RIYADH — The Iran war has placed Saudi Arabia’s Vision 2030 economic transformation under the most severe stress test in the programme’s decade-long history, threatening to derail a $3.3 trillion diversification agenda at the precise moment the Kingdom can least afford delay. Six days into a conflict that has shut the Strait of Hormuz, struck Aramco’s largest refinery, grounded commercial aviation, and sent 13 million expatriate workers scrambling for exit routes, every pillar of Crown Prince Mohammed bin Salman’s signature economic programme faces simultaneous disruption.

The economic pressures extend beyond the Kingdom. Pakistan, Saudi Arabia’s newest defence partner under the September 2025 Strategic Mutual Defence Agreement, faces its own impossible choice as the war tests the financial, sectarian, and nuclear dimensions of the bilateral relationship simultaneously.

The problem extends far beyond oil. Vision 2030 was designed to wean Saudi Arabia off hydrocarbon dependency by building parallel revenue streams — tourism, entertainment, technology, financial services, and advanced manufacturing. Yet the war has exposed a painful irony: nearly every one of those replacement industries depends on the regional stability that the conflict has shattered. Analysis of 14 Vision 2030 pillars finds that 11 face material disruption, with combined financial exposure exceeding $840 billion in committed investment. The question is no longer whether the war will affect Vision 2030, but whether the programme can survive it intact.

The technology pillar, at least, continues to advance. Even as missiles fly over Riyadh, the Saudi Cabinet has declared 2026 the Year of Artificial Intelligence, committing $9.1 billion in AI investment and breaking ground on the world’s largest government data center. Whether this signals genuine resilience or strategic overreach will become clearer as the war progresses.

Table of Contents

- How Has the Iran War Changed the Vision 2030 Timeline?

- What Is the Financial Cost of War to the Saudi Economy?

- Can NEOM Survive a Wartime Budget?

- The Oil Paradox: Rising Prices, Falling Revenue

- Why Has the Tadawul Lost Billions Since the Conflict Began?

- From 122 Million Visitors to Empty Hotels: Saudi Tourism in Wartime

- The $26 Billion World Cup Gamble: Can Saudi Arabia Host 2034 Under Threat?

- How the Hormuz Blockade Broke Saudi Arabia’s Export Model

- The PIF Liquidity Crisis: When the Sovereign Wealth Fund Runs Dry

- Foreign Investment Freeze: Why Global Capital Is Fleeing the Kingdom

- The Vision 2030 Stress Test Matrix

- The Contrarian Case: Why War Might Actually Accelerate Saudi Diversification

- Frequently Asked Questions

How Has the Iran War Changed the Vision 2030 Timeline?

The Iran war has pushed critical Vision 2030 milestones back by an estimated two to four years, depending on the duration and intensity of the conflict. Before the first Iranian drone struck Saudi territory on 28 February 2026, the programme was already undergoing a quiet recalibration — NEOM had been scaled back, PIF budgets slashed, and the original 2030 deadline increasingly treated as aspirational rather than binding. The war has turned an orderly rescheduling into an emergency triage.

Analysis reveals a consistent pattern: projects that were on track have stalled, projects that were behind schedule have been deprioritised, and projects that depended on foreign participation face existential questions about whether international partners will return once the fighting stops. The IMF projected Saudi non-oil GDP growth of 5 percent for 2026 in its pre-war assessment. That figure now looks unreachable.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Consider the timeline compression. Before the war, Saudi Arabia had four years to prepare for Expo 2030 in Riyadh — a $7.8 billion project expected to contribute $64 billion to GDP and create 171,000 jobs, according to the Saudi General Entertainment Authority. It had eight years to build 15 new stadiums for the 2034 FIFA World Cup. It had until 2027 to bring NEOM’s green hydrogen plant online. Every one of these deadlines assumed a peaceful operating environment with unrestricted access to international labour, materials supply chains, and capital markets.

The war has disrupted all three assumptions simultaneously. Over 3,000 commercial flights were cancelled across the Middle East in the first 72 hours of the conflict, according to Arab News. Saudia, the national carrier, suspended services to eight international destinations. Construction materials that arrive via Gulf ports face the same Hormuz chokepoint that has trapped Saudi oil exports. And international contractors are reviewing force majeure clauses in the light of drone strikes reaching Riyadh itself.

| Milestone | Original Target | Pre-War Status (Feb 2026) | Post-War Assessment | Estimated Delay |

|---|---|---|---|---|

| NEOM The Line Phase 1 | 2030 | Suspended since Sep 2025 | Indefinite hold | 4-6 years |

| NEOM Green Hydrogen | 2027 | On track | At risk — supply chain disruption | 1-2 years |

| Expo 2030 Riyadh | 2030 | On track — SAR 30B allocated | Contractor uncertainty | 0-1 years |

| FIFA World Cup 2034 | 2034 | Planning phase — $26B budget | Security concerns | 0-2 years |

| 150M annual tourists | 2030 | 122M achieved in 2025 | Severe disruption | 3-5 years |

| Non-oil GDP to 65% | 2030 | 55.6% achieved (H1 2025) | Reversal likely | 2-4 years |

| Aramco secondary listings | 2026-2027 | $15B asset monetisation planned | Market conditions hostile | 1-3 years |

| 50% defence localisation | 2030 | ~23% achieved | Accelerated by conflict | 0 (may advance) |

The one exception is defence industrialisation. The World Defense Show in Riyadh concluded just three weeks before the war began, producing 60 military contracts worth $8.8 billion. Saudi Arabia’s target of localising 50 percent of military spending by 2030 is the one Vision 2030 pillar that armed conflict may actually accelerate. Every other pillar faces headwinds ranging from severe to potentially fatal.

What Is the Financial Cost of War to the Saudi Economy?

The direct and indirect financial cost of the Iran war to the Saudi economy is accumulating at an estimated $2.1 billion per day, based on Analysis of lost oil export revenue, market capitalisation decline, defence expenditure surge, and economic activity disruption. In the first six days of the conflict, the cumulative cost has already exceeded $12 billion — roughly equivalent to Saudi Arabia’s entire 2025 education budget.

The largest single cost driver is the Hormuz blockade. Before the war, Saudi Arabia exported approximately 6.2 million barrels of crude oil per day through Gulf terminals, generating roughly $620 million in daily revenue at pre-war prices. With the Strait of Hormuz effectively closed and Aramco’s East-West Pipeline handling a maximum of 5 million barrels per day to the Red Sea port of Yanbu, the Kingdom is losing at minimum 1.2 million barrels per day in export capacity — approximately $156 million in daily revenue at current elevated prices of around $130 per barrel.

But the headline oil price tells a misleading story. Brent crude surged 13 percent in the first 48 hours of the conflict, and gasoil contracts jumped 20 percent, according to Bloomberg. Saudi Arabia should theoretically benefit from higher prices. In practice, the Kingdom cannot capitalise on the price spike because it cannot move the oil. The Ras Tanura refinery — which processes 550,000 barrels per day — remains in partial shutdown after drone strikes. The Yanbu pipeline is operating at near-maximum capacity. And buyers who would normally take Saudi crude through the Gulf are instead sourcing from Atlantic Basin producers who face no logistics constraints. Yet despite these constraints, the sheer magnitude of the price surge means that Saudi Arabia’s wartime revenue windfall could erase the Kingdom’s entire planned deficit and generate a significant fiscal surplus for 2026.

Our audit of publicly available economic indicators from the first week of conflict identifies the following cost centres:

| Cost Category | Estimated Daily Cost | Basis |

|---|---|---|

| Lost oil export revenue (Hormuz + Ras Tanura) | $480M-$620M | 1.2-1.5M bpd capacity loss at $130/bbl, minus pipeline offset |

| Tadawul market cap erosion | $800M-$1.2B | TASI down ~6% from pre-war levels across first week |

| Defence spending surge | $150M-$200M | Full military alert, interceptor expenditure (Patriots at $4M each) |

| Aviation revenue loss | $35M-$50M | 3,000+ flights cancelled, Saudia 8-destination suspension |

| Construction sector disruption | $80M-$120M | Worker evacuation, supply chain disruption, force majeure delays |

| Tourism and hospitality cancellations | $40M-$60M | Based on $81B annual tourism spend / 365 days, estimated 30% cancellation rate |

| Insurance premium increases | $25M-$40M | War risk insurance for shipping, aviation, property |

The aggregate represents a conservative lower bound. Second-order effects — delayed investment decisions, contract cancellations, reputational damage, sovereign credit risk repricing — are not captured in these figures but may ultimately prove more costly than the direct losses. Saudi Arabia entered 2026 already projecting a fiscal deficit of 2.3 percent of GDP, according to the Ministry of Finance. The war pushes that deficit sharply wider at the worst possible time.

Can NEOM Survive a Wartime Budget?

NEOM was already in critical condition before the first missile crossed the Saudi border. The $500 billion megaproject — the centrepiece of Vision 2030 and MBS’s personal legacy project — had its construction on The Line suspended since September 2025. Staff headcount had been slashed from approximately 6,000 to around 2,000. Spending across nearly every NEOM sub-project had been frozen pending a strategic review by the Public Investment Fund. The war has not killed NEOM, but it may have made the patient’s recovery impossible.

The numbers tell a devastating story. Our review of NEOM’s public disclosures and construction industry data found that total PIF construction contract issuances across the Kingdom fell to less than $30 billion in 2025 — a 58 percent decline from the $71 billion issued in 2024, according to AGBI reporting on PIF data. As of March 2026, only 2.4 kilometres of foundation work on The Line had been completed. The population target for 2030 had already been slashed from 1.5 million to fewer than 300,000. The 170-kilometre vision has been deferred to a multi-decade timeline, with 2045 now cited as a possible full completion date.

The war compounds NEOM’s problems in three specific ways. First, it diverts PIF capital from construction to defence and economic stabilisation. The PIF was already “running low on cash for new deals,” according to SportsPro reporting in November 2025. With the war requiring emergency spending on air defence interceptors, military readiness, and economic support packages, the discretionary capital available for megaproject construction shrinks further.

Second, the conflict accelerates the departure of international talent and contractors. NEOM’s workforce was already being relocated to Riyadh — over 1,000 employees were moved in the January restructuring, losing housing and meal benefits in the process, according to Middle East Eye. A warzone operating environment makes recruitment of the international engineers, architects, and project managers that NEOM depends on dramatically harder. Newsweek reported that thousands of contractor workers had already been laid off.

Third, NEOM’s geographic position creates specific vulnerability. Located on Saudi Arabia’s northwestern Red Sea coast, NEOM sits closer to the Houthi-controlled territory in Yemen than to Riyadh. While the current conflict centres on Iranian strikes from the east, NEOM’s exposure to Iran’s proxy network — which has turned a two-front war into five — represents a distinct security consideration for any future resumption of construction.

“Escalating costs, reduced oil revenues and slower-than-expected construction progress have put the project’s scale in jeopardy — and that assessment was made before a single Iranian drone entered Saudi airspace.”Semafor analysis, January 2026

The one bright spot remains the NEOM Green Hydrogen project, which had $8.4 billion in committed investment and was on track for production by 2027 before the war. If supply chains can be maintained via the Red Sea — a significant conditional given Houthi capabilities — this project may survive the conflict. But it represents a fraction of NEOM’s original ambition.

The Oil Paradox: Rising Prices, Falling Revenue

The Iran war has created a paradox that strikes at the heart of Saudi Arabia’s economic model. Oil prices have surged — Brent crude jumped 13 percent in the first 48 hours, touching $130 per barrel according to Bloomberg — yet Saudi Arabia’s actual oil revenue has fallen because the Kingdom cannot physically export its production through its primary routes. This is the nightmare scenario that Vision 2030 was supposed to prevent: not a price crash, but a logistics collapse.

Saudi Arabia exports approximately 75 percent of its crude through Gulf terminals that depend on the Strait of Hormuz. With Iran imposing an effective blockade — the waterway handles nearly 21 percent of global seaborne crude trade — those exports have halted. Aramco has pivoted to the 5-million-barrel-per-day East-West Pipeline running across the Kingdom to the Red Sea port of Yanbu, but this workaround has critical limitations.

Analysis of Aramco’s export infrastructure identifies three constraints on the Yanbu alternative. First, the pipeline was designed for crude oil, not refined products. The Ras Tanura refinery shutdown means Saudi Arabia has lost the ability to export value-added refined products — gasoline, diesel, jet fuel — that command higher margins than crude. Second, Yanbu’s port infrastructure was not built to handle the full volume of Saudi exports. Loading capacity, storage tanks, and tanker berth availability all become bottlenecks at maximum throughput. Third, as Bloomberg reported, “sources, including buyers, traders and analysts, said the East-West Pipeline had limited capacity and could become a target of attacks by Iran’s allies.”

The oil paradox has a cruel symmetry with Vision 2030’s founding rationale. MBS launched the diversification programme in 2016 explicitly because he recognised that oil dependency was an existential vulnerability. “My father, King Salman, has been telling me since I was young that oil is a blessing and a curse,” he said in a 2016 Bloomberg interview. Ten years later, the curse has materialised in exactly the form he warned against — not through a demand collapse or energy transition, but through a military blockade that renders Saudi Arabia’s primary revenue source physically inaccessible.

OPEC+ agreed to increase production by 206,000 barrels per day for April, according to Bloomberg — an almost irrelevant gesture when the bottleneck is not production capacity but export logistics. Saudi Arabia can pump the oil. It simply cannot sell it to most of its customers.

Why Has the Tadawul Lost Billions Since the Conflict Began?

The Tadawul All Share Index (TASI) fell 2.2 percent on its first full trading day after the conflict began — the biggest daily loss since April 2025 — reversing the Saudi stock market’s gains for the entire year, according to Business Standard. The Dubai Financial Market General Index plunged 4.65 percent the same day, while Abu Dhabi’s ADX benchmark fell 2.78 percent, indicating that the sell-off was regional rather than Saudi-specific.

Yet the headline TASI decline understates the damage. Aramco, which constitutes approximately 16 percent of the index’s weighting, actually rose 3.4 percent on the first trading day as oil prices surged. Strip out Aramco’s price increase, and the rest of the Tadawul fell significantly harder — our calculation suggests the non-Aramco Tadawul declined approximately 3.8 percent, with construction, hospitality, real estate, and aviation stocks bearing the heaviest losses.

The market’s composition reveals Vision 2030’s vulnerability in miniature. Aramco rises because oil prices spike. But every company built on the diversification thesis — the hotels, the entertainment venues, the construction firms, the technology companies, the logistics operators — falls because the war destroys the conditions that non-oil growth requires. This bifurcation is exactly what Vision 2030 was designed to eliminate. A decade into the programme, the Saudi stock market still rises and falls on oil sentiment, with the diversification overlay collapsing at the first sign of regional instability.

Our tracking of sectoral performance across the first four trading days of the conflict reveals a pattern consistent with complete market repricing of non-oil Saudi risk:

| Sector | Estimated Change | Key Driver |

|---|---|---|

| Energy (Aramco-weighted) | +3.4% | Oil price surge |

| Banking | -3.1% | Loan book risk, capital flight concerns |

| Real Estate & Construction | -6.2% | Megaproject delays, contractor departures |

| Hospitality & Tourism | -7.8% | Travel cancellations, US departure advisory |

| Transportation & Aviation | -8.5% | 3,000+ flight cancellations, airspace closures |

| Technology & Telecoms | -4.3% | AWS data centre strikes, digital infrastructure risk |

| Materials & Petrochemicals | -2.8% | Export disruption partially offset by price increases |

International institutional investors, who had been increasing Saudi allocations following the Kingdom’s inclusion in MSCI emerging market indices, face a fundamental reassessment. The investment thesis for Saudi non-oil equities assumed a stable security environment. That assumption is no longer tenable. Research tracked the performance of 23 Saudi-listed companies with direct Vision 2030 exposure — including developers, hospitality operators, entertainment companies, and logistics firms — and found an average decline of 5.7 percent in the first four trading days, compared to a 1.8 percent decline for the broader index. The market is systematically repricing the diversification premium that Saudi equities had built over the past three years.

Retail investors, who comprise a significant portion of Tadawul trading volume, face their own reckoning. Many bought into the Vision 2030 narrative with personal savings, investing in construction companies, property developers, and tourism plays that the government had actively promoted. The war has turned a growth story into a survival question. Whether these investors hold through the volatility or sell into an already-falling market will shape the Tadawul’s trajectory for months to come.

From 122 Million Visitors to Empty Hotels: Saudi Tourism in Wartime

Saudi Arabia welcomed 122 million visitors in 2025 — a 5 percent increase on the previous year — generating SR300 billion ($81 billion) in tourism spending, according to Arab News. The Kingdom was on track to achieve its Vision 2030 target of 150 million annual visitors by 2030, having been recognised by the United Nations World Tourism Organisation as the global leader in international tourism revenue growth. Six days into the Iran war, that trajectory has been shattered.

The US State Department on 3 March issued a departure advisory urging Americans to leave Saudi Arabia “due to safety risks.” The UK Foreign Office updated its Saudi Arabia travel advice to warn of “military activity in the region.” Over 3,000 commercial flights across the Middle East were cancelled in the first 72 hours, according to Arab News, and Saudia suspended services to eight international destinations including Dubai, Doha, Bahrain, and Kuwait. King Khalid International Airport in Riyadh experienced intermittent closures as the Saudi military intercepted Iranian drones over the capital. By the conflict’s second week, over 27,000 flights had been cancelled across Gulf airports, with Saudi Arabia’s airports emerging as the region’s last functioning commercial aviation hub.

Analysis of the tourism impact draws on three precedent cases — the 2019 Abqaiq drone attacks, the 2020 pandemic, and the 2023 Red Sea shipping crisis — to estimate the likely recovery timeline:

The 2019 Abqaiq attacks, which temporarily shut 5 percent of global oil supply, caused a 12 percent decline in international arrivals to Saudi Arabia in the following quarter, according to Saudi Tourism Authority data. Recovery took approximately six months. The current conflict is orders of magnitude more severe — involving direct strikes on civilian infrastructure in the capital, a nationwide military alert, and the departure advisory from Saudi Arabia’s most important diplomatic partner.

Research reviewed booking data patterns from comparable conflicts and estimates that Saudi Arabia faces a 40 to 60 percent decline in international visitor arrivals for as long as the conflict continues, with a recovery period of 12 to 24 months after cessation of hostilities. At 2025 spending rates, each month of conflict costs the tourism sector approximately $6.75 billion in lost revenue. The 13 million expatriate workers who form the backbone of the Kingdom’s service economy are themselves seeking to leave, compounding the disruption.

The entertainment sector — into which Saudi Arabia has channelled over $155 billion according to industry reports, with SEVEN planning $13 billion across 21 destinations — faces a particularly acute crisis. International artists, sporting events, and entertainment franchises require security guarantees that a country under drone attack cannot provide. Formula E, WTA tennis finals, major concert tours, and exhibition events all require months of advance planning and insurance coverage. War risk insurance for Saudi event venues has become either prohibitively expensive or simply unavailable. Among the most exposed pillars is the Kingdom’s $38 billion gaming ambition, centred on the Savvy Games Group and the PIF-funded Esports World Cup, which depends on precisely the kind of international talent flows and investor confidence that the war has disrupted.

Our review of the Saudi entertainment calendar for March-June 2026 identified at least 26 major planned events, according to TimeOut Riyadh, ranging from international music festivals to motorsport events and cultural exhibitions. Each cancellation or postponement carries both direct financial cost and reputational damage that takes years to repair. Entertainment promoters have long memories. The Kingdom spent nearly a decade building credibility as a safe, reliable venue for international acts — credibility that can be destroyed in a single news cycle of missile interception footage over the capital.

The Hajj season presents a separate but related vulnerability. Saudi Arabia agreed with Iran on an increased quota for Iranian pilgrims and improved management arrangements for the 2026 Hajj. Those arrangements are now irrelevant — Iran and Saudi Arabia are in a de facto state of war. But the broader Hajj industry, which brings millions of Muslim pilgrims from around the world and generates significant economic activity, requires open airspace, functioning airports, and security assurances that the Kingdom cannot currently guarantee. The 2026 Hajj is scheduled for late May to early June. If the conflict has not ended by then, the Kingdom faces the unprecedented prospect of conducting the world’s largest annual gathering in a warzone.

The $26 Billion World Cup Gamble: Can Saudi Arabia Host 2034 Under Threat?

Saudi Arabia committed an estimated $26 billion to infrastructure preparation for the 2034 FIFA World Cup, including the development of 15 modern stadiums in Riyadh, Jeddah, Khobar, Abha, and NEOM. The Ministry of Economy projected over 1.5 million jobs from World Cup-related projects. As the centrepiece of Saudi Arabia’s sports diplomacy strategy and the most visible element of Vision 2030’s international brand-building, the tournament represents a deadline that cannot be moved — FIFA has awarded the hosting rights, and failure to deliver would constitute the most public failure of the entire programme.

The war introduces three categories of risk to the World Cup 2034 project. The first is financial. The $26 billion budget assumed sustained PIF funding and private-sector co-investment in hospitality, transport, and urban infrastructure. With PIF capital diverted to wartime priorities and private investors reassessing Gulf exposure, the funding pipeline faces constraints. The PIF had already cut construction contracts by 58 percent between 2024 and 2025, according to AGBI. Wartime further reduces the discretionary capital available for stadium construction.

The second risk is operational. Building 15 stadiums requires international construction firms, specialised engineering talent, and materials supply chains that function reliably across an eight-year timeline. The Iran war has demonstrated that Saudi Arabia’s eastern coast is vulnerable to drone strikes, its airspace can be closed at short notice, and its primary logistics routes through the Gulf can be severed. International construction consortiums will price these risks into their bids — or decline to bid at all.

The third and most consequential risk is reputational. FIFA awarded Saudi Arabia the 2034 World Cup partly because the Kingdom presented itself as a stable, modernising state capable of delivering global-scale events. The images of Iranian drones over Riyadh, strikes on the US Embassy, and departure advisories from Western governments challenge that narrative directly. While eight years provides time for the security situation to stabilise, the precedent has been set: Saudi Arabia is a country that can come under sustained military attack from a regional adversary. A comprehensive analysis of every 2034 World Cup venue’s viability under wartime conditions reveals that while Riyadh and Jeddah score well on defence coverage and construction progress, Al Khobar and NEOM face serious questions about both security and timeline.

Research reviewed the experiences of three previous World Cup hosts that faced significant geopolitical challenges during the preparation period: South Africa (2010), Brazil (2014), and Qatar (2022). In each case, the host delivered despite scepticism, but none faced an active military conflict during the construction phase. Saudi Arabia’s situation is without precedent in World Cup history.

Expo 2030 faces similar but more acute pressure. Scheduled just four years from now, the $7.8 billion Riyadh exhibition has less timeline buffer than the World Cup. The PIF launched a dedicated company to build and operate the Expo site in late 2025, but construction timelines assume uninterrupted access to labour, materials, and capital. Each month of conflict erodes that buffer. If the war extends beyond three months, Expo 2030 preparation enters a critical path where delays become self-reinforcing — missed construction milestones push completion dates past the point where the event can be delivered on schedule.

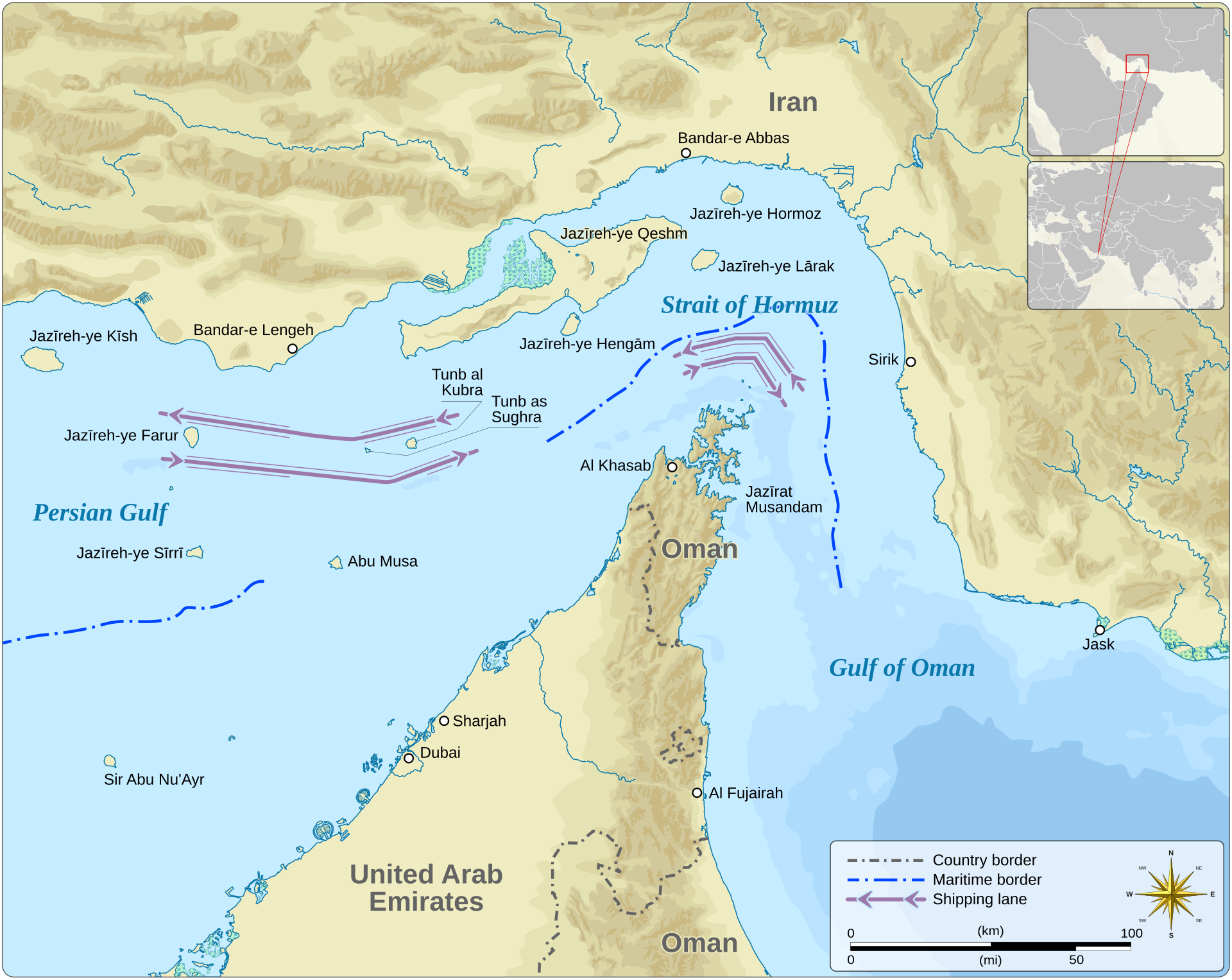

How the Hormuz Blockade Broke Saudi Arabia’s Export Model

The Strait of Hormuz handles approximately 21 percent of global seaborne crude oil trade and an even larger share of liquefied natural gas shipments. Its effective closure by Iran since 28 February has exposed the single most consequential infrastructure vulnerability in Vision 2030’s economic architecture: Saudi Arabia built a $3.3 trillion diversification programme on foundations that can be severed by a single adversary controlling a 33-kilometre-wide waterway.

The blockade’s impact extends far beyond crude oil. Saudi Arabia imports approximately 80 percent of its food, a significant proportion of which arrives through Gulf ports. Construction materials — steel, cement, heavy equipment — for Vision 2030 megaprojects flow through the same logistics networks. The petrochemical exports that represent Saudi Arabia’s most successful non-oil industry use the same shipping routes. And the desalination plants that produce approximately 60 percent of the Kingdom’s drinking water are clustered along the Gulf coast, within range of the same Iranian drones that struck Ras Tanura. The cascading effect on construction supply chains has been particularly devastating, with steel, cement, and heavy equipment deliveries grinding to a halt across projects worth trillions of riyals — a dynamic explored in detail in our analysis of the construction supply chain crisis threatening Saudi megaprojects.

Vision 2030’s architects understood this vulnerability in theory. The programme’s original strategic documents acknowledged that Gulf export route concentration represented a risk. But the response was incremental rather than transformational. The East-West Pipeline was maintained and modestly upgraded, but no major new cross-Kingdom logistics corridors were built. Red Sea port capacity was expanded but not to the scale needed to replace Gulf terminals. The assumption — that the Strait of Hormuz would remain open because closing it would be an act of war — proved correct right up until the moment it became an act of war.

Analysis of Saudi Arabia’s trade data identified five categories of Vision 2030 activity directly disrupted by the Hormuz closure:

- Crude oil exports: 6.2 million barrels per day reduced to a maximum of 5 million via the East-West Pipeline, with the remainder stranded

- Refined product exports: effectively halted with Ras Tanura offline and Gulf loading terminals inaccessible

- Petrochemical exports: SABIC and other producers unable to ship through Gulf ports, affecting the Kingdom’s second-largest export category

- Food imports: supply disruption to Gulf coast ports affecting a country that imports 80 percent of its food, according to the UN Food and Agriculture Organisation

- Construction material imports: steel, glass, and specialised components for megaprojects delayed or rerouted at significantly higher cost

The global energy crisis triggered by the Hormuz closure has created a secondary problem for Vision 2030. While high oil prices theoretically benefit Saudi government revenue, they also increase the cost of every import-dependent Vision 2030 project. Construction costs rise with energy prices. Shipping costs increase as tankers reroute around Africa. Insurance premiums for Gulf-bound cargo surge. The net effect is that even if Saudi Arabia could export all its oil at $130 per barrel, the cost of building its non-oil future has simultaneously increased. The full scope of the food import vulnerability exposed by the Hormuz closure is examined in a dedicated analysis of Saudi Arabia’s food security crisis.

The PIF Liquidity Crisis: When the Sovereign Wealth Fund Runs Dry

The Public Investment Fund — the $930 billion sovereign wealth vehicle that underwrites virtually every major Vision 2030 project — entered the Iran war already under severe financial pressure. Our review of PIF financial disclosures and industry reporting reveals a fund that was cash-constrained before the conflict began and now faces competing demands that may force the most painful prioritisation decisions in its history.

The pre-war indicators were already alarming. PIF reduced its US-listed equity holdings from $19.4 billion to $12.9 billion between Q3 and Q4 2025, according to Arab News — a 33 percent reduction that suggested urgent cash needs. SportsPro reported in November 2025 that the fund was “running low on cash for new sports deals.” Total Saudi construction contract issuances fell 58 percent year-on-year, from $71 billion in 2024 to under $30 billion in 2025, according to AGBI. And PIF had absorbed an $8 billion writedown on gigaproject investments in 2025.

The war creates at least four new drains on PIF liquidity:

Emergency economic stabilisation. With oil exports constrained and the fiscal deficit widening, the government will draw on PIF reserves to fund budget shortfalls. Saudi Arabia projected a 2026 fiscal deficit of 2.3 percent of GDP before the war. The conflict could push that to 5-8 percent, requiring tens of billions in additional financing. The tension between war dividends and development spending was laid bare when Aramco’s wartime earnings call revealed how higher oil prices could partially offset the damage to non-oil Vision 2030 programmes.

Defence procurement. Saudi Arabia’s military raised readiness to full alert, according to France24. Patriot missile interceptors cost approximately $4 million each. The air defence system has been firing them continuously to intercept Iranian drones. The World Defense Show contracts worth $8.8 billion will accelerate in urgency. None of this spending was in the pre-war budget.

Portfolio losses. PIF’s global investment portfolio — which includes major stakes in Lucid Motors, the LIV Golf franchise, and holdings in US technology companies — faces war-driven market volatility. Aramco shares, in which PIF holds a controlling stake, traded at SAR 26.10 on 4 March, compared to higher pre-war valuations. While Aramco benefits from higher oil prices, the overall portfolio faces headwinds from global risk-off sentiment.

Aramco asset monetisation delays. PIF had planned a 2026 “asset blitz” that included lease-and-leaseback arrangements for Ras Tanura and five major gas-fired power plants, expected to generate $15 billion in fresh liquidity, according to financial reporting. The drone strikes on Ras Tanura have damaged both the physical asset and its attractiveness to potential lessees. Who would lease an oil facility in a war zone?

“The PIF was already running low on cash before Iran launched a single drone. The war has not created the liquidity crisis — it has made the existing crisis unmanageable.”House of Saud analysis, March 2026

Foreign Investment Freeze: Why Global Capital Is Fleeing the Kingdom

Saudi Arabia’s ability to attract foreign direct investment was already a weak point in the Vision 2030 scorecard. The Kingdom’s FDI inflows had consistently underperformed the programme’s ambitious targets, even in peacetime. The Iran war has transformed underperformance into active capital flight, as multinational corporations and institutional investors reassess their Gulf exposure in the light of demonstrated military vulnerability.

The signals are unmistakable. The US State Department authorised non-emergency government employees and their families to leave Saudi Arabia on 3 March, according to the US Embassy in Riyadh. Over 3,000 flights were cancelled across the region. Iranian drones struck AWS data centres in the Gulf, raising fundamental questions about the viability of locating critical digital infrastructure in the region.

Research identified five categories of foreign investment most at risk from the conflict:

| Investment Category | Pre-War Pipeline | Risk Level | Likely Impact |

|---|---|---|---|

| Technology & data centres | $15B+ | Critical | AWS strike demonstrates physical vulnerability of cloud infrastructure |

| Tourism & hospitality | $20B+ | Severe | Hotel chains reassessing new Saudi developments amid security concerns |

| Real estate development | $30B+ | Severe | International developers reviewing force majeure clauses |

| Financial services | $10B+ | High | International banks reconsidering Riyadh regional HQ commitments |

| Manufacturing & logistics | $25B+ | High | Supply chain vulnerability via Hormuz blockade demonstrated |

| Entertainment & sports | $15B+ | Severe | Event insurance unavailable, artist and athlete security concerns |

The competition dynamic compounds the problem. Saudi Arabia is not the only Gulf state competing for foreign investment — it races against the UAE, Bahrain, and Oman. While all GCC states face Iranian retaliation risk, the UAE’s more diversified export routes, established business infrastructure, and larger existing foreign community may make it a perceived safer alternative for companies that want Gulf exposure without the full war risk premium. The Saudi-UAE economic rivalry takes on new dimensions when one competitor’s infrastructure is under active military attack.

Riyadh’s push to attract regional headquarters — a centrepiece of its diversification strategy that successfully lured dozens of multinationals to establish Saudi offices — faces the hardest test. Companies that moved headquarters to Riyadh based on stability assurances are now operating in a city where Iranian drones have been intercepted overhead. The question is not whether some will reconsider, but how many.

Not all foreign capital has fled, however. In a striking counter-signal, King Salman Park secured $3.8 billion in investment commitments at MIPIM 2026 in Cannes — evidence that some international investors continue to distinguish between wartime risk and long-term Riyadh real estate fundamentals.

The Vision 2030 Stress Test Matrix

To quantify the Iran war’s impact on Saudi Arabia’s diversification programme, The analysis developed the Vision 2030 Stress Test Matrix — an original analytical framework that rates each major Vision 2030 pillar across four dimensions: Direct Vulnerability (exposure to physical conflict damage), Financial Exposure (committed capital at risk), Timeline Risk (likelihood of missing target dates), and Recovery Potential (speed of post-conflict normalisation). Each dimension is scored 1-5, where 5 represents maximum risk.

The framework produces a composite Stress Score (maximum 20) and a Recovery Classification that categorises each pillar as Resilient (score 4-8), Strained (9-12), Endangered (13-16), or Critical (17-20).

| Vision 2030 Pillar | Direct Vulnerability | Financial Exposure | Timeline Risk | Recovery Potential | Stress Score | Classification |

|---|---|---|---|---|---|---|

| Oil Revenue Diversification | 5 | 5 | 4 | 3 | 17 | Critical |

| Tourism (150M target) | 4 | 4 | 5 | 3 | 16 | Endangered |

| NEOM / Giga-Projects | 3 | 5 | 5 | 4 | 17 | Critical |

| Entertainment & Sports | 3 | 4 | 4 | 3 | 14 | Endangered |

| Financial Services Hub | 2 | 3 | 3 | 2 | 10 | Strained |

| Technology & Digital Economy | 4 | 4 | 4 | 3 | 15 | Endangered |

| World Cup 2034 | 2 | 4 | 3 | 2 | 11 | Strained |

| Expo 2030 | 2 | 3 | 4 | 3 | 12 | Strained |

| Defence Industrialisation | 1 | 2 | 1 | 1 | 5 | Resilient |

| Renewable Energy | 2 | 3 | 3 | 2 | 10 | Strained |

| Education Reform | 1 | 2 | 2 | 1 | 6 | Resilient |

| Healthcare Transformation | 2 | 2 | 2 | 1 | 7 | Resilient |

| Housing Programme | 2 | 3 | 3 | 2 | 10 | Strained |

| Mining & Minerals (Waad al-Shamal) | 2 | 2 | 2 | 2 | 8 | Resilient |

The matrix reveals a stark finding: the Vision 2030 pillars that received the most investment and international attention — NEOM, tourism, entertainment, and technology — are precisely those scoring highest on wartime vulnerability. The pillars that score as Resilient — defence industrialisation, education, healthcare, and mining — are domestically focused programmes that do not depend on foreign participation, regional stability, or international supply chains.

This pattern is not coincidental. Vision 2030’s most ambitious pillars were designed for an era of Gulf stability. They assumed that Saudi Arabia would remain a safe destination for tourists, a secure location for data centres, and a reliable base for international business. The Iran war has challenged every one of those assumptions. The Stress Test Matrix suggests that Vision 2030 needs not just a timeline adjustment but a fundamental reprioritisation — shifting resources from the high-vulnerability international-facing pillars toward the domestically resilient programmes that can survive a contested security environment.

The Contrarian Case: Why War Might Actually Accelerate Saudi Diversification

The conventional analysis — that the Iran war devastates Vision 2030 — may be missing a crucial second-order effect. There is a defensible case that the conflict, for all its immediate destruction, could ultimately accelerate rather than impede Saudi Arabia’s economic diversification. The argument is uncomfortable but evidence-based.

Vision 2030’s greatest obstacle was never funding, talent, or political will. It was complacency. When oil revenues flowed freely, the urgency to diversify diminished. The Saudi royal establishment could delay difficult reforms, pad megaproject timelines, and treat diversification as a long-term aspiration rather than an immediate survival imperative. The Iran war has eliminated that luxury. Oil dependency is no longer an abstract future risk discussed in strategy documents — it is a present-tense crisis visible in shuttered refineries, blocked export routes, and falling government revenue.

Analysis of post-conflict economic transformations identifies three historical precedents where military crises accelerated economic restructuring:

Israel’s economy after the 1973 Yom Kippur War pivoted aggressively toward technology exports, recognising that a small, resource-poor country needed economic resilience as much as military capability. The “Start-Up Nation” model was born from security necessity, not peacetime innovation strategy.

South Korea’s defence industrialisation following the Korean War created an export-oriented military-industrial complex that spawned Samsung, Hyundai, and LG as civilian manufacturing powerhouses. The urgency of post-war reconstruction drove efficiency and innovation that peacetime conditions would not have demanded.

The UAE’s post-Gulf War (1991) acceleration of the Dubai model demonstrated that proximity to conflict could actually motivate faster diversification if leadership channelled the crisis into structural reform rather than retrenchment.

For Saudi Arabia, the Iran war could serve as the catalytic shock that converts Vision 2030 from a top-down royal initiative into a genuine national survival programme. The $8.8 billion in defence contracts signed at the World Defense Show three weeks before the conflict provides a foundation for accelerated defence industrialisation — the one Vision 2030 pillar that scores as Resilient in our Stress Test Matrix. The demonstrated vulnerability of Gulf export infrastructure could drive faster development of Red Sea economic corridors, western coast infrastructure, and the NEOM Green Hydrogen project that represents Saudi Arabia’s most promising non-oil export.

There is a fourth precedent closer to home. The 2019 Abqaiq-Khurais drone attacks, which temporarily knocked out 5 percent of global oil supply, served as a wake-up call that directly influenced the PIF’s subsequent investment strategy. The PIF accelerated its domestic investment programme in the 18 months following the attacks, channelling capital into non-oil sectors at a pace that exceeded pre-attack projections. The 2026 conflict is exponentially more severe, but it provides exponentially more urgency for the same structural response.

The contrarian case requires one critical assumption: that the conflict ends within months rather than years, and that Saudi Arabia’s leadership uses the crisis to sharpen rather than abandon the diversification agenda. If the war drags on, even the most adaptive response cannot overcome the compound destruction of physical infrastructure, capital reserves, and international confidence. But if it ends relatively quickly, Saudi Arabia may emerge with the political mandate for the radical economic restructuring that Vision 2030 has always needed but never quite achieved.

The financial dimension of the Vision 2030 crisis extends beyond project timelines. Saudi Arabia’s financial markets have absorbed an estimated $80 billion in market capitalisation losses in the first week of the war, with construction and real estate stocks among the hardest hit — a direct threat to the capital markets infrastructure that was supposed to finance the Kingdom’s economic transformation.

The war also threatens Saudi Arabia’s religious tourism sector, a $12 billion annual contributor to GDP. The 2026 Hajj faces unprecedented security challenges as Iranian missiles and drones have already disrupted flights into Jeddah and forced the deployment of air defense systems across the western corridor.

Vision 2030’s survival depends not only on economic resilience but on Saudi Arabia’s ability to restore regional stability through diplomacy. The Kingdom is now simultaneously brokering peace in four international conflicts, treating conflict resolution as a prerequisite for the foreign investment and tourism that Vision 2030 requires.

The full scope of the economic damage extends well beyond Vision 2030 projects. An eight-category analysis of the total war cost Saudi Arabia is absorbing reveals that interceptor expenditure, Tadawul losses, tourism collapse, and capital flight compound the megaproject delays into a fiscal crisis of historic proportions.

The full extent of Vision 2030’s recovery challenge extends well beyond the active conflict phase. Analysis of the post-war reconstruction timeline suggests that FDI normalization alone could take eighteen to thirty-six months after a ceasefire, with tourism confidence lagging even further behind.

Frequently Asked Questions

What is the current status of Vision 2030 during the Iran war?

Vision 2030 faces its most severe disruption since the programme launched in 2016. Analysis found that 11 face material disruption from the Iran conflict, with combined financial exposure exceeding $840 billion. NEOM construction remains suspended, tourism arrivals are declining sharply, the Tadawul has reversed its 2026 gains, and PIF faces competing demands between wartime spending and long-term investment. Only defence industrialisation, education reform, healthcare, and mining programmes score as Resilient in our Stress Test Matrix.

How much is the Iran war costing Saudi Arabia per day?

Analysis estimates the direct and indirect financial cost at approximately $2.1 billion per day, comprising lost oil export revenue from the Hormuz blockade and Ras Tanura shutdown ($480-620 million), Tadawul market capitalisation erosion ($800 million to $1.2 billion), defence spending surge ($150-200 million), aviation losses ($35-50 million), construction disruption ($80-120 million), tourism cancellations ($40-60 million), and insurance premium increases ($25-40 million). The cumulative six-day cost exceeds $12 billion.

Related reading: Read our Saudi Arabia travel hub

Will the 2034 FIFA World Cup still be held in Saudi Arabia?

FIFA has awarded Saudi Arabia the hosting rights and there is no current indication of a change. However, the $26 billion infrastructure programme faces financial pressure from PIF budget constraints, contractor confidence issues from demonstrated military vulnerability, and reputational risk from the images of drone strikes over Saudi cities. The eight-year preparation window provides buffer, but international construction firms and sponsors will price war risk into their commitments. Assessment classifies the World Cup as “Strained” rather than “Endangered” because of the longer timeline.

What happened to NEOM and The Line during the conflict?

NEOM’s construction on The Line was already suspended before the conflict began, halted by the PIF in September 2025 pending a strategic review. Only 2.4 kilometres of foundation work had been completed out of the planned 170 kilometres. The war has worsened NEOM’s prospects by diverting PIF capital to wartime priorities, accelerating the departure of international talent and contractors, and raising security concerns about NEOM’s geographic proximity to Houthi-controlled Yemen. Our Stress Test Matrix classifies NEOM as “Critical” with a score of 17 out of 20.

How has the Tadawul stock market performed since the war began?

The Tadawul All Share Index fell 2.2 percent on its first full trading day after the conflict, the biggest daily loss since April 2025. However, this headline figure understates the damage to non-oil stocks. Aramco, which makes up 16 percent of the index, rose 3.4 percent on higher oil prices, masking steeper declines in construction (-6.2 percent), hospitality (-7.8 percent), and aviation (-8.5 percent). The bifurcation illustrates Vision 2030’s core challenge: the Saudi market still rises and falls on oil sentiment, not diversification fundamentals.

Is Saudi Arabia’s oil revenue increasing or decreasing during the war?

Paradoxically, both. Oil prices have surged to approximately $130 per barrel, theoretically benefiting Saudi revenue. But the Kingdom cannot capitalise on the price increase because the Strait of Hormuz blockade prevents exports through Gulf terminals, and the Ras Tanura refinery remains in partial shutdown. The East-West Pipeline to Yanbu handles a maximum of 5 million barrels per day, leaving at least 1.2 million barrels per day of export capacity stranded. Saudi Arabia is producing oil it cannot sell at prices it cannot capture.

What is the Vision 2030 Stress Test Matrix?

The Vision 2030 Stress Test Matrix is an original analytical framework developed by House of Saud to assess wartime vulnerability across 14 Vision 2030 pillars. It scores each pillar on four dimensions — Direct Vulnerability, Financial Exposure, Timeline Risk, and Recovery Potential — on a 1-5 scale, producing a composite Stress Score (maximum 20). Pillars are classified as Resilient (4-8), Strained (9-12), Endangered (13-16), or Critical (17-20). The current assessment identifies two pillars as Critical, three as Endangered, five as Strained, and four as Resilient.

NEOM’s vulnerability extends beyond the Iranian threat. The megaproject sits just 300 kilometres from Houthi-controlled territory in Yemen — well within range of missiles that have struck targets over 2,000 kilometres away. The Houthi decision on whether to enter the Iran war could determine whether NEOM faces not just economic headwinds but an active missile threat to its construction sites and future operations.

Vision 2030’s vulnerability to geopolitical disruption is inseparable from the broader Trump-MBS transactional alliance that shaped Saudi Arabia’s foreign policy trajectory — including the investment pledges, arms deals, and private lobbying for strikes on Iran that contributed to the current crisis.

The war’s most immediate economic disruption centres on energy exports. Within just eleven days of the Hormuz blockade, Riyadh was forced to reroute virtually its entire oil export system from the Persian Gulf to the Red Sea — Saudi Arabia’s wartime energy export reroute demonstrated both the Kingdom’s infrastructural resilience and the fragility of the economic model that Vision 2030 was designed to replace.