RIYADH — Donald Trump told his negotiators on May 24 not to rush into a deal with Iran because “time is on our side.” The same day, a US official told CBS that negotiators had “agreed to broad principles of agreement.” Both statements came within hours of each other. Neither resolved the condition facing Saudi Arabia, where the Strait of Hormuz has been effectively closed for 87 days and collective GCC oil revenue losses are running at approximately $700 million per day.

The distance between “broad principles” and a signed agreement is where Saudi fiscal planning breaks down. When the JCPOA was negotiated in 2015, the interval from framework announcement in Lausanne to actual signature in Vienna took 103 days. Saudi Arabia’s Q1 2026 deficit — $33.5 billion, consuming 76 percent of the full-year projection in 90 days — leaves no buffer for a process that moves at Washington’s pace rather than Riyadh’s need. Goldman Sachs estimates the actual 2026 deficit at $80-90 billion, nearly double the official $44 billion figure published by the Ministry of Finance. Brent’s first break below $100 this month has moved the IMF’s $86.60 fiscal breakeven from forecast to present reality.

Table of Contents

- The Signal Split

- What Does Every Day Without a Deal Cost Saudi Arabia?

- The Asymmetry of Patience

- Does the JCPOA Precedent Predict the Current Timeline?

- The Architecture That Grows While Washington Waits

- Can Saudi Arabia’s Budget Survive a Summer Without a Signature?

- What Can Saudi Arabia Do While Washington Waits?

- Who Benefits from the Clock Running?

- Frequently Asked Questions

The Signal Split

On May 23, Trump posted on Truth Social that a deal with Iran was “largely negotiated” and would be “announced soon.” The Sunday deadline he had floated — a target that structured a week of diplomatic choreography spanning Rome, New Delhi, and Washington — shaped market expectations and pushed Gulf foreign ministries into preparation mode. Brent crude closed at $103.94 on May 22, holding steady on the ambiguity.

Then May 24 arrived. Trump posted again, this time instructing his team not to rush. “Negotiations are proceeding in an orderly and constructive manner,” he wrote. “Time is on our side.” NBC News and CNBC carried the reversal within hours. The White House confirmed to Axios that any deal would take “days,” not hours — the first official concession that Sunday had come and gone without a signature. A US official separately told CBS that negotiators had “agreed to broad principles of agreement,” a formulation that preserved the appearance of momentum without the obligation of a timetable. By the close of May 24, trading desks, Gulf governments, and market participants confronted two simultaneous signals — “broad principles agreed” and “we won’t rush” — and could price neither.

Iran’s response matched the ambiguity with categorical rigidity. President Masoud Pezeshkian told state media on May 24 that his team would “under no circumstances compromise on the country’s dignity and pride.” Fars News Agency called Trump’s “largely negotiated” characterisation “incomplete and inconsistent with reality” and stated that the Strait of Hormuz would “remain under Iranian management.” Tasnim reported that the Strait would “not return to its pre-war status” under any agreement — via NBC News and NPR on the same day.

The deceleration had legible domestic logic in Washington. Sen. Roger Wicker, chairman of the Senate Armed Services Committee, warned on May 24 that “the rumored 60-day ceasefire — with the belief that Iran will ever engage in good faith — would be a disaster.” Mike Pompeo, the former Secretary of State, called the emerging terms “not remotely America First” on i24News and prescribed his alternative: “Open the damned strait. Deny Iran access to money. Take out enough Iranian capability so it cannot threaten our allies in the region.” Sen. Thom Tillis admitted he was “not too far away from where Pompeo is.”

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

“Everything accomplished by Operation Epic Fury would be for naught… a deal that would not be worth the paper it is written on.”

— Sen. Roger Wicker (R-MS), Chairman, Senate Armed Services Committee, The Hill, May 24, 2026

Trump’s “won’t rush” framing solved a Washington problem. It gave him space to absorb Republican criticism — the White House reportedly told Pompeo to “shut his stupid mouth,” a register that conveyed the seriousness of the right-flank threat — without abandoning a deal framework his own officials said was agreed in broad outline. Richard Nephew, former State Department sanctions official, told Fortune on May 23 that the United States had “reached the limit of what we can achieve with sanctions and economic pressure.” That assessment, from Washington’s vantage point, counsels patience rather than urgency: if the pressure has peaked, there is no cost to letting the clock run while domestic opposition is managed.

What Does Every Day Without a Deal Cost Saudi Arabia?

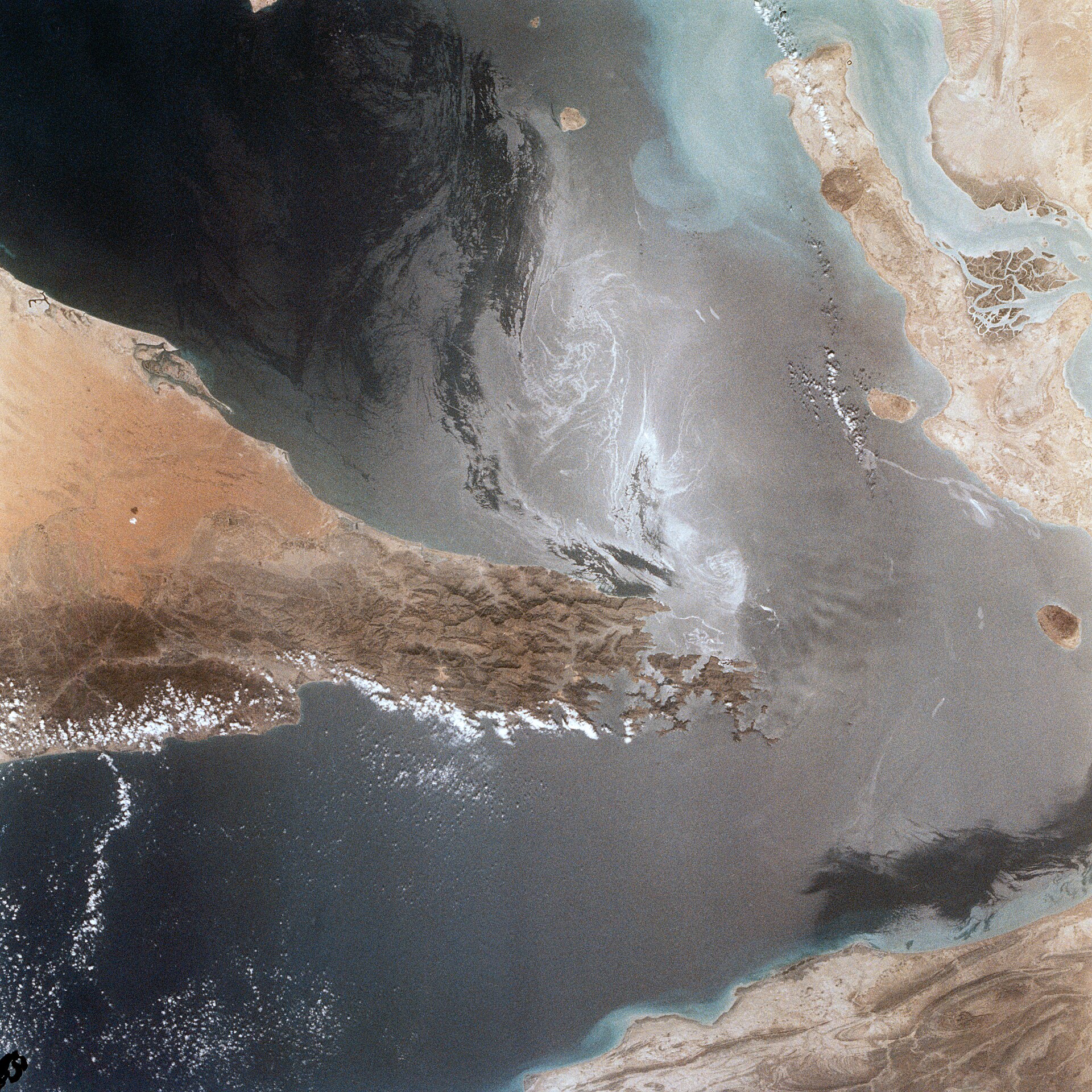

Collective GCC oil revenue losses run approximately $700 million per day with the Strait of Hormuz closed. Saudi Arabia’s production sits 3.41 million barrels per day below its OPEC+ quota — physically undeliverable through a closed waterway, not a policy choice.

The global oil market forfeits an estimated 100 million barrels of crude and petroleum products per week that the Strait remains closed. The losses concentrate where production capacity concentrates. Saudi Arabia’s OPEC+ quota stands at 10.291 million barrels per day; actual output has fallen to approximately 6.879 mbpd. The Yanbu pipeline on the Red Sea coast provides an export ceiling of roughly 5 mbpd, and while Hormuz is closed, that ceiling defines the Kingdom’s hard boundary. The collective OPEC+ shortfall — 27.68 mbpd against a quota of 36.73 mbpd, a 9 mbpd gap — drew Rystad Energy’s assessment as “the worst quarterly compliance failure in OPEC history.”

The borrowing data tracks the revenue data. The GCC’s net government borrowing requirement has doubled from approximately $1.7 billion per week to $3.5 billion per week since the disruption began, according to EnergyNow.com. Goldman Sachs’s MENA team estimated in April 2026 that the real full-year deficit would reach approximately $80-90 billion — roughly 6.6 percent of GDP and nearly double the official $44 billion projection.

| Metric | Value | Source |

|---|---|---|

| GCC daily oil revenue loss | ~$700M | EnergyNow.com |

| Global oil supply loss per week | 100M barrels | Disruption analysis, 2026 |

| Saudi OPEC+ quota vs actual output | 10.291 vs 6.879 mbpd | OPEC+ / Rystad Energy |

| Undeliverable production gap | 3.41 mbpd | Quota minus actual |

| Saudi Q1 2026 deficit | $33.5B | Saudi MoF / Zawya |

| Goldman Sachs full-year deficit estimate | $80–90B (6.6% GDP) | Goldman Sachs MENA, Apr 2026 |

| GCC weekly borrowing requirement | $3.5B (up from $1.7B) | EnergyNow.com |

| Saudi fiscal breakeven (Brent) | $94/bbl | Bloomberg Economics |

| EIA 2027 Brent forecast (normalised) | $79/bbl | EIA STEO |

| Yanbu pipeline export ceiling | ~5 mbpd | Industry estimates |

Aramco CEO Amin Nasser told CNBC on May 11 that the market would “normalize only in 2027” if Hormuz did not reopen within “a few weeks.” Mid-June is the functional deadline embedded in that assessment — the point after which tanker fleet displacement (600-plus vessels rerouted), disrupted Asian refinery maintenance cycles, and missed LNG contract windows lock in supply-chain consequences that persist regardless of when a deal arrives. As of May 21, twenty-seven tankers sat in queue at Kharg Island, a 93 percent increase over the previous week, and verified Hormuz transits had fallen from 95 per day pre-crisis to 2.

The Asymmetry of Patience

Washington’s capacity for patience is structural, not performative. The United States is a net energy exporter. Elevated oil prices inconvenience American consumers and create political friction — the Council on Foreign Relations observed in May 2026 that Iran’s leaders “likely think they can impose political pain on Trump through a drawn-out conflict and elevated gas prices” — but that pain is diffuse, absorbed across a $28 trillion economy with no single-commodity fiscal dependency. Trump’s domestic risk from high gasoline prices operates on a political calendar measured in quarters and electoral cycles, not in daily revenue losses.

Saudi Arabia’s exposure is concentrated in a way that admits no equivalent patience. The Kingdom derives roughly 60 percent of government revenue from hydrocarbons. Its fiscal breakeven — the Brent price at which the budget balances — sits at $94 per barrel according to Bloomberg Economics, with the IMF placing it near $90. But the breakeven price is a secondary concern when the barrels cannot physically move. With Hormuz closed and the Red Sea pipeline capped at roughly 5 mbpd, Saudi Arabia is producing 3.41 mbpd below quota — a gap imposed by a crisis Riyadh did not initiate, in negotiations Riyadh does not attend, on a timeline Riyadh cannot influence.

The temporal mismatch runs deeper than the fiscal gap. When Trump says “time is on our side,” the referent is a political calendar in which months are an acceptable unit of measure. When Aramco’s CEO says the market will not normalise until 2027, the referent is a supply-chain architecture built on tanker fleet positions and refinery scheduling that operates on a different clock entirely. The Kingdom waits twice: first for a deal framework that may or may not materialise over the summer, and then for the nuclear performance track — at minimum 30 days of verification — that must follow any signature before Hormuz governance is addressed. The fiscal cost of the first wait compounds throughout the second. On May 27, Trump made that patience explicit — publicly removing the midterm election as any kind of forcing mechanism and stating he would resume military operations if Iran did not meet US terms. What Trump said, and what it costs Saudi Arabia, is documented here.

Does the JCPOA Precedent Predict the Current Timeline?

The 2015 JCPOA took 103 days from the Lausanne framework agreement on April 2 to the final signature in Vienna on July 14, with one deadline extension along the way. Saudi Arabia was excluded from those negotiations. Its concerns about ballistic missiles, regional proxies, and sunset clauses were raised through diplomatic channels and absent from the final text.

The JCPOA precedent is instructive less for its diplomatic substance than for its temporal architecture. The Lausanne announcement — the moment at which officials could credibly say “broad principles” had been agreed — marked the beginning of the hardest negotiations, not their conclusion. The 103 days that followed contained fights over centrifuge numbers, inspection protocols, enrichment ceilings, and sanctions-relief sequencing. One deadline (June 30) was extended to July 7 before the text was finalised on July 14. The pattern of announced progress followed by protracted technical negotiation is visible in the current trajectory: the White House’s “days, not hours” concession to Axios echoes the extensions that characterised the JCPOA’s final stretch.

If the current deal follows the JCPOA’s timeline, Saudi Arabia faces an unsigned agreement persisting through June and potentially into late summer. Five rounds of talks across 106 days have produced three separate framework documents — Axios’s 14-point MOU, Al-Arabiya’s 8-point “final draft,” and Pakistan’s Munir letter of intent — none signed, no two containing the same terms on enrichment. Foreign Minister Araghchi declared on May 23 that “zero enrichment = no deal.” Khamenei has directed that Iran’s approximately 440 kilograms of 60 percent enriched uranium must remain in the country. The Supreme National Security Council retains a formal veto over any agreement.

The 2015 precedent is also instructive for what Saudi Arabia gained from 103 days of waiting: nothing it had asked for. The Kingdom’s red lines on missiles, proxies, and sunset clauses were noted diplomatically and ignored substantively. The same structural exclusion is visible in 2026: Saudi Arabia has been listed as a “mediating party” by Axios but excluded from all five rounds of direct talks and from the nuclear Track 2 that follows any framework. The Carnegie Endowment assessed in April 2026 that the GCC “has no seat at the table.” The Atlantic Council’s formulation was blunter — Gulf states have been “largely sidelined.” Saudi Arabia co-sponsored the UNSC Hormuz resolution that Russia and China vetoed on April 7, carrying 137 co-sponsors — a record that changed nothing.

The Architecture That Grows While Washington Waits

Negotiating delays are not neutral intervals. They produce structural facts that outlast whatever agreement eventually follows. The 41 days between the Islamabad collapse (April 11-12) and Rome Round 5 (May 23) saw Iran establish the PGSA — the Persian Gulf Security Administration — on May 5, operationalise it on May 18, and by May 24 begin processing transits at $2 million per VLCC, payable in yuan or Bitcoin. The exemption list — Russia, China, India, Iraq, and Pakistan — is identical to the UNSC veto-holder roster plus the states that blocked or abstained from the April 7 Hormuz resolution. The powers with the capacity to dismantle the toll regime through the Security Council are precisely the ones benefiting from its operation.

Iran has suspended Hormuz transit not as a temporary wartime measure but as the foundation of a juridical claim. The PGSA statute — 12 articles of domestic legislation — passed committee on April 21 and awaits a full chamber vote in the Iranian parliament. Tasnim reported on May 24 that the Strait would “not return to its pre-war status” under any agreement. Fars stated that Hormuz would “remain under Iranian management.” These statements accompany legal architecture — committee votes, statutory text, operational infrastructure — designed to outlast whatever ceasefire or framework eventually emerges from the current talks.

The compounding dynamic is what distinguishes delay cost from delay inconvenience. Ships that pay the $2 million toll establish a transactional precedent. Exemptions for Russia and China create commercial constituencies for the regime’s preservation. The PGSA’s operational infrastructure — fee collection in yuan and cryptocurrency, designated transit corridors, a defined Kuh-e Mubarak-to-Fujairah enforcement zone — matures daily through practice. The Chatham House assessment from May 2026 — that “the structural nature of the Hormuz problem leaves Saudi Arabia with little choice” in terms of economic adaptation — assumed a static toll regime when it was written. The regime is not static. It hardens through legislation and commercial habit with every week that the gap between “broad principles agreed” and actual signature remains unclosed. That gap now has a structural cause independent of wording disputes: Iran’s constitutional approval chain runs through Khamenei’s couriers, a physical relay with multi-day latency that delays any confirmed signature regardless of what negotiators agree at the table.

Can Saudi Arabia’s Budget Survive a Summer Without a Signature?

At its current burn rate, Saudi Arabia will exhaust its official $44 billion full-year deficit projection by mid-June — and the Goldman Sachs estimate of $80-90 billion suggests the official figure was already fictional before that point arrives. If Hormuz reopens and Brent normalises to the EIA’s $79 forecast for 2027, that price still sits $15 below Saudi Arabia’s $94 Bloomberg Economics breakeven.

The fiscal mathematics trap the Kingdom in both scenarios. If Hormuz stays closed through the summer, the Q1 burn rate — approximately $370 million per day in deficit accumulation — continues unchecked. Goldman’s estimate assumed some form of partial Hormuz reopening in the second half; without it, the number rises further. The official $44 billion projection, constructed before the war, has become an artefact of pre-crisis planning rather than a guide to fiscal reality.

If Hormuz reopens, the relief arrives more slowly than a signature suggests. Nasser’s “normalize only in 2027” assessment reflects supply-chain physics that no diplomatic ceremony overrides: 600-plus displaced tankers require weeks to reposition, Asian refineries that switched to alternative sourcing need scheduling cycles to revert, and LNG contract windows that closed during the disruption do not simply reopen on command. The EIA’s normalised Brent forecast of $79 per barrel for 2027 assumes full resolution — and at $79, the price sits below every major estimate of Saudi Arabia’s fiscal breakeven. Normalisation does not balance the budget; it shifts the deficit from wartime emergency to structural shortfall.

The construction sector — the physical infrastructure of Vision 2030 — was contracting before the war began. Project awards fell from $71 billion to $30 billion in the prior year. PIF’s $7 billion bond sale on May 7 raised cash at wartime spreads: the 3-year tranche priced at 95 basis points over Treasuries, against a $23.8 billion orderbook that was 3.4 times oversubscribed but carried a 79-basis-point premium over Abu Dhabi’s equivalent issuance. Chatham House noted in March 2026 that Saudi Arabia’s “financial position was already showing signs of strain before the war, and foreign lenders and investors will be reappraising Saudi risk.”

What Can Saudi Arabia Do While Washington Waits?

Structurally, very little. The Kingdom cannot accelerate talks it does not attend, reopen a strait it does not control, or publicly criticise a US pace without undermining the only diplomatic process that might restore its oil exports. Hajj — with the Day of Arafah falling on May 26 and Eid al-Adha on May 27 — imposes a 96-hour window in which Saudi Arabia’s role as custodian of the Two Holy Mosques forecloses any politicisation of the pilgrimage season.

The actions available to Riyadh divide into categories of diminishing utility. The Kingdom has borrowed — through PIF’s wartime bond issuance at elevated spreads. It has lobbied — through Crown Prince Mohammed bin Salman’s calls to multiple world leaders in late May. It has endorsed — through Foreign Minister Prince Faisal bin Farhan’s May 20 public praise of Trump’s approach to Iran, issued four days before Trump announced he was in no rush. It secured the 123 enrichment agreement from Washington, co-sponsored the UNSC Hormuz resolution, and hosted Secretary Rubio in Riyadh. None of these actions shortened the interval between “broad principles” and a signature by a single day.

The Saudi Ministry of Foreign Affairs has not issued a substantive public statement on the Iran negotiations during the war. The silence reads as the rational response of a government that cannot welcome the deal’s likely terms — which threaten Saudi interests on enrichment, Hormuz governance, and regional security architecture — nor oppose the deal’s existence, which represents the only path to reopening the Strait. The 15,000 US troops stationed in the Gulf, whose withdrawal depends on the same timeline Trump has just decelerated, add a further constraint on Saudi freedom of action: requesting their departure signals abandonment of the alliance framework, while requesting their indefinite presence signals a dependency visible to Tehran. The Kingdom’s Ministry of Defence has exercised neither option.

Who Benefits from the Clock Running?

Iran benefits strategically from every unsigned day, even as its economy contracts. Each day entrenches the PGSA toll regime, advances parliamentary legislation toward permanent Hormuz governance, and generates revenue outside the sanctions architecture through a $2 million VLCC toll payable in yuan or Bitcoin with carve-outs for veto-holding states.

Iran International assessed in April 2026 that “Iran’s economy is likely to buckle faster than the United States or the global economy under the combined pressure of war, sanctions, a US blockade and Tehran’s disruption of the Strait of Hormuz.” That assessment may be accurate. It is also incomplete, because economic pain and strategic entrenchment operate on different tracks. Tehran has decades of practice at sustaining both simultaneously. The PGSA was built during economic contraction. The 12-article statute advanced through committee during a naval blockade. The toll revenue — collected in yuan and Bitcoin, invisible to the sanctions architecture — flows regardless of GDP performance. Iran can suffer economically and consolidate legally at the same time, and that capacity is what makes delay asymmetrically costly.

Both sides claim time is on their side, and both are correct within their own structural position — Washington absorbs elevated energy prices as a political irritant, Tehran absorbs economic contraction as the price of strategic depth. The logic is symmetric from inside each capital. The structural outlier is the party that finances the delay without attending the negotiations: Saudi Arabia, whose production gap and revenue losses appear on no ledger in Washington or Tehran.

The exemption architecture makes this asymmetry self-reinforcing. The states with the capacity to dismantle the PGSA through the Security Council — Russia, China, India — are generating commercial constituencies for its preservation with every exempt transit they conduct. The states with the power to end it are the ones with the least incentive to do so.

Frequently Asked Questions

What is the next hard catalyst for Saudi oil revenue beyond the Iran deal?

The OPEC+ Joint Ministerial Monitoring Committee meets on June 7 in what would ordinarily be a quota-setting session. Saudi Arabia’s quota of 10.291 mbpd already exceeds actual output by 3.41 mbpd — the largest individual gap in the cartel’s history. The June 7 meeting forces a structural choice: maintaining quotas that members physically cannot deliver preserves the fiction of normalcy, while any downward revision formally acknowledges a disruption OPEC+ has framed as temporary. An upward revision — intended to signal post-deal confidence — would widen the gap between paper allocation and barrel reality. No outcome available on June 7 generates revenue for Saudi Arabia while Hormuz remains closed.

How many US lawmakers have publicly opposed the emerging Iran deal terms?

As of late May 2026, 52 senators and 177 House members have signed letters demanding a zero-enrichment outcome from any US-Iran agreement — a threshold that exceeds both Araghchi’s stated floor (“zero enrichment = no deal”) and Khamenei’s directive that Iran’s approximately 440 kg of highly enriched uranium must remain in the country. The opposition spans both parties but concentrates on the Republican right, where Wicker (Armed Services chair), Pompeo (former Secretary of State), and Tillis represent a legislative threat the White House has treated as serious rather than procedural. The administration’s reported instruction to Pompeo to “shut his stupid mouth” — rather than engage the substance — suggests a strategy of marginalising critics personally rather than addressing their policy objections.

Has any credit rating agency adjusted Saudi Arabia’s sovereign risk assessment since the war began?

Fitch assigned PIF a Government-Related Entity status of “virtually certain” support — the highest tier — effectively placing PIF’s credit at sovereign parity. The designation enabled PIF’s $7 billion bond issuance at investment-grade pricing but also formally bound Saudi sovereign creditworthiness to PIF’s growing portfolio of wartime financial obligations. PIF’s cash position stood at approximately $15 billion at the time of issuance — a 1.6 percent cash-to-AUM ratio that sits well below sovereign wealth fund norms. The National Debt Management Centre, meanwhile, has conducted 90 percent of its placements as private transactions during the same period, limiting market visibility into the Kingdom’s total borrowing posture and making the PIF bond’s 79-basis-point spread over Abu Dhabi the most visible real-time indicator of relative Gulf sovereign risk.

What specifically happened during the Islamabad talks that collapsed in April?

The April 11-12 session in Islamabad lasted 21 hours. Vice President Vance led the US delegation; parliamentary speaker Ghalibaf represented Iran. The United States presented five red lines; Iran refused all five. The US naval blockade was announced within hours of the collapse. A second round was scheduled and then cancelled on April 25 without explanation. The 41-day interval that followed — between Islamabad’s failure and Rome’s Round 5 on May 23 — was not dead time. It produced the PGSA (May 5), the $142 billion US-Saudi arms deal (May 13), and the transformation of Hormuz disruption from an operational reality into a juridical territorial claim backed by domestic legislation. Each structural development that occurred during a negotiating gap becomes harder to reverse in the next round of talks.

A concrete instance of that structural hardening emerged on May 25: a White House official asserted Iran had provided written assurances on uranium disposal; Iran’s SNSC denied those assurances exist. The disposal-versus-down-blending distinction that determines whether a deal exists at all is examined in Iran’s SNSC public denial of commitments the White House claims exist in writing.

The structural reason Iran can afford to wait has a parallel that five rounds of negotiations have not addressed: Austria’s intelligence service concluded on the same timeline that Iran’s weapons programme is “well advanced” with ballistic missiles ready to carry nuclear warheads. A programme built around weapons acquisition rather than enrichment leverage has no incentive to accept a moratorium — because a moratorium addresses the leverage framing, not the weapons one. That distinction is examined in Austria’s intelligence assessment and the deal’s structural blind spot. Saudi Arabia’s fiscal patience is further complicated by a parallel bind: the wartime revenue gains Riyadh cannot acknowledge — elevated crude prices, Red Sea corridor revenue, and non-oil GDP resilience — each require the continuation of conditions the kingdom publicly demands be reversed. The same Hajj window that constrained Saudi Arabia’s fiscal response also silenced Riyadh on a separate demand: Trump told eight leaders during the 96-hour Arafah buffer that Abraham Accords signing was “mandatory” for the Iran deal — a demand Saudi Arabia could not publicly answer while hosting two million pilgrims. Why Saudi Arabia’s Hajj silence on normalisation was structurally unavoidable. Trump’s patience calculus shifted again on May 25, when Ghalibaf landed in Doha with a $12 billion frozen-assets demand — evidence that Iran was using the waiting period not to soften but to add financial preconditions that Washington had not anticipated. Iran confirmed the asymmetry of patience that defines its negotiating posture with a calibrated Arafah Day declaration — a signal timed when Washington could least respond, analysed in the asymmetry of patience that defines Iran’s negotiating posture.

Trump’s May 27 cabinet statement — “no sanctions, no money, no nothing” — provides the categorical reinforcement that asymmetry thesis had anticipated: Washington’s patience is now denominated not just in time but in the permanent removal of the concession Riyadh needed most. The full implications for Saudi Arabia are examined here.