Saudi Arabia’s Yanbu Bypass Is About to Lose the Only Strait That Made It Work

DHAHRAN — The architecture that was supposed to keep Saudi oil flowing while the United States blockaded Iran has a second chokepoint, and Iran just told the world it has not yet decided to close it. On April 26, Parliament Speaker Mohammad Bagher Ghalibaf — former IRGC Aerospace Force commander, the man who publicly validated the IRGC’s override of Foreign Minister Araghchi’s Hormuz declaration — posted an equation on X that read like a cost ledger: “SOH (partly played) + BEM (unplayed) + Pipelines (unplayed) = Inv Release (played) + Demand Destruction (partly played) + More Price Adj (to come).” BEM is Bab el-Mandeb. “Unplayed” is not a denial. It is a price tag that has not yet been presented.

Two days later, President Trump told aides to prepare for an “extended US naval blockade” and the National Security Council began developing military-options packages for targeting IRGC fast-attack boats, minelaying vessels, and asymmetric naval assets around the Strait of Hormuz. Iran rejected Trump’s proposal to separate nuclear talks from Hormuz reopening on April 28. The dual-chokepoint loop is closing, and the country absorbing its structural consequences is Saudi Arabia — which is producing 7.25 million barrels per day, bleeding revenue against a PIF-inclusive fiscal break-even of $108–111 per barrel, and watching its sole remaining export bypass route come under explicit threat from the same Iranian leadership that already shut down Hormuz. The structural logic of the two-chokepoint trap constraining Saudi Arabia explains why Riyadh cannot endorse Project Freedom even as it benefits from it.

Table of Contents

- The Bypass That Justified the Blockade

- What Does Ghalibaf’s “BEM Unplayed” Equation Mean for Saudi Exports?

- Trump’s “Long Blockade” and the NSC Targeting Package

- Why Can’t Yanbu Handle More Than 5.9 Million Barrels Per Day?

- The SUMED Ceiling and the Cape of Good Hope Problem

- How Much Is Saudi Arabia Losing at 7.25 Million Barrels Per Day?

- The April 14 Diplomatic Break

- The Trap Neither Side Designed

- FAQ

The Bypass That Justified the Blockade

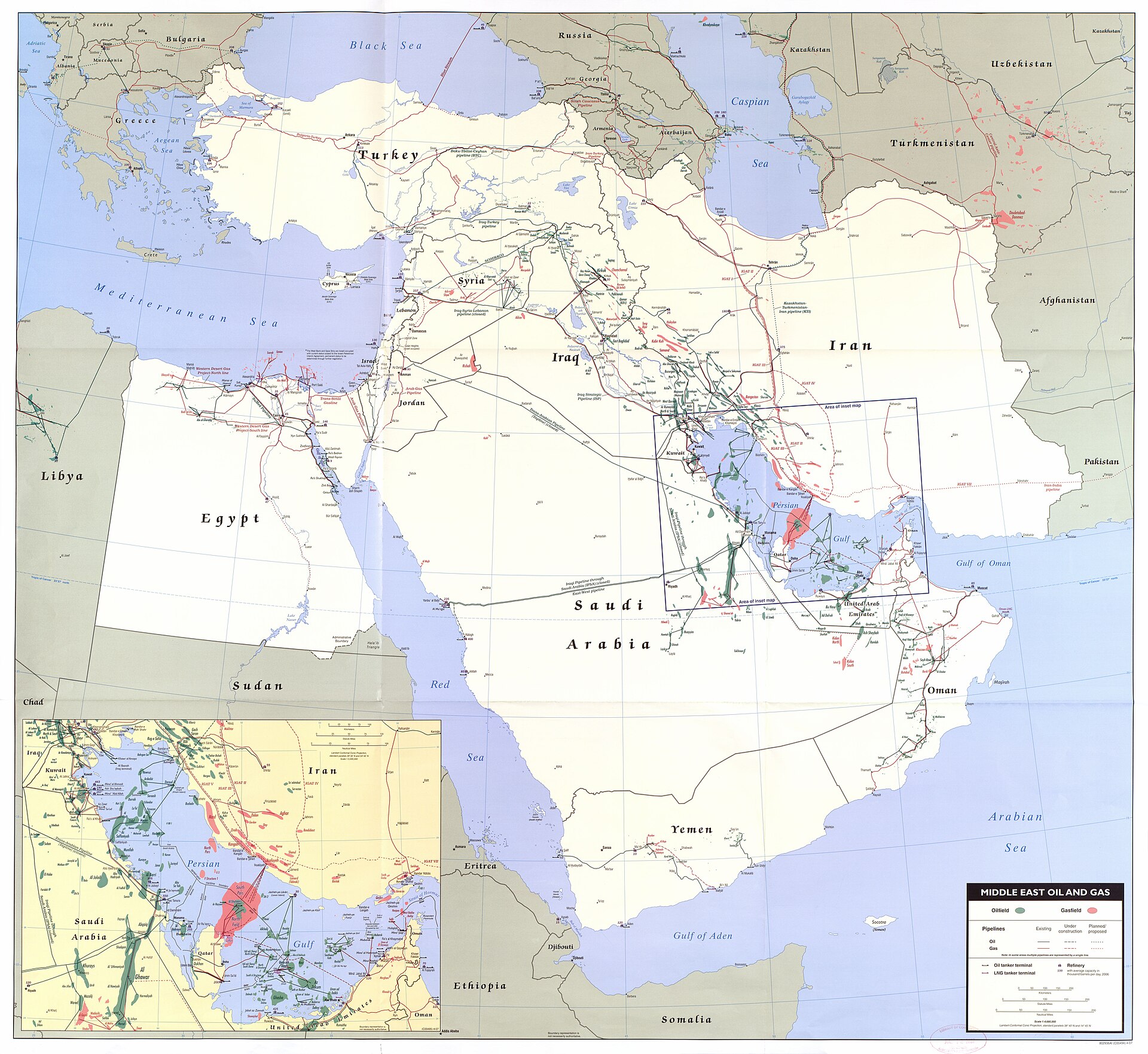

The US naval blockade of Iranian ports, effective since April 13, rested on an implicit premise: that Saudi Arabia could continue exporting enough crude to prevent a catastrophic global supply shock while Iran was squeezed. The mechanism was the East-West Pipeline — the Petroline, built in 1981 as a Hormuz bypass, expanded through the 1990s, and upgraded to a theoretical 7 million barrels per day with NGL-to-crude conversion in 2023–24. Crude would flow west across the kingdom to Yanbu on the Red Sea, load onto tankers, and reach global markets without passing through Hormuz.

James M. Lindsay of the Council on Foreign Relations articulated this assumption on April 13, the day the blockade took effect: “Saudi Arabia and UAE can get some oil out with pipelines that bypass the critical waterway, but much of the crude remains trapped in the Persian Gulf.” The qualifier — “some oil” — was generous. The real number is worse than Washington acknowledged.

Yanbu’s effective loading capacity is 4 to 5.9 million barrels per day. The pipeline can deliver 7 million bpd. The terminal cannot load it. A brief surge to 5 million bpd was achieved in late March; the sustained operational ceiling sits closer to 4 million bpd. This gap — between pipeline throughput and terminal handling — had never mattered before because Saudi Arabia had never needed to route more than 3 to 4 million bpd through Yanbu in peacetime. The war exposed a bottleneck that existed on paper but had never been stress-tested at scale. Saudi production fell from 10.4 million bpd in February to 7.25 million bpd in March — a 30 percent collapse — and even that reduced volume exceeds what Yanbu can load.

But the bypass route had one feature that made the numbers tolerable: it avoided Hormuz entirely. Tankers loading at Yanbu entered the Red Sea, passed south through Bab el-Mandeb, and reached Asian buyers. For Europe-bound crude, the route ran north to Egypt’s Sidi Kerir terminal and the SUMED pipeline. Both paths worked — as long as Bab el-Mandeb stayed open.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

What Does Ghalibaf’s “BEM Unplayed” Equation Mean for Saudi Exports?

Ghalibaf’s April 26–27 post was not commentary. It was a targeting document in cost-accounting syntax. The equation separated Iran’s coercive instruments into played, partly played, and unplayed categories — and assigned Bab el-Mandeb and “Pipelines” to the unplayed column. The structure is a ledger: on the left, coercive tools available to Iran; on the right, damage already inflicted on the adversary. “More Price Adj (to come)” is the balance due.

Three Iranian officials of escalating seniority had laid the doctrinal foundation before Ghalibaf operationalized the timeline. Alaaeddin Boroujerdi, deputy head of Iran’s National Security Committee, told Al Jazeera on April 6–7: “The importance of Bab el-Mandeb may be no less than that of the Strait of Hormuz… We have not yet revealed our new cards.” Ali Akbar Velayati — senior adviser to the Supreme Leader, foreign minister from 1981 to 1997, a man whose statements carry near-doctrinal weight — went further on April 20 via PressTV: “The unified command of the Resistance front views Bab al-Mandeb as it does Hormuz… If the White House dares to repeat its foolish mistakes, it will soon realize that the flow of global energy and trade can be disrupted with a single move.”

The escalation ladder is visible. Boroujerdi named the card. Velayati equated it doctrinally with Hormuz. Ghalibaf — who formally linked Hormuz reopening to US blockade removal on April 22 — placed it into a coercive ledger as a held asset with a declared activation logic. The notation “unplayed” is more threatening than activation would be. A closed Bab el-Mandeb is a known problem with known costs. An unplayed Bab el-Mandeb is a conditional threat that suppresses decision-making across every shipping desk, insurance underwriter, and treasury department in the Gulf.

An unnamed Tasnim military source made the trigger condition explicit: “If the Americans intend to take action regarding the Strait of Hormuz, they should be careful not to add another strait to their challenges.” IRGC messaging on April 19 listed Yanbu as a target alongside Bab el-Mandeb and Fujairah — a three-node interdiction map covering Saudi Arabia’s export infrastructure from loading terminal to transit chokepoint to destination port.

Trump’s “Long Blockade” and the NSC Targeting Package

On April 23, Trump ordered the US Navy to “shoot and kill” any Iranian boat laying mines in the Strait of Hormuz. “There is to be no hesitation,” he said, per Time and Al Jazeera. The instruction accompanied an NSC directive for the military to develop “dynamic targeting” plans for IRGC fast-attack boats, minelaying vessels, and asymmetric assets across the Strait and Gulf of Oman. By April 27–28, Trump had told aides to prepare for an “extended US naval blockade” — what internal planning documents reportedly term the “long blockade” — and rejected Iran’s proposal to decouple nuclear negotiations from Hormuz reopening.

The IRGC Navy retains approximately 60 percent of its pre-war assets intact, including the fast-attack speedboat fleet that constitutes its primary asymmetric capability. Forty-five total transits have passed through Hormuz since the April 8 ceasefire — 3.6 percent of the pre-war baseline. The cumulative supply deficit since February 28 stands at roughly 700 million barrels.

Tasnim News, aligned with the IRGC, responded with a statement that functions as a conditional threat: “The continuation of the naval blockade amounts to continued hostilities. Iran will not reopen the Strait of Hormuz as long as the blockade persists and, if necessary, will break the blockade by force.” Iran’s formal position, reinforced by the rejection of Trump’s April 28 proposal, is that Hormuz and the blockade are a single negotiating package — they open and close together, or not at all.

This is where the dual-chokepoint logic locks into place. Trump’s “shoot and kill” order and NSC targeting package are precisely the kind of US military action that Tasnim’s unnamed source conditioned Bab el-Mandeb activation on. The “long blockade” directive extends the timeline. The targeting package raises the kinetic threshold. Each escalation on Hormuz increases the probability that Bab el-Mandeb moves from Ghalibaf’s “unplayed” column to “partly played.” And the country whose export architecture depends on Bab el-Mandeb remaining open was not consulted on either directive. The pattern continued on April 29, when Trump posted an AI assault rifle image warning Iran “NO MORE MR. NICE GUY” within hours of Tehran formally asserting legal authority over Hormuz — adding yet another escalation node that the country whose bypass route depends on Bab el-Mandeb had no voice in.

Why Can’t Yanbu Handle More Than 5.9 Million Barrels Per Day?

The East-West Pipeline’s 7 million bpd theoretical capacity is a pipeline number, not a terminal number. Yanbu’s loading infrastructure — berths, storage tanks, pumping stations, and vessel scheduling — was designed for a world in which the pipeline served as a supplement to Hormuz, not a replacement. The terminal was built to handle 3 to 4 million bpd of routine bypass traffic. The 2023–24 pipeline upgrade expanded what could be pushed through the pipe. It did not expand what could be loaded onto ships at the other end.

The gap between 7 million bpd of pipeline capacity and 4 to 5.9 million bpd of terminal capacity is an infrastructure problem that takes years to solve. New berths require dredging, environmental assessment, and construction timelines measured in quarters, not weeks. Storage tank expansion requires land allocation and steel. None of this was underway when the war began on February 28, because no scenario in Saudi energy planning assumed that Hormuz would close, the Eastern Province terminals would go offline, and the entire kingdom’s export volume would need to pass through a single Red Sea port simultaneously.

At Saudi Arabia’s current production of 7.25 million bpd, even the optimistic Yanbu ceiling of 5.9 million bpd leaves 1.35 million bpd stranded — crude that is produced but cannot be exported. The realistic sustained ceiling of 4 million bpd leaves 3.25 million bpd without an outlet. OPEC+ quota for April stands at 10.2 million bpd — 3 million above actual output. The kingdom is not cutting voluntarily. It is physically unable to move its own oil. Iran faces a mirror constraint from the opposite side of the ledger: with 12–22 days of storage headroom remaining at Kharg Island and Qingdao Haiye now sanctioned by the US, Tehran’s ability to keep pumping without an export outlet is running out of runway at roughly the same pace as Saudi Arabia’s ability to keep exporting without Hormuz.

The SUMED Ceiling and the Cape of Good Hope Problem

If Bab el-Mandeb closes, Yanbu-loaded tankers heading to Asia — Saudi Arabia’s largest crude market, where the region imported 14.74 million bpd of Middle Eastern crude in 2025 — must reroute around the Cape of Good Hope. That adds 10 to 14 days of transit time and $1.2 to $1.8 million per round trip (as of Q1 2026). For Europe-bound crude, there is an alternative: tankers can sail north from Yanbu to Egypt’s Sidi Kerir terminal and enter the SUMED pipeline, which crosses Egypt to the Mediterranean. SUMED handles approximately 2.4 million bpd — less than half of Yanbu’s reduced throughput.

The arithmetic is unyielding. At a Yanbu loading rate of 4 to 5 million bpd, with SUMED absorbing 2.4 million bpd for European delivery, the remaining 1.6 to 2.6 million bpd must transit Bab el-Mandeb to reach Asian buyers. If the strait closes, that volume either reroutes via the Cape — adding cost and delay that compress margins against a $108–111 break-even — or it does not move at all.

A combined Hormuz and Bab el-Mandeb disruption places an estimated $10 billion per day of global trade at risk, blocking roughly 22 percent of global oil supply and 30 percent of global container shipping, according to the Observer Research Foundation’s dual-chokepoint analysis. The 1973 Bab el-Mandeb closure — when Egyptian and South Yemeni warships blocked Israeli-bound tankers during the Yom Kippur War — lasted weeks before Kissinger’s intervention reopened traffic by November 18. That closure was partial, state-conducted, and dependent on conventional naval assets. The 2026 scenario involves Houthi forces with drone and missile capabilities that make selective denial far cheaper and more durable than anything available in 1973. Houthi forces have already declared “Hour Zero” for renewed Bab el-Mandeb blockade operations.

How Much Is Saudi Arabia Losing at 7.25 Million Barrels Per Day?

Brent crude hit $114.64 per barrel on April 29, having breached $115 overnight on April 28–29. The price sounds like a windfall. It is not.

Saudi Arabia’s fiscal break-even is not the IMF’s central-government figure of $86.60 per barrel. That number excludes the Public Investment Fund’s spending — the $925 billion sovereign wealth vehicle driving NEOM, The Line, the Red Sea tourism project, and the broader Vision 2030 capital program. Bloomberg Economics puts the PIF-inclusive break-even at $94 per barrel. Goldman Sachs places it at $108 to $111. Farouk Soussa, Goldman’s MENA economist, calculated a war-adjusted fiscal deficit of 6.6 percent of GDP — double the official 3.3 percent forecast.

At 7.25 million bpd and $115 Brent, the kingdom’s gross revenue is approximately $834 million per day. At 10.4 million bpd — the February baseline — the same price would yield $1.196 billion per day. The volume collapse costs Saudi Arabia roughly $362 million per day in foregone revenue, even at the highest sustained crude price since 2022. At the PIF-inclusive break-even of $108–111, the margin above break-even is $4 to $7 per barrel — which on 7.25 million bpd generates $29 to $51 million per day of fiscal surplus. Before the war, with 10.4 million bpd and Brent at $75–80, the margin per barrel was thinner but the volume generated comparable total revenue. The price is higher, and the kingdom is poorer. When Project Freedom’s first Hormuz convoy completed on May 4, Brent fell to $107.80 — at or below the $108–111 PIF-inclusive break-even, confirming that market optimism about the convoy’s symbolic success directly compresses the fiscal margin Saudi Arabia needs to sustain Vision 2030 commitments.

The 6.6 percent GDP deficit figure assumes current production levels and prevailing prices. If Bab el-Mandeb closes and Yanbu throughput compresses further — or if Cape routing costs absorb the $4–7 per barrel margin — the deficit widens. The IEA described the supply disruption as the “largest on record.” Asia’s Middle Eastern crude imports fell 38.6 percent in the period tracked by Kpler.

The April 14 Diplomatic Break

On April 14, Saudi Arabia publicly called for negotiations and an end to the Hormuz blockade — what Crisis Group described as “the most significant diplomatic break by a US ally since the conflict began.” The statement was calibrated. It did not name Trump. It did not endorse Iran’s position. It called for an end to the blockade, which amounts to the same thing without the diplomatic cost of attribution.

The break came one day after the US blockade took effect. It preceded Ghalibaf’s “BEM unplayed” post by twelve days. It preceded Trump’s “shoot and kill” order by nine days and the “long blockade” directive by thirteen. Each subsequent escalation has widened the gap between Riyadh’s stated position and Washington’s operational trajectory.

RAND’s Raphael S. Cohen observed that Saudi Arabia, the UAE, Bahrain, and Kuwait are all pushing the United States to keep fighting until Iran is “decisively defeated,” even as they absorb collateral economic damage. The framing captures the public posture but misses the private arithmetic. Saudi Arabia cannot simultaneously call for an end to the blockade (April 14) and push for decisive defeat. The April 14 statement was the moment Riyadh’s private calculus broke through the public alignment. The kingdom’s parallel diplomatic track on Hormuz operates on a timeline measured in months. The NSC targeting package operates on a timeline measured in days.

The Trap Neither Side Designed

Trump and Iran are not in opposing escalatory cycles. They are in a mutually reinforcing loop. Trump’s “long blockade” directive makes Hormuz reopening conditional on Iranian capitulation across multiple domains — nuclear, maritime, and military. Iran’s refusal to separate those domains, confirmed by the April 28 rejection, makes the blockade permanent until either side breaks. The April 30 CENTCOM briefing on Hormuz seizure options — and the Saudi basing commitments every option requires but Riyadh has not provided — are examined in Trump’s 45-Minute Hormuz Briefing and Saudi Arabia’s Indispensability Trap.

The “shoot and kill” order and NSC targeting package raise the kinetic threshold on Hormuz. Iran’s declared response to US kinetic action on Hormuz is Bab el-Mandeb activation. US military action designed to break the Hormuz stalemate triggers the closure of the strait that the US blockade strategy depends on staying open.

Neither government designed this trap for Saudi Arabia. Washington’s blockade strategy treated Saudi export bypass capacity as an adequate cushion. Iran’s dual-chokepoint doctrine treats Bab el-Mandeb as a coercive reserve against US escalation, not as an instrument aimed at Riyadh. But the geometry is indifferent to intent. Saudi crude loads at Yanbu. It exits via Bab el-Mandeb. The Houthi dual-vessel attack demonstrated that the strait is already contested. Ghalibaf’s ledger confirmed it is held in reserve as a deliberate instrument of coercive escalation.

The IRGC’s selective licensing of Hormuz transits — 45 since the April 8 ceasefire — has already established a permissions-based chokepoint regime. If that model extends to Bab el-Mandeb through Houthi proxies, Saudi crude becomes subject to two separate toll authorities that Riyadh has no ability to negotiate with directly, no military capacity to challenge independently, and no diplomatic framework to bypass.

MBS cannot publicly name this exposure. Doing so would validate Iran’s coercive architecture — confirm that the threat works, that the held card has value, that the “unplayed” notation in Ghalibaf’s ledger represents real power over Saudi fiscal outcomes. The April 14 diplomatic break was the closest Riyadh has come to saying so. Each week since, the production collapse has deepened, Yanbu’s ceiling has held, the SUMED bottleneck has not widened, and Ghalibaf’s ledger has acquired two more entries on the played side.

Dual-Chokepoint Exposure: Saudi Export Architecture Under Threat

| Metric | Value | Source |

|---|---|---|

| East-West Pipeline capacity (theoretical) | 7M bpd | Pipeline Technology Journal |

| Yanbu loading capacity (effective) | 4–5.9M bpd | Lloyd’s List / Arab News |

| SUMED pipeline capacity | ~2.4M bpd | EIA |

| Saudi March production | 7.25M bpd | IEA |

| Saudi February production | 10.4M bpd | IEA |

| PIF-inclusive fiscal break-even | $108–111/bbl | Goldman Sachs / Bloomberg Economics |

| Brent crude (April 29) | $114.64/bbl | Fortune / CNBC |

| Hormuz transits since April 8 ceasefire | 45 (3.6% of baseline) | Bloomberg |

| Cumulative supply deficit since Feb 28 | ~700M barrels | Tehran Times |

| IRGC Navy assets intact | ~60% | National Security News |

| Global trade at risk (dual closure) | $10B/day | ORF |

| Asia Middle East crude imports (2025) | 14.74M bpd | ORF / CSIS |

| Cape of Good Hope reroute cost (as of Q1 2026) | $1.2–1.8M per round trip | Lloyd’s List |

| Cape reroute added transit time | 10–14 days | Lloyd’s List |

FAQ

Could Saudi Arabia expand Yanbu’s loading capacity fast enough to close the terminal gap?

No. Terminal expansion at Yanbu requires new berths (dredging, environmental review, marine construction), additional storage tanks, and upgraded pumping infrastructure. Minimum timelines for such projects run 18 to 24 months from approval to first oil loaded — assuming contractor availability, which is constrained by the same war disrupting shipping lanes. The terminal was designed as a supplementary bypass, not a primary export node.

Has Bab el-Mandeb ever been fully closed to commercial shipping?

No. The 1973 partial closure during the Yom Kippur War involved Egyptian and South Yemeni conventional naval assets blocking Israeli-bound tankers specifically; the strait reopened within weeks under US diplomatic pressure. Houthi anti-shipping campaigns in 2023–24 degraded but did not halt traffic. A full closure would require sustained drone, missile, and mine operations across the strait’s 18-mile width — capabilities the Houthis have demonstrated individually but never combined into a total blockade. The IRGC’s April 19 messaging, which listed Yanbu alongside Bab el-Mandeb and Fujairah as a three-node interdiction target set, suggests a selective-denial model rather than full closure — mirroring the permissions-based Hormuz regime.

What happens to Saudi Vision 2030 funding if the PIF-inclusive deficit reaches Goldman’s 6.6 percent?

At 6.6 percent of GDP — approximately $66 billion on Saudi Arabia’s roughly $1 trillion nominal GDP — the deficit would force triage between PIF capital commitments and sovereign operating expenditure. PIF committed $53.4 billion in 2025 across NEOM, Qiddiya, The Red Sea, ROSHN, and other giga-projects. The fund’s domestic allocation targets were set at $40 billion annually through 2030. A sustained 6.6 percent deficit makes simultaneous giga-project capitalization and fiscal balance arithmetically impossible without new external borrowing, asset sales, or project deferrals — none of which MBS has publicly signaled.

Why can’t the US Navy protect Saudi tankers in Bab el-Mandeb while maintaining the Hormuz blockade?

Force disposition. The US has concentrated naval assets — three carrier strike groups as of late April — in the Arabian Sea and Gulf of Oman to enforce the Iranian blockade and support potential kinetic operations against IRGC assets. Bab el-Mandeb is 1,400 nautical miles from the Strait of Hormuz. Escorting Saudi tankers through Bab el-Mandeb while simultaneously enforcing the Hormuz blockade and preparing for IRGC fast-attack engagement requires splitting already-extended forces across two theaters. Operation Prosperity Guardian, the 2023–24 Bab el-Mandeb convoy escort mission, required dedicated destroyer and frigate rotations that are now committed to the Hormuz theater. The Pentagon has not announced any Bab el-Mandeb force posture adjustment.