NEOM — DataVolt committed $5 billion to Oxagon in February 2025, when the Strait of Hormuz was carrying ninety-five tanker transits a day and a Red Sea industrial port looked like the least necessary thing Saudi Arabia could build. Twelve months later, Hormuz carries approximately 3.6 per cent of its pre-war commercial traffic, NEOM has cancelled more than $8.45 billion in contracts elsewhere, and Oxagon — the unglamorous, logistics-first zone that never featured in the drone footage — is the only part of the megaproject whose commercial thesis the war has strengthened rather than destroyed.

The paradox is structural, and nobody in Riyadh appears to have resolved it. Saudi diplomacy is actively working to reopen Hormuz, which would weaken Oxagon’s urgency as a bypass corridor, while private capital is simultaneously committing billions on the premise that the strait’s contestation — or the insurance memory it leaves behind — makes Red Sea infrastructure permanently valuable. The kingdom wants two contradictory outcomes and cannot control the geopolitical condition that determines which one it gets.

Table of Contents

- The Port Nobody Needed

- What Did Hormuz Closure Actually Do to the Bypass Argument?

- Five Billion Dollars Before the First Missile

- How Far Along Is the Port of NEOM?

- Why Does the Data Centre Thesis Survive If Hormuz Reopens?

- Can Oxagon Work Without the Rail Link?

- The Paradox Saudi Arabia Cannot Solve

- Does Private Capital Actually Believe in Oxagon?

- Frequently Asked Questions

The Port Nobody Needed

Before the IRGC closed Hormuz on February 28, 2026, Oxagon’s commercial case rested on a bet that most energy analysts treated as a hedge against a scenario nobody expected to materialise. The pitch was straightforward — a Red Sea industrial zone with deepwater port access, positioned to bypass the Strait of Hormuz for Saudi exports to Europe and Africa — but the logic required a chokepoint disruption that hadn’t occurred since the Tanker War of the 1980s, when the geography of Gulf shipping was simpler and the volumes were a fraction of what they became. Hormuz was carrying roughly twenty-one million barrels per day of crude and condensate plus fifteen per cent of global LNG trade, and there was no active threat credible enough to close it.

The critique of Oxagon was never stated explicitly — nobody published a report calling it redundant — but the commercial arithmetic said it plainly enough. Saudi Arabia already had the East-West Pipeline with a nominal capacity of five million barrels per day, Yanbu and Jeddah were operational Red Sea ports, and NEOM’s ambitious container capacity targets looked extravagant for a zone with no hinterland, no rail link, and no anchor tenant large enough to justify the infrastructure at that scale. The money going into Oxagon — roughly $9.3 billion in construction contracts, according to Global Construction Review and BlackRidge Research — was second only to The Line, which consumed the bulk of NEOM’s ambition and nearly all of its public attention.

Oxagon’s defenders pointed to the data-centre thesis: the zone’s access to submarine cables, abundant solar and wind resources, and empty land made it a natural destination for hyperscale AI infrastructure regardless of what happened in the strait. DataVolt’s $5 billion agreement, announced in February 2025 and confirmed by Data Center Dynamics, MEED, and four other publications, was the clearest expression of that logic — a 1.5-gigawatt campus whose commercial viability depended on power and connectivity, not on tanker traffic. But the logistics-bypass argument, the one that made Oxagon specifically valuable compared to any other site in Saudi Arabia, required a Hormuz problem that did not yet exist — and when one arrived on February 28, 2026, it arrived with enough force to shut the strait almost entirely.

What Did Hormuz Closure Actually Do to the Bypass Argument?

It made the argument self-evident. Since April 8, 2026, approximately forty-five commercial vessels have transited Hormuz — against a pre-war baseline of roughly ninety-five per day — and the European Council on Foreign Relations, in a May 24 report, estimated that the Iran war has handed global business a bill exceeding $25 billion, “much of it traceable to a single chokepoint.” Iran’s PGSA toll system, rebranded as “navigational services” and designated under OFAC sanctions on May 28, charges $2 million per transit for non-exempt vessels payable in yuan or bitcoin, creating a commercial floor beneath which Hormuz passage is no longer economically rational for a growing share of global shipping.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The consequence for Saudi Arabia is particularly concentrated. Petroline can push five million barrels per day to Yanbu, but Saudi production runs at 7.76 million, leaving roughly 2.5 million barrels per day structurally dependent on a strait that now functions as an Iranian toll road under American sanctions. Aramco has redirected the bulk of its Asian exports through the pipeline — India’s share of Saudi crude arriving via Hormuz collapsed from 89 per cent to 11 per cent between March and late April — but the volumes that cannot fit through the pipeline remain exposed to a chokepoint that has been priced, sanctioned, and intermittently fired upon.

Strategy&, the PwC consultancy, published a report framing Hormuz closure as “a structural shock to global trade and a turning point for the Gulf states,” explicitly naming NEOM and Yanbu as “key gateways” for the integrated sea-land corridors it recommended. The ECFR went further, arguing that the India-Middle East-Europe Economic Corridor — conceived for peacetime conditions — “now looks ill-suited to an environment in which maritime chokepoints are routinely weaponised.” Both reports treat Oxagon’s bypass function not as speculative but as a named prescription in post-crisis trade architecture, the kind of institutional endorsement that moves capital allocation committees — and the P&I club exclusions, the war-risk premiums running at eight times pre-war levels, and the force majeure clauses that have turned Hormuz into an invisible blockade are creating what insurers call “memory,” the permanent repricing of risk that persists long after the immediate crisis ends.

Five Billion Dollars Before the First Missile

DataVolt’s agreement with NEOM, announced on February 10, 2025, predated the Iran war by twelve and a half months. The company committed to building a 1.5-gigawatt data-centre campus at Oxagon — the largest single private investment in any NEOM zone — with a first phase of 300 megawatts targeted for 2028. DataVolt is a wholly owned subsidiary of Vision Invest, a Saudi development and investment holding company backed by the Al Muhaidib Group, and its team claims experience developing and operating over twenty gigawatts of renewable energy assets across nine countries. The commitment was Saudi private capital deploying at scale into Saudi state infrastructure, which carries a different risk calculus and a different set of incentives than a genuinely arm’s-length bet from a foreign fund testing the regulatory environment.

The scale expanded considerably in May 2025, when DataVolt signed a $20 billion multi-year agreement with Supermicro for ultra-dense GPU platforms and rack-scale liquid cooling systems designed for hyperscale AI workloads. Data Center Dynamics and Inside HPC reported the deal as one of the largest single hardware commitments in the global data-centre industry, extending Oxagon’s supply chain well beyond the original $5 billion campus investment and locking in a hardware ecosystem before the campus had broken ground — a capital commitment pattern more typical of hyperscale operators like Equinix or Digital Realty than of a megaproject zone that most investors still associated with The Line’s architectural renders.

What makes the DataVolt commitment analytically distinct from the broader NEOM contraction — billions in terminated contracts, including the Connector HSR that would have linked Oxagon to The Line — is that the data-centre thesis does not require Hormuz to remain closed. Data centres need submarine cable access, cheap power, and land, all of which Oxagon provides independently of what happens in the strait, which means DataVolt’s bet survives every scenario: it becomes substantially more valuable in the one where the strait stays contested, and the physical infrastructure backing that bet is further along than the NEOM contraction headlines suggest.

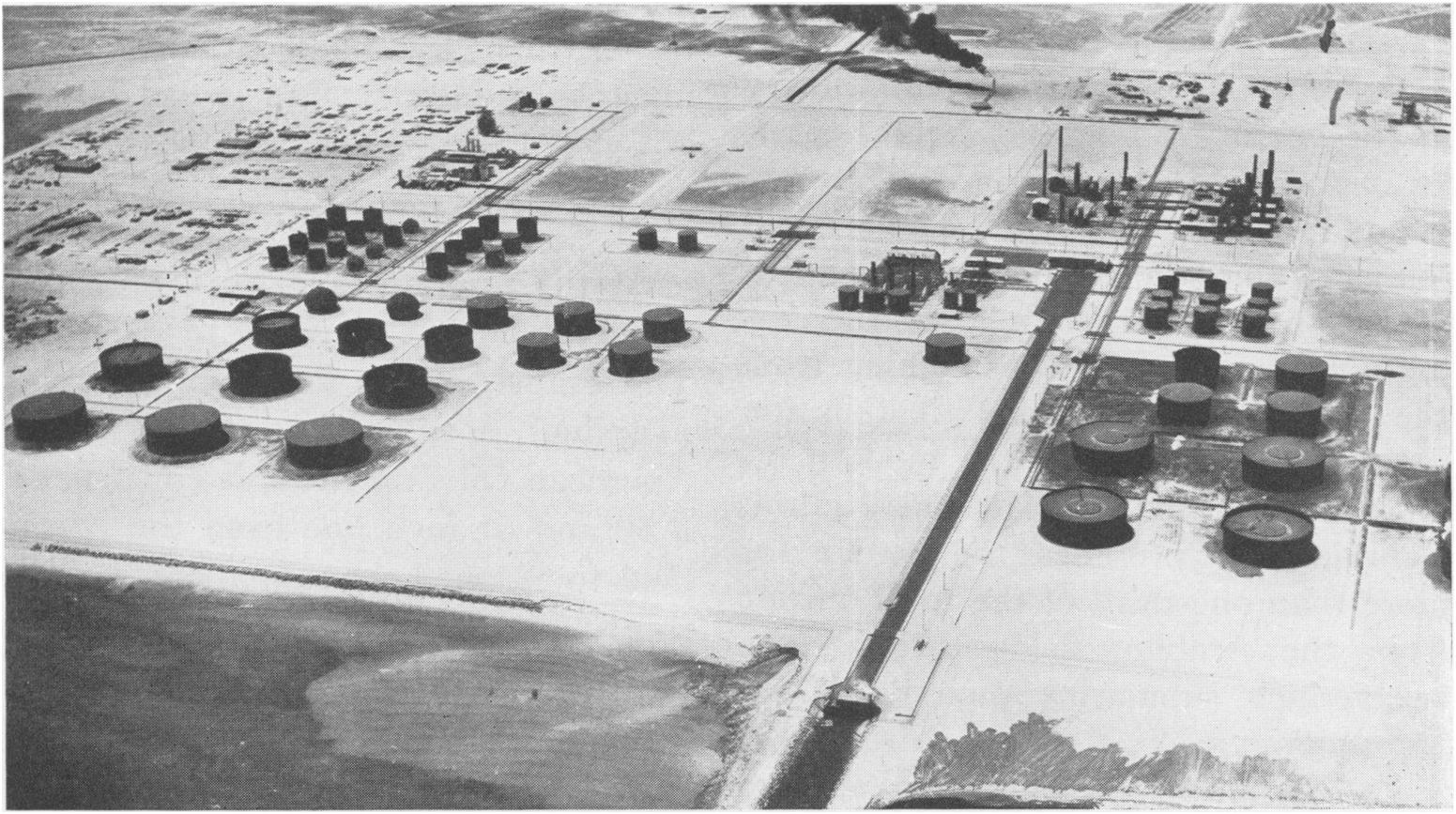

How Far Along Is the Port of NEOM?

Further than most NEOM critics assume. The port is 68 per cent complete, according to Newsweek, with BESIX, MBL, and Boskalis having delivered 4.6 kilometres of quay wall and seven berths at depths between 10.5 and 18.5 metres. The container terminal — 900 metres long with automated cranes already installed — is targeting 1.5 million TEUs per year in capacity, a volume that Oxagon CEO Vishal Wanchoo told AGBI in November 2025 represents the “best option for Iraqi shipping,” capable of cutting transit times to Iraq by up to twelve days.

PIF has committed an estimated $3 billion to port infrastructure specifically, according to Construction Week Online — state investment that sits alongside DataVolt’s private $5 billion and the broader Oxagon contract portfolio. Boskalis completed the Oxagon port expansion in March 2026, weeks after the war began, and DEME/Archirodon won the next-phase Duba port expansion contract valued at approximately $1 billion. PIF chose to keep building the port while cancelling the high-speed rail that would have connected it to The Line, which tells you where the fund’s remaining confidence sits within a portfolio whose liquid cash has fallen to $15 billion — a six-year low representing 1.6 per cent of assets under management.

The most tangible proof that Oxagon has crossed from construction site to functioning logistics node came on April 14, 2026, when NEOM launched a multimodal corridor linking Trieste, Italy, to the Port of NEOM via Damietta and Safaga in Egypt. Pan Marine operates the route with the RoPax vessel Pan Lily — 130 trucks and 100 cars per voyage, four weekly sailings from Safaga — in partnership with DFDS, and importers from Italy, the UK, Germany, and Poland are already using it, having cut Egypt-to-NEOM transit time by more than half. The volumes are small relative to the port’s capacity targets, but the operational fact is not: cargo is moving through Oxagon while The Line remains a 2.4-kilometre trench in the desert, 1.4 per cent of its planned 170-kilometre length, and the question of whether the port’s commercial thesis depends on the war or merely benefits from it is the question that separates Oxagon’s two investment arguments from each other.

| Metric | Figure | Source |

|---|---|---|

| DataVolt campus investment | $5B | NEOM.com, Feb 2025 |

| Campus capacity target | 1.5GW | Data Center Dynamics |

| First phase / online date | 300MW / 2028 | Intelligent CIO ME |

| DataVolt–Supermicro hardware deal | $20B (multi-year) | DCD / MEED, May 2025 |

| PIF port infrastructure | ~$3B | Construction Week Online |

| Total Oxagon contracts awarded | $9.3B | Global Construction Review |

| Port completion | 68% | Newsweek |

| Quay wall / berths | 4.6 km / 7 (10.5–18.5m) | BESIX |

| Container terminal / capacity | 900m / 1.5M TEU target | Port of NEOM / AGBI |

| Next-phase port contract (DEME) | ~$1B | AGBI, Aug 2025 |

| Multimodal corridor launch | April 14, 2026 | NEOM newsroom |

| Iraq transit time saving | Up to 12 days | Wanchoo / AGBI |

| Saudi Hormuz-dependent exports | 2.5M bpd | Situation analysis |

| Hormuz transits since April 8 | ~45 (vs ~95/day pre-war) | Situation analysis |

“We don’t really see obstacles beyond that because we control our own destiny.”

— Vishal Wanchoo, Oxagon CEO, AGBI, November 2025

Why Does the Data Centre Thesis Survive If Hormuz Reopens?

Data centres need submarine cable access, cheap renewable power, and land — all of which Oxagon provides independently of Hormuz, and none of which change if a ceasefire holds, a deal is signed, or Iran dismantles the PGSA tomorrow. DataVolt’s 1.5-gigawatt campus and the $20 billion Supermicro hardware deal that supports it are anchored to a geography that sits on the Red Sea coast with fibre access to Europe, Africa, and South Asia, combined with solar and wind resources that Saudi Arabia’s western desert provides in abundance. The logistics bypass is Hormuz-contingent; the data-centre campus is not, and that distinction is what makes Oxagon structurally different from every other NEOM component.

The distinction matters because Oxagon now carries two commercial theses in one site, tied to the same geopolitical variable but responding to it in opposite ways. If Hormuz reopens fully, the logistics bypass weakens — fewer shippers will pay the premium for a Red Sea route when the Persian Gulf path is cheaper and insured — but the data-centre campus is unaffected, because hyperscale tenants choose location based on power cost, latency, and physical security, none of which Hormuz governs. If Hormuz stays contested, both theses strengthen simultaneously, which gives Oxagon a floor it lacked before February 2026: the worst-case scenario for the bypass argument leaves the data-centre argument intact.

The cable infrastructure running through the Red Sea — the submarine networks linking Europe to Asia via the Suez Canal — provides Oxagon with latency advantages to European, African, and South Asian markets that an inland site in Riyadh or Dammam cannot replicate, and the zone’s access to renewable power at scale means operating costs for energy-intensive AI workloads are structurally lower than in locations dependent on gas-fired generation. These are the fundamentals that attracted DataVolt before the war and they are the fundamentals that will persist after it — the data-centre thesis is properly understood not as a Hormuz play but as a geography play that the Hormuz crisis happens to have made more attractive, and the best case for the combined logistics-and-data-centre thesis requires not just favourable geopolitics but a rail connection to the national network that does not yet exist and is, as of this week, further away than it was.

Can Oxagon Work Without the Rail Link?

Not as a primary trade corridor, and the most rigorous external assessment says so directly. The Bahrain Institute for Strategic and International Studies published an analysis on May 25, 2026, identifying the Tabuk–NEOM rail segment as “not expected to achieve operational capacity before 2029 at the earliest,” which means a port already well into its final construction phase will spend at least three years without the land-bridge connection that would integrate it into the broader GCC logistics network. BISI’s conclusion — that the corridor is “likely to function in a supplementary role rather than as a primary route” — is the kind of frank structural assessment that Oxagon’s advocates need to engage with rather than dismiss, because the gap between a supplementary logistics node and a Hormuz bypass is the gap between a $3 billion port investment that earns its keep and one that waits years for the infrastructure that makes it whole.

The rail problem is compounded by NEOM’s own cancellations. The Connector HSR contract with Webuild, worth EUR 1.4 billion, was terminated on May 27, 2026 — NEOM’s second Webuild termination in sixty days, following the EUR 2.8 billion Trojena dam in March — and total terminated contracts across NEOM now exceed $8.45 billion while construction awards have fallen from $71 billion to $30 billion, a 58 per cent decline. The rail that would have connected Oxagon to The Line is gone, the external rail to the national network is years away, and the multimodal corridor from Europe via Egypt remains Oxagon’s primary logistics lifeline for the foreseeable future.

That corridor — the Trieste–Damietta–Safaga–NEOM route launched on April 14 — partially compensates by providing an operational import pathway that does not depend on Saudi rail, but it handles trucks and cars via RoPax ferries, not bulk cargo or containerised exports at the volumes the port was designed for. BISI also flagged cyberattack risks on the port’s digital systems, a concern that gains weight given the sophistication of Iranian offensive cyber capabilities and the PGSA’s demonstrated willingness to enforce Hormuz compliance through both kinetic and electronic pressure. The honest assessment is that Oxagon’s port is ahead of its logistics ecosystem, and whether that gap closes before the Hormuz crisis resolves will determine whether the port becomes a permanent trade node or a well-built facility waiting for a network that arrives too late.

The Paradox Saudi Arabia Cannot Solve

Saudi diplomacy is working to reopen Hormuz. Foreign Minister Faisal bin Farhan said on May 20 that the goal is to “restore Hormuz to the state prior to February 28th, 2026” — language that implicitly demands the dismantlement of the PGSA toll system and the resumption of unrestricted commercial transit. If that effort succeeds, Oxagon’s urgency as a logistics bypass diminishes to exactly what it was before the war: a theoretical hedge against a scenario that just became theoretical again, with the billions committed to port infrastructure remaining physically intact but commercially undercut, because the freight that justifies 1.5 million TEUs per year of capacity follows the cheapest route, and the cheapest route through an open Hormuz does not run through a new Red Sea port with no rail link.

Private capital, however, is moving in the opposite direction, betting that Hormuz contestation has permanently altered the risk calculus for Gulf shipping regardless of whatever diplomatic language emerges from Muscat or Washington. Insurance memory — the phenomenon by which underwriters reprice risk corridors for years or decades after a crisis, regardless of whether the immediate threat persists — is the mechanism that could make Oxagon’s logistics thesis durable even after a deal is signed. War-risk premiums for Hormuz transit are running at eight times pre-war levels, P&I clubs including Gard, Skuld, and NorthStandard have cancelled cover, and the ECFR’s assessment that IMEC was “conceived for peacetime conditions” implicitly argues that any Hormuz-dependent corridor now carries a structural risk premium that pre-war planning ignored.

“Papers and signatures are not guarantees. The objective guarantee for preserving any agreement is the Strait of Hormuz.”

— Ali Akbar Velayati, senior foreign policy adviser to Supreme Leader Khamenei, May 28, 2026

Velayati’s statement — delivered by the man whose foreign policy portfolio includes the PGSA architecture — captures the paradox from the adversary’s side. If Iran treats Hormuz as a permanent coercive instrument rather than a temporary wartime measure, then the conditions that validate Oxagon’s logistics bypass are conditions that Tehran actively intends to maintain, deal or no deal. The PGSA, even under OFAC sanctions, collects revenue with every transit it prices, and Iran’s incentive to dismantle a toll system generating an estimated $1–2 billion annually is precisely zero unless the sanctions relief on offer exceeds that figure — a threshold the Trump administration has publicly refused to meet.

The paradox deepens when you trace Saudi Arabia’s position in the three governance architectures that will determine Hormuz’s future. The UK-France coalition operating from Northwood has twenty-seven signatories; Saudi Arabia is not among them. Iran’s bilateral track with Oman, which is drafting the legal framework for permanent strait co-management under the 1974 boundary treaty, excludes Saudi Arabia by design — Tehran’s foreign ministry spokesman declared on May 29 that the strait “has nothing to do with the US,” and by extension nothing to do with Washington’s Gulf partners. The PGSA toll system operates independently of any diplomatic process Saudi Arabia participates in, which means the kingdom is building a $9.3 billion bypass for a chokepoint whose future governance is being decided in rooms where Riyadh has no seat, no vote, and no mechanism to obtain either.

Does Private Capital Actually Believe in Oxagon?

DataVolt’s $5 billion is the most concrete answer, but it comes with qualifications that matter. The commitment was made twelve and a half months before the war, by a Saudi-backed company whose parent, Vision Invest, is backed by the Al Muhaidib Group — one of the kingdom’s oldest and most connected family conglomerates — which means this is not BlackRock testing Saudi regulatory waters or SoftBank writing a speculative cheque but domestic capital deploying into domestic state infrastructure, with all the informational advantages and political incentives that arrangement entails. The $20 billion Supermicro hardware deal expanded the commitment’s industrial reach, but both parties sit within an ecosystem where the Saudi state is simultaneously regulator, infrastructure provider, and — through PIF — the largest investor in the zone.

The competition for AI tenants is real, and it comes from inside the kingdom. HUMAIN, PIF’s dedicated AI subsidiary, is building 100-megawatt data-centre facilities in Riyadh and Dammam expected online in Q2 2026, years ahead of DataVolt’s 2028 first phase, with a total capacity target of 6.4 gigawatts over a decade — more than four times DataVolt’s Oxagon commitment. HUMAIN’s locations are connected to existing power grids, fibre networks, and labour markets, which means the state’s own AI programme is Oxagon’s most formidable competitor for the hyperscale tenants both are courting, and whether Oxagon’s submarine cable access and renewable power outweigh Riyadh’s operational maturity will be answered by the tenants themselves, not by press releases.

Set against the broader NEOM contraction, Oxagon’s survival is as much a story of elimination as of endorsement. The Line is frozen at 1.4 per cent of its planned length with an $8 billion PIF writedown; Trojena has lost its dam and its steel contractor; the Connector HSR is cancelled. What remains — the port, the data-centre campus, and the multimodal corridor — is the industrial core that the war inadvertently elevated by creating demand for the kind of infrastructure that NEOM’s showpiece projects were designed to overshadow, sustained by a PIF whose liquid cash has hit $15 billion and a national budget running a $33.5 billion quarterly deficit that represents 76 per cent of the full-year target in ninety days.

Irina Tsukerman, president of Scarab Rising, told The National in April that “NEOM is being pulled into a more grounded phase” where “the focus now is on what can be built, financed and sustained within clearer limits,” and those clearer limits are themselves a function of Oxagon’s central trap: the constraints are set by actors in Tehran, Muscat, and Northwood who have no interest in whether Saudi Arabia’s Red Sea port reaches commercial viability, and every interest in maintaining the conditions — toll extraction, insurance repricing, chokepoint governance — that inadvertently make it viable. In November 2025, when Hormuz was open and Oxagon was still the part of NEOM that nobody mentioned at investor conferences, Wanchoo told AGBI that the port’s only real obstacle was Houthi attacks on Red Sea shipping — not Iran, not a Hormuz toll system, not a war that would begin three months later and redirect the commercial logic of an entire region toward the coastline where his cranes were already working. The obstacles have since multiplied beyond anything that interview anticipated, and the port is 68 per cent built, taking cargo from four European countries, and waiting for a rail link that the kingdom just cancelled.

Frequently Asked Questions

Who owns DataVolt and what is its track record?

DataVolt is a wholly owned subsidiary of Vision Invest, a Saudi development and investment holding company founded in 2023 and led by CEO Rajit Nanda. Vision Invest is backed by the Al Muhaidib Group, one of Saudi Arabia’s oldest family conglomerates with roots tracing to the 1940s, whose portfolio spans real estate, food distribution, industrial services, and now critical digital infrastructure. DataVolt claims to have developed and operated over twenty gigawatts of renewable energy assets across nine countries, though the company is relatively new — its Oxagon campus represents its highest-profile commitment, and the $20 billion Supermicro hardware partnership signed in May 2025 expanded its footprint from a single-site developer to a player in the global hyperscale supply chain.

How does the PGSA toll system create a permanent commercial case for Oxagon?

Iran’s Persian Gulf Shipping Authority operates a three-tier pricing architecture that functions as a de facto commercial blockade even without kinetic closure. Bilateral carve-out agreements with India, Iraq, and Pakistan grant those countries’ vessels free passage, while grey-fleet and non-exempt commercial vessels pay approximately $2 million per transit in yuan or bitcoin — a toll high enough to permanently reroute cost-sensitive cargo. The OFAC designation of the PGSA on May 28, 2026, created a compliance binary: any entity paying the toll now transacts with a sanctioned body, which means insurers, banks, and cargo owners face a choice between Hormuz transit with sanctions exposure and alternative routing without it. That compliance fork makes Oxagon’s bypass function commercially relevant regardless of whether kinetic hostilities continue, because the sanctions architecture persists independently of any ceasefire.

Does Oxagon compete with Yanbu for the same cargo?

Only partially, and the overlap is narrower than it appears. Yanbu is primarily a crude oil and petrochemical export terminal, receiving pipeline crude via the East-West Pipeline and serving as Saudi Arabia’s main Red Sea energy export hub — it handles the rerouted barrels that Aramco diverted from the Persian Gulf but has limited container-terminal infrastructure for non-energy freight. Oxagon is designed for diversified traffic: containerised imports and exports, industrial inputs, data-centre hardware, and the multimodal corridor cargo now arriving from Europe. King Abdullah Port at King Abdullah Economic City, further south on the Red Sea coast, is a more direct competitor with existing container capacity, though it lacks Oxagon’s integration with the data-centre campus and industrial zone that DataVolt and NEOM are building together.

What is the current status of NEOM’s other zones?

The Line, NEOM’s most publicised component, is frozen at 2.4 kilometres of a planned 170-kilometre mirror-walled city, with an $8 billion PIF writedown and a population target reduced from 1.5 million to fewer than 300,000; no construction restart date has been announced. Trojena, the mountain resort that the International Olympic Committee selected to host the 2029 Asian Winter Games, has lost its EUR 2.8 billion dam contract with Webuild and its structural steelwork contractor Eversendai, raising questions about whether the Games timeline can survive the construction pullback. Sindalah, the luxury island that NEOM marketed as its “first destination,” has marina and resort construction reportedly nearing completion, though no firm opening date has been set since the war began. Oxagon is the only zone whose external commercial environment has improved since February 2026 — a distinction that would have seemed implausible when the first missile struck. PIF’s 2026-2030 strategy codified this outcome by reclassifying NEOM as a standalone pillar, isolating its write-downs from the fund’s remaining portfolios while committing $3 billion to Oxagon specifically.