RIYADH — Saudi Arabia posted a $33.5 billion deficit in the first quarter of 2026, burning through 76% of its full-year $44 billion target in 90 days, while Brent crude closed June 28 at $71.99 — a gap of $36–39 per barrel against the $108–111 composite fiscal breakeven Bloomberg Economics calculates when off-balance-sheet Public Investment Fund commitments are included. Through it all, Crown Prince Mohammed bin Salman maintained what may be the most expensive silence in the kingdom’s modern history. His government has offered no strategic statement on IRGC strikes against Bahrain and Kuwait, no position on the first GCC collective defense invocation in the alliance’s 45-year history, and no response to the Geneva-to-Doha venue shift that sidelined the nuclear track Riyadh has the most at stake in. Three fiscal pressures — a deficit overshoot without modern precedent, an oil-price gap the kingdom cannot close by producing its way out, and the industrial shutdown of an entire petrochemical complex at Jubail — have converged on a government that cannot afford to escalate, cannot sustain its current revenue trajectory, and has found every available lever either occupied or removed.

Table of Contents

- The Ninety-Day Overshoot

- How Wide Is the Gap Between Brent and Saudi Arabia’s Breakeven?

- Aramco Is Paying Dividends It Cannot Cover

- What Happens When Sadara Chemical Stays at Zero Revenue?

- The NEOM Bill Nobody Budgeted For

- Why Has MBS Said Nothing About Strikes on GCC Allies?

- Can Saudi Arabia Borrow Its Way Out of the War?

- The Petrostate Precedent Riyadh Doesn’t Want

- The Three-Thread Trap

- Frequently Asked Questions

The Ninety-Day Overshoot

The Saudi Ministry of Finance disclosed in May that the kingdom’s first-quarter deficit reached SAR 125.7 billion — $33.5 billion — the largest quarterly shortfall in its modern fiscal record. The official 2026 budget, published in December 2025 before the Iran war rewrote every assumption underpinning it, projected a full-year deficit of SAR 165 billion ($44 billion). In three months, three-quarters of the annual number was consumed.

The overshoot was not primarily a revenue problem — not yet. The first quarter included January and February, months when Brent still traded well above its current level and Saudi export volumes had not buckled under the Hormuz closure that consolidated in March. The deficit driver was spending. Military expenditure surged 26% year-on-year to SAR 64.7 billion, up from SAR 51.4 billion, as the kingdom scrambled to replenish air defense inventories, sustain readiness across a theater it was not formally fighting in, and absorb the overhead of a conflict whose geography put Saudi desalination plants, power stations, and Aramco processing nodes within range of the same missiles that had already struck allied territory.

Goldman Sachs now projects the full-year 2026 Saudi deficit at $80–90 billion — nearly double the official target — if current oil prices and production volumes hold through December. That estimate was issued before Brent dropped below $72 on June 28 and before WTI fell under $70 for the first time since late February. Those price levels, combined with Saudi production at 6.879 million barrels per day — collapsed from roughly 10 million bpd pre-war — produce what the market has started calling double compression: lower price on lower volume, with neither variable under Saudi control.

The Arab Center Washington DC described the financing mechanism in unambiguous terms: the first-quarter deficit “was financed entirely through debt issuance.” The kingdom did not announce spending cuts, did not disclose reserve drawdowns, and did not revise a single Vision 2030 timeline. It borrowed, and it said nothing about what comes next.

How Wide Is the Gap Between Brent and Saudi Arabia’s Breakeven?

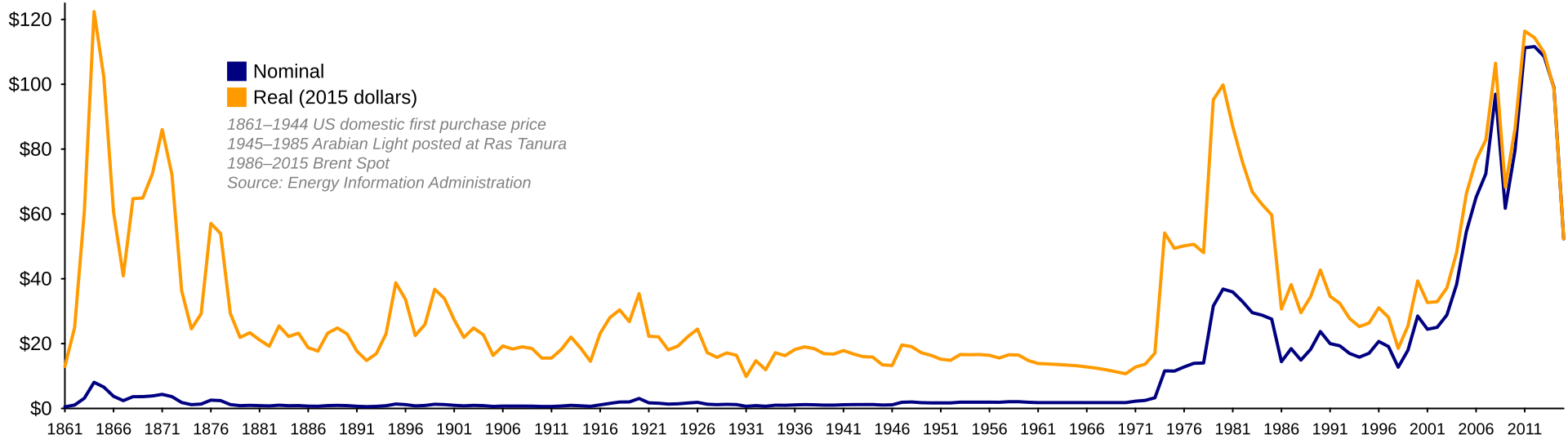

The IMF’s on-budget fiscal breakeven — the oil price Saudi Arabia needs to balance its official government accounts — sits at roughly $86–96 per barrel, based on the Fund’s 2026 Article IV consultation. Bloomberg Economics’ composite figure, which folds in off-balance-sheet PIF commitments including NEOM, The Line, and accumulated sovereign fund debt service, reaches $108–111. Against Brent’s June 28 close of $71.99, the gap runs from $14 per barrel at the narrowest to $39 at the widest — costing Saudi Arabia roughly $160–175 million in foregone revenue every day.

The Middle East briefing 3,000+ readers start their day with.

One email. Every weekday morning. Free.

The distinction between those two breakevens tells a story about how Saudi Arabia accounts for its own ambitions. The official budget captures government operating expenditure and capital investment routed through the Ministry of Finance. It does not capture PIF’s debt service, NEOM’s contractor termination liabilities, Aramco’s backstop obligations on Sadara’s $3.7 billion in guaranteed debt, or the kingdom’s implied commitment to the $300 billion development fund announced under the MOU’s Section 6 framework. Bloomberg’s composite breakeven captures all of it, and the resulting $108–111 figure represents the actual price Saudi Arabia needs to sustain its commitments — not just the ones that appear on the sovereign balance sheet.

Since the MOU’s 60-day Phase 2 clock started on June 17, the kingdom has accumulated more than $1.9 billion in shortfall against its composite breakeven, and the Strait of Hormuz remains under Iranian pre-clearance control through the PGSA mechanism the MOU preserved rather than dissolved. The revenue clock runs whether or not Saudi Arabia’s diplomats speak, and it compounds in their silence.

The IMF’s Article IV mission to Riyadh, conducted April 28 through May 13, introduced a formulation that received less attention than the deficit data. The Fund conditioned Saudi Arabia’s projected 2% GDP recovery on Hormuz normalization — the first time it has made a Gulf state’s growth forecast explicitly contingent on a waterway under adversary control. The Fund’s Middle East director told Arab News that Saudi Arabia possessed “strong financial buffers to confront Iran war impact,” but the Fund’s own methodology told a different story: Saudi fiscal trajectory was no longer a domestic policy variable but a function of decisions being made in Tehran.

| Metric | Target / Pre-War | Actual / Current | Source |

|---|---|---|---|

| 2026 full-year deficit | $44 billion | $80–90 billion (projected) | Saudi MoF / Goldman Sachs |

| Q1 2026 deficit | $11 billion (quarterly run-rate) | $33.5 billion | Saudi MoF / Bloomberg |

| Fiscal breakeven (composite) | $108–111/bbl | Brent: $71.99/bbl | Bloomberg Economics |

| Crude production | ~10 million bpd | 6.879 million bpd | Aramco Q1 2026 |

| Aramco FCF vs. base dividend | $21.9 billion (quarterly) | $18.6 billion (0.85x) | Aramco Q1 2026 |

| Sadara revenue | Operating | Zero (78+ consecutive days) | Tadawul filing |

| Total public debt | — | $445 billion (33% of GDP) | Arab Center / Saudi MoF |

| Military spending (Q1 YoY) | SAR 51.4 billion | SAR 64.7 billion (+26%) | Saudi MoF |

Aramco Is Paying Dividends It Cannot Cover

Aramco reported Q1 2026 free cash flow of $18.6 billion against a quarterly base dividend obligation of $21.9 billion — a coverage ratio of 0.85x. The company was not generating enough cash to pay its shareholders, and its shareholders are, in practical terms, the Saudi government. The state’s 98.5% stake makes Aramco’s dividend the single largest line item in the kingdom’s revenue structure, and for the first time in the company’s listed history, the contractual floor — not a performance bonus, not a special distribution — required Aramco to draw on its balance sheet to fund the payment.

The dividend coverage ratio was calculated at May spot prices. By July, Aramco’s July Official Selling Price to Asia had fallen a further $6 per barrel — the pricing gap that Ras Tanura’s restart could not fix — compressing the revenue per exported barrel at the same moment the kingdom needed every dollar of oil income to service deficit financing that the Arab Center described as funded entirely through new debt.

The arithmetic at current prices is unforgiving. At $72 Brent and the production volumes detailed above, Aramco generates roughly $18–19 billion in quarterly free cash flow before capital expenditure revisions. The base dividend runs at $87.6 billion annually. Every quarter that Brent stays below roughly $80, Aramco either borrows to pay the dividend, sells assets, or cuts — and cutting the dividend means cutting the sovereign budget, which means cutting the programs MBS has staked his domestic legitimacy on.

Saudi crude exports through the Strait of Hormuz fell from roughly 7 million barrels per day pre-war to approximately 4 million during the blockade’s peak. The East-West Pipeline to Yanbu — the kingdom’s only overland bypass — reached full throughput capacity in Q1 and cannot fully substitute for the lost Hormuz volumes. Eight million barrels loaded at Ras Tanura in late June could not move without navigating the PGSA pre-clearance regime or securing escort capacity that CENTCOM has not provided and Saudi Arabia has not requested — two silences, operational and diplomatic, running in parallel.

What Happens When Sadara Chemical Stays at Zero Revenue?

Sadara Chemical Company’s 26 manufacturing units at Jubail have been offline since March 31, producing zero revenue for 78 consecutive days, while $3.7 billion in guaranteed senior debt remains on its books. Dow Chemical has already booked a $292 million EBIT charge against its Q1 earnings — its actuarial assessment that the debt guarantee will be called. Aramco, which backstops 65% of the obligation at roughly $2.405 billion, has disclosed no equivalent provision.

The Tadawul regulatory filing Sadara submitted is written in the sterile language of securities disclosure, but its content is extraordinary. The company stated that it “cannot provide, at the present time, an estimate for the return to production” — a listed entity on the Saudi exchange placing on the public record that it does not know when it will earn revenue again. The filing language is boilerplate in format and without precedent in substance. Dow’s $292 million charge suggests the American partner has made its own calculation about the timeline and concluded that the guarantee exposure is no longer theoretical.

Sadara is not an isolated failure. SABIC, the kingdom’s listed petrochemical flagship, filed its own Tadawul disclosure on April 8, warning of “material impact to 2026 financial results” — the first listed Saudi company to place legally binding war-damage uncertainty on the public record. Five SABIC product lines, including MMA, MEG, and methanol, were placed under force majeure. Together, Sadara’s shutdown and SABIC’s force majeure represent the largest simultaneous disruption to Saudi Arabia’s non-oil industrial base since those facilities were built.

The Chatham House assessment of March 2026 identified what this means for the broader project. The Hormuz closure, it concluded, had exposed a “key threat to Saudi Arabia’s Vision 2030 strategy and plans for economic transformation.” The petrochemical sector at Jubail was constructed specifically to reduce Saudi dependence on crude exports — the hedge against the commodity cycle that has governed the kingdom’s fiscal life for seven decades. The hedge and the asset it was supposed to protect against have now been hit by the same event, and neither is generating the revenue it was designed to produce.

The NEOM Bill Nobody Budgeted For

The Line — NEOM’s 170-kilometer linear city and the most visible commitment of Vision 2030 — has been formally halted until after 2030. A further 15% capital expenditure reduction sits on top of the $41 billion construction cut announced earlier in the conflict. Total PIF construction spending commitments have dropped from $71 billion to $30 billion, a 58% collapse in the investment vehicle that was supposed to be building Saudi Arabia’s post-oil economy while oil was still paying for it.

The termination costs are where the fiscal damage concentrates. NEOM has earmarked SAR 60 billion — approximately $16 billion — to cover contractor termination liabilities between 2026 and 2030. This is expenditure that produces nothing: no infrastructure, no housing units, no tourism capacity, no jobs. It is the cost of stopping, and it was never included in the National Debt Management Center’s 2026 borrowing program because the 2026 budget was written on the assumption that NEOM would be building, not unwinding contracts with international construction firms whose own balance sheets depend on the payments arriving. PIF’s formal classification of NEOM as an “independent ecosystem” — a restructuring completed before any missile flew — is examined in detail in Al-Rumayyan’s ‘good to have’ verdict on a $64 billion city.

PIF’s own finances reflect the accumulating pressure. Cash reserves fell to roughly $15 billion by late 2024 — the lowest since 2020, according to Bloomberg Intelligence — before the war added a new layer of expenditure obligations the fund had not planned for. PIF has issued approximately $45 billion in international bonds since 2022, with analysts at S&P Global projecting a further $8–12 billion in 2026 issuance. Carnegie Endowment’s analysis — titled “The Iran War Isn’t the Only Challenge Facing Saudi Arabia’s Vision 2030” — captured the compounding dynamic: the war did not create the mismatch between PIF’s investment ambitions and its cash generation, but it removed the oil price environment that had been covering the gap.

Saudi Arabia is now servicing three categories of obligation simultaneously — the debt of projects it is building at reduced scope, the termination costs of projects it is canceling, and the operating losses of projects it completed but cannot run at capacity. All three draw on the same treasury, in the same fiscal year, against the same contracting revenue base. The PIF was designed to earn Saudi Arabia’s future; it has become one of the largest sources of demand on Saudi Arabia’s present.

Why Has MBS Said Nothing About Strikes on GCC Allies?

On June 28, Crown Prince Mohammed bin Salman’s only confirmed public engagement was receiving condolence messages after fourteen Saudi nationals died in an Aramco helicopter crash at Ras Tanura. No statement on the IRGC strikes. No position on the GCC invocation. No response to the Geneva-to-Doha shift.

Foreign Minister Prince Faisal bin Farhan’s record runs parallel. Saudi Arabia’s top diplomat issued no formal public statement on IRGC strikes against GCC member states through June 28 — a silence of at least 14 days. His first documented contact on June 28 was a condolence call from Pakistan’s Foreign Minister Dar regarding the Ras Tanura crash, not the IRGC strikes that had hit allied territory hours earlier. On June 30, rather than engaging any of the active negotiating tracks, Faisal flew to Beijing for talks with Chinese FM Wang Yi — a visit that underscores how Saudi diplomacy is navigating the margins of the crisis rather than its center. The Arab Center Washington DC described the broader diplomatic pattern precisely: Saudi activity “was specifically designed to avoid the kind of diplomatic product — a treaty, a joint statement, a formal position — that would constrain Saudi Arabia’s future options.” The available diplomatic forums — from the Geneva-to-Doha nuclear track to Baghdad’s regional security framework proposal — each demand a position the kingdom has declined to take.

The three-way frozen assets dispute that crystallized on June 30 — Pezeshkian claiming $6 billion agreed, the US denying any release, and Qatar silent on both — is analyzed in a June 30 analysis of the competing Doha narratives, a session Saudi Arabia had no seat at and no mechanism to contest.

Bernard Haykel, professor of Near Eastern Studies at Princeton, identified the risk that makes the silence rational in a March 2026 interview with Bloomberg: “Saudi Arabia is worried that if Trump strikes the energy and electricity infrastructure in Iran, the Iranians still have the capability of striking back and destroying desalination plants, electricity generation plants — the infrastructure of Saudi Arabia.” MBS has watched what the IRGC can reach — Ali Al Salem, Juffair, Al Udeid, Al Dhafra — and the kingdom’s PAC-3 interceptor inventory, estimated at 80 to 400 rounds remaining from an original stock of roughly 2,800, cannot absorb a sustained retaliatory campaign against the civilian infrastructure Haykel described. No confirmed resupply has been announced.

The fiscal and military constraints reinforce each other. A kingdom posting the largest quarterly deficit in its history cannot fund the defense posture that would make a strong diplomatic stance costless, and a kingdom with depleted air defense stocks cannot absorb the retaliatory risk that such a stance might invite. MBS has declined all three G7 bilateral invitations extended directly to him — Italy 2024, Canada 2025, France 2026 — not because he has nothing to say, but because every available setting demands a position that carries a price tag the treasury cannot cover and a military risk the interceptor inventory cannot manage. The Clingendael Institute described the compound condition in the title of its 2026 paper: “The Saudi Economy Amidst War, Competition and Reassessment.” War, competition, and reassessment are not three stages — they are three simultaneous constraints, each narrowing the space in which the next can be addressed.

Can Saudi Arabia Borrow Its Way Out of the War?

The National Debt Management Center pre-sold approximately 90% of its SAR 217 billion ($58 billion) 2026 borrowing program before the Q1 deficit overshoot was known. That program was sized for a $44 billion full-year deficit and the routine rollover of maturing debt. Goldman Sachs now projects the actual deficit at $80–90 billion — a gap the existing borrowing plan cannot cover without substantial new issuance at terms the NDMC did not negotiate.

Saudi Arabia’s total public debt stood at SAR 1.67 trillion, approximately $445 billion, at the end of Q1 — a debt-to-GDP ratio of roughly 33%. By advanced-economy standards, that ratio is conservative; Japan services debt at 260% of GDP, and the United States at 123%. But petrostate debt dynamics operate under different gravity. Saudi Arabia’s revenue base is a single commodity whose price the kingdom influences but does not control, and whose primary export route — the Strait of Hormuz — is under the operational authority of an adversary that has demonstrated willingness to close it. The Arab Center warned that second-quarter results are “expected to be considerably worse if the Strait of Hormuz remains effectively closed,” and the Strait remains under the MOU framework that preserved PGSA pre-clearance rather than dismantling it.

PIF’s borrowing runs on a parallel track that compounds the exposure. The fund’s ~$45 billion in accumulated international bond issuance since 2022, with $8–12 billion more expected this year, is technically off the sovereign balance sheet but functionally sovereign risk: PIF is 100% state-owned, its chairman is MBS, and its liabilities — including the Aramco backstop on Sadara’s $2.4 billion guaranteed debt share — become government liabilities the moment the market questions whether PIF can service them independently. Two entities are borrowing against the same underlying revenue base, and that base is contracting at a rate neither entity’s borrowing plan anticipated.

The Petrostate Precedent Riyadh Doesn’t Want

Venezuela between 2014 and 2016 is the comparison Saudi officials would reject and Saudi fiscal planners cannot afford to ignore. Venezuelan oil revenue collapsed from $94 billion in 2012 to $27 billion by 2016 as crude prices fell from above $100 to under $30 per barrel. The Council on Foreign Relations documented the sequence: “the oil price plunge from more than $100 per barrel in 2014 to under $30 per barrel in early 2016 sent Venezuela into an economic and political spiral.” The first casualty was not the domestic budget — it was foreign policy agency. Petrocaribe subsidies ceased, regional alliance commitments defaulted, and the diplomatic weight Caracas had built through a decade of oil-funded influence evaporated within eighteen months.

Saudi Arabia is not Venezuela, and the editorial distinction matters. The kingdom holds substantially larger financial reserves, maintains investment-grade credit ratings, operates a functional central bank and a competent finance ministry, and possesses the institutional capacity to execute an austerity program if the political will materializes — a capacity Caracas lacked entirely. The Saudi government survived the 2015–2016 fiscal crisis, when the annual deficit reached 367 billion riyals ($97.9 billion) at 15% of GDP, by cutting 2016 spending 14%, eliminating public-sector bonuses, and raising fuel prices between 67% and 133%. That austerity cycle created the political logic for Vision 2030 itself: the diversification promise was explicitly framed as the alternative to permanent dependence on an oil price the kingdom could not set.

But the structural dynamic — revenue collapse outpacing institutional commitments — is the same, and the Venezuelan case demonstrates where it leads when the gap persists. When what a petrostate earns falls below what it has promised faster than the government can bridge the difference through borrowing or reserves, foreign policy contracts before domestic spending does. Foreign policy requires discretionary spending, alliance contributions, and the credibility that comes from financial surplus; domestic obligations are politically irreducible. Saudi Arabia in June 2026 is exhibiting the pattern: diplomatic passivity while Kuwait lifted its force majeure and ramped production at Saudi Arabia’s expense, alliance free-riding while the GCC invoked collective defense without Saudi force deployment, and the absence of any new Saudi initiative on the crisis that is draining the treasury fastest.

The 1986 precedent is older and sharper on domestic sequencing. When OPEC crude fell from $23.29 to $9.85 per barrel between December 1985 and July 1986, Saudi Arabia responded with capital project postponements, subsidy reductions, and a five-month postponement of its national balance sheet publication — a delay that itself told international creditors what the numbers would eventually confirm. The institutional memory of what Saudi planners describe as the “painful experience of the 1985–2000 austerity period” shaped a generation of fiscal policy and helps explain why MBS has not yet announced spending cuts even as the Q1 overshoot consumed three-quarters of the annual target: the political cost of visible austerity, in a kingdom where the social contract runs on state provision, may be higher than the financial cost of borrowing for another quarter.

The Three-Thread Trap

The fiscal compression Saudi Arabia faces in June 2026 is not additive — it is multiplicative. Each thread tightens the others in a loop that has no internal exit. The deficit overshoot accelerates borrowing, which consumes the NDMC capacity that was supposed to fund Vision 2030 commitments, which increases PIF’s standalone borrowing burden, which widens the composite breakeven that measures Saudi Arabia’s true fiscal need, which deepens the gap against $72 Brent, which expands the deficit. Every thread that might offer relief — higher oil prices, Hormuz reopening, a production increase, a diplomatic breakthrough at Geneva or Doha — is controlled by actors other than Saudi Arabia.

Chatham House identified the external dimension in May 2026, writing that the Iran war was reshaping Saudi strategy “from Hormuz and Houthis to the UAE’s OPEC exit” — a reshaping being done to the kingdom rather than by it. The kingdom that built Vision 2030 on the premise of sovereign agency over its own economic trajectory is waiting for Iran to decide whether the Strait reopens, for Washington to decide whether the MOU holds, for the oil market to decide whether demand justifies a recovery from $72, and for its own creditors to decide whether 33% debt-to-GDP at a $72 oil price warrants the same terms as 33% at $90. The Trump administration’s own rhetoric — threatening Iran “will no longer exist” — has introduced escalatory risk that the kingdom’s depleted interceptor stocks cannot absorb and its depleted treasury cannot fund a response to.

The PGSA mechanism is the institutional expression of the trap. The 40-category pre-clearance system survived the MOU and continues to impose costs on Saudi exports whether or not another missile flies. Iran paused the war but kept the tollbooth running, and the tollbooth’s operating costs compound the fiscal damage on a daily cycle. Day 12 of the MOU’s 60-day Phase 2 clock leaves 48 days until the PGSA fee structure reverts to whatever Iran sets unilaterally on Day 61 — a deadline arriving in mid-August, when Saudi Arabia will have posted a second-quarter deficit the Arab Center expects to be “considerably worse” than the first.

PressTV, the Iranian state broadcaster, framed the convergence with characteristic inversion on May 22: “Saudi Vision 2030 in freefall as fiscal woes from US-Israeli war on Iran deepens.” The propaganda is transparent, but the underlying observation — that Saudi Arabia is bearing fiscal costs vastly disproportionate to its role in the conflict — is one that Chatham House, Carnegie, Clingendael, and the Arab Center Washington DC have each reached through independent analysis. On the evening of June 28, as WTI dipped below $70 and the IRGC’s latest strike damage was still being assessed across the Gulf, the Saudi Press Agency published one royal item: MBS had received a condolence call from Pakistan’s foreign minister about a helicopter crash. In the 48 days before the PGSA clock runs out, the kingdom will accumulate roughly $7.7 billion more against its composite breakeven — and a borrowing program sized for a $44 billion deficit will have been spent covering one running nearly twice that.

Frequently Asked Questions

How does Saudi Arabia’s fiscal position compare to other Gulf states under the same Hormuz closure?

Kuwait and the UAE are structurally better positioned. Kuwait entered the war with near-zero sovereign debt and a reserve fund exceeding $700 billion — roughly 500% of GDP — giving it years of fiscal runway even at suppressed oil prices. The UAE’s Abu Dhabi Investment Authority holds an estimated $1 trillion in assets, and its non-oil GDP share exceeds 70%, insulating the federal budget from the commodity shock to a degree Saudi Arabia cannot match. Bahrain is in the worst position of any GCC member, with debt already at 130% of GDP before the conflict; its fiscal survival has become functionally dependent on Saudi support that Riyadh can no longer as easily provide.

What would happen to Saudi Arabia’s debt rating if the Strait remains closed past Day 61?

The Day 61 trigger — when PGSA transit fees revert to an Iran-set rate — would mark the first time Saudi Arabia faces a permanent, unilateral cost on its primary export route with no bilateral mechanism to negotiate it away. Rating agencies have so far treated the crisis as temporary; a Day 61 fee event would shift the scenario from war disruption to structural export cost, which is the kind of category change that precedes a negative outlook placement. The Oman 2020 precedent is instructive: Moody’s moved Oman to junk over 18 months as it became clear that low oil prices were not transitory for that country’s fiscal model. The Saudi trajectory question — not the current level — is what matters to the agencies.

Has Saudi Arabia’s sovereign credit rating been downgraded?

As of June 29, 2026, Saudi Arabia retains investment-grade ratings from all three major agencies — Moody’s at A1, S&P at A/A-1, and Fitch at A+. However, ratings assessments published to date do not fully incorporate the Q1 deficit data, the $80–90 billion full-year trajectory Goldman Sachs projects, or the SAR 60 billion in NEOM termination liabilities that sit off the sovereign balance sheet but represent functionally sovereign exposure through PIF. Rating actions typically lag fiscal deterioration by two to four quarters; the Q2 data, which the Arab Center expects to be considerably worse than Q1, will be the first full test of agency methodology under war conditions.

What is the PGSA and why does it affect Saudi Arabia’s fiscal exposure?

The Persian Gulf Shipping Authority is a pre-clearance regime established by Iran on May 5, 2026 — 43 days before the MOU was signed — requiring vessels transiting the Strait of Hormuz to submit a 40-category registration form covering vessel identity, cargo, destination, and crew nationality. The MOU waived PGSA transit fees for 60 days but did not dissolve the authority, its pre-clearance requirements, or its institutional staffing. At pre-war Saudi export volumes, the PGSA’s cost structure amounts to approximately $5.5 million per day. On Day 61, estimated around mid-August 2026, the fee reverts to whatever rate Iran sets unilaterally — creating a sovereign cost-of-export variable that did not exist before the war and that Saudi Arabia has no bilateral mechanism to negotiate away, since the kingdom holds no seat at the US-Iran table where the MOU was written. The talks that table was supposed to convene in Doha on June 30 were themselves disputed: Iran’s deputy foreign minister publicly denied that any sessions had been scheduled, hours after Trump announced Iran had requested the meeting — a contradiction that left the Doha process, and Saudi Arabia’s exclusion from it, unresolved.

Against that fiscal backdrop, Aramco moved to prevent further Asian customer defection: six million barrels of spot crude sold on three supertankers to South Korea, Japan, and China via the Oman corridor, discounted below the already-reduced OSP. The transaction confirms the corridor is operational but also that Aramco is absorbing a pricing penalty to keep Asia buying: Aramco Sells Six Million Barrels at a Discount to Keep Asia Buying. Iraq’s OPEC exit threat — Baghdad signalling it may abandon the cartel rather than absorb further enforced cuts — adds a new fiscal dimension: Saudi Arabia would be left defending OPEC quotas alone at a breakeven that requires oil prices Hormuz disruption has rendered unreachable, as analysed in Iraq’s OPEC Exit Threat Leaves Saudi Arabia Defending a Cartel Alone.