced material deprivation at the lower end of the income distribution.