RIYADH — Saudi Arabia’s war with Iran has accomplished what a decade of Vision 2030 presentations could not: it has made the kingdom’s western coastline the center of its economic future. With Hormuz throughput collapsed to 3.6% of pre-war baseline and Saudi crude production down 30% — from 10.4 million to 7.25 million barrels per day — Mohammed bin Salman arrives at next week’s Trump investment forum in Riyadh carrying $600 billion in announced deals and an economic map that faces the Red Sea, not the Persian Gulf.

The pivot is no longer aspirational. Chatham House concluded in May 2026 that the kingdom is “beginning to reassess its economic geography, reducing its dependence on Hormuz and reorienting policy towards the Red Sea” — a judgment that would have read as speculation two years ago and now reads as a description of government policy. What MBS is building along the western coast — automated ports, green hydrogen plants, AI data centers, expanded crude terminals — is not the Vision 2030 that was already faltering before the first missile fell. It is the post-Hormuz economy that the war demanded and that $600 billion in foreign capital is now underwriting.

Table of Contents

- What Does Saudi Economic Geography Look Like If Hormuz Never Fully Reopens?

- The Pipeline That 1981 Built

- Why Can’t Yanbu Replace Hormuz?

- Oxagon, Green Hydrogen, and the Red Sea Industrial Corridor

- How Is MBS Funding a New Economy During a $33.6 Billion Deficit?

- $600 Billion in Four Days

- Can Iran Neutralize the Red Sea Pivot?

- Two Coasts, One Advantage

- Key Metrics

- Frequently Asked Questions

What Does Saudi Economic Geography Look Like If Hormuz Never Fully Reopens?

If Hormuz remains restricted, Saudi Arabia’s economic center of gravity shifts permanently to the Red Sea coast. The East-West Pipeline, Yanbu crude terminals, NEOM’s industrial port at Oxagon, and planned AI data center clusters become the kingdom’s primary economic infrastructure — replacing the Eastern Province’s 90-year role as the country’s export engine.

The question sounds hypothetical, but the infrastructure spending does not. Saudi Arabia has already converted its East-West Pipeline to full crude capacity, surged Yanbu exports far above pre-war levels, and directed the Public Investment Fund — with $912 billion under management — to allocate 80% of its capital domestically, with the Red Sea corridor absorbing a disproportionate share. The reallocation happened not because Riyadh chose it on a strategic planning timeline but because Iranian missiles made the choice.

Chatham House laid out the structural logic in its May 2026 assessment with unusual directness: “Significant long-term investment will be needed in infrastructure that allows goods — especially oil — to move between the Red Sea and major urban centres across the Gulf if Saudi Arabia is to establish itself as a regional trading hub. Longer timelines and higher costs will be unavoidable, but the structural nature of the Hormuz problem leaves Saudi Arabia with little choice.”

That phrase — “little choice” — carries more weight than any investment figure in the assessment. It means the Red Sea pivot is not a diversification play and certainly not the vanity-driven megaproject spending that defined early Vision 2030; it is economic geography being rebuilt under fire, with the understanding that the old geography may not come back whole. The Eastern Province still holds Saudi Arabia’s oil reserves, its largest refining complexes, and the infrastructure of a petrochemical superpower — but if Hormuz stays contested, the coast that ships the crude is no longer the coast that pumps it.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Kristian Coates Ulrichsen, a Baker Institute fellow at Rice University, framed the urgency driving the acceleration: “The Saudis are so concerned about any potential escalation because they realize they have this largely untapped Red Sea coastline, which they are now developing and see a lot of potential in.” That potential was always latent — Saudi Arabia’s western coast runs more than 1,800 kilometers from the Jordanian border to the Yemeni frontier. The urgency is new, and urgency changes everything from permitting timelines to capital allocation to which NEOM projects survive and which get cut.

The Pipeline That 1981 Built

The East-West Pipeline was commissioned during the Iran-Iraq War, when the previous generation of Saudi planners confronted the same vulnerability MBS faces now: a hostile Iran with the capability to close a chokepoint. The pipeline — 1,201 kilometers from Abqaiq in the Eastern Province to Yanbu on the Red Sea — was built as insurance against a scenario that everyone assumed would remain theoretical. The scenario arrived on February 28, 2026.

By March 11, Saudi Aramco had converted the accompanying NGL pipelines to carry crude, bringing total East-West capacity to 7 million barrels per day — a conversion that Fortune reported took less than two weeks. Yanbu crude exports surged to 4.0 to 4.3 million bpd by March — more than triple pre-war levels — with supertankers backing up at terminals along the Red Sea coast. The pipeline activated exactly as designed, validating a 45-year-old investment thesis in the span of 11 days.

Iran understood exactly what the pipeline represented for Saudi survivability. In April 2026, IRGC forces struck the East-West Pipeline itself, cutting throughput by roughly 700,000 bpd — a targeted attack on the infrastructure Saudi Arabia depends on to bypass Hormuz. Saudi Arabia declared it back to full capacity within six days, by April 12, but the attack established a precedent: the infrastructure that bypasses Hormuz is itself a target, and Iran will treat it as one.

Engineering News-Record captured the question that wartime validation opens for post-war planning: “The question energy infrastructure planners will face when this crisis resolves is whether the original bet can still be defended or whether the engineering calculus around Hormuz bypass capacity needs to be fundamentally reconsidered.” The answer is already being written in concrete and steel along the Red Sea coast. But the pipeline’s performance also exposed the system’s binding constraint — the pipeline can push 7 million barrels per day to the coast, and the coast cannot load 7 million barrels per day onto ships.

Why Can’t Yanbu Replace Hormuz?

Yanbu’s two terminals — Yanbu North and Yanbu South — have a combined nominal capacity of approximately 4.5 million barrels per day, but Vortexa estimates wartime congestion limits actual throughput to roughly 3 to 4 million bpd. At maximum operational ceiling — with auxiliary berths and ongoing upgrades — Yanbu can load approximately 5.4 to 5.9 million barrels per day. Pre-war Saudi exports through Hormuz ran at 7 to 7.5 million bpd, leaving a structural gap of 1.1 to 1.6 million bpd even at maximum Red Sea loading capacity.

The arithmetic is well understood in Riyadh and poorly understood everywhere else. The pipeline’s 7 million bpd capacity is a theoretical ceiling that hits a physical floor at the Yanbu waterfront, where only two terminals exist and neither was designed for the volumes they are now handling. Wartime loading throughput — a 330% surge from pre-war levels — is simultaneously extraordinary and insufficient.

Chatham House identified this gap as the central infrastructure challenge: “Saudi Aramco will need to reorient crude exports to the Red Sea or at least build capacity to convey 7 million barrels a day to match pre-war exports. It is currently transporting around 4 million barrels per day of crude by pipeline from east to west and exporting it via the Yanbu terminal on the Red Sea.” The 1.1 to 1.6 million bpd shortfall translates to roughly $100 million per day in revenue that cannot reach international markets through the western route, even with the pipeline running at full capacity.

Expanding Yanbu to handle full pipeline throughput is a multiyear engineering project involving deepwater berths, single-point mooring buoys, and tank farm construction at a scale the terminal has never accommodated. Saudi Aramco has not publicly disclosed an expansion timeline, which is itself informative: the gap exists, the government acknowledges it, and no one has committed to a date for closing it. The congestion is visible at the waterfront — supertankers line up for berths at a terminal built for regional export volumes, now serving as Saudi Arabia’s primary global crude loading point.

Oxagon, Green Hydrogen, and the Red Sea Industrial Corridor

While Aramco fights the loading bottleneck at Yanbu, a different kind of Red Sea economy is being assembled 400 kilometers north along the coast at NEOM. Unlike the pipeline conversion, this infrastructure was designed from scratch for the western seaboard — built for an economy that does not depend on crude tankers transiting either chokepoint.

NEOM’s Port of NEOM at Oxagon, the octagonal industrial complex, is 68% complete with SR7.5 billion ($2 billion) invested to date. Its container terminal — launching in 2026 with 1.5 million TEU capacity — will house Saudi Arabia’s first fully automated ship-to-shore cranes, purpose-built for Red Sea supply chains that the war has made necessary rather than optional. This is logistics infrastructure arriving at the precise moment the kingdom’s eastern ports are functionally cut off from global maritime routes.

Adjacent to Oxagon, the NEOM Green Hydrogen Plant is 80% complete — an $8.4 billion facility designed to produce 600 metric tons of green hydrogen per day, targeting commissioning in the third quarter of 2026. The plant positions Saudi Arabia’s Red Sea coast as an export hub for the energy commodity that European and Asian industrial buyers are competing to secure, a product that ships as ammonia through established chemical routes rather than by crude tanker through contested chokepoints. Green hydrogen does not solve the oil-revenue shortfall, but it begins diversifying the revenue base in a way that exploits the same coastal geography without inheriting the same vulnerability.

“The kingdom is beginning to reassess its economic geography, reducing its dependence on Hormuz and reorienting policy towards the Red Sea. Projects along Saudi Arabia’s western coastline, including ports, industrial zones and tourism developments, will now become key priorities.”

— Chatham House, May 2026

NEOM is not an all-or-nothing proposition, and the war has forced PIF to demonstrate it knows the difference. The Line’s 2030 residential targets have been abandoned, and Trojena — the indoor ski resort in the Tabuk mountains — has shed major construction contracts, signaling that prestige without near-term economic return is no longer fundable. What survived the pruning reveals where the capital is flowing: industrial port infrastructure, energy export capacity, and the logistics backbone of a Red Sea economy that did not exist three years ago.

The Gulf International Forum described the underlying discipline: PIF has “narrowed its focus to sectors with near-term commercial returns, including logistics, mineral extraction, and religious tourism, while extending timelines and trimming costs on higher-risk ventures.” The Red Sea corridor absorbs the first two categories directly — Oxagon is logistics, the hydrogen plant is extraction-adjacent — while Amaala’s luxury resort opening in Q3 2026 fills the third. Wartime triage applied to a $912 billion portfolio is, in its own way, a form of industrial policy.

How Is MBS Funding a New Economy During a $33.6 Billion Deficit?

Saudi Arabia posted a first-quarter 2026 deficit of SAR 126 billion ($33.6 billion) — the largest in eight years — with government spending up 20% year-over-year. MBS is financing the Red Sea build through PIF’s $912 billion in assets, an 80% domestic allocation, and $600 billion in foreign commitments secured at the Trump forum.

The fiscal picture is the least comfortable part of the Red Sea narrative, and anyone presenting the pivot as a wartime triumph has to confront what Al Jazeera reported on May 6. That quarterly shortfall — spending running a fifth above the same period last year — represents the kingdom building the next economy while hemorrhaging in the current one, drawing on the same finite pool of capital, contractors, and institutional bandwidth.

PIF’s April 2026 strategy refresh offers the clearest signal of how MBS intends to manage the contradiction. The fund shifted to an 80% domestic allocation — down from a 30% international peak — while adding AI infrastructure as a named priority with a 3,000-megawatt data center target. Karen Young of the Middle East Institute read the shift as “a focus on how to localize projects and drive investment both locally and from foreigners into supply chains and manufacturing of projects.” The strategy uses PIF domestic spending as foundation-laying and positions foreign capital as the multiplier that makes the math work.

But PIF’s domestic turn means the fund competes for the same construction labor, materials, and contractor capacity that Aramco needs to expand Yanbu. Aramco’s wartime earnings cannot sustain both the largest quarterly deficit in eight years and a multibillion-dollar infrastructure build along the entire western coastline without external financing. The bet — and it is a bet, not a certainty — is that Red Sea industrial infrastructure generates returns faster than oil-revenue recovery from a Hormuz restoration that may never reach pre-war levels.

The deficit number alone does not capture the fiscal compression MBS is navigating. Saudi Arabia is simultaneously funding a war it did not start, subsidizing an economy adjusting to 30% lower crude output, investing in infrastructure that will not produce revenue for years, and trying to attract foreign capital into a theater where Iranian missiles have already struck the pipeline carrying the kingdom’s oil. That the $600 billion in announced deals materialized at all, in this environment, is either a testament to Saudi Arabia’s structural proposition or to the risk premium investors will accept for access to the kingdom’s sovereign market — likely both, in proportions no one will disclose.

$600 Billion in Four Days

The Trump-Saudi Investment Forum, scheduled for May 13 in Riyadh, is not a trade conference — it is MBS’s financing vehicle for the post-Hormuz economy packaged as a diplomatic event and anchored by the largest technology commitments Saudi Arabia has ever secured. The $600 billion in announced deals maps directly onto the infrastructure gaps the war has exposed, and the composition of the investor list reveals which gaps MBS considers most urgent.

The headline is Nvidia, which is supplying 18,000 GB300 Blackwell chips to Humain — the PIF subsidiary whose CEO, Tareq Amin, told CNBC that the company’s ambition is “to be the third-largest AI provider in the world, behind the United States and China.” Those chips will power 500 megawatts of data center capacity, a substantial fraction of PIF’s 3,000-megawatt target, and the data centers are being sited on the western side of the country — where submarine cable routes to Europe run through the Red Sea and the Suez Canal, not through Hormuz-adjacent waters. Amazon, Oracle, AMD, Qualcomm, and DataVolt (which committed $20 billion independently) round out a technology investment package that positions the Red Sea corridor as digital infrastructure, not just an oil bypass.

Trump’s Riyadh visit serves MBS in a second, less visible capacity. By anchoring American technology firms to Saudi infrastructure with decade-long supply agreements, MBS converts US corporate interests into a constituency for Red Sea corridor security — Nvidia does not care about Freedom of Navigation as a legal doctrine, but it cares intensely about the physical safety of the data center housing its most advanced chips. The $600 billion is not aid and not charity; it is commercial investment being converted into a security guarantee by making the Red Sea corridor too valuable for Washington to neglect.

The geographic logic of the AI build reinforces the energy logic of the pipeline pivot. Red Sea submarine cables connect Saudi Arabia to Europe and Africa through the Suez Canal; Gulf-side cables run through waters that are, as of May 2026, contested by the IRGC. A data center on the Red Sea coast serves European and African clients with lower latency than one sited on the Gulf, a geographic advantage that exists independent of any war but that the war has made visible to every infrastructure planner reading the shipping reports.

Can Iran Neutralize the Red Sea Pivot?

Iran can threaten the Red Sea pivot through two vectors: pipeline strikes, as demonstrated in April 2026, and Bab el-Mandeb disruption through Houthi proxies. Velayati, senior adviser to Khamenei, declared that “the unified command of the Resistance front views Bab al-Mandeb as it does Hormuz” — explicitly linking both chokepoints as instruments of pressure.

The war has already provided two proof points, and both should concern the investors assembling for the May 13 forum. Iran struck the East-West Pipeline in April, cutting throughput by 700,000 bpd — a targeted attack on the single piece of infrastructure Saudi Arabia depends on to bypass Hormuz, repaired within six days but establishing a precedent of kinetic contestation. That declaration signals that Tehran views the westward pivot not as Saudi Arabia’s escape but as a new pressure surface to be exploited — one that connects the Red Sea export corridor to a chokepoint Iran believes it can contest through proxy forces.

The vulnerability is structural and well quantified. JP Morgan estimates that a Bab el-Mandeb disruption alone could add $20 per barrel to oil prices, and approximately 70 to 75% of Yanbu’s exports destined for Asian markets must transit the strait. A combined closure of Hormuz and Bab el-Mandeb — the double-chokepoint scenario Saudi Arabia has been quietly modeling — would put an estimated $10 billion per day in global trade at risk and block roughly 30% of global container shipping.

The Houthi Red Sea shipping campaign that began in November 2023 demonstrated that Bab el-Mandeb is vulnerable to disruption by non-state actors with relatively modest weapons systems, rerouting major container lines around the Cape of Good Hope for more than a year. That campaign was conducted without direct Iranian kinetic participation; by late March 2026, IRGC sources suggested Iran may direct Houthi allies to target Bab el-Mandeb specifically in response to Saudi Arabia’s Red Sea export pivot. Chatham House acknowledged the implication directly: “Attacks on Red Sea shipping by the Iran-aligned Houthis show that maritime insecurity will become a central constraint on Saudi Arabia’s westward reorientation, not a secondary concern.”

Ulrichsen captured the non-energy dimension of the threat: “The optics of stray missiles and drones slamming into Saudi cities when they’re trying to attract the sort of high-end luxury markets would be disastrous.” That observation cuts to the heart of the NEOM investment proposition. The Red Sea pivot does not eliminate chokepoint exposure — it trades one chokepoint for another while adding overland vulnerability in the 1,201-kilometer pipeline corridor between Abqaiq and Yanbu.

MBS appears to be betting on “manageable” rather than “disqualifying.” The air defense architecture protecting the western coast, combined with the US naval presence that $600 billion in American corporate investment creates commercial incentive to maintain, may be sufficient to secure the corridor at a cost the kingdom can absorb. Whether that judgment holds depends on variables — IRGC escalation decisions, Houthi capability evolution, US force posture in the Red Sea — that no amount of Saudi infrastructure spending can control.

Two Coasts, One Advantage

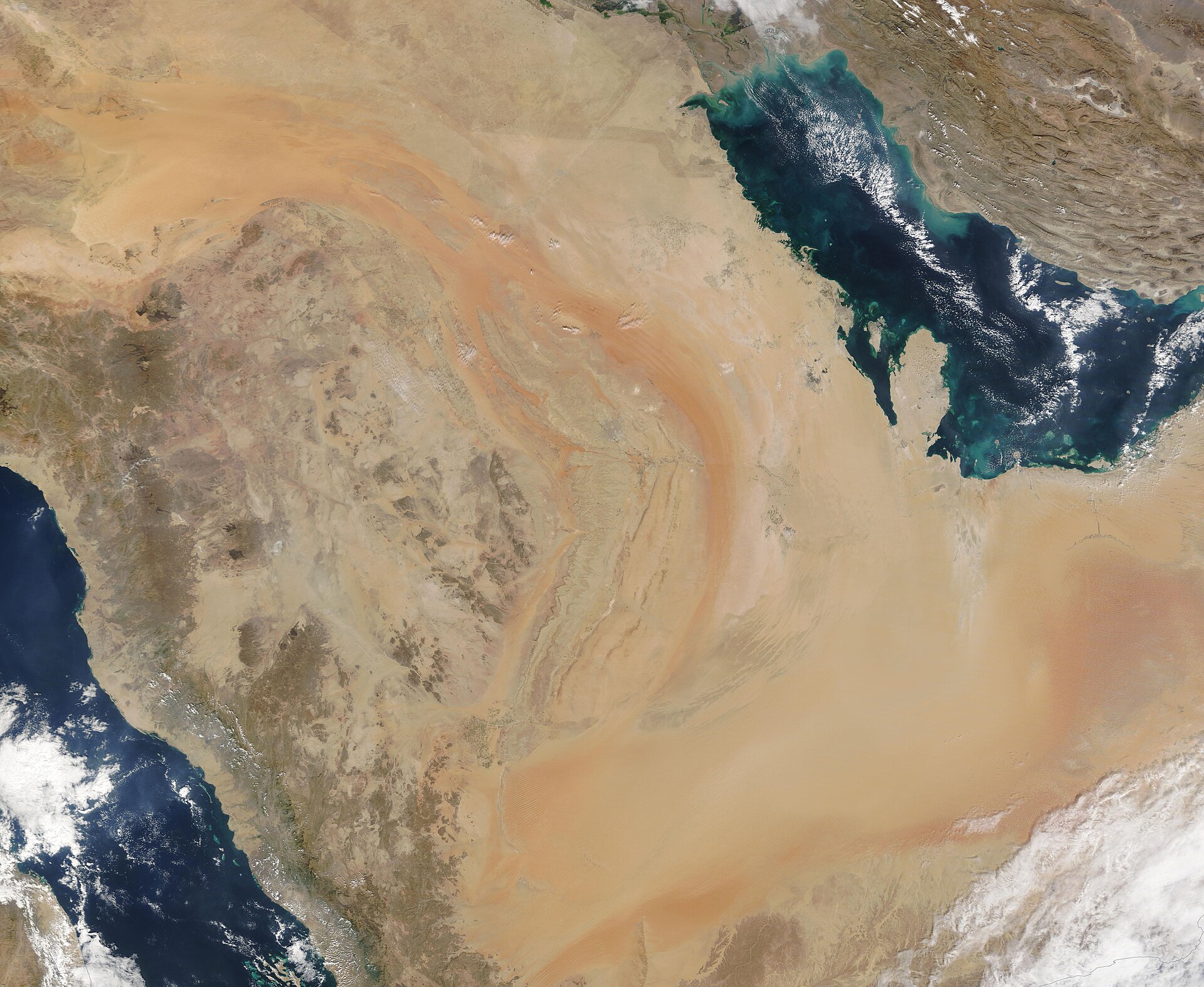

Among the Gulf states absorbing the consequences of the Hormuz crisis, Saudi Arabia holds one structural asset that no sovereign wealth fund can replicate: a second coastline. The UAE, Qatar, Kuwait, and Bahrain are single-coast economies whose entire export infrastructure faces the Persian Gulf and whose maritime access runs through a strait the IRGC now controls. Saudi Arabia’s western seaboard — more than 1,800 kilometers from the Gulf of Aqaba to the Yemeni border — provides an alternative that is geographic, not engineered, and that no rival can construct.

Chatham House was explicit about the competitive implication: Saudi Arabia’s two coastlines give it “a significant geographical advantage over its neighbours, which it will look to capitalize on to distinguish itself — especially from the UAE — as the region’s main export and logistics hub.” The UAE’s unilateral OPEC exit on May 1, 2026, reflected that recognition in action. Abu Dhabi cannot replicate the Red Sea bypass — its crude has no overland route to a non-Hormuz port, and its strategic options narrow with every month the strait stays contested.

The Red Sea economy MBS is constructing is not a temporary wartime adaptation that reverses when the shipping lanes reopen. Pipeline conversion can be undone, but terminal capacity, hydrogen plants, and data centers cannot be unbuilt — the Nvidia chips arriving in 2026 do not migrate east because Hormuz normalizes, and the Oxagon port does not close because tankers resume Gulf loading. Every quarter of construction on the western coast widens the two-coast advantage over neighbors who have no western coast at all, a compounding structural gap that grows regardless of how the war concludes.

When Saudi planners buried a 1,201-kilometer pipeline across the desert in 1981, they were hedging against a war that might close Hormuz. Forty-five years later, supertankers sit queued off Yanbu — Bloomberg and Vortexa counted 27 in the March loading surge — waiting for a coast that is only now learning what it means to be the country’s front door.

Saudi Arabia’s Red Sea Economic Pivot — Key Metrics

| Metric | Pre-War | Current (2026) | Source |

|---|---|---|---|

| Saudi crude production | ~10.4M bpd | 7.25M bpd (−30%) | IEA, May 2026 |

| Yanbu crude exports | ~1.0M bpd | ~4.0–4.3M bpd (+330%) | Bloomberg / Vortexa |

| East-West Pipeline capacity | Shared crude/NGL | 7M bpd (full crude conversion) | Fortune, March 2026 |

| Yanbu terminal loading ceiling | ~4.5M bpd nominal | 5.4–5.9M bpd (max, with aux. berths) | Bloomberg / Vortexa |

| Structural export gap | — | 1.1–1.6M bpd | Chatham House / Vortexa |

| PIF domestic allocation | ~70% | 80% ($912B AUM) | PIF / The National, April 2026 |

| Q1 2026 budget deficit | — | SAR 126B ($33.6B) | Al Jazeera, May 2026 |

| Port of NEOM (Oxagon) | — | 68% complete; 1.5M TEU capacity | NEOM / The National |

| NEOM Green Hydrogen Plant | — | 80% complete; Q3 2026 commissioning | AGBI / The National |

| Trump Forum announced deals | — | $600B total | Saudi Gazette / Newsweek |

| Bab el-Mandeb disruption impact | — | +$20/barrel (JP Morgan est.) | ORF Middle East |

Frequently Asked Questions

What is Saudi Arabia’s non-oil export performance during the war?

Saudi non-oil exports reached SAR 63.3 billion ($16.9 billion) in January and February 2026, up 17.5% year-over-year, providing evidence that the kingdom’s economic diversification is generating measurable returns even during wartime. Foreign reserves climbed to SAR 1.786 trillion ($476.3 billion) — a 10% increase — giving Riyadh a financial cushion for infrastructure spending. Ras Al-Khair Industrial City has attracted $26.67 billion in total investment and hosts the King Salman International Complex for Maritime Industries, a shipbuilding and naval construction facility that positions the kingdom as a regional maritime manufacturer independent of the Red Sea energy corridor.

What happened to NEOM’s Trojena ski resort project?

Trojena shed approximately £3.7 billion (~$4.7 billion) in construction contracts in January 2026, with Webuild and a Hyundai-Samsung consortium both losing their awards, according to AGBI. The cancellations reflect a wartime triage that distinguished between NEOM projects with near-term commercial or logistical utility — Oxagon, the green hydrogen plant — and prestige projects whose returns were speculative and whose timelines extended well beyond the current crisis. Trojena’s losses became Oxagon’s continued funding.

What would it cost and how long would it take to expand Yanbu terminal capacity to match full pipeline throughput?

Closing the gap between the East-West Pipeline’s 7 million bpd capacity and Yanbu’s current loading ceiling requires deepwater berth construction, additional single-point mooring buoys, and tank farm expansion at a scale Yanbu has never previously attempted. Saudi Aramco has not publicly committed to a completion date or capital budget — a silence notable given that the gap costs the kingdom roughly $100 million per day in stranded export revenue. The same contractor market simultaneously building NEOM’s Oxagon and the green hydrogen plant competes for the same deep-water construction capacity, creating a resourcing conflict that MBS has not publicly resolved.

What share of Yanbu crude exports must transit the Bab el-Mandeb strait?

Approximately 70 to 75% of crude exported from Yanbu and destined for Asian markets — Saudi Arabia’s largest customer base — must transit Bab el-Mandeb, which is 18 miles wide at its narrowest point and carries roughly 10% of global trade by volume according to Coface analysis. The 2023-2024 Houthi shipping campaign demonstrated that even low-cost disruption at the strait can force global rerouting, adding two to three weeks to Europe-Asia transit times and raising container freight rates by 200 to 300% on affected routes — costs that would fall directly on the Yanbu export corridor MBS is now building as Saudi Arabia’s primary energy outlet.