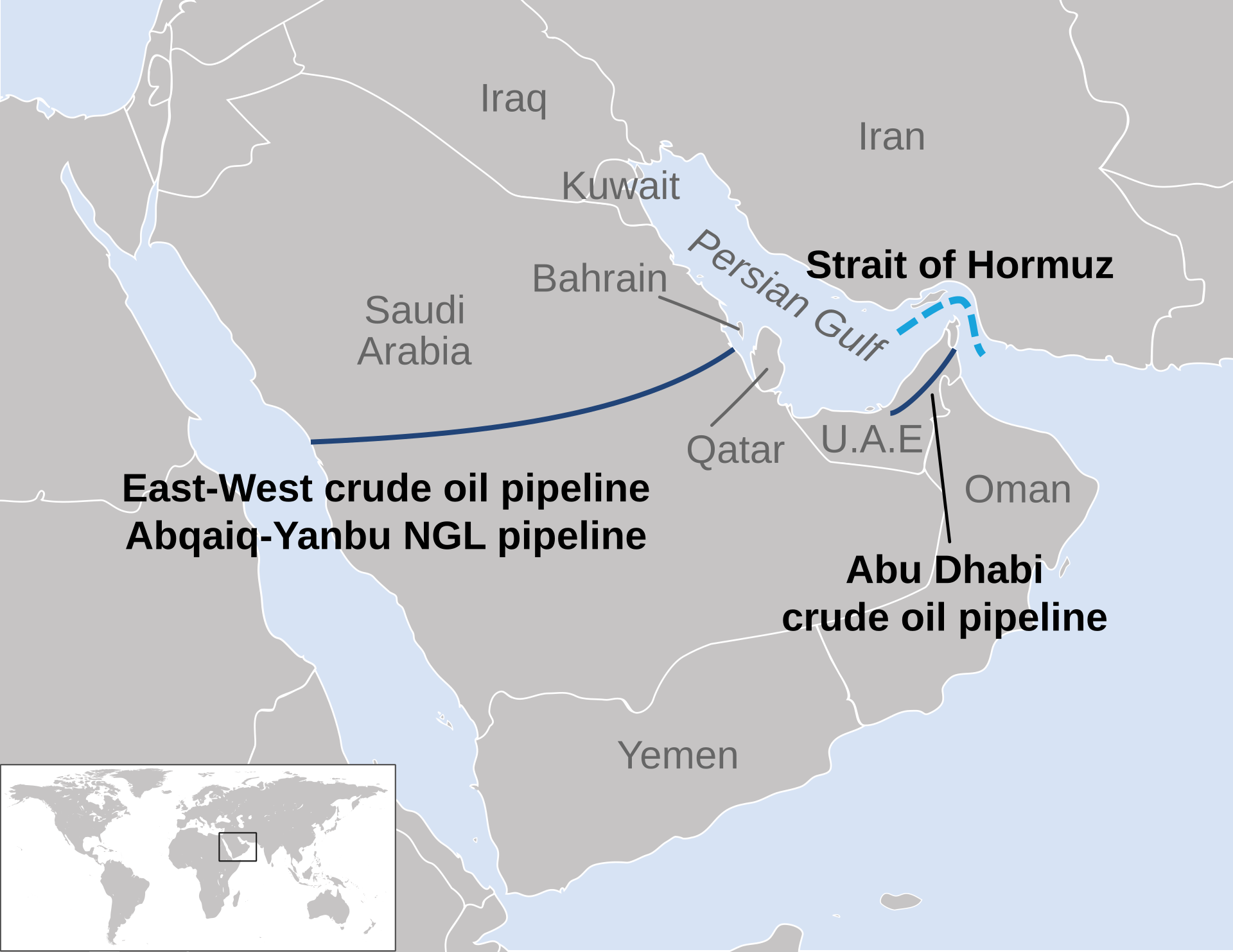

WASHINGTON — Iran and the United States are no longer negotiating the same Phase 1. On June 2, Secretary of State Marco Rubio told the Senate Foreign Relations Committee that Phase 1 of any agreement requires Iran to declare the Strait of Hormuz open, stop charging a toll on commercial vessels, assist in removing mines, and pledge not to fire on shipping. On the same day, Iranian negotiators in Doha pressed for $12 billion in frozen assets released immediately upon signing — before any Hormuz measures begin. Two days later, on June 4, Foreign Minister Abbas Araghchi told Al Mayadeen that “no tangible progress has been made in the negotiation process.” Hours earlier, Donald Trump told reporters that Hormuz would reopen “immediately upon signing” and that talks were going “very well.”

The contradiction is not rhetorical. It is structural. Rubio’s Phase 1 requires Iran to act before it receives anything. Iran’s Phase 1 requires Washington to pay before Tehran acts. Neither side has moved. The practical consequence for Saudi Arabia is that Hormuz — the chokepoint on which the IMF has now conditioned the Kingdom’s economic recovery — has no priceable reopening date. The June 9 convergence of Aramco’s $21.89 billion dividend obligation, Iran’s formal MOU rejection, and the expected Omani counteroffer arrives with zero agreed sequencing between the two parties that control the outcome. The sequencing inversion Iran proposed through Muscat — frozen-assets release before Hormuz reopening — confirmed on June 6 that no bridging framework exists. Aramco’s wartime fiscal arithmetic — including what the $21.89B dividend disbursement leaves in the balance sheet for Sadara Chemical’s .7B parent guarantee — is detailed in Aramco’s post-dividend cash position.

Table of Contents

- What Did Iran Demand as Phase 1?

- Rubio’s Phase 1: Hormuz First, Assets Later

- Why Can’t Washington and Tehran Agree on Sequencing?

- The $6 Billion Precedent Iran Already Rejected

- The JCPOA Model Iran Is Trying to Reverse

- What Does the June 9 Convergence Mean for Saudi Arabia?

- Saudi Arabia’s Fiscal Exposure to a Dispute It Cannot Influence

- Three Conditions Araghchi Set on June 4

- Congress Can Re-Freeze Anything the White House Releases

- Frequently Asked Questions

What Did Iran Demand as Phase 1?

Iranian negotiators led by Mohammad Bagher Ghalibaf demanded, during Doha talks, that $12 billion in frozen assets held in Qatar be released immediately upon signing any memorandum of understanding. A second tranche of $12 billion would follow within 60 days, bringing the total to $24 billion. The demand was first reported by The National on May 26 and confirmed by Iran International.

Iran did not frame this as a concession or a negotiating position to be traded. It framed asset release as a precondition — what Tehran calls “Phase A.” Hormuz measures, mine clearance, and toll suspension would come only after Iran had verified liquid access to the funds. Qatar-based mediators proposed a restricted humanitarian fund of several billion dollars as a compromise. Iran rejected it, insisting on unrestricted liquid access. PressTV reported on May 28 that Tehran demanded “unconditional” release of all frozen assets.

The semi-official Fars Agency reported on May 30 that the $12 billion figure was already embedded in the MOU draft text. From Iran’s perspective, the number is not a demand — it is a term both sides have already discussed, and Washington is now attempting to resequence what was provisionally agreed.

Ali Bagheri Kani, Deputy Secretary of Iran’s Supreme National Security Council, stated the position in institutional terms: “We are seeking the release of all Iranian assets frozen by the United States, and this is the legal right of the Iranian nation.” Iran’s total claim on globally frozen assets exceeds $100 billion, per Iranian government statements reported by PressTV. The $24 billion demand covers only the portion Tehran considers immediately recoverable.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Rubio’s Phase 1: Hormuz First, Assets Later

Rubio’s testimony to the Senate Foreign Relations Committee on June 2 described a two-phase structure in which Iran acts before it receives. Phase 1 requires four specific steps: Iran must declare the Strait of Hormuz open, cease charging the Persian Gulf Security Arrangement toll on commercial vessels, assist in the removal of sea mines, and formally pledge not to fire on commercial shipping. Rubio called this “the predicate that opens the door to Phase 2.”

Phase 2 is where sanctions relief lives. It requires, in Rubio’s words, “severe and long-term limitations and/or cancellation of enrichment activity” and “a team of experts to meet over a 30, 60, 90-day period” to negotiate terms. The Foundation for Defense of Democracies confirmed the architecture: frozen assets are “back-ended to when they turn over enriched uranium” in Phase 2. The question, an FDD analyst noted, is “not if these funds become available, but when.”

Under this framework, Iran opens Hormuz for free. No assets at signing. No restricted funds at signing. Iran gets nothing in Phase 1 except the promise that Phase 2 will begin. Phase 2 then requires Iran to make nuclear concessions — enrichment limits, HEU handover, inspection access — before any frozen assets move. The entire incentive structure depends on Iran trusting that Washington will deliver Phase 2 after Iran has already dismantled its primary enforcement instrument.

Iran’s response to this architecture was operational before it was verbal. Euronews reported on May 25 that Iran’s foreign minister and central bank chief arrived in Qatar simultaneously — the demand was being operationalized financially, not merely stated diplomatically. The parallel presence of the central bank governor signaled that Tehran was treating the asset question as a banking transaction to be executed at signing, not as a diplomatic promise to be honored later. Rubio’s Phase 1 asks Iran to dismantle its Hormuz enforcement apparatus on the strength of a future negotiation. Iran’s negotiators arrived in Doha with their banker.

Why Can’t Washington and Tehran Agree on Sequencing?

The gap is not over the components of a deal. Both sides acknowledge that Hormuz reopening, frozen asset release, and nuclear talks will be part of any agreement. The gap is over the order. Iran demands: pay, then we open. Washington demands: open, then we discuss payment. Each side’s Phase 1 is the other side’s Phase 2.

This is not a negotiating tactic that splits the difference. Sequencing in arms control and sanctions diplomacy is the deal. The party that acts first accepts the risk that the other side will pocket the concession and stall. Iran’s experience with the 2023 prisoner-swap funds — $6 billion transferred to Qatar, then re-frozen after October 7 — reinforces Tehran’s position that acting first without guaranteed payment is a structural trap. Washington’s experience with JCPOA verification timelines — where Iran received sanctions relief only after IAEA certification — reinforces its position that payment without verified action produces no compliance.

Tasnim, the IRGC-affiliated outlet, published Iran’s stated Phase 1 framework: end the war within 30 days, lift the US naval blockade, release frozen assets, remove sanctions, and establish a new Hormuz governance mechanism. Nuclear talks are deferred entirely. “At this stage,” a Tasnim summary stated, “we do not have nuclear negotiations.” Iran’s Phase 1 contains five items. Rubio’s Phase 1 contains four. They share zero elements.

The $6 Billion Precedent Iran Already Rejected

In September 2023, $6 billion in Iranian funds held in South Korea were transferred through European intermediary banks to restricted accounts in Qatar as part of a prisoner exchange. The funds were limited to humanitarian purchases — food, medicine, and medical equipment. Iran had no direct access. The Qatari central bank administered disbursements under US oversight.

After the October 7 Hamas attack, Congress pressured the Biden administration to re-freeze the accounts. The funds were frozen again, and Iran received none of the $6 billion. The episode demonstrated three things relevant to the current sequencing dispute. First, restricted accounts are the US baseline for any asset release — Washington will not transfer unrestricted liquid funds. Second, Iran views restricted accounts as functionally equivalent to continued seizure, not as a concession. Third, Congress can re-freeze assets regardless of executive branch waivers, because Iran sanctions rest on multiple overlapping congressional authorities, not solely on executive orders.

Iran’s current demand for “unconditional” release of $12 billion in liquid form is a direct response to the 2023 model. Tehran is not negotiating access to humanitarian accounts. It is negotiating sovereign control over its own funds — a framing that separates the two sides on principle before they reach any technical discussion of timelines or verification.

The JCPOA Model Iran Is Trying to Reverse

The 2015 Joint Comprehensive Plan of Action established a sequencing precedent that lasted through Implementation Day on January 16, 2016. Under the JCPOA, Iran first took all required nuclear steps — reducing centrifuge numbers, shipping out enriched uranium stockpile, redesigning the Arak reactor, granting IAEA expanded access. Only after the IAEA certified compliance did sanctions lift and frozen assets become accessible. Iran acted. The world verified. Then Iran was paid.

Iran’s current demand inverts this entirely. Tehran wants payment at signing — before any action, before any verification, before any Hormuz measure. The JCPOA required approximately six months between the agreement (July 14, 2015) and Implementation Day (January 16, 2016) for Iran to complete its nuclear steps. Iran’s current proposal compresses that to zero: assets upon signature.

The inversion reflects Iran’s institutional memory of what happened after the JCPOA. Tehran complied, received sanctions relief, and then watched the United States withdraw from the agreement in May 2018 under Trump’s first term. Iran’s negotiating position in 2026 is shaped by the conclusion that sequencing in which Iran acts first and gets paid later is a mechanism for extraction without reciprocity. Whether that conclusion is fair is beside the point. It is the operating assumption behind Iran’s $12 billion demand, and no US counterargument has moved it.

The nuclear dimension makes the inversion harder to reverse. The IAEA has been in a 93-day reporting blackout on Iran’s enrichment activities. Iran holds 440.9 kilograms of unverified highly enriched uranium — enough, by most estimates, for multiple weapons. Under the JCPOA, Iran’s nuclear concessions were verified before assets moved. Under Iran’s current proposal, assets move before any nuclear verification occurs, and nuclear talks are explicitly deferred to a later phase that has no agreed start date. The Arms Control Association described the broader Saudi-US 123 Agreement as a “gilded sweetheart deal” that lacks the Gold Standard safeguards — a critique Iran has not yet deployed in MOU negotiations but that sits available as an argument against any sequencing that treats US nonproliferation commitments as credible.

What Does the June 9 Convergence Mean for Saudi Arabia?

Three events converge on June 9. Aramco’s $21.89 billion quarterly dividend is payable — against Q1 free cash flow of $18.6 billion, a coverage ratio of 0.85x. Iran is expected to formally reject the MOU through the Omani channel, accompanied by a counteroffer whose terms remain unknown. And the five-day window since Trump’s amended MOU text was sent to Mojtaba Khamenei’s courier network expires, with eight of ten Khamenei conditions already violated by the unamended draft.

For Saudi Arabia, the June 9 date concentrates fiscal and diplomatic exposure into a single day. The Kingdom must fund a dividend that exceeds its operating cash flow while the only mechanism that could reopen Hormuz — the US-Iran MOU — faces formal rejection with no agreed sequencing for a replacement. The private Saudi de-escalation track with Iran remains the only channel not formally suspended, but it has produced no public outcome since FM Faisal bin Farhan’s last Iran call on May 6.

Saudi Arabia has issued no statement on the MOU, its suspension, the frozen asset dispute, or Phase 1 sequencing. The Ministry of Foreign Affairs has been publicly silent for more than ten days as of June 4. Saudi Arabia is not at the table for any of the three Hormuz tracks: the US-Iran direct channel, the Oman mediation, or the UK-France maritime coalition coordinated through Northwood. The Kingdom’s fiscal survival depends on an outcome it cannot influence and a timeline it cannot model. Washington’s attempt to repurpose Iran’s Phase 1 demand as Gulf reconstruction reparations added a second claimant to the same asset pool — without consulting Riyadh, which holds no seat in the dispute and no claim on the money at its center.

Treasury Plans to Seize Iranian Assets to Pay Gulf Allies for War Damage details the legal authorities Bessent invoked, the jurisdictions where Iranian assets are held, and why the $24 billion Tehran designated as its peace precondition cannot be redirected to Gulf reconstruction without congressional authorization that does not yet exist.

Saudi Arabia’s Fiscal Exposure to a Dispute It Cannot Influence

Saudi Arabia’s breakeven oil price stands at $108–111 per barrel, according to IMF and Goldman Sachs estimates. Brent traded at $96.97 on June 4 — an $11–14 gap. Goldman Sachs estimates that approximately $14 per barrel of the current Brent price is war premium. If Phase 1 succeeded and Hormuz reopened, that premium would collapse, pushing Brent below $95 and widening the Saudi breakeven gap further. This is the structure that the IMF identified on June 3 when it made Saudi Arabia’s recovery “contingent on Hormuz normalising” — the first Article IV chokepoint conditionality for any Gulf state.

| Metric | Figure | Source |

|---|---|---|

| Brent (June 4) | $96.97/bbl | Market data |

| Saudi breakeven | $108–111/bbl | IMF / Goldman Sachs |

| War premium embedded | ~$14/bbl | Goldman Sachs |

| Q1 2026 deficit | SAR 125.7B | Saudi MOF |

| Full-year 2026 target deficit | SAR 165B | Saudi MOF |

| Q1 deficit as % of full-year | 76% | Calculated |

| Aramco dividend (Q2, payable June 9) | $21.89B | Aramco |

| Q1 free cash flow | $18.6B | Aramco |

| Dividend coverage ratio | 0.85x | Calculated |

| PIF cash reserves | $15B | PIF disclosure (six-year low) |

| NDMC borrowing capacity used | ~90% | Estimated |

Saudi Arabia has consumed three-quarters of its annual deficit allowance in a single quarter, drawn its sovereign wealth fund to a six-year low, and exhausted most of its statutory borrowing room — all before any resolution of the dispute that is the primary cause of the revenue shortfall. The Kingdom entered the sequencing dispute with no fiscal buffer and no diplomatic access to the talks that will determine whether one can be rebuilt.

The sequencing inversion compounds the problem. Under Rubio’s framework, Hormuz could theoretically reopen within 30 days of signing. Under Iran’s framework, Hormuz reopening is deferred until after $24 billion in asset releases are verified and a new governance mechanism is established — a timeline measured in months, not weeks. Every additional month of Hormuz closure at current Brent prices costs Saudi Arabia approximately $80–100 million per day in foregone revenue against breakeven — roughly $2.4–3 billion per month at current production and price levels. Meanwhile, the June 7 OPEC+ decision to add 188,000 b/d deepens the trap: a pre-committed supply increase Saudi Arabia cannot produce, arriving at a Brent price it cannot afford.

Three Conditions Araghchi Set on June 4

Araghchi’s June 4 appearance on Al Mayadeen introduced three conditions for returning to talks, expanding the sequencing dispute beyond Hormuz and frozen assets. The conditions were: respect for the rights of the Iranian people, meaning asset releases; ending the war in Lebanon; and stopping regional tensions. CBS News and Naharnet carried the full statement.

Communications with the Americans have not been cut off, and messages have been exchanged regarding the need to stop aggression against Beirut, but no tangible progress has been made in the negotiation process.

Abbas Araghchi, Iranian Foreign Minister, June 4 (Al Mayadeen)

The Lebanon condition is not new to Iran’s negotiating framework. It appeared in Iran’s March 2026 five-point counter-proposal, in the April Pakistan-brokered ceasefire effort, and in the late-May MOU draft. But Araghchi’s public reassertion on June 4 came hours after the US-Israel-Lebanon trilateral ceasefire was announced — a ceasefire in which Hezbollah was named as a condition, not a party, and which contained no IDF withdrawal timeline. Araghchi’s “violation on all fronts including Lebanon” formulation, first stated June 1, remained operative.

The addition of Lebanon as a return condition means the sequencing dispute is no longer bilateral. Iran’s Phase 1 now requires the US to resolve a separate conflict — one involving Israel, Lebanon, Hezbollah, and France — before Hormuz talks resume. For Saudi Arabia, which was excluded from the June 22 Washington follow-on and whose envoy Yazid bin Farhan was told by Aoun not to meet Netanyahu in April, the Lebanon linkage adds a second uncontrollable variable to an already unmodelable timeline.

FM Faisal bin Farhan’s last public statement on Hormuz, issued May 20, called for restoration of the pre-war status quo — a position that is diplomatically incoherent after more than 90 days of PGSA toll collection, a US naval blockade, and mine-laying that Oman reported but did not attribute. Saudi Arabia’s MOFA silence since late May is not passivity. It is the absence of a position that survives contact with either side’s Phase 1. Endorsing Rubio’s framework means accepting that Iran opens Hormuz before any payment — a position Tehran has explicitly rejected. Endorsing Iran’s framework means accepting that $12 billion moves before Hormuz reopens — a position that extends the closure Saudi Arabia cannot afford. The Kingdom has no available public position because neither Phase 1 serves its interests.

Congress Can Re-Freeze Anything the White House Releases

Even if the executive branch agreed to Iran’s demand for $12 billion at signing, congressional authorities create an independent re-freeze mechanism. Iran sanctions are built on multiple overlapping legislative foundations — the Iran Sanctions Act, the Comprehensive Iran Sanctions, Accountability, and Divestment Act, and specific appropriations riders — not solely on executive orders that a president can waive unilaterally.

The 2023 precedent is unambiguous. The Biden administration authorized the $6 billion Qatar transfer under existing waiver authorities. After October 7, bipartisan congressional pressure forced the re-freeze within weeks. No legislation was required. The executive branch reversed its own waiver under political pressure that both parties generated.

Any significant asset release under the current MOU would require congressional notification under the Iran Nuclear Agreement Review Act’s provisions, giving Congress a window to block or condition the transfer. The structural consequence: even if Iran obtained a presidential commitment to release $12 billion at signing, Tehran would hold an instrument that Congress could void by the following news cycle. Iran’s negotiators are aware of this. Bagheri Kani’s demand for “unconditional” release is, in part, a demand for a mechanism that survives congressional reversal — a mechanism that does not exist under current US law.

| Position | US (Rubio, June 2) | Iran (Ghalibaf / Araghchi) |

|---|---|---|

| Phase 1 requirement | Iran opens Hormuz, clears mines, stops toll | US releases $12B frozen assets immediately |

| Phase 2 requirement | Nuclear limits; experts meet 30/60/90 days | Hormuz governance, nuclear talks deferred |

| When Iran gets assets | Phase 2, after HEU handover | Phase 1, upon signing |

| When Hormuz reopens | Phase 1, before any payment | After asset verification + governance framework |

| Lebanon linkage | Not mentioned in SFRC testimony | Explicit return condition (June 4) |

| JCPOA precedent invoked | Act-then-pay (Implementation Day 2016) | Act-then-betrayed (US withdrawal 2018) |

Iran frames Hormuz as a sovereignty question, not a concession. Five preconditions for strait normalization include formal recognition of Iranian sovereignty over the operating architecture of the waterway. The PGSA toll — approximately $2 million per VLCC per day — has been collected for more than 81 days, establishing a revenue precedent Tehran will not surrender without compensation it considers equivalent. From Iran’s vantage, Rubio named a price on June 2 that Iran never agreed to, then demanded Iran pay it in advance.

On June 8 — after 100 days of conflict — Iran confirmed all three of those preconditions remain in force: Hormuz stays closed, the MOU framework is “no longer feasible,” and the PGSA sovereign claim stands unmodified. Hormuz Stays Closed as Iran Halts Strikes, Declares Talks Dead reports the June 8 triple-track collapse and what Iran’s simultaneous positions mean for the sequencing dispute documented here.

Frequently Asked Questions

How much money does Iran want released before it will discuss opening Hormuz?

Iran’s lead negotiator Ghalibaf demanded $12 billion in immediate liquid access to funds held in Qatar upon signing the MOU, followed by a second $12 billion tranche within 60 days, totaling $24 billion. Iran specifically rejected a Qatar-mediated compromise that would have provided several billion dollars in a restricted humanitarian fund — Tehran insists on unrestricted sovereign access, not administered accounts. Iran’s total global frozen asset claim exceeds $100 billion, but the $24 billion covers what Tehran considers immediately recoverable through the current negotiation.

Has the United States ever released frozen Iranian assets before, and what happened?

Yes. In September 2023, $6 billion was transferred from South Korean banks through European intermediaries to restricted Qatari accounts as part of a prisoner exchange. The funds were limited to humanitarian purchases under US oversight — Iran had no direct access. After the October 7 Hamas attack, the accounts were re-frozen under bipartisan congressional pressure without requiring new legislation. Iran received none of the $6 billion. Separately, after the 2016 JCPOA Implementation Day, approximately $55 billion in previously frozen assets became accessible to Iran — though US officials at the time disputed the liquid portion, estimating Iran could access only $30–50 billion of the headline figure due to prior encumbrances and committed obligations.

Why can’t Saudi Arabia influence the sequencing negotiations?

Saudi Arabia is excluded from all three active Hormuz negotiation tracks: the US-Iran direct channel, the Omani mediation pathway, and the UK-France maritime coalition coordinated through Northwood HQ. The Kingdom’s last direct FM-to-FM contact with Iran was the May 6 Araghchi call. Saudi Arabia’s own envoy was told by Lebanese President Aoun not to meet with Netanyahu, removing a potential indirect channel through the Lebanon track that Araghchi made a return condition on June 4. The Saudi private de-escalation track with Iran — reportedly through intelligence rather than foreign ministry channels — has produced no publicly observable outcome since the May 6 call.

What is the PGSA toll and why does Iran treat it as established revenue?

The Persian Gulf Security Arrangement toll is approximately $2 million per VLCC per transit day, collected by Iran from commercial vessels passing through the Strait of Hormuz since late February 2026. Over 81-plus days of collection, the toll has generated an undisclosed but substantial revenue stream and, from Tehran’s perspective, established Iranian administrative authority over strait transit. Iran treats the toll not as an emergency wartime measure but as an exercise of sovereignty — one of its five preconditions for Hormuz normalization is formal recognition of Iranian sovereignty over the strait’s operating architecture, which would institutionalize the toll framework even after any MOU.

What happens if Iran formally rejects the MOU on June 9 as expected?

A formal rejection through the Omani channel would close the current negotiating text and require a new draft. The Omani counteroffer expected alongside the rejection is likely to reflect Iran’s asset-first sequencing — placing $12 billion release as a precondition rather than a Phase 2 reward. Simultaneously, Aramco’s $21.89 billion dividend falls due the same day against $18.6 billion in Q1 free cash flow, meaning Saudi Arabia would absorb the formal collapse of the MOU on the same day it funds a dividend it cannot cover from operations. The convergence eliminates any remaining ambiguity about whether Saudi fiscal planning can assume a near-term Hormuz reopening.

The IEEPA mechanism that Bessent would use to vest those assets is the same instrument Iran cites as foreclosing the Algiers precedent — the legal collision is traced in Twenty-Four Billion Dollars Cannot Move in Two Directions, which shows why the $24 billion cannot simultaneously fund Gulf reconstruction and serve as Tehran’s Hormuz reopening price.