DHAHRAN — Saudi Aramco cut the Official Selling Price for Arab Light crude to Asia by $0.40 per barrel for July loading, setting the premium at $3.50 above the Oman/Dubai average — the first reduction in three months and a signal that the kingdom is willing to sacrifice revenue to prevent Asian buyers from locking in long-term contracts with rival suppliers.

The cut will cost Aramco approximately $51-60 million per month in foregone revenue at current Yanbu throughput, according to HouseofsauD estimates based on terminal loading data. It arrives while Saudi production sits 23.2% below its February level, the kingdom operates below the $108-111 per barrel fiscal break-even that Bloomberg Economics calculates when PIF spending obligations are included, and Aramco has no spare barrels to offer — a pricing concession without a volume promise, paid at a moment when Goldman Sachs projects the kingdom’s war-adjusted fiscal deficit at $80-90 billion against an official budget gap of $44 billion.

Table of Contents

The $0.40 Cut in Context

The July OSP of +$3.50 per barrel above Oman/Dubai continues a rapid unwinding of the war premium that peaked in May at +$19.50 — set on April 6 when Brent traded near $109. That May premium was the largest single-month OSP increase on record, eclipsing the prior record of +$4.40 set in April 2022 during the post-Ukraine supply panic. The June OSP had already fallen to +$3.90, a $15.60 collapse in one announcement cycle.

Aramco’s OSP sets the pricing trend for approximately 9 million barrels per day of Gulf crude bound for Asia, according to Reuters. A $0.40 move ripples through every term contract between the Persian Gulf and Yokohama. Clyde Russell, Reuters’ commodity columnist, characterized Aramco’s OSP philosophy as “just enough to stay competitive” — deliberately following market dynamics rather than slashing aggressively.

Brent closed at $105.33 on April 25, still elevated by war disruption but below the $108-111 fiscal break-even — meaning every OSP cut that holds Brent near current levels deepens the treasury shortfall rather than alleviating it. Goldman Sachs’s 6.6% GDP war-adjusted deficit projection gives the government limited tolerance for further concessions.

Why Is Saudi Arabia Discounting Oil It Cannot Ship?

Saudi crude production fell to 7.763 million bpd in March, down from 10.111 million bpd in February — a decline of 2.348 million bpd, or 23.2%, according to CEIC and Trading Economics data. The OPEC+ quota stands at 10.2 million bpd, leaving Saudi Arabia 2.44 million bpd below its own allocated ceiling.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

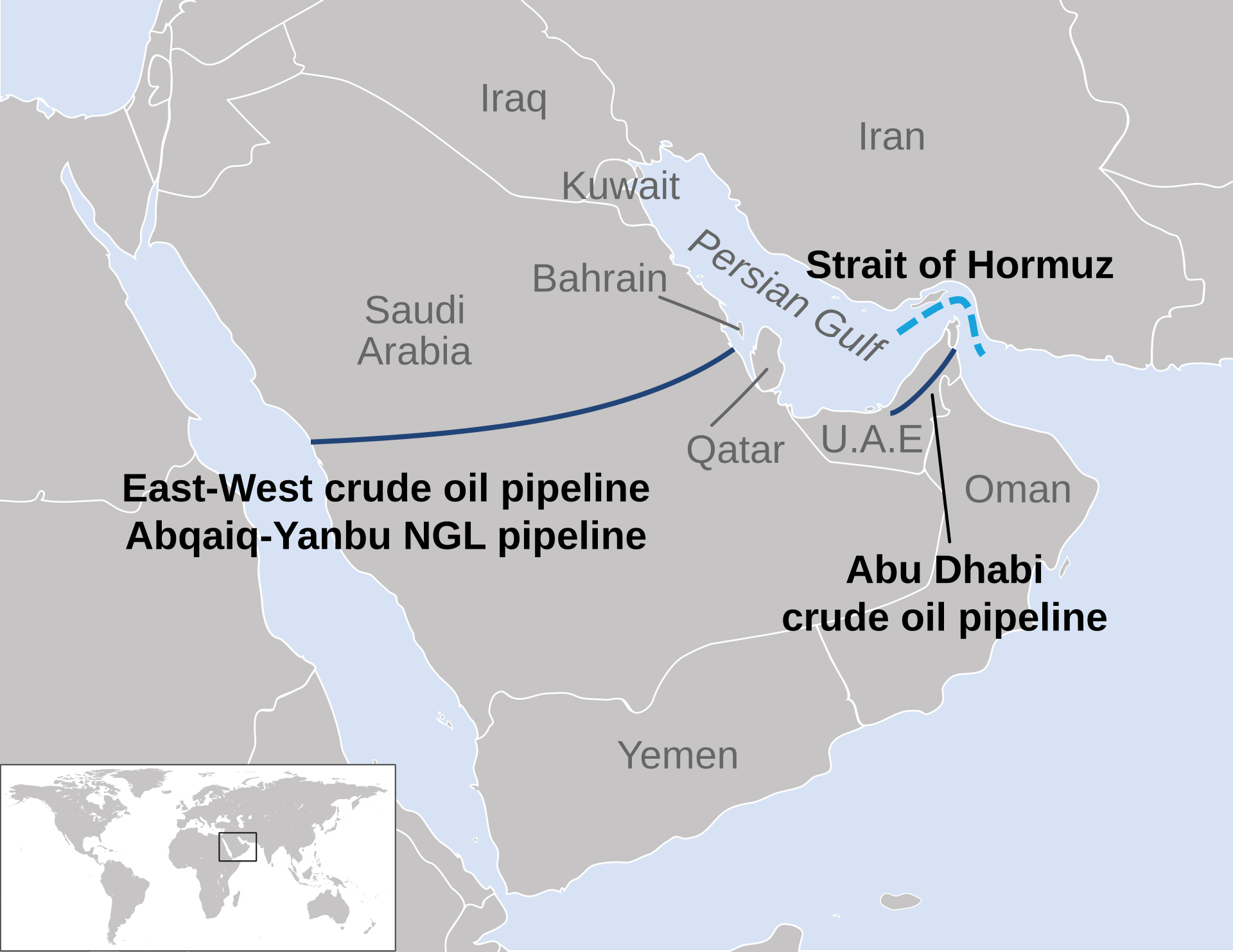

The constraint is not underground. Amin Nasser, Aramco’s CEO, has said the company can ramp production “in days” once the Strait of Hormuz is cleared. The constraint is at Yanbu, the Red Sea terminal that became Saudi Arabia’s sole major export outlet after the functional closure of Hormuz. The East-West Pipeline feeding Yanbu has a practical throughput ceiling of 4.0-4.5 million bpd — enough to move 56-63% of pre-war Asian export volumes.

Saudi crude exports to Asia fell 38.6% in March, from 7.108 million bpd to 4.355 million bpd, according to Kpler shipping data. The IEA called the broader disruption “the largest supply disruption in the history of the global oil market.” Russell Hardy, CEO of Vitol Group, estimated that 600-700 million barrels had already been lost to the war, with a projected total of one billion barrels.

The $0.40 cut is not a volume play. Aramco cannot fill additional tankers. It is pricing for a future in which Hormuz reopens and Saudi Arabia needs its Asian customers to have kept contract slots open rather than filled them with Russian ESPO, Iraqi Basra Light, or Iranian barrels moved through the dark fleet.

The Competitors Aramco Is Pricing Against

Russia has moved aggressively into the gap. Sinopec purchased 8-10 cargoes of ESPO blend crude from Kozmino at premiums of $8-10 per barrel above Brent, according to energynews.oedigital.com — a reversal from pre-war conditions when Russian crude typically traded $10 below Brent. China’s Russian crude imports rose 40.9% year-on-year in January-February 2026, according to Chinese customs data reported by Reuters, and Russia’s crude shipments to China reached 2.07 million bpd in April.

India has become equally dependent. Indian refiners imported 4.57 million bpd of crude in March, of which 2.14 million bpd — 47% — came from Russia, according to CNBC. In Q1 2026, 90% of Russia’s total crude exports went to China and India combined.

Iran’s dark fleet adds another layer. China absorbed 1.6 million bpd of Iranian crude in March, roughly 16% of China’s 10 million bpd in seaborne imports. The IRGC charges $2 million per VLCC for passage through its controlled 5-nautical-mile Hormuz corridor. But that channel is narrowing. Five Shandong teapot refiners stopped Iranian crude purchases in April due to compliance exposure after the expiry of OFAC General License U on April 19. Zhao Dong, president of Sinopec, told Hydrocarbon Processing in March that the company would “basically not buy” Iranian crude despite the US sanctions waiver. On April 23, Iran’s parliament confirmed that the first cash receipts from those transit fees have been deposited at the Central Bank of Iran — converting the collection mechanism from a coercive instrument into a line-item in Iran’s fiscal architecture and giving the IRGC a bureaucratic, not merely strategic, interest in maintaining corridor control.

Iraq’s position is more ambiguous. Basra Light is a direct competitor to Arab Light in Asian refinery configurations, but Iraq’s southern production has fallen over 70% since the war began. The Zubair field — normally 400,000 bpd — dropped to roughly 250,000 bpd after Iranian strikes, according to Reuters. Iraq is simultaneously a competitor Aramco must price against and a disrupted source whose lost barrels inflate the premium Aramco could theoretically charge.

| Supplier | Asia Volume (March 2026) | Price vs. Brent | Trend |

|---|---|---|---|

| Saudi Arabia (Yanbu) | 4.355M bpd (-38.6%) | +$3.50 Oman/Dubai (July) | Cutting OSP to hold contracts |

| Russia (ESPO/Kozmino) | 2.07M bpd (April) | +$8-10 above Brent | Volume rising 40.9% YoY |

| Iran (dark fleet) | 1.6M bpd to China | Discounted, $2M/VLCC transit | Shandong teapots exiting |

| Iraq (Basra Light) | Sharply reduced | Tracking Saudi OSP | Southern output down 70%+ |

Oman/Dubai Benchmark Under Strain

Aramco’s OSP is denominated as a premium to the Oman/Dubai average, but the benchmark itself is under structural strain. S&P Global Platts suspended Hormuz-loading grades from the Oman/Dubai assessment after the strait’s functional closure, removing the physical cargoes that historically anchored the benchmark to actual loading costs in the Persian Gulf.

The result is a benchmark that has become structurally more expensive for buyers than Brent-based alternatives — inflating Aramco’s effective cost to Asian refiners relative to competitors pricing off other indices. When Aramco cuts the OSP by $0.40, part of that cut is absorbed by benchmark distortion rather than flowing through as a genuine discount to buyers.

Xu Tianchen, senior economist at the Economist Intelligence Unit, told the South China Morning Post that “China has been an opportunistic oil buyer, capitalising on periods of low oil prices to fill its stockpile. Since oil prices are high and China has enough inventory, it’s likely to cut its oil purchases.” China’s strategic petroleum reserve stands at 1.2 billion barrels — 109 days of import cover — giving Beijing the buffer to wait for better terms rather than accept current prices from any supplier.

How Does Aramco Post Record Profits on 30% Less Oil?

Aramco’s Q1 2026 results illustrate the paradox at the core of the OSP cut. The company is expected to report a 57% profit surge on approximately 30% less volume, with revenue estimated at SAR 455.3 billion — up 6% year-on-year — according to Zawya and Reuters forecasts. The war premium that inflated prices more than compensated for the barrels Aramco could not ship.

But Q1 results reflect January-March pricing, when the May OSP at +$19.50 was still ahead and Brent averaged above $100. The July OSP at +$3.50 points to a different quarter. At current Yanbu throughput of roughly 4.2 million bpd and a $0.40 per barrel reduction, the monthly revenue cost is $51-60 million — manageable against Aramco’s overall revenue but painful for a government running a war-adjusted deficit that Goldman Sachs estimates at 6.6% of GDP.

The kingdom’s fiscal position explains why the cut is $0.40 and not $2.00. Saudi Arabia cannot afford to aggressively chase volume it does not have. The move is calibrated — large enough to signal intent, small enough to avoid compounding a deficit Goldman Sachs already projects at roughly double the official budget figure.

Background: OSP Trajectory Since the War Began

Before the Iran-Saudi war began on February 28, 2026, Aramco had cut the Arab Light OSP to Asia for four consecutive months — a competitive response to soft Chinese demand and rising Russian competition. The war inverted this pattern overnight. The March OSP held steady, but by April Aramco had begun building in a war premium that peaked with the May figure of +$19.50.

| Loading Month | Arab Light OSP (vs. Oman/Dubai) | Brent (approx.) | Context |

|---|---|---|---|

| January 2026 | Cut (pre-war trend) | ~$78 | Fourth consecutive cut |

| February 2026 | Cut (pre-war trend) | ~$76 | Competitive pricing |

| May 2026 | +$19.50 (record) | ~$109 | War premium peak, set April 6 |

| June 2026 | +$3.90 | ~$99 | $15.60 collapse from May |

| July 2026 | +$3.50 | ~$105 | First cut in three months |

The May 2022 episode offers a partial precedent. Saudi Arabia cut the June 2022 OSP for Asia by more than 50% — from +$9.35 to +$4.40 — because China’s COVID-Zero lockdowns had destroyed demand even as Brent held at $112. But in 2022, Aramco had full production capacity and open shipping lanes. The cut was backed by available barrels.

The 2020 price war provides the opposite precedent. In March 2020, Saudi Arabia slashed OSPs by $6-8 per barrel across all regions as part of a deliberate market-share offensive, simultaneously surging production to 12.3 million bpd. The 2026 cut accompanies a 23% production collapse. There is no surge behind the signal.

Saudi Arabia has been lobbying Washington to lift the US naval blockade that, combined with Hormuz’s functional closure, has compressed the kingdom’s export options to a single Red Sea corridor. At current Yanbu throughput of 4.0-4.5 million bpd, Saudi Arabia is moving roughly 3 million bpd less than its pre-war Asian export level — volume that Russian, Iranian, and West African suppliers are filling under long-term and spot arrangements.

Frequently Asked Questions

What is the Official Selling Price and who sets it?

The OSP is a monthly price differential set by Saudi Aramco for each crude grade, denominated as a premium or discount to a regional benchmark — Oman/Dubai for Asia, ICE Brent for Europe, and ASCI for the US. Aramco announces OSPs in the first week of each month for loading the following month. The pricing committee factors in refining margins, freight rates, competitor pricing, and demand signals from term contract holders. Because Saudi Arabia is the largest single crude exporter, its OSP decisions influence the pricing of approximately 9 million bpd of Gulf crude flowing to Asia.

Can Asian refiners switch away from Saudi crude permanently?

Not easily. Arab Light’s API gravity (32.8) and sulfur content (1.77%) match the configuration of most major Asian refineries — particularly in Japan, South Korea, and coastal China. Switching to ESPO (34.8 API, 0.62% sulfur) or Basra Light (29-33 API, 2.9% sulfur) requires yield adjustments and, in some cases, secondary unit modifications that take 12-18 months. Term contracts with Aramco typically run on annual renewal cycles with volume commitments. The risk for Saudi Arabia is not that refiners permanently replace Arab Light but that they reduce contracted volumes and fill the gap with spot purchases from Russia or West Africa — each renewal cycle at reduced volume is a barrel Aramco must win back at full competition when Hormuz reopens.

How long could the Yanbu bottleneck persist?

The East-West Pipeline feeding Yanbu has a design capacity of 5 million bpd but practical throughput of 4.0-4.5 million bpd, constrained by pumping station damage from the April 8 IRGC strike and maintenance limitations. Aramco has not disclosed a repair timeline for full pipeline capacity. Even at maximum pipeline throughput, Yanbu cannot match the 7-7.5 million bpd that Saudi Arabia shipped through Hormuz before the war — leaving a structural gap of 2.5-3.5 million bpd that persists until the strait reopens to commercial traffic.

Why did Russia’s crude flip from a Brent discount to a premium?

Before the Iran-Saudi war, Russian ESPO crude traded approximately $10 per barrel below Brent — a discount driven by Western sanctions, insurance restrictions, and the costs of using a shadow fleet. The war removed roughly 5-6 million bpd of Persian Gulf supply from the market simultaneously, creating a structural shortage that allowed Russian producers to charge $8-10 above Brent for ESPO cargoes to Chinese buyers. Russia now occupies the position Saudi Arabia held before the war: the reliable, available supplier commanding a premium for certainty of delivery.

What happens to the OSP if the ceasefire holds and Hormuz reopens?

If Hormuz reopens to commercial traffic, approximately 3-4 million bpd of Saudi export capacity currently stranded behind the strait would re-enter the market within weeks, based on Nasser’s “days” estimate for production ramp-up. Aramco would face a choice between maintaining current OSP levels to rebuild revenue or cutting aggressively to recapture market share from Russia and Iran. The May 2022 precedent — when Aramco cut the OSP by more than 50% after Chinese demand collapsed — suggests the company will move sharply if it needs to win back volume. The fiscal deficit may constrain how far Saudi Arabia can cut before the treasury’s needs override the commercial logic.