DHAHRAN — Trump threatened to seize Kharg Island at the NATO summit in Ankara on July 8. The island sits twenty miles off Iran’s coast and loads approximately 1.5 million barrels per day — between 90 and 96 percent of everything Iran exports — and Brent surged more than 5 percent before anyone in Riyadh could decide whether the kingdom should welcome the price spike or brace for the retaliation it triggers. Saudi Arabia is the principal financial beneficiary of an escalation it was not consulted on, cannot endorse without activating the IRGC’s publicly stated 2:1 retaliation doctrine against its own oil infrastructure, and cannot oppose without fracturing the one relationship keeping its 400 remaining PAC-3 interceptors on a resupply track.

The windfall arithmetic is seductive: every dollar above the IMF’s $86.60-per-barrel Saudi breakeven reclaims ground on a Q1 deficit that consumed $33.5 billion in ninety days, and every barrel Iran loses at Kharg is a barrel the market eventually sources elsewhere. The problem is the ceiling. The kingdom’s only export route bypassing the Gulf — the East-West Petroline — hit its absolute maximum capacity of 7 million barrels per day on March 11. Every additional barrel beyond that must load at Ras Tanura and Ju’aymah, the very terminals Iran has already struck and publicly named as future targets.

Table of Contents

- What Does Kharg Mean to Iran’s War Economy?

- How Much Is the Windfall Actually Worth to Riyadh?

- The Petroline Ceiling

- Why Can’t Saudi Arabia Fill the Gap Kharg Leaves?

- The 2:1 Doctrine and the Ras Tanura Arithmetic

- What Happens When Retaliation Reaches Ras Tanura?

- The Tanker War in Reverse

- The Silence That Isn’t Neutral

- Frequently Asked Questions

What Does Kharg Mean to Iran’s War Economy?

Kharg handles between 90 and 96 percent of Iran’s total crude export capacity. It is a flat shelf roughly five kilometres long in shallow water off Iran’s Bushehr province — a single point of failure for a war economy running on crude revenue. Three terminal systems (the main T-jetty, the Sea Island installation, and the offshore single-point moorings) can load up to 7 million barrels per day at maximum capacity, though actual throughput hovers between 1.52 and 1.58 million bpd, constrained by sanctions rather than infrastructure, according to Iran Open Data and Al Jazeera’s March 2026 reporting. When Trump told the NATO press pool at Ankara that he might seize the island outright, he was describing the capture of the central economic artery that funds the IRGC’s war.

“We may take over Kharg Island, and there’s not a thing they can do about it.”

Donald Trump, NATO summit, Ankara, July 8, 2026

CENTCOM had already struck Kharg as part of the July 7–8 retaliatory package — more than 80 strikes across Kharg, Bandar Abbas, Sirik, and Qeshm Island, according to CNN and NPR — but the Pentagon specified that US forces “attacked everything except the islands’ energy infrastructure,” a distinction Trump appeared to erase within twenty-four hours by floating seizure and blockade. The escalation ladder here is not between striking and not striking, it is between degrading Iran’s military positions on the island and seizing or blockading the commercial infrastructure that funds the IRGC’s ability to fight. Bilal Y. Saab, a senior fellow at the Middle East Institute’s defence and security programme, framed the logic bluntly: the US military could “remove an economic lifeline for the regime — and perhaps lower its chances of survival — and stabilize global energy markets.”

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The United Against Nuclear Iran (UANI) project tracked 47 tankers carrying approximately $4.5 billion worth of Iranian crude during the MOU ceasefire window before GL X1 sanctions were reimposed on July 7 — a rough measure of what Kharg’s continued operation is worth to Tehran in any given pause. Remove it entirely, and Iran’s war economy loses its primary revenue artery. The barrels do not disappear from global demand — they become someone else’s market share to claim. The obvious candidate sits four hundred miles across the Gulf in a kingdom that desperately needs the revenue but cannot safely collect it.

How Much Is the Windfall Actually Worth to Riyadh?

Saudi Arabia entered 2026 with an IMF-confirmed fiscal breakeven of $86.60 per barrel — the price at which government revenue covers government spending — according to the December 2025 Article IV assessment. Brent closed at $76.24 on July 10, a $10.36 gap that costs the kingdom roughly $50 million per day in forgone revenue across approximately 5 million barrels of daily exports. A full Kharg disruption would remove 1.5 to 2.0 million barrels per day from global supply and push Brent $10 to $15 per barrel higher, according to TradeThePool’s price-elasticity modelling. That would theoretically vault prices above breakeven for the first time since the war’s early weeks.

The haemorrhage is real and measurable. Aramco’s Q1 2026 free cash flow came in at $18.6 billion against a quarterly dividend obligation of $21.89 billion — a coverage ratio of 0.85x — meaning the company paid out more than it generated and drew reserves down to $53.3 billion, the lowest since end-2018, according to the Q1 Interim Report. The kingdom’s Q1 deficit hit $33.5 billion, consuming 76 percent of the full-year budget projection in ninety days. Goldman Sachs now forecasts the actual annual deficit at $80 to $90 billion, with total public debt at SAR 1.67 trillion (roughly $445 billion) at end-Q1. Frank Callen of the Arab Gulf States Institute put it plainly: “funding will depend on borrowing or the sale of existing assets.”

| Metric | Value | Source |

|---|---|---|

| IMF fiscal breakeven | $86.60/bbl | IMF Article IV, Dec 2025 |

| Brent close (July 10) | $76.24 | Market data |

| Breakeven gap | −$10.36/bbl | Derived |

| Q1 2026 deficit | $33.5 billion | MoF / AGSI |

| Aramco FCF coverage ratio | 0.85× | Q1 Interim Report |

| Aramco cash reserves | $53.3 billion | Q1 Interim Report |

| Goldman full-year deficit forecast | $80–90 billion | Goldman Sachs |

| Full Kharg disruption price impact | +$10–15/bbl | TradeThePool |

| EIA STEO Brent forecast Q4 2026 | $70/bbl | EIA July 2026 |

The table describes a kingdom bleeding cash at every price below $86.60 and a single external event — Kharg’s closure — that could push Brent above that line, but only temporarily. The EIA’s Short-Term Energy Outlook for July 2026 projects Brent averaging $70 in Q4 and $65 in 2027, with global inventories building by 2.7 million barrels per day in Q4 and 5.0 million in 2027 — a market structurally pushing prices lower regardless of Kharg. AGBI’s June editorial, written when Brent still traded above $90, captured the structural paradox: “The war Saudi Arabia is asking to end is the mechanism keeping Brent above $90,” the paper wrote, adding that “the peace Saudi Arabia is asking for is the fiscal event most damaging to its own budget.” As Brent’s war premium has already evaporated, Kharg is the only remaining catalyst with enough force to move prices back toward breakeven — and it comes attached to a retaliation risk the kingdom cannot absorb.

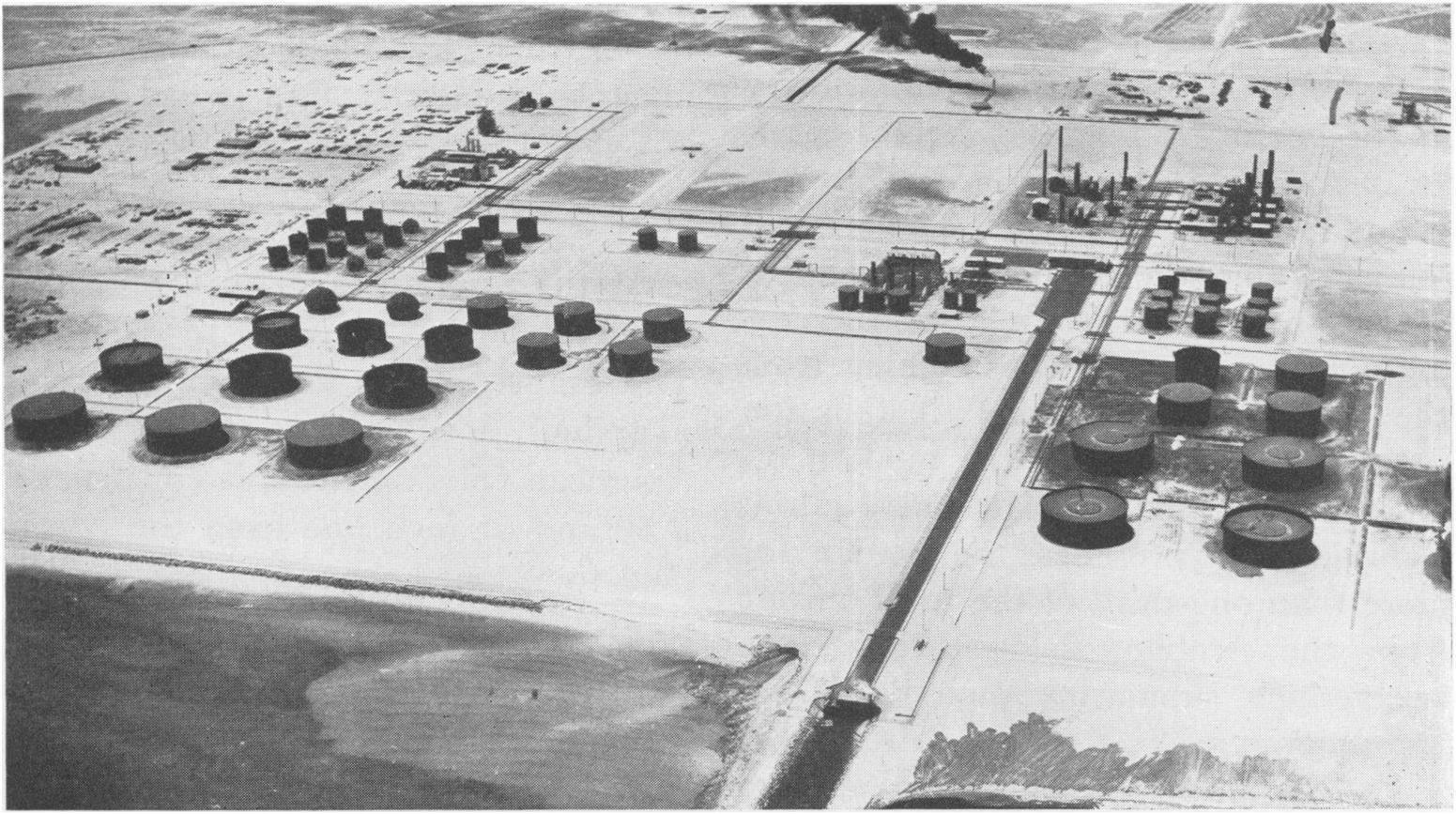

The Petroline Ceiling

The East-West Petroline — the 1,200-kilometre twin pipeline connecting Aramco’s Eastern Province fields to the Yanbu terminal on the Red Sea coast — is Saudi Arabia’s only crude export route that bypasses the Gulf entirely. It is the single piece of infrastructure that allows the kingdom to ship oil without threading it past Iranian missiles. On March 11, 2026, the Petroline reached its absolute maximum capacity of 7 million barrels per day, according to Fortune and the Pipeline Technology Journal. It cannot be expanded further: the right-of-way, pumping stations, and terminal capacity at Yanbu represent a hard physical ceiling that no amount of capital can raise in the timeline of this war.

Of that 7 million bpd, approximately 2 million is consumed by domestic refineries along the route, leaving roughly 5 million barrels per day available for export through Yanbu. Saudi Arabia’s current production exceeds that exportable figure, which means every barrel the kingdom pumps beyond 5 million bpd for export must load at its Gulf-facing terminals: Ras Tanura, Ju’aymah, and the associated offshore platforms. Those terminals sit less than 250 kilometres across the water from Iranian launch sites in Bushehr province and are well within range of the Zolfaghar ballistic missile at 700 kilometres and the Fattah-2 hypersonic system at 1,400 to 1,500 kilometres, according to assessments from the Missile Defense Advocacy Alliance and DefenceSecurityAsia.

This is the structural fact that coverage of the Kharg windfall consistently omits: the windfall is physically capped by the infrastructure that is simultaneously the primary Iranian retaliation target. If Kharg goes offline and Saudi Arabia attempts to capture the freed market share, the additional barrels must route through the exact loading terminals that the IRGC’s 2:1 doctrine designates as response targets, and the pipeline that could bypass this exposure has been running at maximum since before the current escalation cycle began. The ceiling is welded steel and fixed pumping capacity, and it was reached four months ago.

Why Can’t Saudi Arabia Fill the Gap Kharg Leaves?

Saudi Arabia can pump the oil. It cannot move it safely. Every barrel the kingdom adds above the Petroline’s 5 million bpd export ceiling must load at Gulf-facing terminals that Iran has already struck and publicly named as future targets. The theoretical opportunity is large — 1.5 to 2.0 million barrels per day freed from global supply, a market hungry for replacement crude, and the world’s largest declared spare capacity ready to deploy. OPEC+ approved its fifth consecutive 188,000 bpd output hike for August. But producing more barrels means routing them through terminals in the IRGC’s targeting doctrine.

On March 2, 2026, two Iranian drones struck the Ras Tanura refinery complex, according to Bloomberg and The National; both were intercepted, but debris triggered a fire that shut the plant for several weeks. In April, an Iranian drone strike on a Petroline pumping station cut throughput by 700,000 bpd for three days — a brief disruption with lasting implications, because it demonstrated that even the Yanbu bypass route has nodes the IRGC can reach. On April 3, Iran struck Saudi oil export architecture across both coasts in a single coordinated operation that targeted the full breadth of the kingdom’s loading capacity.

The IRGC’s targeting doctrine has explicitly named Sadara — the Aramco-Dow joint venture in Jubail — ExxonMobil facilities in Jubail’s petrochemical corridor, Ras Tanura’s offshore loading platforms, and the Shaybah NGL plant in the Empty Quarter, prioritising infrastructure where American corporate equity sits alongside Saudi crude. To fill the gap Kharg leaves, Aramco would need to push more barrels through Ras Tanura and Ju’aymah at precisely the moment when escalation at Kharg makes those terminals the IRGC’s most valuable retaliation targets — a situation in which the reward of additional market share is denominated in the same barrels that become targets the moment they reach the loading dock.

The 2:1 Doctrine and the Ras Tanura Arithmetic

The IRGC’s retaliation framework is not ambiguous: for every Iranian target struck, Iran will strike at least two enemy targets, a ratio the corps has stated publicly and that analysts documented in the aftermath of the July 7–8 strikes. The doctrine includes an additional threshold — any action triggering permanent seizure of Kharg activates full closure of the Strait of Hormuz, which is no longer a theoretical threat given that tracked transits above 10,000 deadweight tonnage have fallen to near zero since July 7. Mona Yacoubian of the United States Institute of Peace assessed the IRGC’s operational posture as rejecting calibrated responses in favour of “unbridled escalation,” a characterisation that the corps validated within forty-eight hours by hitting US installations in four countries — Kuwait, Bahrain, Jordan, and Qatar — in the most geographically dispersed Iranian offensive operation of the conflict.

Against this threat, the kingdom’s air defences are operating from a stockpile that cannot hold. Saudi Arabia has approximately 400 PAC-3 interceptor rounds remaining from a pre-war supply of 2,800 — an 86 percent depletion rate with no resupply expected until 2030 at the earliest, according to assessments confirmed across prior reporting. The sole supplementary system is a single Greek ELDYSA Patriot battery positioned near Yanbu with a deployment commitment extending only through November 2026. Washington has weighed punitive drawdown from Prince Sultan Air Base as leverage over the kingdom’s Operation Project Freedom, which means the interceptors Saudi Arabia depends on are themselves a coercive instrument rather than a guaranteed shield.

The arithmetic runs in one direction. Iran struck four countries in forty-eight hours between July 8 and 9, firing at least ten missiles at Jordan’s Muwaffaq Salti Air Base and destroying a $15 million AN/GSC-52B satellite communications dish at Al Udeid in Qatar — the first Iranian strike on Qatari territory since the crisis began. If the IRGC applies its 2:1 ratio to the July 7–8 package alone — more than 80 strikes, as detailed above — the implied retaliatory volume already exceeds 160 strikes, a number that would consume a large fraction of the kingdom’s remaining interceptors even before Saudi Arabia became the primary target. The Zolfaghar’s 700-kilometre range covers Ras Tanura comfortably from launch sites in southern Iran, and the Fattah-2 at 1,400 to 1,500 kilometres reaches every Saudi facility from positions deep in Iran’s interior, well beyond any Saudi counterstrike capability.

What Happens When Retaliation Reaches Ras Tanura?

A salvo against Ras Tanura does not need to penetrate the facility to shut it. The March 2 strike demonstrated that: intercepted drones still dropped debris that triggered a fire shutting refinery operations for weeks. A larger salvo — even one partially stopped — would produce worse outcomes at a terminal where crude, condensate, and refined product sit in close proximity. And both halves of the Saudi export equation are reachable: the April Petroline pumping station strike showed the IRGC can degrade Gulf-facing terminals and the Red Sea bypass in the same operational cycle.

“America still hasn’t learned that bullying and breaking promises are no longer cost-free. Let me put it plainly: If you strike, you’ll get hit.”

Mohammad Bagher Ghalibaf, Speaker of Iran’s Parliament, CNN live blog, July 7, 2026

Ghalibaf directed the threat at Washington, but the targets his IRGC has named are overwhelmingly Saudi and Gulf-state infrastructure — a distinction that captures the central asymmetry of the Kharg question. The United States strikes Iranian facilities and absorbs retaliatory fire at regional bases where it has depth, rotation capacity, and logistics to sustain operations; Saudi Arabia absorbs retaliatory fire at oil terminals where a single successful strike can shut loading for weeks and where the alternative routing through Yanbu is already at its physical maximum. The gap between ambition and capability is measured in interceptors that do not regenerate, and every Kharg escalation that draws IRGC fire toward Saudi infrastructure is a drawdown on a stockpile that Washington has used as leverage, not as an alliance commitment.

The Tanker War in Reverse

There is a painful historical echo in the Kharg crisis, and it runs in the wrong direction for Riyadh. Between 1984 and 1988, Iraq attacked Kharg Island repeatedly during the Iran-Iraq War, attempting to sever the same crude export artery that CENTCOM struck in July 2026. Iran responded by running shuttle tankers to Sirri Island further south in the Gulf, maintaining reduced but continuous exports under sustained bombardment, while retaliating against tanker traffic serving Iraq’s Gulf allies. Roughly 400 ships were damaged or destroyed and some 600 crew were killed or wounded across the broader Tanker War, according to Britannica and the Naval History and Heritage Command’s H-Gram 018 assessment.

The United States intervened with Operation Earnest Will from July 1987 to September 1988 — the largest naval convoy operation since the Second World War — escorting Kuwaiti tankers reflagged under the American flag through the Strait of Hormuz. Saudi Arabia was the quiet beneficiary. The kingdom had provided Iraq between $25 and $50 billion in financial aid during the Iran-Iraq War, according to the Strauss Center and Britannica, making it a de facto party to a conflict it publicly stayed out of while the US Navy absorbed the operational risk of keeping Gulf shipping lanes open. Washington protected Gulf oil exports from Iranian retaliation, and Saudi Arabia shipped its crude under that umbrella without assuming direct exposure.

The 2026 inversion is almost exact in structure but reversed in its implications. The United States is no longer protecting Gulf shipping from Iran; it is destroying Iran’s primary export facility, and the retaliation that follows runs directly toward the same Saudi loading terminals that Earnest Will was designed to shield. Riyadh’s role has flipped from protected bystander to exposed beneficiary — a country that profits from the destruction of Kharg while sitting in the path of the response, with Hormuz carrying 34 million barrels on state fleets and dark tankers that no escort operation can track or protect.

The Silence That Isn’t Neutral

Saudi Arabia’s diplomatic position on the Kharg escalation is defined entirely by absence. The kingdom holds no seat at the Switzerland talks where the MOU was negotiated, no role in the Islamabad implementation track where the next round opens July 11, and no observer status at the table where the future of Kharg — whether it remains a military target, becomes a seizure, or triggers a blockade — will effectively be decided. Riyadh’s sole informational pipeline into the process, as Al Jazeera reported on June 21, is FM Dar’s briefings to FM Faisal — a secondhand channel from a mediator country, Pakistan, whose co-mediator Qatar has established back-channel contact with Iran that explicitly excludes Riyadh.

The kingdom’s silence on Trump’s Kharg seizure threat is not strategic ambiguity. It is the posture of a government that has no good option and no mechanism to influence the outcome. Endorsing the strike or seizure activates the 2:1 doctrine against Saudi infrastructure. Opposing it publicly fractures the US relationship at the precise moment when PAC-3 resupply and the Reema-Rubio ambassador-level meeting represent the only active thread of US-Saudi contact. And expressing no position does not insulate the kingdom from retaliation: the IRGC targets infrastructure based on geographic proximity and American corporate presence, not on diplomatic statements from host governments.

Princess Reema met Rubio, but Faisal did not, and the channel between Riyadh and Washington runs at ambassador level — containment, not coordination — on a question where the next escalatory step would reorder the structure of Gulf oil exports for a generation. The July 11 Islamabad session will determine whether Kharg stays a pressure point or becomes the pretext for permanent restructuring of the strait, and Saudi Arabia’s exposure to that outcome — fiscal, physical, diplomatic — is total, while its influence runs through a single secondhand briefing from a foreign minister in Islamabad who has his own agenda to manage.

Frequently Asked Questions

Could the United States actually seize and hold Kharg Island?

Kharg sits roughly 100 kilometres from Iran’s Faw Peninsula and 25 kilometres from the mainland coast at its nearest point, which means any garrison force would operate within range of Iran’s coastal defence cruise missiles and IRGC naval fast-attack craft without a deep defensive perimeter. During the Iran-Iraq War, Iran maintained control of Kharg despite years of sustained Iraqi air attack specifically because the island’s proximity to the mainland allowed continuous resupply and reinforcement — a US seizure force would face the mirror image of that problem, sustaining an isolated garrison against an adversary with extensive anti-ship and coastal missile batteries across a narrow waterway. The logistical requirements — layered air defence, sea-lane protection, continuous supply — would likely demand a carrier strike group on permanent station, a commitment the Navy has not sustained in the Gulf since drawing down the dual-carrier posture in 2023.

Has Kharg Island been attacked before, and what happened to Iran’s exports?

Iraq struck Kharg repeatedly from 1984 onward, initially with Exocet-armed Super Étendard aircraft and later with Tu-22 bombers carrying conventional gravity bombs. Iran absorbed the damage by running a shuttle-tanker system: smaller vessels loaded at Kharg during pauses between attacks, ferried crude to Sirri Island further south in the Gulf, and transferred it to larger tankers outside the Iraqi strike envelope. At its lowest operational point, Kharg throughput fell to approximately 500,000 bpd from a pre-war baseline of roughly 1.5 million — reduced by two-thirds but never fully severed, even under sustained bombardment over four years, which suggests that destroying Kharg’s export capacity requires sustained repeated strikes over months rather than a single retaliatory package.

What would prolonged Kharg closure mean for China?

China is Iran’s largest remaining crude customer, purchasing an estimated 1.2 to 1.5 million barrels per day through a mix of direct contracts and intermediary traders, much of it carried on “dark fleet” tankers operating with transponders off. A prolonged Kharg closure would force Beijing to source replacement barrels from other producers — primarily Saudi Arabia, the UAE, Iraq, and Russia — at higher prices and in competition with other importers scrambling for the same supply. Sinopec, China’s largest refiner, has already made zero purchases of Saudi crude for two consecutive months, a commercial signal suggesting Beijing is not preparing for closer Saudi energy ties despite the supply disruption; China’s strategic petroleum reserve, estimated at roughly 950 million barrels, provides approximately 80 to 90 days of import coverage at current consumption rates.

How long can Aramco sustain its dividend at current oil prices?

At the Q1 2026 coverage ratio of 0.85x — spending $21.89 billion per quarter on dividends against $18.6 billion in free cash flow — Aramco depletes approximately $3.3 billion in cash reserves each quarter. With reserves at $53.3 billion, the company could mathematically sustain the gap for roughly four years at the current burn rate, but this ignores capital expenditure obligations, minimum operating reserves, and the likelihood that continued below-breakeven pricing compresses FCF further. If Brent averages the EIA’s forecast of $65 per barrel in 2027, coverage could drop below 0.70x, accelerating the drawdown and raising the prospect of the first Aramco dividend reduction since the 2019 IPO — an event that would ripple directly through PIF’s funding model, given that Aramco dividend income is the sovereign wealth fund’s primary revenue stream for Vision 2030 projects.

What is the Persian Gulf Security Accord and how does it connect to Kharg?

The PGSA is the Iran-proposed maritime security framework that would impose transit fees and classification requirements on all vessels passing through the Strait of Hormuz, with an outstanding balance of approximately $253 million accumulating at $5.5 million per day toward an August 18 deadline. The accord’s relevance to Kharg is structural: if Kharg is permanently seized or blockaded, Iran’s incentive to enforce the PGSA escalates from revenue collection to full strait closure, because the friendly-nation carve-out system Beijing negotiated only functions while Iran controls Kharg and has an economic interest in keeping partial Gulf traffic flowing. Remove Kharg revenue, and Tehran’s cost of full Hormuz closure — already low given near-zero tracked transits — drops to near zero, while the coercive value of closure rises

MBS addressed the fiscal exposure directly in his July 11 call with Trump — the first leader-to-leader contact since the war re-escalated — deploying a maritime navigation formula that reads as a hedge against both full Hormuz closure and unilateral US escort operations that could trigger the IRGC’s 2:1 doctrine. The three readings the SPA readout was engineered to sustain are examined in MBS Told Trump What Riyadh Would Allow in the Gulf — In One Sentence.

as the kingdom’s only way to export above the Petroline ceiling requires Gulf-facing terminals that a closed strait would render unreachable.