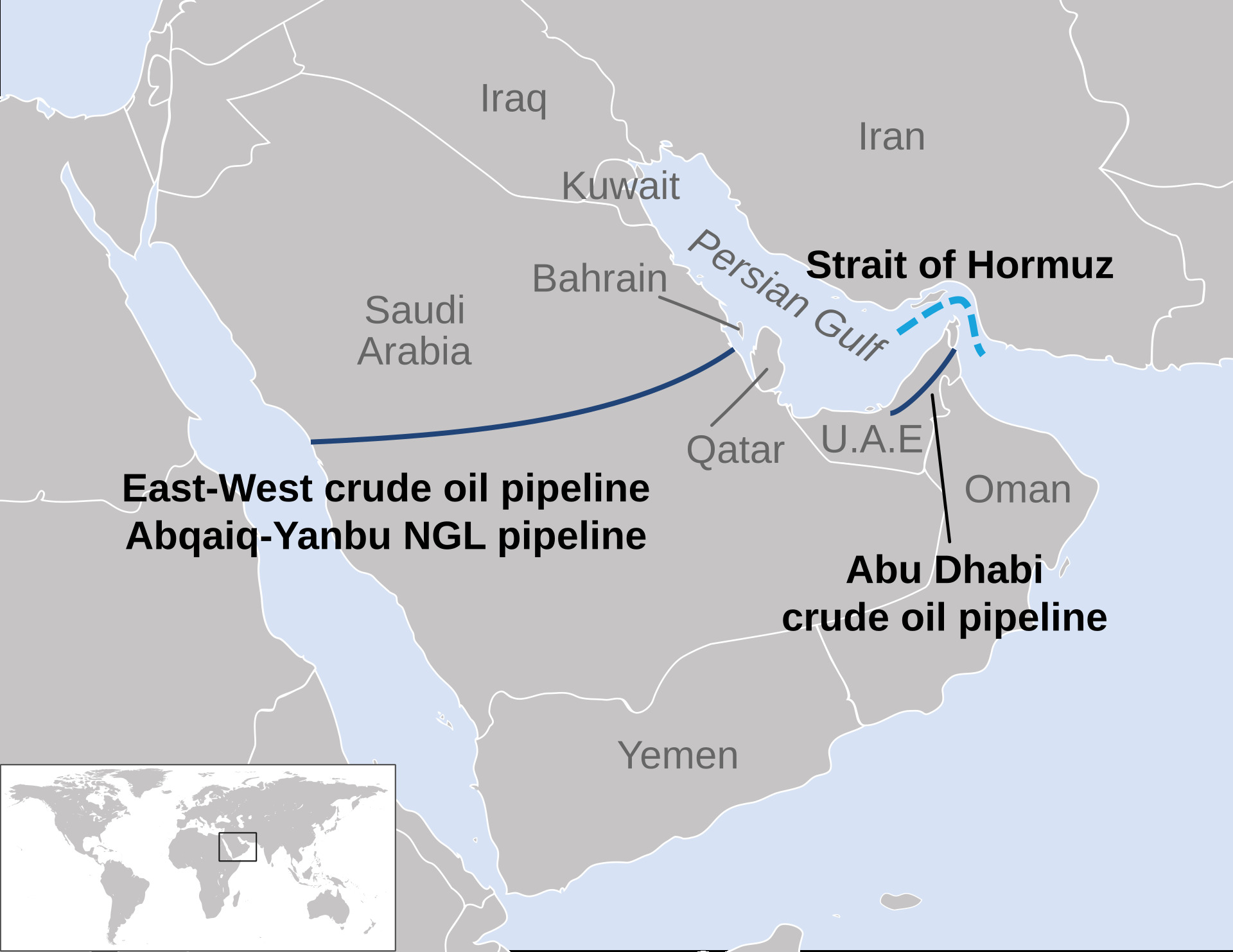

JEDDAH — Houthi military spokesman Brigadier General Yahya Saree declared “a complete and total ban on Israeli maritime navigation” in the Red Sea on June 8, warning that “all enemy movements are to be considered legitimate military targets” for Houthi forces, according to Bloomberg and gCaptain. The declaration, issued under the Iran-led “Unity of the Fronts” doctrine on the hundredth day of Iran’s closure of the Strait of Hormuz, extends the war to the only bulk crude export corridor Saudi Arabia has left — the 1,200-kilometre East-West Pipeline terminating at Yanbu on the Red Sea coast.

Saudi Arabia built the Petroline for exactly this scenario — a land-based bypass connecting Eastern Province oil fields to a port that does not depend on Hormuz. Aramco pushed it to an all-time record of 7 million barrels per day by late March, according to S&P Global Commodity Insights, making Yanbu the most important loading terminal in the kingdom’s history. But an estimated 70 to 75 percent of Yanbu’s Asia-bound exports must still transit Bab el-Mandeb to reach buyers in Japan, South Korea, and India, according to the Observer Research Foundation’s dual-chokepoint analysis — which means the bypass Saudi Arabia spent decades constructing runs directly into the blockade zone the Houthis declared on Sunday morning. India, which imports more Saudi crude than any other single buyer, would later file a formal demarche over US wartime maritime enforcement in the Gulf of Oman — placing Riyadh in the position of being unable to support India’s diplomatic protest against its own security guarantor. Three days later, on Day 103, US Energy Secretary Wright told financial television that traffic through the strait was rising “very meaningfully” — a claim that IMF PortWatch data from June 7 directly contradicts and that Day 103 of the Hormuz blockade documents in full.

Table of Contents

The Bypass That Ends in a Blockade Zone

Of the 7 million barrels per day flowing through the East-West Pipeline, approximately 2 million are diverted to Saudi domestic refineries, leaving around 4.5 million reaching Yanbu’s twin export terminals — Yanbu North at 1.5 million barrels per day capacity and Yanbu South at 3.0 million, according to Bloomberg and Argus Media. Under wartime loading conditions, effective throughput is approximately 4 million barrels per day, with around 22 million barrels sitting in Yanbu’s tank farms at roughly 60 percent of storage capacity.

The pipeline and the port are both performing at or near capacity, and neither is the weak link. The problem starts after a tanker clears Yanbu heading south. Asia takes the overwhelming majority of Saudi crude exports, and the sea route from Yanbu to East Asian buyers transits Bab el-Mandeb, the 18-to-21-mile-wide strait that the Houthis control from Yemen’s western coastline. Willis Towers Watson issued what now reads as a prescient warning on March 26 — “WTW warns on Hormuz-Bab el Mandeb simultaneous closure nightmare” — and on June 8, Saree turned the modelled scenario into an operational one.

| Strait of Hormuz | Bab el-Mandeb | |

|---|---|---|

| Pre-crisis daily oil flow | ~21M bpd | ~5.6M bpd |

| Width at narrowest point | ~21 nautical miles | 18–21 miles |

| Closure / interdiction date (2026) | February 28 | June 8 (declared) |

| Saudi bypass route | East-West Pipeline to Yanbu | None |

| Cape reroute penalty | +10–14 days, $1.2–1.8M per voyage | +10–14 days, $1.2–1.8M per voyage |

The combined interdiction of both straits puts an estimated $10 billion per day of global trade at risk and would block approximately 25 percent of the world’s oil and gas supply, according to ORF and corroborated by WTW’s risk assessment for Lloyd’s. Cape of Good Hope rerouting — adding 3,000 to 3,500 nautical miles and over a million dollars in fuel costs per voyage — falls directly on the competitiveness of Saudi crude against grades that do not require tankers to circumnavigate Africa to reach the same Asian refineries.

How Much Revenue Disappears?

Saudi crude exports had already collapsed from approximately 7.3 million barrels per day before the Hormuz closure in February to roughly 4.4 million in March — a loss driven by the shutdown of Gulf port loading and Asian buyers’ refusal to charter through designated war-risk zones, according to JODI data. Brent crude traded at $98.29 intraday on June 8, sitting $10 to $13 below the $108-to-$111 fiscal breakeven Saudi Arabia needs to balance its budget, a gap that costs approximately $100 million per day for every dollar Brent stays below the threshold. Riyadh captured the Gulf’s wartime air traffic and tourist overflow, but the treasury has seen none of it compensate for the export collapse, and the Bab el-Mandeb declaration threatens to make the revenue picture materially worse. Three days later, Trump’s unverified settlement announcement erased the residual wartime price premium, with Brent dropping to $89.15 — how the deal narrative is eroding the wartime price premium that had partially cushioned Saudi fiscal exposure.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

Aramco’s July Official Selling Prices, released on June 8 hours before Saree’s statement, tell the story before the export data catches up. Arab Light was cut $6 per barrel to Asia, and Europe and Mediterranean grades were cut $10 per barrel — the steepest European discount on record, according to Reuters and OilPrice.com. The Asian discount reflects the difficulty of finding tankers willing to load at Yanbu with war-risk premiums already elevated; the European cut, far larger, signals that Aramco is pricing in the prospect that Mediterranean-bound cargoes will face disruption if Suez Canal traffic — which enters the Red Sea through Bab el-Mandeb from the south — slows or diverts around the Cape entirely.

The timing compounds the fiscal pressure beyond what any single data point captures. On June 9, Aramco pays its $21.89 billion base quarterly dividend against Q1 free cash flow of just $18.6 billion — a $3.3 billion structural overpayment identified by Sahm Capital in May. Goldman Sachs projects Saudi Arabia’s full-year 2026 deficit at SAR 300 to 330 billion ($80 to $90 billion); the kingdom burned through 76 percent of that projected total in Q1 alone, posting a SAR 125.7 billion ($33.5 billion) first-quarter shortfall that must now absorb a second chokepoint closure before summer ends. Aramco’s $53 billion cash floor was already under siege at $95 Brent — at $98 with both exits compromised, the gap between what Saudi Arabia earns and what it has committed to spend is widening at a pace the dividend structure was never designed to withstand.

What Can Saudi Arabia Actually Say?

Saudi Arabia’s Ministry of Foreign Affairs has issued zero public statements on any Houthi Red Sea operation throughout the entire war — not when the Houthis resumed strikes in February, not when container transits cratered, and not on June 8 when the formal blockade was declared. This is not bureaucratic delay. It is the logical endpoint of the de facto truce that Riyadh spent years and considerable political capital constructing with Ansarallah, a truce whose central bargain — Houthi restraint toward Saudi territory in exchange for Saudi silence on Houthi operations elsewhere — has held for over 100 days while the Houthis struck Kuwait, Bahrain, and central Israel with Iranian-supplied weapons.

The truce that was supposed to protect Saudi Arabia is now the constraint that prevents it from acting. Condemning the Red Sea ban would signal pro-Israel alignment, unravel the ceasefire, invite Houthi strikes on Saudi soil and Aramco facilities, and hand Tehran a propaganda tool in the same week that Iran declared Hormuz talks dead. Staying silent means watching export revenue evaporate through a strait Saudi Arabia lacks the naval capacity to keep open unilaterally. Asking Washington to intervene against the Houthis raises the question that has defined every Gulf defence arrangement since February: why should American forces protect Saudi commerce when Riyadh has contributed no military assets to the maritime security mission, no operational access to Prince Sultan Air Base, and no presence in the US-led Combined Maritime Forces or its Red Sea successor mission? The same structural logic applies at Hormuz: the IRGC’s shoot-on-sight order and the collapse of the April 8 ceasefire framework left Saudi Arabia with no leverage at either chokepoint — a gap that Hormuz Has No Ceasefire to Collapse documents in full. Beyond the kinetic dimension, Iran has institutionalized the per-barrel Hormuz toll mechanism through the Persian Gulf Strait Authority — a $1/barrel service fee on every cargo in the Qeshm-Larak corridor that represents a structural revenue stream for Tehran regardless of whether any ceasefire holds.

The Houthi definition of “Israeli-linked” adds a layer of commercial risk that extends well beyond Israeli-flagged vessels. During the 2024 campaign, the Houthis applied the term expansively to encompass vessels owned or operated by Israeli entities, vessels headed to Israeli ports, and vessels owned by companies doing business with Israeli port facilities, according to Skuld P&I Club analysis. Aramco sells crude to Japanese refiners, Korean petrochemical firms, and Indian state oil companies, several of which also receive cargoes at ports the Houthis have previously designated as Israeli-connected. Whether a VLCC carrying Arab Light to Yokohama constitutes an “enemy movement” under Saree’s blanket declaration is a question that neither Aramco’s trading desk nor the Houthis have any incentive to answer clearly — and that insurers, as of June 8, must price as though the answer could be yes.

The Nightmare the Insurers Already Modelled

Marine war insurers had already repriced Arabian Gulf risk at approximately 60 times pre-crisis rates within 48 hours of the Hormuz closure in February, according to Property Casualty 360, and the Lloyd’s Joint War Committee redesignated the entire Arabian Gulf as a conflict zone. Lewis Hart, head of marine in Asia at Willis Towers Watson, warned that war risk premium rates were “unlikely to decline immediately” even under ceasefire conditions — an assessment that predated the dual-chokepoint escalation by months and assumed only one strait was in play.

“The scenario marine war underwriters have modelled but hoped not to face: simultaneous disruption to both the Strait of Hormuz and the Bab el-Mandeb Strait.”

Insurance Business Magazine, June 8, 2026

The 2023-2024 Houthi campaign disrupted approximately $1 trillion in Red Sea trade, according to Russell Group estimates, and that campaign operated without a formal total ban and without a concurrent Hormuz closure. Daily container transits through Bab el-Mandeb fell from roughly 70 to 19 by January 2024, according to Seatrade Maritime data, under conditions far less severe than those prevailing now — when both chokepoints are interdicted, the Houthis have declared a blanket enforcement posture rather than selective targeting, and the Iran-led coalition is operating under an explicit doctrine of coordinated pressure. For Saudi tanker charterers, the practical effect is a choice between Red Sea transits carrying premiums that may approach Hormuz-crisis levels and Cape rerouting that adds two weeks and over a million dollars to every voyage, with neither option restoring the cost structure that made Saudi crude competitive in Asian spot markets three months ago.

Why Is June 8 Different From 2024?

The Houthis ran a punishing Red Sea campaign through 2024, striking dozens of commercial vessels and forcing major container lines to reroute around Africa, but the 2024 operations and Saree’s June 8 declaration are structurally different in ways that matter for Saudi Arabia’s exposure. The first is instrument: the 2024 attacks were rolling, individual targeting decisions based on real-time intelligence about specific vessels, while June 8 is a declared total ban — a stated legal posture with blockade framing, not a de facto one — which changes the insurance and chartering calculus for every vessel considering a Red Sea transit regardless of flag, cargo, or destination.

The second is context. In 2024, the Strait of Hormuz was open, Saudi Arabia’s Gulf ports were functioning, and the East-West Pipeline was a strategic reserve rather than the kingdom’s sole export lifeline. Yanbu was one loading point among several, handling overflow and European-bound cargoes. On June 8, Hormuz has been closed for 100 days, Gulf ports are shuttered, and Yanbu handles nearly all of Saudi Arabia’s crude exports — meaning that any disruption to Red Sea shipping no longer affects one route among several but the route that replaced all the others. What a hundred days of war already cost Saudi Arabia is quantifiable; the cost of losing the bypass that was supposed to limit the damage has no precedent in the kingdom’s fiscal history.

The third is integration. Saree framed the ban explicitly under the “Unity of the Fronts” doctrine, citing “Israeli aggression against Lebanon, Iran, and Gaza” in a single operational statement, according to The National News in Abu Dhabi. The Houthis simultaneously claimed a missile barrage on “sensitive targets in occupied Jaffa,” according to JNS and Middle East Monitor, confirming that the maritime interdiction and missile strikes are components of a single campaign, not separate initiatives. Houthi leader Abdul-Malik al-Houthi called the broader Iran war a “great victory” for the Axis of Resistance, according to Eurasia Review — language that frames Red Sea operations not as an independent Yemeni initiative, as they were partially characterised in 2024, but as an integral element of Iran’s multi-front war. For Saudi Arabia, that integration makes standalone diplomacy with the Houthis harder to pursue and impossible to present domestically as anything other than accommodation of the Iranian war effort.

The Truce That Became the Constraint

Saudi Arabia fought the Houthis in Yemen from March 2015, leading a coalition that conducted thousands of airstrikes and spent tens of billions of dollars over seven years without dislodging Ansarallah from Sanaa or the western highlands that overlook Bab el-Mandeb. A UN-mediated truce in April 2022 held despite never advancing to a formal peace agreement, and by September 2023 the diplomatic track had progressed far enough that a Houthi delegation flew to Riyadh for talks with Defence Minister Prince Khalid bin Salman, according to Al Jazeera and Reuters — the first announced Houthi visit to the Saudi capital since 2014. No treaty was signed, but the de facto ceasefire endured through the Gaza war, through the 2024 Red Sea campaign, and into 2026, making Saudi Arabia the only state in the region that the Houthis have consistently refrained from striking since the Iran war began on February 28.

That restraint now functions as a cage with the lock on the outside. The Houthis have given Saudi Arabia exactly what it asked for — no cross-border drone swarms, no missiles aimed at Riyadh, no attacks on the Aramco facilities that an already depleted Patriot belt can barely defend — while simultaneously destroying the commercial utility of the kingdom’s only functioning export route. The 2024 US re-listing of the Houthis as a Foreign Terrorist Organisation rendered the UN Yemen roadmap legally unworkable, closing the one formal channel through which Riyadh might have applied pressure on Ansarallah to moderate its Red Sea posture. What remains is an informal understanding in which the Houthis spare Saudi territory and Saudi Arabia says nothing while they close the strait that carries its oil to the world.

The East-West Pipeline was built in 1981, during the Iran-Iraq War, to guarantee that Saudi crude could reach global markets even if Iran closed the Strait of Hormuz. Forty-five years later, it works as designed — 7 million barrels per day flowing west across the desert, away from the Gulf war, to a Red Sea port that was supposed to be the safe exit. The strait it empties into is now a declared blockade zone, enforced by the same force that Saudi Arabia spent seven years trying to destroy and then paid, in political capital and silence, to leave alone.

Frequently Asked Questions

Can Saudi Arabia reroute Yanbu exports north through the Suez Canal to avoid Bab el-Mandeb?

Northbound Suez transits from Yanbu reach European and Mediterranean buyers without crossing Bab el-Mandeb, but these represent only 25 to 30 percent of Yanbu’s export volume. Suez capacity is already strained by rerouted Gulf traffic, and Mediterranean refiners have limited incremental demand for the heavy-sour Saudi grades that Asian refinery configurations are optimised to process. The structural mismatch between available refining capacity and crude quality narrows this option further than geography alone suggests.

Have the Houthis ever struck a Saudi-flagged or Saudi-chartered vessel in the Red Sea?

No confirmed Houthi strike on a vessel explicitly identified as Saudi has occurred during the 2024 campaign or the current war. However, the expanded “Israeli-linked” definition applied in 2024 led to strikes on at least two vessels later determined to have been misidentified, according to Skuld P&I Club. The Houthis have published no exemption list for Saudi cargoes, and the blanket “all enemy movements” language in Saree’s June 8 declaration offers less specificity than the 2024 targeting criteria.

What military assets does Saudi Arabia have in the Red Sea?

The Royal Saudi Naval Forces’ Western Fleet, based at King Faisal Naval Base in Jeddah, operates frigates, corvettes, and patrol craft. Saudi Arabia has not conducted any interdiction or escort operations against Houthi maritime activity and was not part of Operation Prosperity Guardian during the 2024 campaign. Any unilateral Saudi naval action against Houthi positions would represent a rupture of the de facto truce with no precedent in the current conflict.

Is there a pipeline alternative that bypasses both Hormuz and Bab el-Mandeb entirely?

The only existing cross-regional pipeline that avoids both straits is the Iraq-Turkey pipeline (Kirkuk-Ceyhan), which terminates at the Turkish Mediterranean port of Ceyhan at approximately 900,000 barrels per day capacity. It carries Iraqi crude, not Saudi, and has been subject to repeated sabotage and Turkish-Kurdish political shutdowns. No pipeline connecting Saudi oil fields to a Mediterranean or Indian Ocean port that circumvents both chokepoints is under construction or in advanced planning.

A separate bilateral constraint — the presence of 30,000 Iranian Hajj pilgrims inside Saudi territory — also expired on June 9 as the pilgrimage season closed. The passive deterrent that had restrained both governments from overt escalation throughout the Hajj period has now lapsed, removing the last informal check on Saudi-Iranian hostilities examined in Mecca Held 30,000 Iranians for Thirty-Nine Days — Today the Shield Expires.

Within hours of that declaration, the ban moved from policy to kinetic enforcement: Houthi missiles struck M/V Tavvishi and the Norderney in the Gulf of Aden, the first confirmed ship strikes under the new interdiction regime, demonstrating that Saree’s June 8 announcement carried immediate operational force. Both maritime interdictions ran parallel to Operation Nasr within the same 48-hour window: while the IRGC struck Nevatim and Tel Nof, the Houthis enforced the blockade at sea — coordinated pressure under the Unity of Fronts doctrine, with Saudi Arabia targeted by neither. The freight increment compounds a separate insurance overlay: war-risk premiums now add $800,000 to $2 million per VLCC voyage, and the actuarial mechanism that sets them cannot be unlocked by any ceasefire announcement.