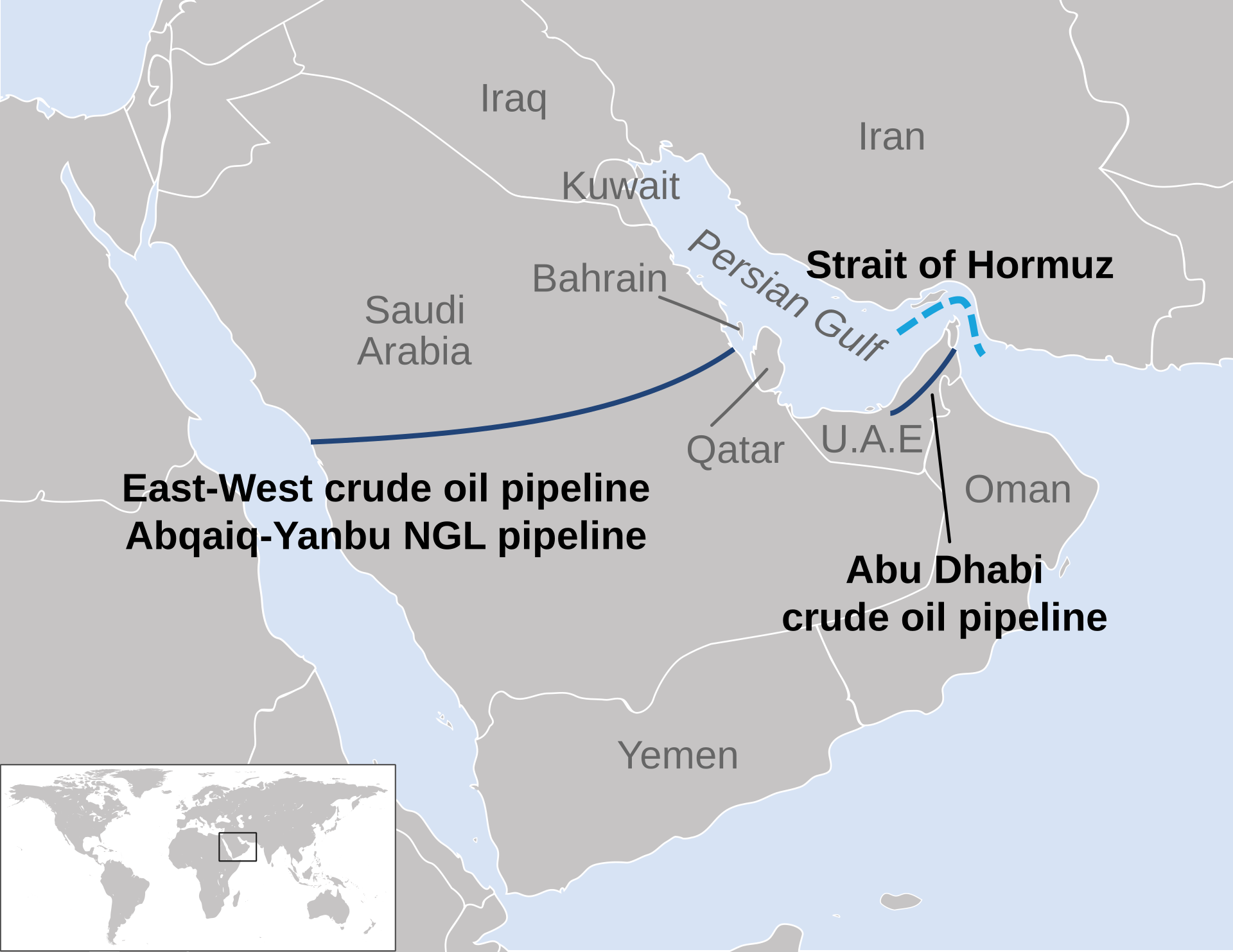

DHAHRAN — Saudi Arabia’s East-West Pipeline — the Petroline — reached its physical maximum throughput of seven million barrels per day on March 11, 2026. No additional bypass capacity exists between the kingdom’s eastern oil fields and the Red Sea.

Bloomberg and Fortune covered that number as a milestone. Neither addressed the constraint at the other end. Yanbu port’s two loading terminals can operationally handle approximately three to four million barrels per day under wartime conditions, according to Vortexa and Argus Media estimates. Three domestic refineries draw roughly one million barrels per day from the pipeline before any crude reaches a tanker. The effective Saudi export ceiling while the Strait of Hormuz remains closed sits closer to four million barrels per day than seven.

That gap converges on three deadlines within seventy-two hours. OPEC+ meets Saturday to approve a quota increase Saudi Arabia is already three million barrels short of filling. Aramco pays a $21.89 billion dividend Monday against $18.6 billion in free cash flow. Iran is expected to formally reject the Trump MOU proposal the same day. The Petroline was designed in 1979 to survive a Hormuz disruption measured in weeks. It entered its eighty-sixth day of maximum-capacity operation on June 4.

Table of Contents

What Is the Petroline’s Physical Maximum?

The Petroline’s maximum physical throughput is seven million barrels per day — a ceiling confirmed by Aramco CEO Amin Nasser on the Q4 2025 earnings call on March 10, 2026, and achieved the following day. The increase from the pipeline’s prior five-million-barrel capacity came from converting the parallel 48-inch natural gas liquids pipeline to crude oil service, an emergency measure first prepared after the Abqaiq-Khurais drone strikes of September 2019. No third pipeline exists in the corridor.

King Khalid authorized the Petroline in 1979, during the Iran-Iraq War, at a cost of approximately $2.5 billion. Bechtel completed the 1,201-kilometer line from Abqaiq to Yanbu in 1981. The system comprised two parallel pipes — a 56-inch main crude line and a 48-inch NGL line — running the full width of the Arabian Peninsula from the Eastern Province to the Red Sea coast.

The crude line reached approximately five million barrels per day by the early 1990s. The NGL line continued carrying gas and petrochemical feedstocks to Yanbu’s industrial complex for more than three decades. Dual service — crude and natural gas liquids moving west in parallel — was the Petroline’s operating mode from commissioning until the Hormuz closure forced a choice between the two.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The September 2019 Abqaiq-Khurais strikes — eighteen drones and seven cruise missiles that temporarily knocked out 5.7 million barrels per day of Saudi processing capacity — exposed a vulnerability the original Petroline design had not contemplated. Aramco’s engineers began preparing the NGL pipeline for rapid conversion: modifying pump configurations, installing crude-compatible valve assemblies, and testing the 48-inch line for the higher viscosity and corrosion profile of Arabian Light crude. The preparation took years. The conversion itself, when Hormuz closed, took days.

On the Q4 2025 earnings call (S&P Global Commodity Insights), Nasser told analysts the pipeline would reach full throughput “in the next couple of days.” He described the system as “a critical supply artery, helping to mitigate the impact of a global energy shock and providing relief to customers affected by shipping constraints in the Strait of Hormuz.” Three months later, Aramco’s Q1 2026 results — released May 10 — confirmed seven million barrels as “the maximum capacity.”

The word “maximum” distinguishes a ceiling from a waypoint. The 48-inch NGL line was the only reserve pipeline in the corridor. It now carries crude. No parallel right-of-way has been permitted for a third line, and the corridor’s pumping stations — more than a dozen along the 1,201-kilometer route — are already operating at their engineering limits.

Why Is Yanbu the Binding Constraint?

Yanbu’s two loading terminals — Yanbu North and Yanbu South — have a nominal combined capacity of approximately 4.5 million barrels per day, according to Argus Media. Tested wartime operational throughput is lower: approximately three to four million barrels per day, per Vortexa estimates. The port, not the pipeline, determines how many barrels Saudi Arabia can actually export while Hormuz remains closed.

Before the conflict, Yanbu loaded roughly 1.1 to 1.3 million barrels per day, according to Kpler data. Most of that volume served Asian and Mediterranean refiners who preferred the Red Sea route for transit-time reasons rather than supply necessity. The port’s berths, buoy mooring systems, and anchorage areas were engineered for that peacetime volume — a diversification outlet, not a wartime lifeline. Yanbu crude loadings peaked at approximately 4.3 million barrels per day in late March 2026 (Kpler), a fourfold increase from pre-war levels and, functionally, the port’s ceiling.

The fourfold increase has exposed every physical limitation. In March 2026, 68 percent of arriving VLCCs experienced anchorage delays exceeding thirty-six hours as pipeline inflows overwhelmed loading berth capacity (Argus Media / Vortexa). Tanker demurrage costs compound at several tens of thousands of dollars per day per vessel. The queue at Yanbu in late March stretched to timelines that pre-war port engineers would have treated as a system failure, not a steady state.

The port’s berths were designed for a rotation cycle in which vessels arrived, loaded, and departed within roughly twenty-four hours — the standard for a facility processing 1.1 million barrels per day. At four times that volume, the entire logistics chain has compressed. Pilot availability, tugboat scheduling, pipeline-to-berth manifold connections, and anchorage spacing all operate at or beyond their design tolerances. Yanbu was built to supplement Ras Tanura on the Gulf coast, which handled the majority of Saudi crude exports before Hormuz closed. It was never designed to replace it.

Three domestic refineries consume crude from the Petroline before any barrel reaches a tanker berth. SAMREF processes 400,000 barrels per day. YASREF handles approximately 405,000. The Aramco Yanbu refinery takes 240,000. Combined domestic draw: roughly 1.045 million barrels per day, according to Pipeline Technology Journal data.

| Component | Volume (bpd) | Source |

|---|---|---|

| Pipeline maximum throughput | 7,000,000 | Aramco Q1 2026 |

| Domestic refinery draw (SAMREF + YASREF + Yanbu) | ~1,045,000 | Pipeline Technology Journal |

| Pipeline volume available for export | ~5,955,000 | Calculated |

| Yanbu port nominal capacity | ~4,500,000 | Argus Media |

| Yanbu port wartime operational throughput | ~3,000,000–4,000,000 | Vortexa |

| Peak wartime loadings (March 2026) | ~4,300,000 | Kpler |

| Saudi OPEC+ quota | 10,291,000 | OPEC |

| Estimated actual production | ~7,250,000 | OPEC MOMR |

| Involuntary shortfall vs. quota | ~3,041,000 | Calculated |

Aramco’s Q1 2026 results showed liquids production averaged 10.6 million barrels per day. At the pipeline’s full seven-million-barrel throughput, roughly 3.6 million barrels of daily eastern production have no westward route. After the refinery draw and Yanbu’s loading constraints, the crude that reaches a paying customer totals approximately three to four million barrels per day — less than 40 percent of total production.

Can Saudi Arabia Build Beyond Seven Million?

Not within any timeline relevant to the current conflict. Janiv Shah, Vice President of Commodity Markets at Rystad Energy, told The National that building additional bypass capacity is technically possible but “involves a lot of investment and requires time.” Engineering News-Record assessed in March 2026 that closing the remaining gap “would require a construction program without precedent in the region’s infrastructure history, undertaken while the adversary targeting the existing terminals remains in the field.”

The NGL-to-crude conversion was a one-time maneuver, and it is irreversible under current conditions. Saudi Arabia cannot simultaneously carry natural gas liquids and crude oil through the same 48-inch pipe. The petrochemical feedstock supply chain that depended on the NGL line — feeding Yanbu’s downstream industrial complex — has been disrupted for the duration of the conversion.

The cost of the conversion extends beyond pipeline throughput. Saudi Arabia’s petrochemical industry — anchored by SABIC and Aramco’s downstream operations — depends on NGL feedstock delivered by pipeline to the western industrial complex at Yanbu. With the NGL line carrying crude, petrochemical plants that relied on pipeline-delivered feedstock have been forced to source by truck or rail — modes that cannot match pipeline volume — or curtail output. The conversion gained two million barrels per day of crude capacity while constraining a petrochemical sector that contributes billions in non-oil revenue, a trade-off that was designed to be temporary.

The original Petroline took two years to build in peacetime, with uncontested supply chains and no adversary targeting the construction corridor. Iran’s strikes since the conflict began have followed a specific pattern: pumping stations, loading terminals, and port approaches — the fixed nodes of the bypass — are the targets. Building new nodes under fire has no published timeline or cost estimate. No Saudi or Aramco official has announced plans for a second line.

The combined bypass capacity of both the Saudi Petroline and the UAE’s Habshan-Fujairah pipeline — which adds approximately 1.5 million barrels per day — reaches 3.5 to 5.5 million barrels per day, according to the IEA. Hormuz carried roughly twenty million barrels per day before the conflict. The two existing pipelines replace less than 28 percent of that volume.

The Quota That Does Not Exist

Saudi Arabia’s OPEC+ quota stands at 10.291 million barrels per day. Estimated actual production is approximately 7.25 million barrels per day — an involuntary shortfall of roughly three million barrels, larger than the combined output of Libya and Algeria. Saturday’s 41st OPEC+ ministerial, the first since the UAE’s departure, will approve a 188,000-barrel-per-day quota increase, according to The National.

The increase is arithmetically meaningless. Saudi Arabia is not producing below quota because it chose restraint. It is producing below quota because the pipeline connecting its eastern oil fields to Yanbu carries seven million barrels, the port loads three to four million, and no alternative export route exists while Hormuz remains closed. The OPEC+ compliance framework was designed to measure voluntary production discipline — countries choosing to pump less than they could. Saudi Arabia’s constraint is involuntary, imposed by infrastructure physics, and the framework has no mechanism for that distinction.

Kazakhstan presents the inverse problem. Tengiz field output, driven by Chevron’s $48.5 billion FGP completion, has pushed Kazakhstan 322,000 barrels per day above its quota — an overproduction that is structurally irreversible given the capital already deployed. Combined compliance debt across OPEC+ reaches 4.779 million barrels per day. The cartel that Saudi Arabia anchors cannot enforce discipline on its members and cannot physically deliver the production its largest member has been allocated.

The June 7 meeting will proceed under a procedural fiction. The 188,000-barrel-per-day increase — the seventh monthly increment under the gradual unwinding schedule agreed in late 2025 — was calculated on the assumption that member states could physically deliver their quotas. Saudi Arabia’s inability to export at quota levels means the increase adds capacity on paper and nowhere else. The communiqué will not mention the Petroline or Yanbu. OPEC+ has never acknowledged that its largest producer’s output is capped by infrastructure rather than policy.

The gap between OPEC+ quotas and physical capacity has widened every month since Hormuz closed. Saturday’s communiqué will affirm a production schedule. The schedule assumes export infrastructure that the Petroline and Yanbu cannot provide at the volumes the schedule describes.

What Does the June 9 Dividend Reveal?

Aramco’s declared Q1 2026 dividend of $21.89 billion exceeds its free cash flow of $18.6 billion — a coverage ratio of 0.85 times. The dividend is payable June 9, the same day Iran is expected to formally reject the Trump MOU proposal. Both events arrive forty-eight hours after OPEC+ approves a quota Saudi Arabia cannot fill.

The $3.29 billion shortfall means Aramco is paying shareholders more than it generated in cash. The gap draws on reserves or debt at a moment when the kingdom’s fiscal breakeven oil price — $108 to $111 per barrel, according to IMF and Goldman Sachs estimates — sits $11 to $14 above Brent crude’s June 4 level of approximately $96.97. Goldman estimates roughly $14 per barrel of war premium embedded in current Brent pricing. Remove that premium — the scenario Wood Mackenzie models as “Quick Peace,” with Brent settling near $80 per barrel — and the fiscal position worsens from the opposite direction.

The pipeline ceiling connects directly to the revenue shortfall. Saudi Arabia’s pre-war oil export model assumed full Hormuz access — roughly 7.5 million barrels per day of crude exports, predominantly through Ras Tanura and Ju’aymah terminals on the Gulf coast. With Hormuz closed, the entire export burden falls on a pipeline and port system that can deliver less than half the pre-war volume. Revenue has fallen not because the price of oil collapsed — Brent sits at $96.97, above the pre-war average — but because the barrels Saudi Arabia can physically ship have been cut by more than half.

The arithmetic of Saudi Arabia’s war-peace revenue trap has not changed: war keeps Brent elevated but constrains exports through the pipeline ceiling; peace restores export volume but collapses the price below breakeven. Saudi Arabia’s Q1 2026 fiscal deficit reached SAR 125.7 billion — 76 percent of the full-year budget target consumed in a single quarter, according to Ministry of Finance data. Military spending in Q1 rose 26 percent year-on-year to SAR 64.7 billion.

The kingdom is simultaneously paying for the war and paying a dividend it cannot cover from cash flow, while the infrastructure generating its revenue operates at a ceiling with no expansion path. Aramco’s Q1 adjusted net income rose 26 percent to $33.6 billion — a number that reflects global price increases, not Saudi export volumes.

On June 9, Iran is expected to formally reject Washington’s MOU — a harder position than Tasnim’s June 1 suspension announcement. The Phase 1 framework requires Hormuz to open before sanctions relief, a sequencing Iran has refused. The IMF’s June 3 Article IV assessment conditioned Saudi recovery on Hormuz normalizing. The Petroline reached its engineering ceiling nearly three months before the IMF published that condition.

Can Iran Disable the Bypass?

Iran has already demonstrated the capability. A drone attack struck a Petroline pumping station in March 2026, temporarily reducing throughput by approximately 700,000 barrels per day, according to Bloomberg. A separate missile was intercepted over Yanbu port. Saudi Arabia confirmed the pipeline had been restored to full capacity on April 12 — a restoration that took approximately two weeks.

BloombergNEF assessed that Iran’s targeting of Yanbu represents a deliberate second-phase strategy: having closed Hormuz, the IRGC is applying pressure to the alternative export route, creating what analysts describe as a dual-chokepoint architecture. Iran’s earlier strike on Camp Arifjan demonstrated the same operational logic — targeting logistics and sustainment infrastructure rather than frontline military positions. ENR noted that Iran’s strikes “map precisely onto the Gulf’s bypass infrastructure — it moved immediately against the exit ramps.”

At full seven-million-barrel throughput, the pipeline system has no operational margin. The April disruption demonstrated what a single pumping station strike does to a system running at capacity: not a marginal reduction but a 10 percent throughput loss cascading across the full length of the line. A sustained campaign against multiple pumping stations — spread across 1,201 kilometers of exposed desert corridor — would impose compounding losses that maintenance crews could not repair faster than the strikes accumulate.

The timeline of Iran’s infrastructure targeting follows the logic of the bypass itself. IRGC strikes first closed Hormuz — eliminating Saudi Arabia’s Gulf coast export terminals at Ras Tanura, Ju’aymah, and the King Fahd Industrial Port from service. When Saudi Arabia rerouted exports through the Petroline to Yanbu, Iran struck the pipeline’s pumping infrastructure. The April attack demonstrated that the bypass is targetable. Each escalation addresses the response to the previous one.

The second vulnerability sits at the pipeline’s economic exit. Yanbu exports transit the Red Sea and pass through the Bab al-Mandab strait to reach most global customers. The Bab al-Mandab closure threat would shut the exit for crude that has already bypassed Hormuz. Houthi Deputy Foreign Minister Hussein al-Ezzi has been explicit.

“If Sana’a decides to close the Bab al-Mandab, then all of mankind and jinn will be utterly powerless to open it.”Hussein al-Ezzi, Houthi Deputy Foreign Minister

Iranian state media — IRNA, PressTV, Tasnim — have not explicitly invoked the pipeline ceiling in the MOU negotiations. The IRGC has communicated through targeting instead: a pumping station on the Petroline, a missile aimed at Yanbu port, and — through the Houthis — a stated willingness to close the Red Sea exit. The pipeline delivers crude to a port that loads it onto tankers that transit a strait controlled by Iran’s closest ally. Iran or its proxies have struck or threatened every link in that chain.

Sized for a Short Disruption

The Petroline served its original strategic purpose during Iraq’s invasion of Kuwait in 1990. Saudi crude flowed to Yanbu while the northern Gulf was contested. That disruption lasted months, not years, and Hormuz remained open throughout. The pipeline provided redundancy — a backup to the primary Gulf export terminals — not the kingdom’s sole export artery.

The Gulf War precedent is instructive for what it does not share with the current conflict. In 1990-91, Saudi Arabia’s Gulf coast terminals at Ras Tanura and Ju’aymah continued operating. The Petroline supplemented a functioning export system. Iraq’s military occupation of Kuwait was a territorial conflict with a discrete, achievable military objective — liberation — and a coalition willing to fight for it. The current Hormuz closure has no comparable exit criteria. Iran’s stated conditions for reopening the strait include recognition of Iranian sovereignty claims and a transit toll structure that Saudi Arabia and Washington have not agreed to negotiate. The coalition that liberated Kuwait in 1991 could restore the prior order by force. No comparable military pathway to reopen Hormuz has been proposed without risking the Gulf oil infrastructure the reopening would aim to protect.

The 2019 Abqaiq-Khurais strikes prompted a different engineering posture. Aramco prepared the NGL pipeline for rapid conversion to crude service — an emergency measure designed for a scenario that might close Hormuz for weeks while the international community organized a military or diplomatic response. Engineering News-Record’s structural assessment captured the gap between design intent and operational reality: the bypass infrastructure “was sized for a short disruption. This is not that.”

Pankaj Srivastava, Senior Vice President at Rystad Energy, described the downstream consequence of prolonged operation at the ceiling: “With crude supply increasingly stranded in the Gulf, refiners may soon be forced to adjust operations, curtailing runs as product exports stall and directing output solely to domestic markets.” The domestic market cannot absorb what the export market cannot reach.

Wood Mackenzie’s assessment is blunter: a return to full Saudi production capacity depends on Hormuz reopening and infrastructure repair “which could take months or years, with supply backlog in critical site components.” A comparable expansion today, under active targeting, does not have a timeline. Hormuz remains closed. The Petroline has no higher gear.

Frequently Asked Questions

Could Saudi Arabia reverse the NGL conversion and restore gas export capacity?

Technically, yes — but not without surrendering two million barrels per day of crude throughput, reducing pipeline capacity from seven million to five million. The conversion requires swapping batching pigs and recalibrating pumping station pressure profiles. Industry standards estimate 72 to 96 hours for the physical reversal under normal conditions. Under current wartime operations, the trade-off is untenable: every barrel of crude throughput lost to NGL restoration reduces an already constrained export ceiling.

How does the UAE’s Habshan-Fujairah pipeline compare?

The Abu Dhabi Crude Oil Pipeline (ADCOP) runs 370 kilometers from Habshan to Fujairah on the Gulf of Oman, bypassing Hormuz entirely. Maximum capacity is approximately 1.5 million barrels per day. Fujairah’s structural advantage over Yanbu: the terminal exits directly to the Indian Ocean, making it immune to a Bab al-Mandab closure. Yanbu exports must transit the Red Sea and pass through the Bab al-Mandab to reach most global markets — a vulnerability Fujairah does not share.

What would it take to build a second Petroline?

The original Petroline cost approximately $2.5 billion in 1981 and was completed in two years of peacetime construction. A comparable project today would face decades of steel price inflation, upgraded safety standards requiring drone and missile resilience at every pumping station, and contested construction corridors within range of IRGC targeting. Engineering News-Record described the required program as “without precedent in the region’s infrastructure history.” As of June 2026, no construction authorization has been issued for additional pipeline capacity in the corridor.

Have tankers rerouted to other Saudi ports to avoid the Yanbu queue?

Saudi Arabia has no alternative Red Sea crude loading terminal. Ras Tanura, the kingdom’s largest export facility, sits on the Persian Gulf coast inside the Hormuz closure zone. Jeddah Islamic Port handles containers and general cargo but lacks crude loading infrastructure. King Abdullah Port at Rabigh serves commercial container traffic. The absence of a second Red Sea crude terminal reflects the pre-war assumption — shared across every Gulf state’s infrastructure planning — that Hormuz would remain open indefinitely.