DHAHRAN — OPEC’s April monthly report confirms what commodity desks already suspected: the Iran war produced the largest crude supply shock in at least four decades. Total OPEC output fell 7.9 million barrels per day in March — a 27% monthly collapse — while the broader OPEC+ group came in 8.14 million bpd below its pre-war production baseline. Saudi Arabia holds more pricing power than at any point since 1973. It cannot collect the fiscal reward. Brent at $98–103 per barrel, depressed by Round 2 ceasefire diplomacy, sits $5–13 below the Kingdom’s PIF-inclusive fiscal breakeven of $108–111. The world’s peace dividend is Riyadh’s budget crisis. The IMF’s own 3.1% forecast for 2026 rests on a Hormuz normalisation assumption that the mine-clearance timeline makes impossible before late Q3.

The numbers describe a structural trap with no precedent in modern oil-market history. Saudi Arabia’s production fell 23% to 7.8 million bpd — not because its wells failed, but because the Strait of Hormuz, which carried 7.1 million bpd of Saudi crude before the war, now carries almost nothing. The East-West Pipeline to Yanbu is running at its 7 million bpd transport capacity. The port can load roughly 5 million bpd. That 1.1–1.6 million bpd infrastructure gap cannot be closed before mid-2027.

Table of Contents

- What Does the OPEC+ March Data Actually Show?

- The Country-Level Breakdown

- Why Is Brent Below Saudi Arabia’s Fiscal Breakeven Despite the Worst Supply Shock in Decades?

- The 1990 Parallel: When Windfalls Disappear

- The Revenue Neutrality Trap

- Does MBS Have a Financial Incentive to Let the Crisis Continue?

- The May OSP Trap and the June Repricing Crisis

- Who Is Profiting from Saudi Arabia’s Structural Deficit?

- What Happens When the Ceasefire Expires on April 22?

- FAQ

What Does the OPEC+ March Data Actually Show?

OPEC’s 13-member crude output fell from 28.7 million bpd in February to 20.79 million bpd in March — a decline of 7.9 million bpd in a single month. The broader OPEC+ group (including Russia and allied producers) delivered 25.201 million bpd against a planned 32.078 million bpd, a shortfall of 6.877 million bpd against quota. Measured against February’s actual production rather than the quota floor, the gap widens to 8.14 million bpd.

Goldman Sachs called it “the largest supply shock in the history of the global crude market.” The IEA’s Fatih Birol went further. “This rivals the two major oil crises in the 1970s and the 2022 natural gas crisis after Russia invaded Ukraine, all put together,” the IEA executive director told Euronews on April 14. Global inventories drew down 85 million barrels in March alone. April demand destruction is running at 2.3 million bpd — demand is falling, and the deficit is still widening.

OPEC’s April incremental production increase — 206,000 bpd split across eight countries — replaces less than 2% of the disrupted supply. The next formal OPEC+ review is May 3. The market is not waiting for OPEC+ to act; it is pricing the ceasefire.

The Country-Level Breakdown

The distribution of the production collapse tells its own story. Three Gulf producers — Saudi Arabia, Iraq, and Kuwait — account for the bulk of the shortfall. All three depended on Hormuz for the majority of their export volumes.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

| Country | Feb 2026 Output (mbd) | Mar 2026 Output (mbd) | OPEC+ Quota (mbd) | Gap vs Quota (mbd) | Monthly Change |

|---|---|---|---|---|---|

| Saudi Arabia | 10.1 | 7.8 | 10.1 | −2.304 | −23% |

| Iraq | 4.2 | 1.63 | 4.3 | −2.670 | −61% |

| Kuwait | ~2.7 | ~1.33 | 2.7 | −1.367 | ~−51% |

| UAE | ~3.3 | ~1.96 | 3.3 | −1.341 | ~−41% |

| Iran | 3.24 | 3.06 | n/a | n/a | −5.6% |

| Russia | 9.164 | 9.167 | 9.574 | −0.407 | +0.03% |

| Kazakhstan | — | — | — | +0.783 | Overproduced |

Iraq’s 61% collapse is the sharpest in the table. Its southern export terminals — Basra Oil Terminal and Khor al-Amaya — depend on tanker access through the northern Gulf and Hormuz. Saudi Arabia’s 23% decline is smaller in percentage terms but larger in absolute volume: 2.3 million bpd removed from a market that was already drawing inventories before the war began.

Two entries stand out at the bottom of the table. Iran’s production fell 5.6% — from 3.24 to 3.06 million bpd — a rounding error relative to the carnage elsewhere. Russia’s output rose by 3,000 bpd. Kazakhstan overproduced its OPEC+ quota by 783,000 bpd, free-riding on the supply shock with impunity. The compliance problem that plagued OPEC+ before the war has not gone away; it has become irrelevant in a market where the constraint is not quotas but infrastructure.

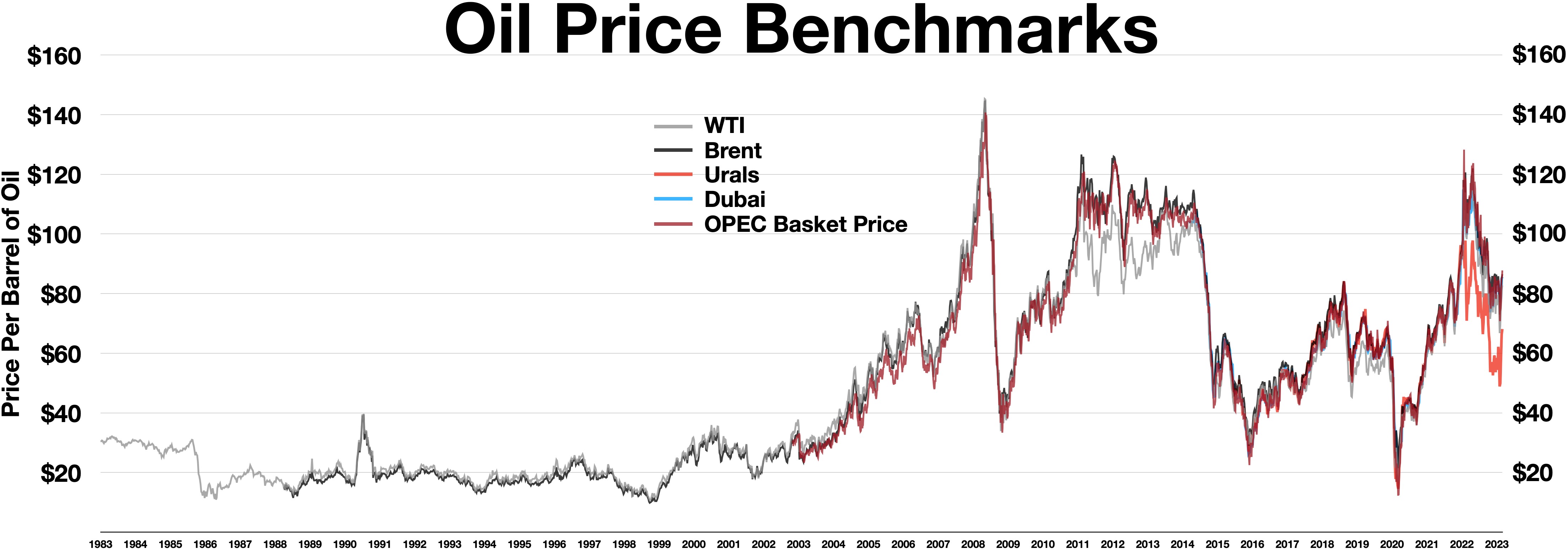

Why Is Brent Below Saudi Arabia’s Fiscal Breakeven Despite the Worst Supply Shock in Decades?

The answer is ceasefire diplomacy. Brent peaked near $130 in early March, when the Hormuz closure was total and Round 1 negotiations had not yet begun. The April 7–8 ceasefire — fragile, unsigned by the IRGC, and enforced by Pakistan through an improvised relay mechanism — triggered a 13.3% single-day drop in Brent to $94.75. The subsequent drift back to $98–103 reflects the market’s probability-weighted bet: Round 2 diplomacy in Islamabad will produce a Hormuz reopening framework before the April 22 ceasefire expiry.

That bet may be wrong. But the market does not need to be right; it needs to be priced. At $98–103, the price sits in the zone that hurts Saudi Arabia most: high enough to signal crisis, too low to fund the PIF-inclusive budget.

Bloomberg Economics pegs the PIF-inclusive fiscal breakeven at $108–111 per barrel — the threshold that captures both central government spending and the sovereign wealth fund’s $71 billion in committed disbursements. The IMF’s narrower central-government-only figure of $86.60 excludes the spending that defines MBS’s domestic programme. Tim Callen of the Arab Gulf States Institute frames the dependency plainly: “Oil revenue remains critical to the Saudi budget outcome even as non-oil revenue grows.”

At $98–103, every barrel Saudi Arabia exports generates revenue. It does not generate enough. Goldman Sachs estimates the 2026 budget deficit at 6.6% of GDP — roughly $80–90 billion against the official projection of $44 billion. AGSI calculates that every $10 per barrel increase in Brent reduces the Saudi fiscal deficit by 80 billion riyals (~$21 billion); every $10 decrease widens it by 50 billion riyals (~$13 billion). Brent needs to rise $5–8 from current levels just to reach the low end of the breakeven band — and even that assumes full export volumes, which Saudi Arabia does not have.

The 1990 Parallel: When Windfalls Disappear

When Iraq invaded Kuwait on August 2, 1990, crude spiked from $21 to $46 per barrel. Saudi Arabia was the world’s swing producer. It ramped from 5.4 million bpd to 7.9 million bpd within months. Business Week projected a windfall of $45–65 billion.

The windfall never arrived. As the Middle East Research and Information Project documented, “the costs of the Gulf war exceeded all of the petrodollar windfall and most of its liquid assets, compelling Riyadh to borrow abroad.” Saudi Arabia was simultaneously the dominant supplier and the primary financier of the coalition — paying an estimated $60 billion toward war costs while absorbing Kuwaiti refugees and displaced workers. The higher price and the higher volume existed on paper; the fiscal surplus did not.

The 2026 version inverts the mechanism but reaches the same result. In 1990, the windfall was consumed by war expenditures. In 2026, the windfall cannot be produced. Saudi Arabia’s wells can pump 10.1 million bpd. Its pipeline can transport 7 million bpd. Its port at Yanbu can load roughly 5 million bpd. The bottleneck is a loading dock on the Red Sea coast, and expanding it requires 18–24 months of construction — a timeline that outlasts any plausible ceasefire framework.

The 1973 embargo offers the other bookend. King Faisal held roughly 25% of global reserves and used them to quadruple oil prices — from $3 to $12 per barrel — in a matter of months. Saudi oil revenues jumped 40-fold between 1965 and 1975. Even Faisal recognized the feedback loop: petrodollars invested in Western banks would be eroded by the very inflation the embargo triggered. In 2026, the constraint is physical rather than monetary, but the result — maximum pricing power that cannot be converted into fiscal gain — is the same.

The Revenue Neutrality Trap

At $98–103 Brent with approximately 5 million bpd in exports, Saudi Arabia generates roughly $490–515 million per day in crude revenue. Before the war, at $75 Brent with 7.1 million bpd flowing through Hormuz, daily revenue was approximately $533 million — roughly $20–43 million more per day than now.

The war gave Saudi Arabia the price it needed and took away the volume to collect it. Revenue is down slightly on a per-day basis while the fiscal position has deteriorated sharply, because the war imposed additional costs: PAC-3 interceptor expenditure alone has consumed an estimated $3.49 billion since March 3, and Aramco infrastructure from Ras Tanura to SABIC’s Jubail complex has sustained physical damage. The East-West Pipeline to Yanbu is intact and running at capacity, but the port infrastructure that converts pipeline throughput into export revenue was built for a supplementary role, not as the Kingdom’s sole maritime outlet.

The revenue trap has a second dimension. Aramco set its May Official Selling Price for Arab Light to Asia at a record +$19.50 per barrel above the Oman/Dubai benchmark average — announced April 6 when Brent was trading near $109. With Brent now at $98–103, term-contract buyers are paying $11–15 per barrel above spot. A Bloomberg survey of Asian traders had expected a May OSP of +$40 per barrel; Aramco left $20.50 per barrel on the table. The EIA’s April STEO projects this pricing paradox extends through year-end: the quarterly fiscal exposure sees Q4 2026 Brent falling to $88 — a level at which the May OSP restraint, compounding through successive repricing cycles, converts from a market-share gamble into a structural deficit accelerant.

The restraint was deliberate. At full Hormuz volumes, Aramco can afford to underprice spot because volume compensates — term-contract loyalty is worth more than marginal barrel revenue. At 5 million bpd, every dollar of OSP restraint is a dollar that cannot be recovered through volume. Aramco priced the May OSP for a world where Hormuz reopens. If Hormuz does not reopen by June, the restraint becomes a subsidy to Asian refiners funded by Saudi Arabia’s fiscal deficit.

Does MBS Have a Financial Incentive to Let the Crisis Continue?

Three scenarios define MBS’s decision space, and none of them produces fiscal recovery before 2027.

Scenario 1: Hormuz reopens, Brent crashes. If Round 2 diplomacy succeeds and Hormuz traffic normalizes, the supply gap closes rapidly. JPMorgan’s modelling suggests Brent could fall to $70–75 within 60–90 days of a full reopening — below even the IMF’s central-government-only breakeven of $86.60. Saudi exports would recover to 7+ million bpd, but at prices that produce a deficit larger than the current one. This is the scenario the market is pricing. It is the worst fiscal outcome for Riyadh.

Scenario 2: Blockade persists, Yanbu ceiling holds. Brent stays at $98–103 or drifts higher as inventories deplete. Saudi exports remain capped at ~5 million bpd. The deficit widens toward $80–90 billion. PIF construction spending, already cut 58% to $30 billion, faces further reduction. The Aramco base dividend — cut approximately one-third from $124.2 billion in 2024 to $85.4 billion for 2025 — may need another revision. This is the status quo, and it is not sustainable.

Scenario 3: Hormuz reopens with a US security guarantee. This scenario requires both Hormuz reopening (restoring volume) and a binding mechanism — a mutual defense treaty, a permanent CENTCOM force posture, or a NATO-equivalent Article 5 commitment — that prevents the next Hormuz closure. That would raise Saudi Arabia’s structural export baseline above the Yanbu ceiling permanently, making the $108–111 breakeven achievable at lower prices through higher volume. It is not on the table in Islamabad. The US has not offered it. Pakistan cannot deliver it.

MBS does not have a financial incentive to prolong the crisis. He has no financial incentive to end it on the terms currently available. Riyadh’s optimal outcome is a negotiated settlement that includes infrastructure guarantees — and the absence of such guarantees from the Islamabad framework is the gap that Saudi diplomacy has not yet bridged.

The May OSP Trap and the June Repricing Crisis

Aramco must announce its June Official Selling Price around May 5. The decision will be made in the shadow of the May 3 OPEC+ review and within 11 days of the April 22 ceasefire expiry. Three variables will have moved by then, and none of them in a direction that simplifies the pricing decision.

If the ceasefire holds and extends, Brent will likely fall further — toward $90 or below — as the market prices normalization. Aramco would face pressure to cut the OSP from the record +$19.50, potentially by $5–10, to retain Asian term-contract buyers who have been paying well above spot for two months. A sharp OSP cut signals weakness and invites buyers to renegotiate 2027 term contracts at structurally lower premiums.

If the ceasefire collapses on April 22, Brent spikes — JPMorgan’s $150 scenario becomes plausible if Hormuz remains blocked into mid-May. Aramco could raise the June OSP toward the $40 premium that Bloomberg’s trader survey expected for May. But at 5 million bpd export capacity, the higher OSP generates incremental revenue only on barrels that are already committed to term contracts. There are no marginal barrels to sell at the higher price.

North Sea Dated crude — the physical delivery benchmark — is already trading at approximately $130 per barrel, a $20–30 premium over Brent futures. The physical market is tighter than the financial market acknowledges. If the June OSP lands in the gap between futures and physical, Aramco may inadvertently anchor a repricing of the entire Asian term-contract market at levels that assume permanent supply disruption.

Who Is Profiting from Saudi Arabia’s Structural Deficit?

The OPEC+ production table contains its own answer. Iran’s output fell 5.6% — from 3.24 to 3.06 million bpd — in the month it caused the worst supply shock in four decades. Iran’s Parliament passed a bill on March 31 authorizing the collection of transit fees through Hormuz at rates exceeding $1 million per vessel, processed through Kunlun Bank and USDT on the Tron blockchain. Iran is earning revenue from the crisis it created. Saudi Arabia is earning less than it did before the crisis began.

Russia’s output rose by 3,000 bpd in March. Its OPEC+ underperformance — 407,000 bpd below quota — is modest and likely reflects sanctions logistics rather than physical disruption. Elevated Brent prices flow directly to the Russian fiscal position through non-sanctioned export routes. Moscow voted with OPEC+ to hold production levels on April 5.

Kazakhstan overproduced its quota by 783,000 bpd — the largest free-riding violation in the current OPEC+ framework. In a normal market, Saudi Arabia would respond with a price war, as it did in 2020 and threatened in late 2024. In this market, Saudi Arabia cannot increase production to discipline a free-rider because its export infrastructure, not its wellhead capacity, is the binding constraint. Kazakhstan’s overproduction is a consequence of Saudi vulnerability, not its cause.

The annual revenue gap attributable to the export constraint — the difference between what Saudi Arabia would earn at current prices with full Hormuz access and what it actually earns at the Yanbu ceiling — is approximately $63 billion per year at current Brent levels. That figure exceeds the official 2026 budget deficit of $44 billion.

What Happens When the Ceasefire Expires on April 22?

The ceasefire expires in eight days. There is no extension mechanism. The Soufan Center has documented the absence of a renewal clause in the Islamabad framework. Pakistan, the sole enforcement mechanism, is simultaneously Iran’s interlocutor and Saudi Arabia’s SMDA treaty ally — a structural contradiction that limits its capacity to adjudicate violations.

The oil market’s response to April 22 will depend on what the preceding days produce. If Vance and Ghalibaf’s Islamabad track yields a framework — even a preliminary one — Brent will price the expectation of extension. If the talks collapse, or if the IRGC’s “full authority” declaration over Hormuz (issued April 5 and reiterated April 10) translates into a resumption of vessel interdictions, the physical market reprices toward the $130 North Sea Dated level within days.

Saudi Arabia’s position in either outcome is constrained by the same infrastructure ceiling. A Hormuz reopening takes weeks to translate into higher Saudi export volumes — tanker scheduling, insurance reinstatement, and the de-mining of the approaches that the IRGC declared a “danger zone” on April 9. The US Navy has three Littoral Combat Ships in Asia and zero Avenger-class mine countermeasure vessels in the Gulf after the last four were decommissioned at Bahrain in September 2025. The IEA estimates that clearing the standard shipping lanes would require 200 square miles of survey, a process benchmarked against the 1991 Kuwait operation at approximately 51 days.

Even the optimistic scenario — ceasefire extended, Hormuz gradually reopened, mine clearance begun — does not deliver full Saudi export capacity before mid-June. The June OSP will be set around May 5. The May 3 OPEC+ review will convene before the ceasefire has expired or extended. The Sadara debt grace period expires June 15. Each pricing and production decision in the next three weeks precedes the diplomatic outcome it depends on.

| Date | Event | Oil Market Impact |

|---|---|---|

| April 18 | Hajj arrival corridor opens; Umrah cordon seals | Raises kinetic threshold — military escalation during Hajj carries Custodian-title risk |

| April 22 | Ceasefire expires (no extension clause) | Binary: extension = Brent drift lower; collapse = spike toward $130+ physical |

| May 3 | OPEC+ ministerial review | Production adjustment decision — 206,000 bpd April increment under review |

| ~May 5 | Aramco June OSP announcement | Repricing of entire Asian term-contract market based on post-ceasefire outlook |

| May 25–26 | Hajj peak (Arafat/Muzdalifah) | Maximum diplomatic sensitivity window — 2+ million pilgrims in Mecca corridor |

| June 15 | Sadara $3.7B debt grace period expires | First potential corporate default linked to war-related production shutdown |

FAQ

How does Saudi Arabia’s current export capacity compare to its pre-war peak?

Saudi Arabia exported 7.1 million bpd through Hormuz before the war. The East-West Pipeline to Yanbu is now transporting at its full 7 million bpd design capacity, but Yanbu’s port loading infrastructure — berths, single-point mooring buoys, and storage — was built as a supplementary outlet, not a primary one. Engineering News-Record and Bloomberg reporting indicate the effective loading ceiling is 5–5.9 million bpd. Closing the gap requires new deep-water berth construction at Yanbu, a project estimated at 18–24 months. Aramco CEO Amin Nasser has confirmed the pipeline is operating at design capacity but has not publicly addressed the port bottleneck.

Why did Aramco set the May OSP below what traders expected?

Bloomberg surveyed Asian traders who expected a May OSP of +$40 per barrel above the Oman/Dubai average. Aramco set it at +$19.50 — a record, but $20.50 below expectations. The restraint reflects term-contract management: Aramco’s major Asian buyers (refiners in China, India, Japan, and South Korea) have long-term supply agreements, and aggressive crisis pricing risks triggering contract renegotiations or diversification toward non-Saudi suppliers once Hormuz reopens. Aramco’s December 2024 market-share defense — when it cut the OSP to protect volume against Russian and Iraqi competition — established the institutional precedent that term-contract loyalty outweighs short-term margin maximization. The decision assumed Hormuz would reopen; if it does not, the restraint becomes an unrecoverable loss.

What is the Sadara debt default risk mentioned in the timeline?

Sadara Chemical Company — a $20 billion Aramco-Dow joint venture in Jubail — has been in force majeure since late March following IRGC missile strikes that damaged petrochemical infrastructure in the Eastern Province. The company carries $3.7 billion in project-finance debt. A grace period on debt service obligations expires June 15. If Jubail operations have not resumed by that date, Sadara’s lenders — a consortium led by Saudi and international banks — face the first potential corporate default directly attributable to the war. ExxonMobil and Dow Chemical hold indirect equity exposure through their stakes in Saudi downstream ventures, creating a transmission mechanism to US capital markets that the credit agencies have not yet priced.

Could OPEC+ increase production to offset the shortfall?

The April incremental increase of 206,000 bpd — split across eight countries — replaces less than 2% of the 8.14 million bpd gap between OPEC+ February output and March actuals. The constraint is not quota allocation but physical export capacity. Saudi Arabia, Iraq, Kuwait, and the UAE collectively lost access to Hormuz-dependent export terminals. Even if OPEC+ authorized maximum production, the tankers cannot reach the loading docks. The producers with spare capacity outside the Hormuz chokepoint — primarily Kazakhstan, which is already overproducing its quota by 783,000 bpd — lack the pipeline connectivity and port infrastructure to substitute for Gulf volumes at scale. OPEC+ can adjust targets. It cannot move oil through a closed strait.

How does the IEA characterize the severity of this crisis relative to historical precedents?

IEA Executive Director Fatih Birol, speaking to Euronews on April 14, called it worse than the 1970s oil shocks and the 2022 European gas crisis combined. The IEA’s April Oil Market Report documents an 85-million-barrel global inventory draw in March and a Hormuz throughput collapse from 20 million bpd to 3.8 million bpd — an 81% reduction. The physical crude market (North Sea Dated) is trading at approximately $130 per barrel, a $20–30 premium over Brent futures, indicating the paper market has not fully priced the physical scarcity. The IEA rarely draws direct parallels to the 1973 and 1979 crises; both of those restructured the global energy order. The mechanics of that gap — why physical crude hit $148.87 while Brent futures sat at $99.36 on the same April 13 session — are analyzed in detail in The $50 Crude Gap Saudi Arabia Has to Fix Before May 5.

The cost of winning the market is now visible in China’s loading schedules: record-low Saudi volumes to China in May — approximately 20 million barrels, down from 40 million in April — show that the OSP premium required to sustain Saudi fiscal arithmetic has already triggered the buyer defection that makes that arithmetic unsustainable.

The same fiscal pressure accelerating PIF’s retreat from prestige spending is behind its decision to pull funding from LIV Golf after 2026, replacing the Khashoggi-era reputation architecture with Special Economic Zones designed to generate returns. That strategic reset is analyzed in PIF Just Killed the Architecture It Built to Apologise for Khashoggi.