RIYADH — Iran’s semi-official Tasnim News Agency, which has documented editorial links to the Islamic Revolutionary Guard Corps, reported on May 18 that Washington’s latest negotiating text includes a temporary waiver on Iranian oil sanctions during ceasefire talks. No US government official has confirmed the claim. Brent crude fell approximately $4 per barrel within hours of publication, from an intraday high of $112 to $107.78 by 1310 GMT, according to Reuters.

The report arrived eighteen hours before President Donald Trump’s scheduled National Security Council meeting on May 19 to review military options against Iran, confirmed by Axios citing two US officials — and one day after Trump posted on Truth Social that the “clock is ticking” for Tehran and “there won’t be anything left of them.” At $107.78, Brent sat below the lower bound of Goldman Sachs’ fiscal break-even estimate for Saudi Arabia ($108–111 per barrel, per Bloomberg), a kingdom that burned through its annual deficit allocation in ninety days. The longer-term price picture is more severe: the EIA projects Brent averaging $79 per barrel through 2027 as Saudi production recovery floods an already oversupplied market — why that timing breaks Vision 2030’s fiscal architecture is a structural problem that no short-term waiver cycle resolves.

Table of Contents

What Tasnim Reported

Tasnim cited “a source close to the negotiation team” as saying that “unlike its previous texts, the Americans had accepted in the new text to waive Iran’s oil sanctions during the negotiation period.” The English-language relay appeared across CNBC, Reuters, Bloomberg, and the Times of Israel liveblog within the hour. L’Orient Today describes Tasnim as “affiliated with the Islamic Revolutionary Guard Corps.”

CNBC noted that “the US hasn’t confirmed that it has offered a waiver publicly.” Reuters attributed the story to “Iranian reports.” The Times of Israel liveblog added a second claimed concession: US flexibility on civilian nuclear activity. No statement from the State Department, Treasury Department, or National Security Council has been located confirming or denying Tasnim’s account. The number of US officials who publicly corroborated the claim as of May 18, across all outlets monitored by Reuters, CNBC, and Bloomberg: zero.

Iran’s formal negotiating position, published via GlobalSecurity.org citing the PDO on May 11, demands a 30-day window for rescinding US sanctions on Iranian oil sales as a Phase 1 condition — before any nuclear discussion begins. Iran insists all sanctions must be “fully lifted” under any final deal.

Brent’s Four-Dollar Swing

Brent July futures rose as much as 2.5 percent in early May 18 trading, touching $112 per barrel — the highest since May 5 — driven by military tensions and the UAE nuclear plant drone attack. After Tasnim published, Brent fell $1.48 (1.4 percent) to $107.78 by 1310 GMT. WTI June futures dropped $1.90 (1.8 percent) to $103.52, off an intraday high of $108.70. The net intraday swing on Brent from peak to settlement direction: approximately $4.22 per barrel, per Reuters and CNBC.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The move sat on a fragile baseline for Riyadh. Goldman Sachs puts Saudi Arabia’s fiscal break-even — including PIF obligations — at $108–111 per barrel (Bloomberg). At $107.78, Brent sat below that floor. Saudi Arabia’s Q1 2026 budget deficit reached a record SR125.7 billion, according to the Saudi Finance Ministry. Brent had touched $111 during IRGC operations running through the Beijing summit days earlier, but triple-digit pricing depends on the expectation that Iranian supply stays off the market. A single Tasnim dispatch tested that expectation and moved the price below Saudi Arabia’s fiscal threshold within hours.

Did Washington Just Reverse a Four-Week-Old Decision?

If the Tasnim report is accurate, the Trump administration is proposing to reinstate a sanctions mechanism it explicitly allowed to lapse four weeks ago. The Office of Foreign Assets Control issued General License U on approximately March 20, authorizing delivery and sale of Iranian-origin crude oil loaded on vessels by that date. Treasury Secretary Scott Bessent announced the measure when oil hit approximately $112 per barrel — the same price Brent reached on May 18 before the Tasnim report — and said it would “help keep oil prices down for 10 to 14 days,” according to NBC News.

General License U covered approximately 140 million barrels over 30 days, expiring April 19. It was a cargo-level transaction authorization — not a country-level waiver, not a Significant Reduction Exception. Treasury stated it “does not authorize any other transactions prohibited by any other Executive order.” Bloomberg reported on April 14 that the administration would let the waiver expire. Iran International confirmed the lapse. The Foundation for Defense of Democracies estimated the waiver provided Iran approximately $139 million per day in additional revenue, publishing its assessment under the title “Funding the Enemy” on March 21.

The policy timeline since April runs in the opposite direction of a new waiver. On May 11, Trump sanctioned a major Chinese oil refinery for purchasing Iranian crude, according to Fortune. On May 15, Trump told CNBC he would “make a decision over the next few days” on whether to lift sanctions on Chinese companies buying Iranian oil. At the Trump-Xi summit around May 13–15, both sides agreed Iran should not obtain a nuclear weapon and that Hormuz should reopen, but China avoided concrete commitments on sanctions enforcement, per RFERL and Al Jazeera. Seven days separated the Chinese refinery sanctions from Tasnim’s claim that Washington had accepted an oil sanctions waiver in its negotiating text.

The Council on Foreign Relations warned in April that renewing waivers benefits US adversaries while letting them expire compounds instability in a market Washington helped unsettle. The Atlantic Council noted separately that sanctions waivers simultaneously provide financial lifelines to Iran and Russia.

Two Signals, Eighteen Hours Apart

Trump’s Truth Social warning on May 17 — “clock is ticking,” “there won’t be anything left of them” — landed one day before Tasnim published the sanctions waiver claim, and two days before the May 19 NSC review of military options, confirmed by Axios citing two US officials. The NSC meeting carried additional weight: the PMF had reached Saudi Arabia’s border, and the agenda extended well beyond Iran’s nuclear file.

Oil traders on May 18 had to price two incompatible inputs simultaneously: military escalation, which pushes crude higher, and sanctions relief, which pushes it lower. The coercive architecture question — whether the annihilation threat and the sanctions waiver hit Iran the same day by design — cuts directly to why the market could not resolve the contradiction. The $4 swing was the market registering the contradiction. If the waiver claim is accurate, Washington is preparing to strike Iran and offering to relieve sanctions on Iranian oil in the same forty-eight-hour window. If the claim is fabricated, an IRGC-aligned outlet managed to move global commodity prices $4 per barrel with a single anonymously sourced report that no government party to the negotiations confirmed.

“Unlike its previous texts, the Americans had accepted in the new text to waive Iran’s oil sanctions during the negotiation period.”

— Tasnim News Agency, citing “a source close to the negotiation team,” May 18, 2026

The timing was precise. Tasnim published while markets were open and before the NSC meeting — maximizing the report’s impact on both crude prices and the policy debate in Washington. The IRGC does not exercise direct editorial control over Tasnim the way it commands its naval forces, but the alignment between the outlet’s coverage of sanctions matters and the IRGC’s institutional interest in keeping Asian buyers purchasing Iranian crude is well established. An unconfirmed claim that sanctions relief is coming serves the same function whether or not it is true: it tells Chinese and Indian refiners that the compliance risk of buying Iranian crude is about to drop.

What Does Saudi Arabia Hedge Against?

Saudi Arabia issued no public statement on the Tasnim report. No comment from Foreign Minister Prince Faisal bin Farhan or the energy ministry has been located as of May 18.

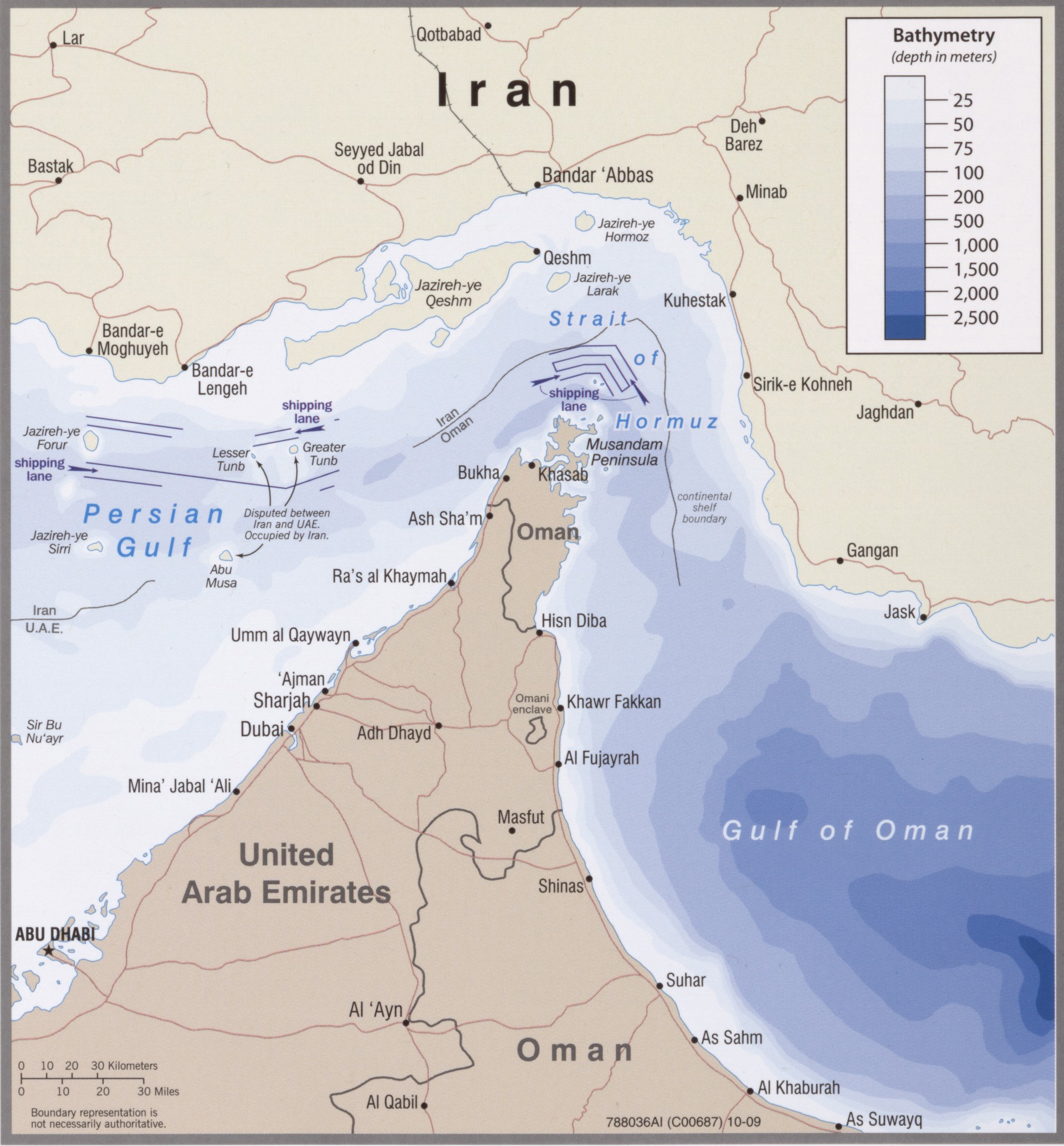

The kingdom’s exposure branches depending on which signal proves real. If Washington offers a sanctions waiver and Iranian crude returns toward pre-war export levels — Iran shipped a record 2.2 million barrels per day in February 2026, per Vortexa, before dropping to 1.71 million bpd in April — Riyadh faces a supply competitor at the moment it can least afford one. Saudi Arabia’s Yanbu loading corridor operates at 4–5.9 million bpd, well below the 7–7.5 million bpd that moved through Hormuz before the war. April production sat at approximately 6.879 million bpd. Every dollar off Brent below $108 compounds a deficit that the first quarter already exhausted.

If no waiver materializes and the Tasnim report is an information operation, the damage is different but not absent. An IRGC-affiliated outlet demonstrated on May 18 that it can move Brent $4 with an unconfirmed claim. During the March–April General License U window, the waiver channeled discounted Iranian crude from China toward India, disrupting China’s near-monopsony over sanctioned Iranian supply and accelerating a shift in Saudi Arabia’s traditional customer base, according to Vortexa and Iran International. A second waiver — or even the sustained expectation of one — extends that disruption into Aramco’s forward pricing.

Iran’s crude production dropped from 3.065 million bpd in March to 2.854 million bpd in April, partly due to Israeli strikes on South Pars condensate processing, according to Columbia University’s Center on Global Energy Policy. But production capacity and export recovery speed are separate variables. A waiver does not rebuild South Pars overnight, but it removes the legal risk that currently keeps non-Chinese buyers on the sideline — and it was non-Chinese buyers, primarily Indian refiners, who moved fastest during General License U.

The OFAC Mechanism and Its Precedents

The Trump administration has oscillated on Iran oil sanctions across two terms. In November 2018, during Trump’s first term, the administration granted 180-day Significant Reduction Exceptions to eight countries: China, India, South Korea, Japan, Italy, Greece, Taiwan, and Turkey. On April 22, 2019, Secretary of State Mike Pompeo announced no extensions, citing the goal of reducing Iranian exports to “zero across the board.” China continued purchasing Iranian crude outside the waiver system using shadow-fleet mechanisms.

General License U in March 2026 was a different instrument — a cargo-level, time-bound authorization rather than a country-level exemption. Bessent described it as “tightly circumscribed.” The 30-day window and 140-million-barrel scope matched the operational need (relieving a $112 price spike) without conceding the broader maximum-pressure framework. Letting it lapse in April returned sanctions enforcement to pre-March conditions.

If a new waiver has entered the US negotiating text — as Tasnim claims — it would mark the third policy shift in the current term: waiver (March), revocation (April), re-waiver (May). The 30-day duration demanded by Iran’s draft proposal matches the General License U precedent exactly, though for opposite purposes — Tehran frames 30 days as a minimum trust-building condition, while Washington framed 30 days as a maximum containment window. That structural echo is the kind of ambiguity both CENTCOM planners and Aramco’s pricing team have to price in real time, against a sanctions regime that has shifted three times in ten weeks.

Frequently Asked Questions

Has an IRGC-affiliated media report moved oil markets before this incident?

Yes. IRGC-linked outlets have triggered intraday crude volatility multiple times during the current conflict, primarily through military claims — Hormuz closure status, naval exercises, and pipeline attack announcements via Fars News and Tasnim. The INSS tracking project, in coordination with NewsGuard, identified over 37,000 AI-generated or IRGC-aligned content items reaching an estimated 145 million views, with 72 percent distributed via TikTok. The May 18 incident is distinct because it moved markets on a diplomatic claim — sanctions relief — rather than a kinetic one, and because the price moved below Saudi Arabia’s fiscal break-even threshold.

What would a new sanctions waiver mean for Indian crude buyers?

During General License U (March–April 2026), India resumed Iranian crude purchases after a seven-year hiatus, with Indian Oil Corporation and BPCL among the entities navigating the authorization. Indian refiners purchased Iranian crude at a discount of $6–8 per barrel below Brent during that window, creating a direct price competitor to Saudi Arab Light in the Indian market. A new waiver could accelerate what the first window began: redirecting Iranian flows from China’s shadow fleet toward legitimate Indian refineries. India’s Nayara Energy, partially owned by Rosneft, faces a separate compliance layer, as its Russian ownership structure intersects with both Iran and Russia sanctions regimes.

What is the gap between Iran’s production capacity and its actual export volumes?

Iran’s April production of 2.854 million bpd (Columbia University’s CGEP, CEIC data) sits 1.14 million bpd above its April export figure of 1.71 million bpd (Vortexa). That gap reflects two separate constraints operating simultaneously: physical damage to South Pars condensate infrastructure from Israeli strikes, which caps what Iran can produce, and the legal risk premium that keeps non-Chinese buyers out of the market, which caps what Iran can sell. A sanctions waiver addresses only the second constraint. It does not repair South Pars, but it does allow Indian and other Asian refiners to absorb Iranian barrels currently moving through the Chinese shadow fleet — volumes that would otherwise not compete directly with Saudi grades in transparent markets.

How does the Tasnim report relate to the Trump-Xi summit?

At the Trump-Xi meeting around May 13–15, both leaders agreed Iran should never obtain a nuclear weapon and that Hormuz should reopen, according to RFERL and Al Jazeera. Trump raised the possibility of sanctions flexibility for some Chinese refiners handling Iranian crude in exchange for Chinese purchases of US crude — though this was not confirmed publicly. Beijing avoided concrete commitments on enforcement. The Tasnim report three days later could reflect an actual concession discussed in that context, or it could represent Tehran’s attempt to lock in a position that was floated but never formalized — pressuring Washington to own a proposal it may only have tested.

Why does 30 days matter in both the US and Iranian positions?

The 30-day unit appears in both frameworks, but the two sides assign it opposite meanings. For Washington, 30 days was a ceiling: General License U was a contained, expiring authorization designed to relieve a price spike without conceding the maximum-pressure architecture. For Tehran, 30 days is a floor — the minimum window Iran requires before any nuclear discussion begins, framed as a precondition for establishing good faith. Any new waiver negotiated on the 30-day model would enter a draft text already carrying that definitional dispute unresolved. Whether 30 days is a temporary market tool or a treaty obligation is not a detail — it is the negotiation.